Antireflective Coating (ARC & BARC) Market Insights

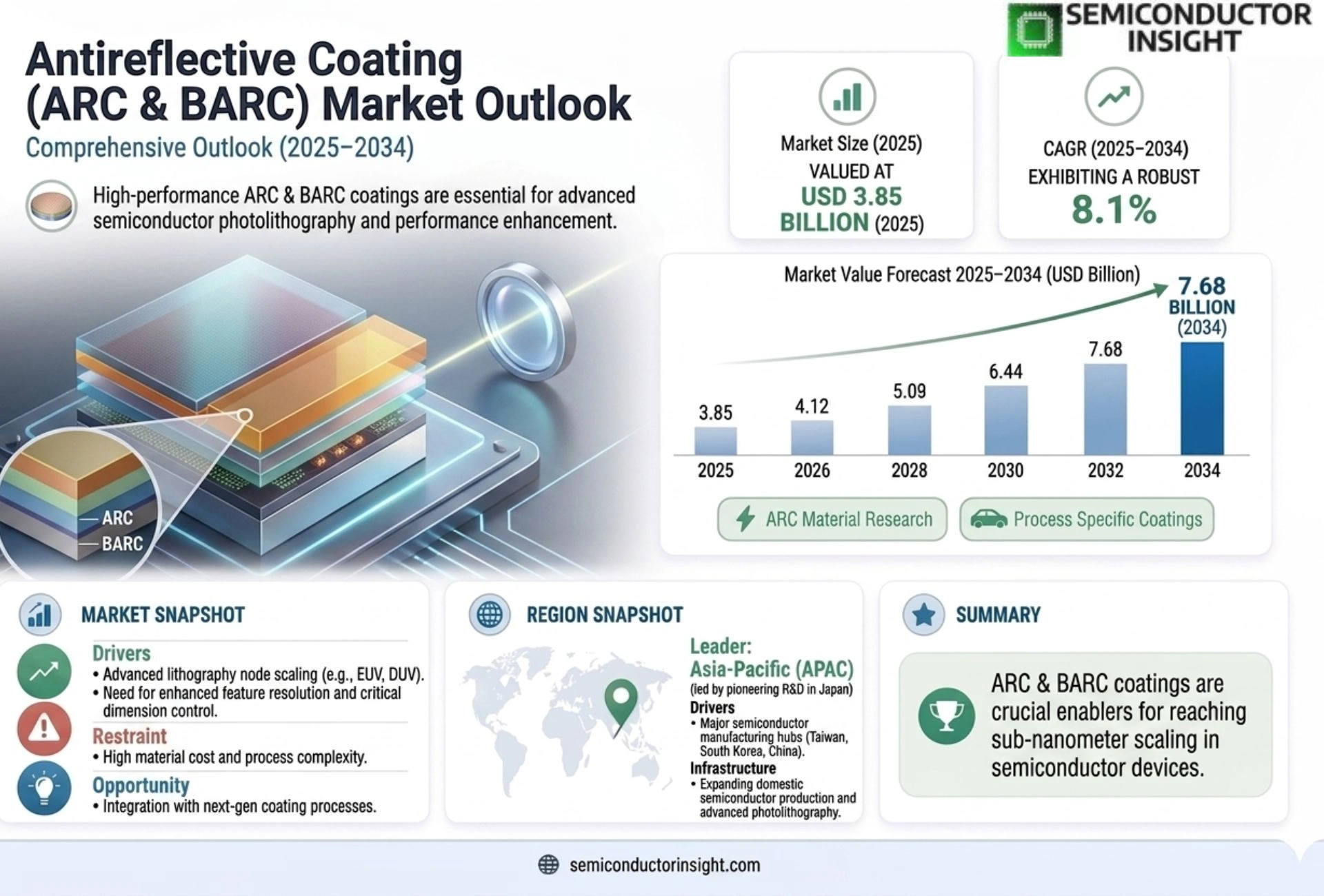

Global Antireflective Coating (ARC & BARC) Market size was valued at USD 3.85 billion in 2025. The market is projected to grow from USD 4.12 billion in 2026 to USD 7.68 billion by 2034, exhibiting a CAGR of 8.1% during the forecast period.

Antireflective coatings, including Anti-Reflective Coatings (ARC) and Bottom Anti-Reflective Coatings (BARC), are thin optical layers applied to surfaces to minimize light reflection and enhance transmission. While ARC primarily reduces surface reflections on lenses, displays, and solar panels, BARC is specifically engineered for semiconductor manufacturing processes, improving lithography precision by suppressing substrate reflections during photoresist exposure. These coatings leverage advanced materials such as magnesium fluoride, silicon dioxide, and organic polymers to achieve optimal refractive index matching and durability across diverse applications.

The market is witnessing robust expansion due to escalating demand for high-performance optical devices, rapid advancements in display technologies, and the proliferation of photovoltaic installations worldwide. Furthermore, stringent regulatory standards mandating energy-efficient solutions in electronics and automotive sectors are accelerating adoption rates. Recent innovations, such as nanostructured ARC designs offering superior broadband performance, are further propelling market growth while addressing challenges related to mechanical stability and environmental resistance.

MARKET DRIVERS

Rising Demand in Semiconductor Manufacturing

Antireflective Coating (ARC & BARC) Market growth is primarily fueled by the exponential increase in global semiconductor fabrication activities. As foundries move toward advanced process nodes, the necessity for minimizing signal loss during photolithography has become paramount. High-throughput lithography equipment requires coatings that can withstand intense exposure cycles while maintaining precise critical dimension control.

Expansion in Photonics Application Sectors

Furthermore, the proliferation of photonic integration systems in telecommunications and data centers is driving demand for high-performance surface treatments. Optical systems demand exceptional clarity and minimal reflectance to maximize data transfer efficiency. Analysts predict that the shift toward 5G and beyond necessitates a surge in optical component manufacturing, thereby boosting the consumption of specialized coatings globally.

➤ Enhanced light transmission rates are critical for achieving optimal device efficiency across Antireflective Coating (ARC & BARC) Market.

This technological evolution ensures that manufacturers prioritize coating solutions that offer superior anti-reflective properties without compromising etch resistance, cementing the market’s upward trajectory in the coming decade.

MARKET CHALLENGES

High Cost of Custom Coating Solutions

Antireflective Coating (ARC & BARC) Market faces persistent challenges related to the high production costs associated with specialized thin-film deposition. Processes such as chemical vapor deposition (CVD) and atomic layer deposition (ALD) require expensive equipment and specialized gases, which can strain the budgets of smaller foundries. These capital intensive requirements often limit the adoption of advanced coating technologies to large-scale industry players.

Other Challenges

Film Adhesion and Durability Issues

Ensuring long-term adhesion of the coating to various substrate materials remains a technical hurdle. Environmental stressors, such as thermal cycling and humidity, can lead to coating delamination if the material properties are not perfectly matched.

Material Compatibility Constraints

Different resist materials and silicon wafer surfaces react variably to coating solutions, making it difficult to develop a “universal” coating type that performs optimally across varied manufacturing environments.

MARKET RESTRAINTS

Material Degradation Over Time

A significant restraint for Antireflective Coating (ARC & BARC) Market is the propensity for optical coatings to degrade under prolonged UV exposure and environmental conditions. As photolithography nodes shrink, the thickness of these coatings becomes critical; any deviation due to wear or environmental impact can lead to a drastic reduction in yield. This necessitates frequent cleaning protocols or re-coating, which adds to operational downtime.

MARKET OPPORTUNITIES

Emerging Applications in Medical Diagnostics

Market analysts identify a significant growth vector in the integration of optical components within the medical device sector. Next-generation endoscopes and imaging equipment require surfaces that virtually eliminate internal reflections to improve imaging clarity. The development of biocompatible ARC solutions for these critical medical applications presents a lucrative opportunity for suppliers looking to diversify their customer base.

Expansion into Emerging Economies

Additionally, the rapid industrialization in countries across Asia-Pacific and Latin America is creating new opportunities for market expansion. As these regions ramp up their local semiconductor fabrication capabilities, the demand for local supply chains of Antireflective Coatings (ARC & BARC) is expected to rise substantially.

Trends

Robust Expansion Driven by High-Performance Optical Demands

Antireflective coatings, encompassing both Anti-Reflective Coatings (ARC) and Bottom Anti-Reflective Coatings (BARC), are sophisticated thin optical layers designed to minimize light reflection while simultaneously enhancing overall transmission rates. The Global Antireflective Coating (ARC & BARC) Market size was valued at USD 3.85 billion in 2025. This significant market is projected to grow from USD 4.12 billion in 2026 to USD 7.68 billion by 2034, indicating a stable upward trajectory. This growth is fueled by the escalating demand for high-performance optical devices and rapid advancements in display technologies across various industries.

Other Trends

Specialization of BARC for Semiconductor Lithography

BARC is strictly engineered for the highly precise environment of semiconductor manufacturing processes. It functions by improving lithography precision and is crucial for suppressing substrate reflections during the critical photoresist exposure stage. To successfully achieve these results across various substrates, these specialized coatings leverage advanced materials such as magnesium fluoride and silicon dioxide, ensuring they provide optimal refractive index matching and superior durability in complex fabrication settings.

Impact of Regulatory Standards on Energy Efficiency

The market is witnessing robust expansion driven by more than just technology; it is the proliferation of photovoltaic installations worldwide. Furthermore, stringent regulatory standards are actively accelerating adoption rates by mandating energy-efficient solutions within the automotive and electronics sectors. Recent innovations, such as nanostructured ARC designs, are further propelling market growth while effectively addressing challenges related to mechanical stability and environmental resistance.

COMPETITIVE LANDSCAPE

Key Industry Players

High-growth trends driven by nanostructures and advanced semiconductor lithography require precise refractive index management to minimize signal loss.

Antireflective Coating (ARC & BARC) Market is characterized by a consolidated landscape featuring global giants specializing in optical materials and semiconductor processing tools. Major manufacturers leverage proprietary formulations to optimize refractive indices, catering to the dual demand for display enhancement and advanced photolithography in semiconductor fabrication. Technology differentiation focuses on broadband performance, durability, and compatibility with environmentally friendly processing chemistries, ensuring sustained growth despite challenges related to mechanical stability.

The competitive dynamics are increasingly influenced by regional supply chain capabilities and custom-engineered solutions for niche substrates. While standard silicon-dioxide and magnesium fluoride solutions dominate bulk applications, competition is intensifying in high-value verticals such as next-generation organic light-emitting diodes (OLEDs) and extreme ultraviolet (EUV) lithography. This segment requires manufacturers to simultaneously address mechanical stability challenges and increasing regulatory pressures regarding green manufacturing processes and energy-efficient solutions.

List of Key Antireflective Coating Companies Profiled

- Shin-Etsu Chemical

- Applied Materials

- JSR Corporation

- DuPont

- Daikin Industries

- Merck Group

- Atotech

- Tokyo Ohka Kogyo

- MacroEx

- Fuzhou King Sci-Tech

- Fujifilm

- Dow

- Henkel

- LG Chem

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Optical Arcs & BARCs: Optimize visual clarity in camera modules and smartphone screens; critical for suppressing photoresist reflections in semiconductor lithography. The shift towards multi-layer ARCs enables better spectral control, enhancing light transmission without compromising durability across diverse substrates. |

| By Application |

|

High-Performance Electronics: Rising demand for ultra-high resolution camera lenses in premium smartphones drives the optical segment. Meanwhile, the solar industry leverages multi-layer solutions to maximize energy conversion efficiency, significantly reducing reflectivity losses on glass surfaces for photovoltaic installations. |

| By End User |

|

Electronics OEMs: Consumer electronics giants are aggressively integrating high-pass light transmission coatings to meet consumer expectations for brighter, sharper displays with higher sunlight readability. Semiconductor fabricators require specialized coatings to achieve micron-level precision during the photolithography process, directly impacting yield rates. |

| By Material |

|

Inorganic Durability: Silicon dioxide and magnesium fluoride offer superior durability, chemical inertness, and thermal stability, making them the preferred choice for harsh environment applications and long-term optical fidelity. Organic polymer coatings provide flexibility and ease of application for curved surfaces but face challenges regarding environmental resistance and long-term stability in outdoor settings. |

| By Technology |

|

Advanced Deposition: PVD techniques are extensively utilized for precise, thin-film deposition required in microelectronics manufacturing, ensuring uniform coverage at the atomic scale for micro-optics. CVD methods are scaling rapidly for large-area coating requirements in the solar and architectural glass sectors, allowing for efficient deposition over vast surfaces without manual intervention. |

Regional Analysis: Global Antireflective Coating (ARC & BARC) Market

Asia-Pacific

The transition to Extreme Ultraviolet lithography technologies in foundries is creating a surge in demand for specialized BARC solutions. This shift requires coatings that can withstand high-energy photons while providing superior etch selectivity, thereby driving innovation in Antireflective Coating (ARC & BARC) Market.

The booming consumer electronics sector in APAC is heavily reliant on visual clarity. Manufacturers are adopting Antireflective Coating (ARC) solutions to minimize glare and maximize light transmission in smartphone and tablet screens, directly contributing to the market’s expansion in this critical sub-segment.

To meet the diverse requirements of local chipmakers, chemical suppliers are increasingly focusing on bespoke Antireflective Coating (ARC & BARC) formulations. Tailoring these solutions to specific wafer chemical compositions ensures improved process optimization, which is a key business strategy in this highly competitive regional market.

Regional analysis indicates a trend toward deep partnerships between material suppliers and foundries. These alliances facilitate rapid technology transfer and co-development, allowing Antireflective Coating (ARC & BARC) Market to respond swiftly to the evolving demands of advanced semiconductor fabrication.

North America

North America remains a critical hub for high-value applications including defense, aerospace, and advanced photonics. The region emphasizes R&D and strategic collaborations, ensuring that Antireflective Coating (ARC & BARC) Market in this area is driven by technological superiority and innovation in optical performance. While the semiconductor manufacturing landscape is mature, the demand for next-generation coatings that enhance the durability and optical clarity of precision instruments continues to rise. This strategic focus on quality over quantity ensures that investments in Antireflective Coating (ARC & BARC) Market here yield long-term returns, as companies prioritize high-end solutions for specialized industrial needs.

Europe

The European sector is characterized by mature optical infrastructure and a strong automotive sector that requires high-performance glass coatings. Manufacturers here are focusing heavily on the longevity and durability of Antireflective Coating (ARC) products to withstand harsh environmental conditions while maintaining aesthetic appeal. The region’s strategic approach involves integrating sophisticated surface engineering into existing production lines, ensuring that Antireflective Coating (ARC & BARC) Market supports the region’s transition toward cleaner energy-efficient automotive technologies.

South America

This region is witnessing a gradual but steady adoption of ARC technologies primarily within the consumer electronics and healthcare sectors. Antireflective Coating (ARC & BARC) Market in South America is experiencing growth driven by increasing urbanization and a rising middle class eager for better visual experiences in devices. As infrastructure develops, there is a growing recognition of the performance benefits offered by advanced optical coatings, which are slowly making their way into standard retail products and industrial equipment.

Middle East & Africa

Emerging markets in this region are focusing on infrastructure development and construction-related optical solutions. This creates a niche but growing demand for Antireflective Coating (ARC) solutions that can reduce glare and improve energy efficiency in large-scale architectural projects. Although Antireflective Coating (ARC & BARC) Market in the Middle East and Africa represents a smaller fraction of the global total, it is becoming increasingly important for international suppliers looking to diversify their geographical presence and explore new revenue streams in developing economies.

Report Scope

This market research report provides a comprehensive analysis of the Antireflective Coating (ARC & BARC) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Antireflective Coating (ARC & BARC) Market?

-> The Global Antireflective Coating (ARC & BARC) Market was valued at USD 3.85 billion in 2025 and is expected to reach USD 7.68 billion by 2034, exhibiting a CAGR of 8.1%.

Which key companies operate in Antireflective Coating (ARC & BARC) Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include escalating demand for high-performance optical devices, rapid advancements in display technologies, and proliferation of photovoltaic installations.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include nanostructured ARC designs offering superior broadband performance, mechanical stability, and environmental resistance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...