Wi-Fi 6E (6 GHz) Access Point Chipset Market Insights

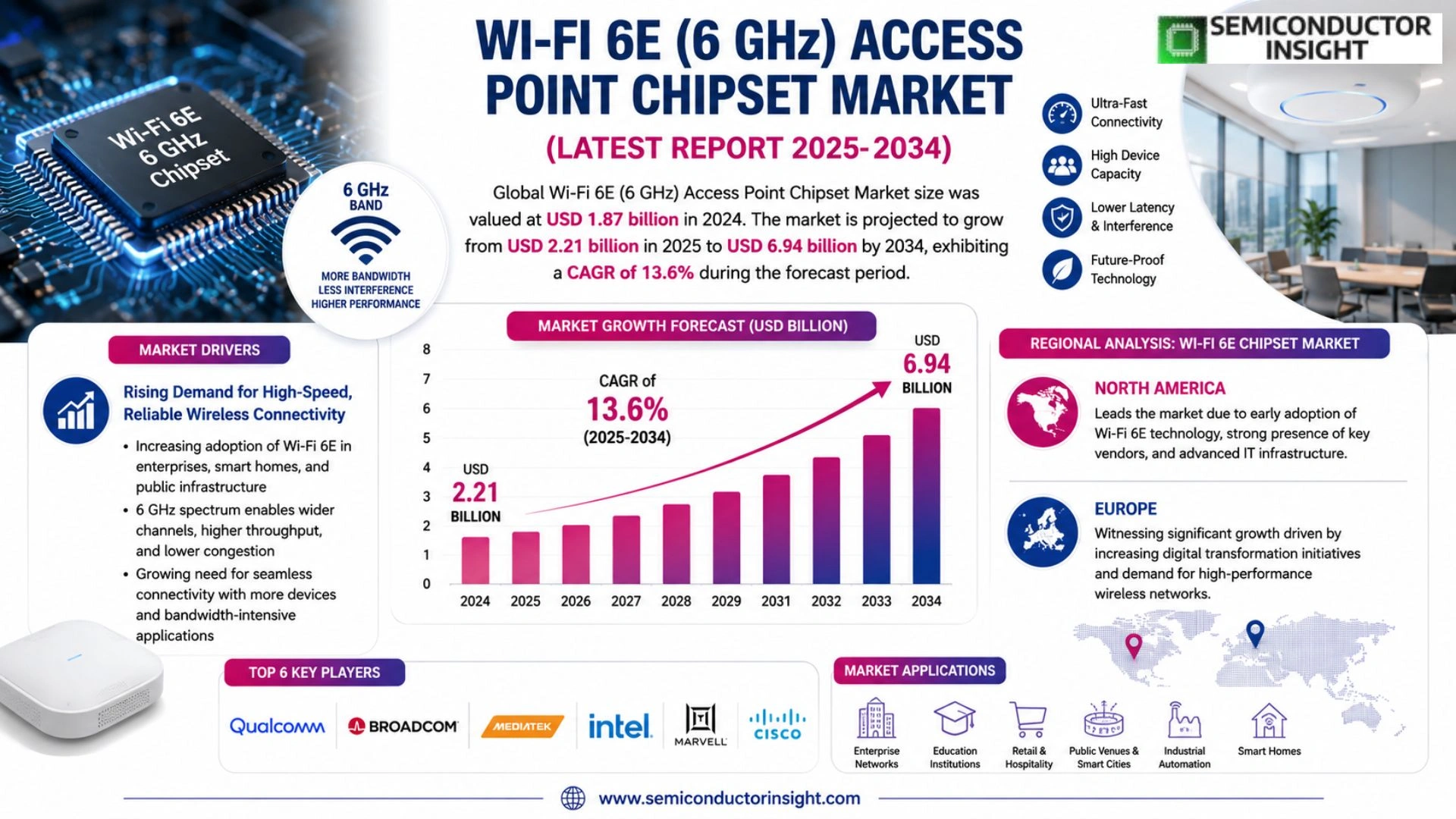

Wi-Fi 6E (6 GHz) Access Point Chipset Market size was valued at USD 1.87 billion in 2024. The market is projected to grow from USD 2.21 billion in 2025 to USD 6.94 billion by 2034, exhibiting a CAGR of 13.6% during the forecast period.

Wi-Fi 6E (6 GHz) access point chipsets are advanced semiconductor components that enable wireless networking devices to operate across the newly opened 6 GHz frequency band, in addition to the traditional 2.4 GHz and 5 GHz bands. These chipsets support the IEEE 802.11ax standard extended to the 6 GHz spectrum, delivering significantly higher throughput, reduced latency, and improved network efficiency. The chipset category encompasses tri-band and multi-band solutions, integrated radio frequency (RF) modules, baseband processors, and system-on-chip (SoC) architectures designed for enterprise, residential, and industrial access point deployments.

The market is witnessing strong momentum driven by the accelerating global rollout of Wi-Fi 6E-certified infrastructure, surging demand for high-density wireless connectivity in enterprise environments, and rapid adoption of bandwidth-intensive applications such as 4K/8K video streaming, augmented reality (AR), and cloud computing. Furthermore, regulatory approvals of the 6 GHz band across major economies , including the United States, European Union, Brazil, South Korea, and Saudi Arabia , have substantially broadened the addressable market. Key industry participants actively shaping the competitive landscape include Qualcomm Technologies, Inc., Broadcom Inc., and MediaTek Inc., each offering a broad portfolio of Wi-Fi 6E chipset solutions targeting diverse access point applications.

MARKET DRIVERS

Surging Demand for High-Speed Wireless Connectivity Fueling Wi-Fi 6E Access Point Chipset Adoption

The rapid proliferation of bandwidth-intensive applications , including 4K/8K video streaming, cloud gaming, augmented reality, and enterprise collaboration platforms , has created an urgent need for wireless infrastructure capable of delivering consistent, low-latency throughput. Wi-Fi 6E (6 GHz) Access Point Chipset Market is directly benefiting from this transition, as chipset manufacturers develop solutions that leverage the newly unlocked 6 GHz spectrum band to deliver multi-gigabit speeds with significantly reduced congestion. Unlike the crowded 2.4 GHz and 5 GHz bands, the 6 GHz band offers up to 1,200 MHz of additional spectrum in regions where regulators have approved its use, enabling access point chipsets to support wider channels and higher data throughput without interference from legacy devices.

Regulatory Approvals Across Key Markets Accelerating 6 GHz Spectrum Deployment

Regulatory support has emerged as one of the most consequential drivers for Wi-Fi 6E (6 GHz) Access Point Chipset Market. The United States Federal Communications Commission (FCC) opened the 6 GHz band for unlicensed use in 2020, and this decision set a global precedent. Subsequently, regulators in the European Union, United Kingdom, Brazil, Saudi Arabia, South Korea, and Chile have approved varying degrees of 6 GHz spectrum access for Wi-Fi use. This expanding regulatory landscape is incentivizing chipset vendors to invest heavily in 6 GHz-capable silicon, as enterprises and service providers in newly approved markets move quickly to upgrade their wireless infrastructure. The growing international alignment on 6 GHz spectrum policy is strengthening supply chain confidence and enabling chipset manufacturers to pursue economies of scale.

➤ The global regulatory push to unlock the 6 GHz band for unlicensed Wi-Fi use is creating a synchronized demand cycle across enterprise, hospitality, healthcare, and public venue segments , positioning Wi-Fi 6E access point chipset suppliers at the center of a multi-year infrastructure upgrade wave.

The enterprise sector, in particular, is driving substantial chipset procurement as organizations seek to support dense device environments, including IoT endpoints, employee mobile devices, and wireless-first office architectures. Chipset vendors are responding with tri-band and multi-link operation (MLO)-capable designs that can simultaneously manage traffic across 2.4 GHz, 5 GHz, and 6 GHz bands. This technological advancement is broadening the addressable market for Wi-Fi 6E access point chipsets, with commercial deployments increasingly replacing older Wi-Fi 5 (802.11ac) infrastructure ahead of schedule.

MARKET CHALLENGES

Interoperability Complexity and Device Ecosystem Fragmentation Constraining Uniform Market Growth

Despite strong growth momentum, Wi-Fi 6E (6 GHz) Access Point Chipset Market faces notable challenges related to device ecosystem maturity. While access point chipset availability has improved significantly, the base of Wi-Fi 6E-capable client devices , including smartphones, laptops, and IoT endpoints , remains smaller relative to the installed base of Wi-Fi 5 and Wi-Fi 6 (5 GHz) devices. This asymmetry means that enterprises deploying 6 GHz access points may not immediately realize the full performance benefits of the technology, complicating ROI justification for some procurement decision-makers. Chipset vendors must therefore articulate a clear forward-looking value proposition that accounts for the gradual client device upgrade cycle, which typically spans three to five years in enterprise environments.

Other Challenges

Coexistence with Incumbent 6 GHz License Holders

In many jurisdictions, the 6 GHz band is shared with incumbent licensed users such as fixed microwave backhaul operators and broadcast auxiliary services. Access point chipsets deployed in standard-power outdoor configurations must incorporate Automated Frequency Coordination (AFC) mechanisms to prevent interference with these incumbents. The technical and compliance complexity of AFC integration adds to chipset development costs and may delay time-to-market for certain product categories, particularly those targeting outdoor and campus-wide deployments.

Higher Bill-of-Materials Costs Impacting SMB and Consumer Segment Penetration

Tri-band Wi-Fi 6E access point chipsets carry a higher bill-of-materials (BOM) cost compared to dual-band Wi-Fi 6 alternatives. While large enterprises and service providers can absorb these premiums, small and medium-sized businesses (SMBs) and cost-sensitive consumer markets may defer upgrades. Chipset manufacturers and access point OEMs are actively working to reduce per-unit costs through process node transitions and increased production volumes, but meaningful price parity with legacy chipsets is expected to take additional time to materialize across all market tiers.

MARKET RESTRAINTS

Uneven Global Regulatory Harmonization Limiting Uniform Market Expansion

One of the most significant structural restraints facing Wi-Fi 6E (6 GHz) Access Point Chipset Market is the lack of uniform global regulatory approval for 6 GHz spectrum access. While the United States, European Union, and several other markets have moved forward with 6 GHz unlicensed allocations, major economies including China, India, and Japan have not yet fully approved 6 GHz Wi-Fi access under the same parameters. This regulatory fragmentation forces chipset vendors to maintain region-specific product variants, increasing design complexity, certification overhead, and inventory management challenges. Until major Asia-Pacific markets align on 6 GHz spectrum policy, global chipset deployment volumes will remain constrained relative to the technology’s full potential.

Infrastructure Investment Cycles and Enterprise Budget Constraints Slowing Replacement Rates

Enterprise wireless infrastructure operates on defined refresh cycles, typically ranging from five to seven years for access points. Organizations that upgraded to Wi-Fi 6 (802.11ax) on the 5 GHz band in recent years may be reluctant to undertake an immediate additional capital expenditure for Wi-Fi 6E access point hardware, even where the 6 GHz performance benefits are well understood. This upgrade fatigue, compounded by macroeconomic pressures on IT budgets in certain sectors, is moderating the pace of Wi-Fi 6E access point chipset adoption in established enterprise markets. Chipset vendors and their OEM partners are responding by emphasizing total cost of ownership (TCO) benefits and the long-term scalability advantages of 6 GHz-capable infrastructure to accelerate purchasing decisions.

MARKET OPPORTUNITIES

Wi-Fi 6E Chipset Integration in Next-Generation Smart Building and Industrial IoT Applications

The convergence of wireless connectivity with smart building management systems, industrial automation, and private network deployments is opening substantial new addressable markets for Wi-Fi 6E (6 GHz) access point chipset suppliers. Facilities deploying dense sensor networks, real-time location systems (RTLS), and machine-vision platforms require the combination of high throughput, low latency, and deterministic performance that 6 GHz chipsets are uniquely positioned to deliver. As smart building certifications and energy efficiency mandates drive infrastructure modernization across commercial real estate, healthcare campuses, and manufacturing environments, demand for Wi-Fi 6E access point chipsets embedded in purpose-built industrial access points is expected to grow significantly through the latter half of this decade.

Service Provider and Carrier Wi-Fi Deployments Creating Large-Scale Chipset Volume Opportunities

Telecommunications service providers and cable operators are increasingly incorporating Wi-Fi 6E access point hardware into their residential gateway and managed enterprise Wi-Fi service portfolios. The ability to offload mobile data traffic onto 6 GHz Wi-Fi while delivering guaranteed quality-of-service to subscribers represents a compelling use case for carrier-grade Wi-Fi 6E chipsets. As service providers roll out next-generation CPE (customer premises equipment) and managed Wi-Fi platforms at scale, chipset vendors with proven 6 GHz silicon capable of meeting carrier certification requirements stand to capture significant volume contracts. This opportunity is further amplified by the ongoing transition to Wi-Fi 7 (802.11be), which builds upon the 6 GHz foundation established by Wi-Fi 6E, incentivizing early investment in 6 GHz chipset ecosystems as a strategic platform for multi-generational product roadmaps Wi-Fi 6E (6 GHz) Access Point Chipset Market.

Trends

Accelerating Global Regulatory Approvals Driving Wi-Fi 6E Chipset Adoption

One of the most defining trends shaping Wi-Fi 6E (6 GHz) Access Point Chipset Market is the rapid expansion of regulatory approvals across major economies. Governments and spectrum regulators in the United States, European Union, Brazil, South Korea, and Saudi Arabia have progressively opened the 6 GHz frequency band for unlicensed Wi-Fi use. This regulatory momentum has significantly widened the addressable market for access point chipset manufacturers, enabling chipset developers such as Qualcomm Technologies, Inc., Broadcom Inc., and MediaTek Inc. to introduce tri-band and multi-band solutions optimized for global deployment. As more jurisdictions formalize their 6 GHz spectrum policies, demand for IEEE 802.11ax-compliant chipsets continues to gain considerable traction across enterprise, residential, and industrial access point segments.

Other Trends

Rising Enterprise Demand for High-Density Wireless Connectivity

Enterprises are increasingly prioritizing high-performance wireless infrastructure capable of supporting dense device environments without compromising throughput or latency. Wi-Fi 6E (6 GHz) Access Point Chipset Market is benefiting directly from this shift, as organizations deploy 6 GHz-capable access points in offices, hospitals, universities, and manufacturing facilities. The 6 GHz band’s wider channel widths and reduced interference characteristics make it particularly well-suited for high-density deployments, reinforcing chipset adoption across commercial verticals. System-on-chip (SoC) architectures and integrated RF modules tailored for enterprise-grade access points are witnessing growing procurement activity as a result.

Surge in Bandwidth-Intensive Application Usage

The proliferation of bandwidth-intensive applications , including 4K and 8K video streaming, augmented reality (AR), and cloud computing , is creating sustained pressure on existing wireless network infrastructure. This usage trend is directly accelerating the transition toward Wi-Fi 6E-enabled access points, as the 6 GHz spectrum delivers substantially higher throughput and significantly lower latency compared to legacy 2.4 GHz and 5 GHz bands. Chipset vendors are responding by developing advanced baseband processors and multi-band chipset solutions capable of handling the escalating data demands of modern connected environments, further reinforcing momentum Wi-Fi 6E (6 GHz) Access Point Chipset Market.

Competitive Innovation Among Leading Chipset Manufacturers

The competitive landscape of Wi-Fi 6E (6 GHz) Access Point Chipset Market is characterized by active product innovation and portfolio expansion among key industry participants. Qualcomm Technologies, Broadcom, and MediaTek continue to invest in next-generation chipset architectures that enhance spectral efficiency, power optimization, and multi-band integration. These advancements are enabling access point manufacturers to deliver solutions that meet the evolving performance expectations of both enterprise and residential end users. As the global rollout of Wi-Fi 6E-certified infrastructure accelerates, chipset providers are expected to sustain their focus on delivering differentiated silicon solutions that address the full spectrum of access point deployment requirements.

COMPETITIVE LANDSCAPE

Key Industry Players

Wi-Fi 6E (6 GHz) Access Point Chipset Market: Competitive Dynamics and Leading Innovators

The global Wi-Fi 6E (6 GHz) access point chipset market is defined by intense technological competition among a concentrated group of semiconductor powerhouses. Qualcomm Technologies, Inc. holds a commanding presence in the space, leveraging its Networking Pro series chipsets , including the Networking Pro 1210 and Networking Pro 820 platforms , to address both enterprise-grade and residential access point deployments. These SoC solutions deliver tri-band and multi-band functionality across the 2.4 GHz, 5 GHz, and newly opened 6 GHz spectrum, positioning Qualcomm as the dominant supplier for major OEM and ODM access point manufacturers globally. Broadcom Inc. closely rivals Qualcomm with its BCM6710 and BCM43 series chipset families, offering high-throughput, low-latency solutions optimized for dense enterprise wireless environments. MediaTek Inc. has similarly strengthened its competitive standing through its Filogic 880 and Filogic 830 chipset platforms, targeting cost-sensitive yet performance-demanding segments in both consumer and commercial access point markets. With regulatory approvals across the United States, European Union, Brazil, South Korea, and Saudi Arabia accelerating infrastructure deployments, these three players collectively shape the market’s technological and commercial trajectory as the market grows from USD 2.21 billion in 2025 toward USD 6.94 billion by 2034 at a CAGR of 13.6%.

Beyond the tier-one leaders, several specialized and emerging players are carving out meaningful positions within the Wi-Fi 6E access point chipset ecosystem. Intel Corporation contributes through its Wi-Fi 6E-capable silicon integrated into access point reference designs, while Celeno Communications , now part of Renesas Electronics , brings differentiated beamforming and interference mitigation technologies suited for high-density deployments. Marvell Technology continues to serve carrier-grade and enterprise segments with its OCTEON Fusion and 88W9064 chipset offerings, and ON Semiconductor addresses power-efficient chipset architectures targeting IoT-adjacent access point form factors. Cypress Semiconductor, operating under Infineon Technologies, maintains relevance in embedded and industrial Wi-Fi 6E chipset applications. As bandwidth-intensive workloads such as 4K/8K video streaming, augmented reality, and cloud computing drive sustained chipset demand, these niche participants are investing heavily in RF integration, multi-link operation support, and advanced MIMO configurations to differentiate their portfolios and capture share in this rapidly expanding market.

List of Key Wi-Fi 6E (6 GHz) Access Point Chipset Companies Profiled

- Qualcomm Technologies, Inc.

- Broadcom Inc.

- MediaTek Inc.

- Intel Corporation

- Marvell Technology, Inc.

- Renesas Electronics Corporation (Celeno Communications)

- Infineon Technologies AG (Cypress Semiconductor)

- ON Semiconductor (onsemi)

- Maxlinear, Inc.

- Atlas Signal Processing Inc.

- Peraso Technologies Inc.

- Realtek Semiconductor Corp.

- NXP Semiconductors N.V.

- Microchip Technology Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Tri-Band Chipsets represent the leading segment within the Wi-Fi 6E access point chipset market, owing to their ability to simultaneously operate across the 2.4 GHz, 5 GHz, and newly opened 6 GHz frequency bands.

|

| By Application |

|

Enterprise Access Points constitute the dominant application segment, driven by the surging demand for robust, high-throughput wireless infrastructure capable of supporting increasingly complex organizational connectivity requirements.

|

| By End User |

|

Commercial End Users lead the Wi-Fi 6E access point chipset market, encompassing a broad spectrum of verticals including corporate enterprises, healthcare organizations, retail chains, hospitality groups, and educational institutions.

|

| By Architecture |

|

Integrated SoC Architecture has emerged as the predominant chipset design paradigm within the Wi-Fi 6E access point market, consolidating baseband processing, radio frequency management, and network processing functions onto a single semiconductor die.

|

| By Deployment Mode |

|

Indoor Deployment represents the leading deployment mode segment for Wi-Fi 6E access point chipsets, reflecting the concentration of high-density wireless connectivity requirements within enclosed environments where the 6 GHz band’s propagation characteristics are most advantageous.

|

Regional Analysis: Wi-Fi 6E (6 GHz) Access Point Chipset Market

North America

North America’s early and comprehensive allocation of the 6 GHz band provides chipset developers with the broadest operational canvas globally. The FCC’s proactive spectrum governance has reduced time-to-market barriers for Wi-Fi 6E access point chipset vendors, enabling faster commercialization cycles that consistently outpace regulatory timelines observed in other major markets worldwide.

Large enterprises across North America are prioritizing Wi-Fi 6E access point chipset deployments to support the surging volume of bandwidth-intensive applications, including video conferencing, cloud-native workloads, and IoT device proliferation. The region’s advanced IT infrastructure and high enterprise capital expenditure cycles continue to stimulate strong chipset procurement activity across verticals.

North America hosts a dense concentration of leading semiconductor design firms actively advancing Wi-Fi 6E chipset architectures. The presence of well-funded R&D centers, fabless chip designers, and strategic partnerships with global foundries ensures a continuous stream of performance improvements in power efficiency, multi-link operation support, and integrated security features within the chipset landscape.

Beyond enterprise deployments, North America’s residential sector presents a compelling demand driver for Wi-Fi 6E access point chipsets. Rising consumer expectations for seamless 4K and 8K streaming, smart home automation, and low-latency gaming are compelling service providers and consumer electronics brands to accelerate the integration of 6 GHz-capable chipsets into next-generation home access point platforms.

Europe

Europe represents the second most significant regional market for Wi-Fi 6E (6 GHz) Access Point Chipset Market, characterized by a measured yet accelerating pace of spectrum harmonization and enterprise adoption. The Electronic Communications Committee and national regulatory authorities across key economies including Germany, France, the United Kingdom, and the Netherlands have progressively granted access to portions of the 6 GHz band, albeit with varying power level restrictions compared to North America. This regulatory differentiation has introduced some complexity for chipset vendors serving the European market, necessitating region-specific product configurations. Nevertheless, Europe’s strong industrial automation sector, smart city initiatives, and digitally progressive enterprise landscape are generating meaningful demand for Wi-Fi 6E access point chipsets. The region’s emphasis on data sovereignty and cybersecurity compliance is also influencing chipset selection criteria, with vendors increasingly required to demonstrate robust security feature sets. As regulatory frameworks continue to converge toward broader spectrum access, Europe is well-positioned to significantly expand its share of the global Wi-Fi 6E (6 GHz) Access Point Chipset Market through the forecast horizon.

Asia-Pacific

Asia-Pacific is emerging as one of the most dynamic and high-potential regions Wi-Fi 6E (6 GHz) Access Point Chipset Market, underpinned by rapid urbanization, expansive digital infrastructure investments, and a growing base of technology-forward enterprises. Countries such as South Korea, Japan, Australia, and Singapore have moved proactively to enable 6 GHz spectrum access, cultivating early adopter markets for Wi-Fi 6E chipset deployment. China, while operating under a distinct regulatory framework with more constrained 6 GHz band allocation, continues to influence the global chipset supply chain through its dominant manufacturing capabilities and deep integration within semiconductor production ecosystems. India presents a particularly compelling long-term opportunity as regulatory bodies advance spectrum policy reforms aligned with national digital infrastructure priorities. The region’s appetite for smart manufacturing, connected healthcare, and next-generation educational facilities is accelerating enterprise procurement of Wi-Fi 6E access point chipsets, making Asia-Pacific a critical growth frontier for market participants through 2034.

South America

South America occupies a developing position within the global Wi-Fi 6E (6 GHz) Access Point Chipset Market, with adoption dynamics shaped primarily by spectrum regulatory progress and macroeconomic conditions across the region. Brazil, as the region’s largest economy and telecommunications market, has taken initial steps toward 6 GHz band authorization, generating early interest among enterprise and service provider segments in Wi-Fi 6E access point chipset solutions. Argentina and Chile are similarly observing regulatory developments, though widespread commercial deployment remains at a nascent stage. Infrastructure investment constraints and foreign exchange volatility present challenges for accelerated chipset market penetration; however, the growing presence of multinational enterprises, expanding hospitality sectors, and government-backed digital connectivity programs are progressively stimulating demand. As spectrum harmonization advances and chipset prices trend downward with scale, South America is expected to transition from an emerging to a more actively growing regional market during the latter phase of the 2026 to 2034 forecast period.

Middle East & Africa

The Middle East and Africa region represents an early-stage yet strategically significant market within the global Wi-Fi 6E (6 GHz) Access Point Chipset Market. Gulf Cooperation Council nations, particularly the United Arab Emirates, Saudi Arabia, and Qatar, are at the forefront of regional adoption, driven by ambitious smart city projects, world-class hospitality infrastructure, and large-scale venue deployments that demand high-density, high-performance wireless connectivity solutions. These markets are increasingly specifying Wi-Fi 6E access point chipsets as a foundational requirement for next-generation network builds aligned with national vision programs. Africa, while presenting a longer-term adoption horizon due to regulatory and infrastructure development timelines, holds considerable potential as mobile broadband expansion and enterprise digitalization initiatives gain momentum. The region’s youthful population, rising smartphone penetration, and growing interest from global technology investors collectively signal that the Middle East and Africa will play an increasingly meaningful role in the evolving Wi-Fi 6E (6 GHz) Access Point Chipset Market landscape by the close of the forecast period.

Report Scope

This market research report provides a comprehensive analysis of the Wi-Fi 6E (6 GHz) Access Point Chipset Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Wi-Fi 6E (6 GHz) Access Point Chipset Market?

-> Global Wi-Fi 6E (6 GHz) Access Point Chipset Market size was valued at USD 1.87 billion in 2024. The market is projected to grow from USD 2.21 billion in 2025 to USD 6.94 billion by 2034, exhibiting a CAGR of 13.6% during the forecast period.

Which key companies operate Wi-Fi 6E (6 GHz) Access Point Chipset Market?

-> Key players include Qualcomm Technologies, Inc., Broadcom Inc., and MediaTek Inc., among others, each offering a broad portfolio of Wi-Fi 6E chipset solutions targeting diverse access point applications.

What are the key growth drivers?

-> Key growth drivers include the accelerating global rollout of Wi-Fi 6E-certified infrastructure, surging demand for high-density wireless connectivity in enterprise environments, rapid adoption of bandwidth-intensive applications such as 4K/8K video streaming, augmented reality (AR), and cloud computing, and regulatory approvals of the 6 GHz band across major economies including the United States, European Union, Brazil, South Korea, and Saudi Arabia.

Which region dominates the market?

-> Asia-Pacific is among the fastest-growing regions driven by rapid digital infrastructure expansion, while North America remains a dominant market supported by early regulatory approvals and widespread enterprise adoption of Wi-Fi 6E technology.

What are the emerging trends?

-> Emerging trends include the expansion of tri-band and multi-band chipset solutions, growing adoption of system-on-chip (SoC) architectures, integration of AI-driven network optimization, and the proliferation of IEEE 802.11ax standard deployments across enterprise, residential, and industrial access point environments leveraging the newly opened 6 GHz frequency spectrum.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...