Solder Resist (LPI, Dry Film) for Substrates Market Insights

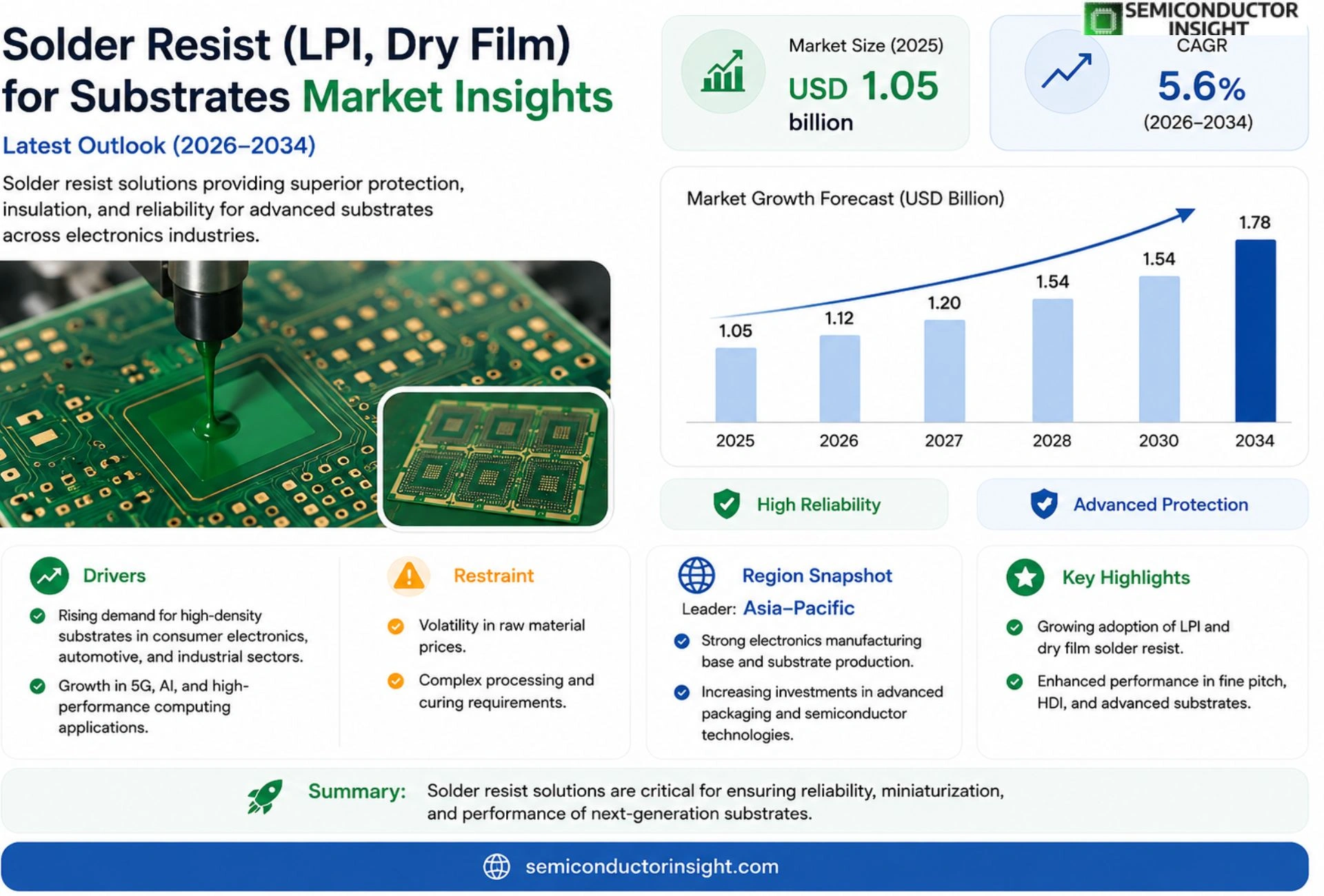

Global Solder Resist (LPI, dry film) For Substrates Market size was valued at USD 1.05 billion in 2025. The market is projected to grow from USD 1.12 billion in 2025 to USD 1.78 billion by 2034, exhibiting a CAGR of approximately 5.6% during the forecast period.

Solder resist materials, including Liquid Photoimageable (LPI) and dry film types, are essential coatings applied to printed circuit board (PCB) substrates to prevent solder bridging and protect circuitry during assembly. These materials provide insulation and enhance the reliability of electronic devices by ensuring precise solder mask application. LPI solder resist is favored for its fine-line resolution and adaptability to complex PCB designs, while dry film solder resist offers advantages in uniform thickness and ease of handling for high-volume production.

The market is witnessing steady growth driven by the expanding electronics manufacturing sector, especially in consumer electronics, automotive, and telecommunications industries. Furthermore, the increasing adoption of advanced PCBs with higher density and miniaturization demands more sophisticated solder resist solutions. However, challenges such as raw material price volatility and stringent environmental regulations on chemical compositions influence market dynamics. Key players continue to innovate by developing eco-friendly and high-performance solder resist materials to meet evolving industry standards and customer requirements.

MARKET DRIVERS

Rising Demand for Advanced PCB Technologies

Solder Resist (LPI, Dry Film) for Substrates Market is being driven by the increasing adoption of advanced printed circuit board (PCB) technologies across various industries such as consumer electronics, automotive, and telecommunications. The superior protective qualities of liquid photoimageable (LPI) and dry film solder resists ensure higher reliability and performance of substrates, which is critical as devices become more compact and complex.

Enhanced Manufacturing Efficiency and Cost-effectiveness

Another key driver is the enhancement in manufacturing processes brought about by the use of LPI and dry film solder resists. These materials provide excellent adhesion and fine-line resolution, facilitating high-precision PCB fabrication and reducing production defects. Consequently, manufacturers can achieve cost savings through reduced rework and increased throughput.

➤ The shift towards miniaturization and multilayer PCB designs significantly fuels demand for high-quality solder resist solutions that ensure substrate integrity and electrical insulation.

Furthermore, environmental regulations promoting the use of lead-free and eco-friendly materials have encouraged the adoption of solder resists that comply with international standards, thus expanding market opportunities.

MARKET CHALLENGES

Complexity in Material Compatibility and Process Integration

Solder Resist (LPI, Dry Film) for Substrates Market faces challenges due to the complexity involved in ensuring material compatibility with diverse substrate types and PCB manufacturing processes. Achieving optimal adhesion, resolution, and thermal resistance requires precise process control, which can hinder widespread adoption among smaller manufacturers lacking advanced capabilities.

Other Challenges

Supply Chain Vulnerabilities

Global disruptions in raw material availability, including specialty photoimageable polymers, can lead to production delays and cost fluctuations, affecting the consistent supply of solder resist materials.

Cost Sensitivity in Emerging Markets

While demand is growing in emerging regions, price sensitivity among local manufacturers limits the adoption rate of premium LPI and dry film solder resists, impacting overall market growth.

MARKET RESTRAINTS

High Initial Investment and Technical Expertise Requirements

The market growth is restrained by the high capital expenditures necessary for integrating advanced solder resist application equipment and the need for skilled operators to manage precision coating and curing processes. Small and medium PCB manufacturers might find these investment thresholds prohibitive, thereby slowing the adoption of LPI and dry film solder resist technologies.

MARKET OPPORTUNITIES

Emergence of IoT and 5G Technologies Driving Demand

The proliferation of Internet of Things (IoT) devices and the rollout of 5G infrastructure present substantial opportunities for Solder Resist (LPI, Dry Film) for Substrates Market. These applications require highly reliable PCBs with enhanced protection, which can be achieved through advanced solder resist materials that support miniaturized and multilayer circuit configurations.

Trends

Growth Driven by Electronics Manufacturing Expansion

Solder Resist (LPI, Dry Film) for Substrates Market continues to expand, fueled primarily by the increasing demand from the electronics manufacturing sector. Industries such as consumer electronics, automotive, and telecommunications are key contributors to this growth. The growing adoption of advanced printed circuit boards (PCBs) with higher density and miniaturization requires more efficient solder resist materials that ensure precision and reliability in soldering processes. Both Liquid Photoimageable (LPI) and dry film solder resist types play critical roles in safeguarding PCB substrates against solder bridging and mechanical damage, which is essential for maintaining the integrity of complex electronic assemblies.

Other Trends

Technological Advancements

Innovation in solder resist formulations is a significant market trend. The industry is witnessing the development of eco-friendly and high-performance solder resist materials that comply with stricter environmental regulations. These advancements focus on improving the fine-line resolution and adaptability of LPI types to accommodate intricate PCB designs, while enhancing the uniform thickness and handling ease offered by dry film variants. Such improvements help manufacturers address the challenges posed by miniaturization and high-density layouts in modern electronic devices.

Market Challenges and Regulatory Impact

Raw material price volatility remains a notable challenge impacting Solder Resist (LPI, Dry Film) for Substrates Market. Additionally, stringent environmental standards related to chemical compositions of solder resist materials are shaping product development strategies. Manufacturers are increasingly prioritizing sustainable and compliant solutions to meet evolving regulatory requirements without compromising performance and reliability.

Innovation and Future Outlook

Looking forward, key market players continue to invest in research and development to create solder resist products that address the dual needs of functionality and environmental responsibility. The demand for solder resist with superior insulation properties and enhanced durability is expected to rise as the complexity of PCB designs intensifies. This focus on innovation, coupled with the robust expansion of the electronics sector, positions Solder Resist (LPI, Dry Film) for Substrates Market to maintain steady growth and meet the nuanced requirements of next-generation electronic applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Market competition and overview of leading Solder Resist (LPI, Dry Film) manufacturers for substrates

Solder Resist (LPI, Dry Film) for Substrates Market is characterized by a blend of global chemical giants and specialized coating manufacturers, ensuring a competitive yet fragmented landscape. The market leadership primarily revolves around companies that have established technical expertise in producing high-quality, reliable solder resist materials that meet stringent industry requirements including fine-line resolution needed for advanced PCBs. Market leaders leverage expansive R&D capabilities and global manufacturing footprints to address growing demand across consumer electronics, automotive, and telecom sectors.

In addition to the dominant players with broad portfolios, several niche companies focus on innovative formulations emphasizing environmental compliance and high-performance materials. These entities contribute significantly to technology advancements in solder resist films, catering to miniaturized and high-density substrates. The competitive dynamics are shaped by continuous product innovation aimed at balancing cost, regulatory adherence, and functional performance while overcoming challenges such as raw material price fluctuations and evolving application needs.

List of Key Solder Resist (LPI, Dry Film) Companies Profiled

- MacDermid Alpha Electronics Solutions

- Huntsman Corporation

- DuPont Electronics & Imaging

- Tokyo Ohka Kogyo Co., Ltd.

- The Matthey Company

- Sumitomo Chemical Co., Ltd.

- Jiangsu Canglong Chemical Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Allresist GmbH

- Keystone Electronics Corporation

- Dream Solder Resist Co., Ltd.

- Evonik Industries AG

- MicroChem Corp.

- Nittobo Co., Ltd.

- Kosei Coatings & Chemicals

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Liquid Photoimageable (LPI) segment is preferred for its ability to achieve fine-line resolution and flexibility in accommodating complex PCB designs, making it suitable for high-precision electronics manufacturing.

Dry Film segment is prominent for its uniform thickness and ease of handling, providing operational efficiency in high-volume production environments.

|

| By Application |

|

Consumer Electronics application dominates due to the increasing demand for miniaturized, high-functionality gadgets requiring precise solder resist application.

Automotive Electronics application is growing steadily as vehicles integrate advanced electronic systems that demand robust PCB protection.

Telecommunications segment benefits from solder resist coatings that ensure reliable circuit protection in dense network hardware.

|

| By End User |

|

Original Equipment Manufacturers (OEMs) prioritize solder resist materials that enhance final product reliability and compliance with regulatory standards.

PCB Manufacturers focus on solder resist types that streamline fabrication processes and maintain consistency across complex PCB designs.

Electronic Manufacturing Services (EMS) Providers seek multifunctional solder resist materials to meet diverse client requirements efficiently.

|

| By Environmental Compliance |

|

Eco-friendly Solder Resists are increasingly prioritized due to rising regulatory pressures and the electronics industry’s commitment to sustainability.

Standard Chemical Solder Resists remain in use where cost-effectiveness and proven reliability are critical.

|

| By Innovation & Performance Features |

|

High Thermal Resistance features are crucial for solder resist materials used in applications exposed to elevated temperatures, ensuring longevity and functionality.

Enhanced Chemical Resistance is essential where PCBs encounter aggressive environments or cleaning processes.

Fine-Line Resolution distinguishes premium solder resist materials, enabling manufacturers to meet demands of increasingly compact and complex PCB layouts.

|

Regional Analysis: Global Solder Resist (LPI, dry film) For Substrates Market

Continuous innovations in photolithographic techniques and polymer chemistry improve the performance and application precision of solder resist films. Asia-Pacific manufacturers focus on enhancing UV-curable formulations that offer better adhesion and fine line resolution essential for next-generation substrates.

Electronics miniaturization and growing automotive electronics requirements spur demand for reliable substrate protection. The expansion of 5G network infrastructure also stimulates the use of advanced solder resist materials to support higher circuit densities and durability.

A dense supplier network, including regional and global chemical corporations, fosters competitive pricing and ensures diverse material availability. Suppliers in Asia-Pacific increasingly invest in R&D to meet stringent environmental and performance criteria.

Compliance with RoHS and REACH regulations shapes product development and market entry in Asia-Pacific. Manufacturers emphasize eco-friendly formulations to align with governmental policies promoting sustainability in electronics manufacturing.

North America

North America maintains a strong presence Solder Resist (LPI, Dry Film) for Substrates Market through its focus on high-reliability applications in aerospace, defense, and automotive sectors. The region’s preference for cutting-edge technologies and stringent quality standards drives adoption of advanced solder resist materials that ensure durability under extreme conditions. Investment in smart manufacturing and Industry 4.0 also enhances production efficiency. However, market growth is moderated by higher production costs and regulatory complexities. Collaborations between material science companies and OEMs facilitate innovation aimed at reducing environmental impact while enhancing material performance.

Europe

Europe’s market for solder resist materials emphasizes sustainability and compliance with rigorous environmental directives. Strong automotive and industrial automation industries spur demand for reliable and environmentally friendly solder resist solutions. European manufacturers prioritize product innovation to achieve lower volatile organic compound emissions without compromising film integrity. The region’s mature market and well-established supply chains support steady demand, though growth is tempered by cautious capital expenditure and economic uncertainties. Strategic partnerships and investment in advanced coatings technology continue to shape the competitive landscape.

South America

South America presents emerging opportunities in the solder resist market driven by increasing industrialization and growth in electronics manufacturing hubs. Brazil and Argentina lead regional demand with expanding automotive and consumer electronics sectors. Challenges include infrastructural limitations and inconsistent regulatory frameworks, but rising local production encourages adoption of both LPI and dry film solder resist technologies. Investment in workforce skill development and supply chain enhancement supports gradual market maturation, with increased focus on cost-effective and versatile solder resist materials suitable for a broad range of substrates.

Middle East & Africa

The Middle East & Africa region remains in a nascent stage of market development for solder resist in substrates, with growth prospects tied to diversification of industrial activities beyond oil and gas. Expansion in electronics assembly and construction of manufacturing facilities drive early demand for quality solder resist coatings. Market participants focus on building awareness and technical capabilities to attract investments. Environmental regulations are evolving, prompting manufacturers to consider compliance early in their product offerings to capture future market share.

Report Scope

This market research report provides a comprehensive analysis of the Solder Resist (LPI, Dry Film) for Substrates Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Solder Resist (LPI, Dry Film) for Substrates Market?

-> Solder Resist (LPI, dry film) For Substrates Market size was valued at USD 1.05 billion in 2025. The market is projected to grow from USD 1.12 billion in 2025 to USD 1.78 billion by 2034, exhibiting a CAGR of approximately 5.6% during the forecast period.

Which key companies operate Solder Resist (LPI, Dry Film) for Substrates Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include the expanding electronics manufacturing sector, particularly in consumer electronics, automotive, and telecommunications industries, along with the increasing adoption of advanced high-density PCBs and miniaturization demands.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by electronics manufacturing growth, while Europe remains a dominant market due to established industrial bases and stringent quality standards.

What are the emerging trends?

-> Emerging trends include development of eco-friendly and high-performance solder resist materials, focusing on sustainability and compliance with stringent environmental regulations, as well as innovations in solder resist formulations for complex PCB designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...