RF Filter (BAW, SAW, IPD) Market Insights

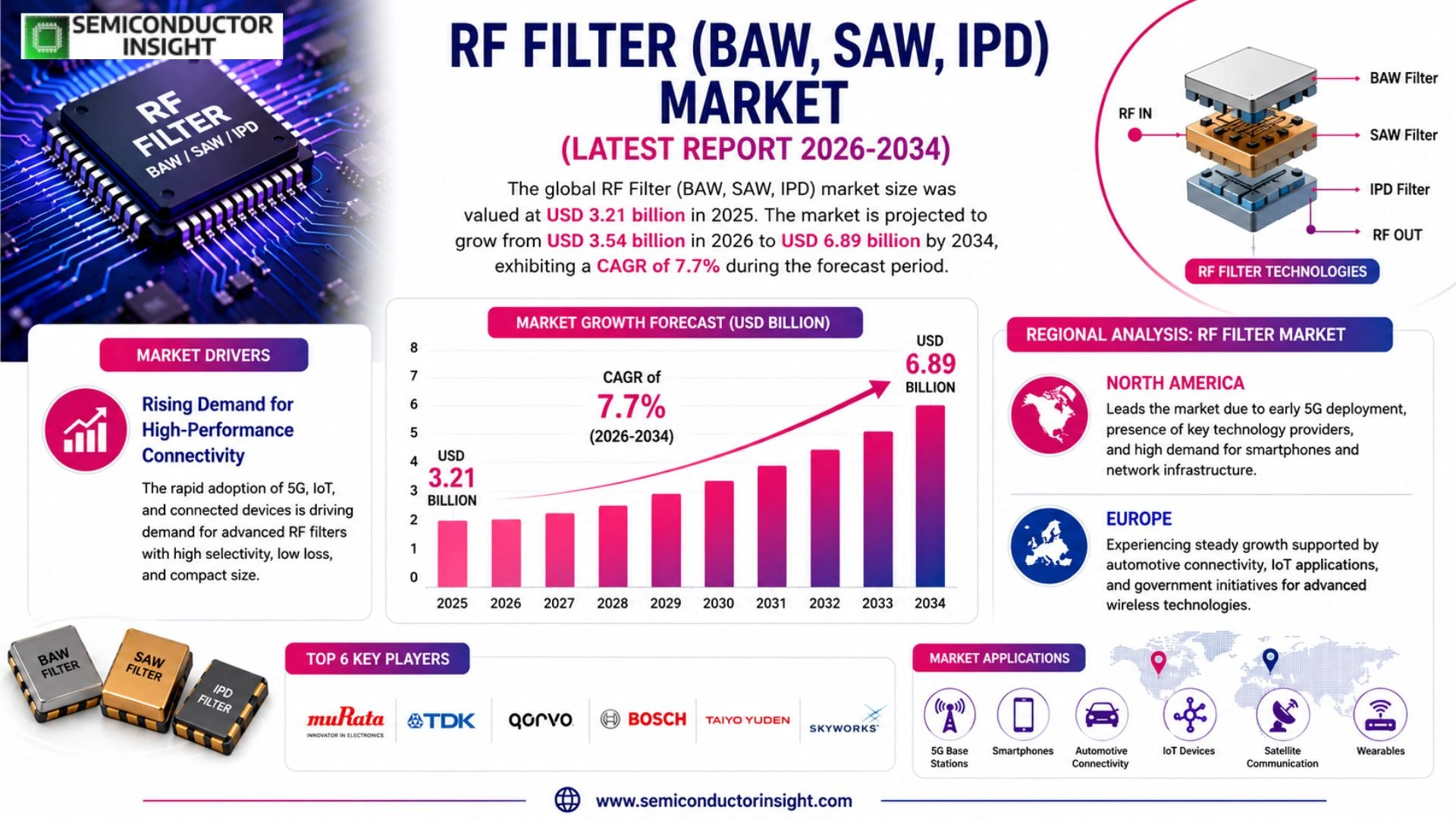

Global RF Filter (BAW, SAW, IPD) Market size was valued at USD 3.21 billion in 2025. The market is projected to grow from USD 3.54 billion in 2026 to USD 6.89 billion by 2034, exhibiting a CAGR of 7.7% during the forecast period.

RF filters , encompassing Bulk Acoustic Wave (BAW), Surface Acoustic Wave (SAW), and Integrated Passive Device (IPD) technologies , are critical components used to select or reject specific frequency bands in wireless communication systems. These filters enable precise signal management by eliminating interference and noise across a wide range of frequencies. BAW filters are particularly valued for their performance at higher frequency bands, SAW filters are widely adopted for their cost efficiency and compact form factor, while IPD-based filters offer superior integration capabilities suited for advanced multi-band and multi-mode devices.

The market is witnessing strong growth momentum driven by the rapid global rollout of 5G networks, the proliferating adoption of smartphones and connected IoT devices, and the increasing complexity of multi-band RF front-end architectures. Furthermore, the growing demand for high-performance filters capable of operating across sub-6 GHz and mmWave frequency bands continues to accelerate technology investment. Key industry participants such as Murata Manufacturing Co., Ltd., Qorvo, Inc., TDK Corporation, Broadcom Inc., and Skyworks Solutions, Inc. maintain significant market presence through continuous product innovation and strategic capacity expansion initiatives.

MARKET DRIVERS

Surging Demand for Advanced Connectivity in Consumer Electronics and Telecommunications

RF Filter (BAW, SAW, IPD) Market is experiencing robust growth driven primarily by the accelerating global rollout of 5G networks and the exponential proliferation of connected devices. Bulk Acoustic Wave (BAW) and Surface Acoustic Wave (SAW) filters are critical components in modern smartphones, base stations, and wireless communication modules, enabling precise frequency selection and signal integrity across increasingly crowded spectrum bands. As mobile network operators continue expanding 5G infrastructure across North America, Europe, and Asia-Pacific, the demand for high-performance RF filters has intensified significantly, with BAW filters particularly favored for their superior performance at higher frequency ranges above 2 GHz.

Expansion of IoT Ecosystems and Smart Device Integration

The rapid expansion of the Internet of Things (IoT) ecosystem is a compelling force propelling RF Filter (BAW, SAW, IPD) Market forward. Billions of connected devices , spanning smart home appliances, industrial sensors, wearables, and automotive telematics , require compact, energy-efficient RF filtering solutions to ensure reliable wireless communication. Integrated Passive Devices (IPD) have emerged as a preferred solution in this segment due to their ability to consolidate multiple passive components into a single miniaturized package, reducing board space and improving overall system performance. The proliferation of Wi-Fi 6, Wi-Fi 6E, and Bluetooth 5.x standards further reinforces the need for advanced RF filters capable of managing multi-band, multi-mode signal environments.

➤ The transition toward 5G-Advanced (5G-A) and early groundwork for 6G research is expected to further elevate the performance benchmarks required of BAW, SAW, and IPD filters, making continuous innovation in filter architecture a critical competitive differentiator in the RF Filter market.

Automotive connectivity represents another high-growth driver withRF Filter (BAW, SAW, IPD) Market. The increasing adoption of vehicle-to-everything (V2X) communication systems, connected navigation, and in-vehicle infotainment platforms demands reliable RF filtering across multiple frequency bands. SAW and BAW filters are being integrated into automotive-grade modules designed to withstand harsh environmental conditions, while meeting stringent electromagnetic compatibility (EMC) standards. As autonomous and semi-autonomous vehicle development accelerates globally, the automotive segment is anticipated to contribute meaningfully to overall RF filter demand in the medium-to-long term.

MARKET CHALLENGES

Technical Complexity in Designing Filters for Multi-Band 5G Spectrum Environments

One of the most pressing challenges confronting RF Filter (BAW, SAW, IPD) Market is the increasing technical complexity involved in designing filters that can effectively operate across the diverse and fragmented spectrum allocations associated with 5G deployment. Globally, 5G networks operate across sub-6 GHz mid-bands, low-band frequencies, and millimeter-wave (mmWave) bands, each presenting distinct filtering requirements. Designing BAW and SAW filters that maintain high selectivity, low insertion loss, and adequate power handling across such a wide and varied frequency landscape requires significant engineering investment, longer development cycles, and advanced manufacturing precision , placing considerable pressure on filter manufacturers to continuously innovate.

Other Challenges

Supply Chain Vulnerabilities and Raw Material Constraints

RF Filter (BAW, SAW, IPD) Market is exposed to supply chain risks stemming from the concentration of specialized raw material production and semiconductor fabrication capacity in specific geographic regions. Piezoelectric materials such as lithium tantalate and lithium niobate, which are essential substrates for SAW filter manufacturing, face periodic supply constraints due to limited global production sources. Geopolitical tensions and trade policy shifts can disrupt the flow of these critical materials, creating cost volatility and potential production bottlenecks for filter manufacturers worldwide.

Intense Price Competition and Commoditization Pressure

RF Filter (BAW, SAW, IPD) Market, particularly in the SAW filter segment serving mid-range and entry-level mobile devices, faces intensifying price competition driven by the entry of low-cost Asian manufacturers and the commoditization of established filter designs. Original equipment manufacturers (OEMs) in the consumer electronics space routinely exert downward pricing pressure on component suppliers, compressing margins and challenging the profitability of filter vendors who lack differentiated, high-performance product portfolios or proprietary manufacturing processes. This dynamic makes sustained R&D investment increasingly critical yet financially challenging for smaller market participants.

MARKET RESTRAINTS

High Capital Investment Requirements and Barriers to Advanced Filter Manufacturing

A significant structural restraint RF Filter (BAW, SAW, IPD) Market is the exceptionally high capital expenditure required to establish and maintain competitive BAW and IPD filter manufacturing capabilities. Fabricating BAW filters demands sophisticated thin-film deposition equipment, advanced photolithography systems, and highly controlled cleanroom environments comparable to leading-edge semiconductor fabs. These infrastructure requirements create formidable barriers to entry, limiting the number of credible manufacturers globally and concentrating market share among a relatively small group of established players. New entrants seeking to compete in the BAW filter segment face multi-year timelines and substantial financial risk before achieving production-ready yields at commercial scale.

Technological Limitations of SAW Filters at Higher 5G Frequency Bands

While SAW filters continue to represent a significant portion of RF Filter (BAW, SAW, IPD) Market by volume, their inherent physical limitations at frequencies above approximately 2.5 GHz present a growing restraint on their applicability in next-generation wireless systems. Conventional SAW filter performance degrades at higher frequencies due to increased acoustic losses and temperature coefficient of frequency (TCF) challenges, making them less suitable for critical 5G mid-band and mmWave applications without significant design modifications. Although temperature-compensated SAW (TC-SAW) and advanced variants such as high-band SAW have been developed to partially address these limitations, the fundamental physics constraints continue to restrain SAW filter adoption in premium 5G device configurations, ceding ground to BAW-based solutions in the most demanding frequency applications.

MARKET OPPORTUNITIES

Growing Adoption of RF Filters in Advanced Driver Assistance Systems and Automotive Wireless Platforms

The automotive sector presents a compelling and rapidly expanding opportunity for RF Filter (BAW, SAW, IPD) Market. The increasing integration of advanced driver assistance systems (ADAS), cellular vehicle-to-everything (C-V2X) communication modules, and multi-band GNSS receivers in modern vehicles is driving demand for ruggedized, automotive-grade RF filtering solutions. SAW and BAW filters designed to meet AEC-Q200 qualification standards are gaining traction among Tier 1 automotive suppliers and module integrators, while IPD-based solutions offer the miniaturization benefits essential for space-constrained automotive electronics platforms. As electric vehicle adoption grows and in-vehicle connectivity becomes a standard feature across vehicle segments, the automotive RF filter opportunity is expected to expand substantially through the latter part of this decade.

Emergence of Filter Integration Technologies Enabling Next-Generation Module Architectures

Significant market opportunity exists in the development and commercialization of advanced RF filter integration technologies, particularly solutions that combine BAW, SAW, and IPD components within highly integrated RF front-end modules (RFFEM). As smartphone OEMs demand increasingly compact and power-efficient RF front-end architectures to accommodate more antenna bands within thinner device form factors, filter vendors with the capability to deliver co-designed, co-packaged multi-filter solutions are well-positioned to capture premium design wins. The trend toward antenna tuning, carrier aggregation support, and MIMO configurations in 5G devices amplifies this integration opportunity, encouraging collaboration between RF filter specialists, power amplifier vendors, and semiconductor packaging innovators to deliver differentiated system-level solutions RF Filter (BAW, SAW, IPD) Market.

Trends

5G Network Expansion Driving Demand for Advanced RF Filtering Solutions

RF Filter (BAW, SAW, IPD) Market is undergoing a significant transformation, largely propelled by the accelerating global rollout of 5G networks. As wireless carriers and network operators deploy 5G infrastructure across both sub-6 GHz and millimeter wave (mmWave) frequency bands, the demand for high-performance RF filters capable of managing complex signal environments has intensified considerably. Bulk Acoustic Wave (BAW) filters, in particular, have gained prominence due to their superior performance at higher frequency ranges, making them a preferred choice for 5G-compatible RF front-end modules. This shift is compelling leading manufacturers such as Murata Manufacturing Co., Ltd., Qorvo, Inc., and TDK Corporation to ramp up production capacity and invest heavily in next-generation filter technologies.

Other Trends

Rising Complexity of Multi-Band RF Front-End Architectures

Modern smartphones and connected devices are increasingly required to support multiple frequency bands and communication standards simultaneously. This growing complexity in multi-band and multi-mode RF front-end architectures is creating sustained demand for filters that can operate efficiently across diverse spectrum allocations. Surface Acoustic Wave (SAW) filters continue to maintain strong adoption in cost-sensitive, compact form factor applications, while Integrated Passive Device (IPD) technology is gaining traction for its superior integration capabilities in space-constrained, high-density module designs. Companies like Broadcom Inc. and Skyworks Solutions, Inc. are actively advancing IPD-based solutions to address these evolving design requirements.

IoT Proliferation Expanding the RF Filter Addressable Market

The rapid expansion of the Internet of Things (IoT) ecosystem is broadening the addressable market for RF Filter (BAW, SAW, IPD) solutions beyond traditional smartphone applications. Industrial IoT, smart home devices, wearables, and connected automotive systems each demand reliable wireless connectivity, necessitating robust signal filtering across a wide range of operating conditions. This diversification of end-use applications is encouraging filter manufacturers to develop versatile, low-power solutions tailored to the unique frequency and integration requirements of IoT platforms, further sustaining market momentum across multiple verticals.

Strategic Innovation and Capacity Expansion Among Key Market Participants

Leading players RF Filter (BAW, SAW, IPD) Market are responding to escalating demand through continuous product innovation and strategic manufacturing capacity expansion. Investments in advanced packaging technologies, wafer-level processing, and proprietary filter design platforms are enabling manufacturers to deliver higher performance, smaller footprint solutions aligned with the stringent requirements of next-generation wireless devices. This competitive innovation landscape is expected to remain a defining trend as the industry works to meet the technical demands of evolving wireless communication standards globally.

COMPETITIVE LANDSCAPE

Key Industry Players

RF Filter (BAW, SAW, IPD) Market: Competitive Dynamics and Leading Manufacturers

Global RF Filter (BAW, SAW, IPD) Market is characterized by a moderately consolidated competitive landscape, with a handful of established semiconductor and electronic component manufacturers commanding significant market share. Murata Manufacturing Co., Ltd. leads the market through its extensive portfolio of SAW and BAW filter solutions, underpinned by robust R&D capabilities and high-volume manufacturing infrastructure. Qorvo, Inc. and Broadcom Inc. are equally prominent, leveraging their advanced BAW filter technologies to serve the surging demand from 5G-enabled smartphone OEMs and network equipment manufacturers. TDK Corporation and Skyworks Solutions, Inc. further strengthen the competitive field through continuous product innovation, strategic partnerships, and capacity expansion initiatives tailored to meet the evolving requirements of multi-band RF front-end architectures. The competitive intensity of the market is amplified by the rapid global 5G rollout, which is compelling manufacturers to accelerate the development of high-performance filters capable of operating across sub-6 GHz and mmWave frequency bands.

Beyond the dominant tier-one players, several niche and regional manufacturers contribute meaningfully to the RF Filter market ecosystem. Companies such as Taiyo Yuden Co., Ltd. and EPCOS AG (a TDK Group company) have carved out strong positions in the SAW filter segment, particularly for cost-sensitive consumer electronics applications. Resonant Inc. has emerged as a noteworthy innovator with its XBAR technology targeting next-generation BAW filter performance. Meanwhile, WIN Semiconductors and Qualcomm Technologies continue to influence the IPD and integrated RF front-end filter space, addressing the growing complexity of multi-mode, multi-band device architectures. Competitive differentiation in this market is primarily driven by filter performance at higher frequency bands, miniaturization, integration capability, manufacturing yield, and total cost of ownership , factors that are increasingly scrutinized as wireless communication standards continue to evolve.

List of Key RF Filter (BAW, SAW, IPD) Companies Profiled

- Murata Manufacturing Co., Ltd.

- Qorvo, Inc.

- Broadcom Inc.

- Skyworks Solutions, Inc.

- TDK Corporation

- Taiyo Yuden Co., Ltd.

- EPCOS AG (TDK Group)

- Resonant Inc.

- Qualcomm Technologies, Inc.

- WIN Semiconductors Corp.

- Akoustis Technologies, Inc.

- CTS Corporation

- Anhui Yunta Electronic Technology Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Bulk Acoustic Wave (BAW) Filters represent the leading segment within the RF filter market, driven by their superior performance characteristics at higher frequency bands that are central to modern 5G deployments.

|

| By Application |

|

Mobile Devices & Smartphones constitute the dominant application segment for RF filters, reflecting the central role these components play in enabling seamless multi-band wireless connectivity in modern handsets.

|

| By End User |

|

Consumer Electronics Manufacturers represent the leading end-user segment, underpinned by the massive global production volumes of smartphones, tablets, and wearable devices that each require multiple RF filtering components.

|

| By Frequency Band |

|

Mid Band (Sub-6 GHz) filters represent the leading frequency segment, serving as the primary workhorse for 5G deployments that balance coverage reach with data throughput performance.

|

| By Form Factor & Integration |

|

Integrated Front-End Modules (FEM) are emerging as the leading form factor segment, reflecting the broader industry trend toward higher levels of RF component integration to meet the board space, power efficiency, and performance demands of modern wireless devices.

|

Regional Analysis: RF Filter (BAW, SAW, IPD) Market

Asia-Pacific

The accelerating deployment of 5G networks across Asia-Pacific is a primary catalyst for RF Filter (BAW, SAW, IPD) demand. Telecom operators in China, South Korea, and Japan are investing in dense urban network infrastructure, requiring sophisticated multi-band filter solutions capable of isolating high-frequency signals with minimal insertion loss and superior selectivity across sub-6GHz and mmWave spectrum bands.

Asia-Pacific hosts the world’s largest cluster of consumer electronics manufacturers, creating an enormous and consistent demand pipeline for RF Filter components. Smartphone production volumes in China and associated supply chains in Taiwan and South Korea ensure that BAW and SAW filter suppliers benefit from high-volume, long-term procurement contracts, reinforcing the region’s structural advantage in global market share.

Government-backed programs in China, South Korea, and Japan are channeling substantial investment into domestic RF Filter and broader semiconductor ecosystems. These initiatives are fostering local innovation in BAW and IPD filter technologies, reducing reliance on foreign suppliers, and cultivating a new generation of regionally competitive filter manufacturers capable of addressing both domestic and export market requirements through 2034.

Beyond smartphones, Asia-Pacific is witnessing rapid adoption of connected automotive platforms and industrial IoT systems, both of which rely on precision RF Filter solutions for reliable wireless communication. The region’s strong automotive manufacturing base in Japan, South Korea, and China, combined with booming smart factory deployments, is broadening RF Filter (BAW, SAW, IPD) Market’s end-use diversity and long-term demand resilience.

North America

North America represents a strategically critical region in Global RF Filter (BAW, SAW, IPD) Market, underpinned by the presence of leading semiconductor design firms, defense electronics contractors, and pioneering 5G network operators. The United States is home to several of the world’s most influential RF Filter innovators, whose proprietary BAW and IPD technologies are integral to premium smartphone platforms and advanced military communication systems. The region’s robust research and development ecosystem, supported by federal funding and academic collaboration, continues to push the boundaries of filter miniaturization, power efficiency, and multi-band performance. North America’s 5G commercialization trajectory, particularly across enterprise and private network segments, is generating differentiated demand for high-performance RF Filter solutions that go beyond consumer handset applications. Canada is also emerging as a contributor through its growing semiconductor design community. Overall, North America’s market is characterized by technological leadership, high-value applications, and strong intellectual property generation in the RF Filter domain.

Europe

Europe occupies a significant position RF Filter (BAW, SAW, IPD) Market, driven by its advanced automotive sector, robust industrial electronics industry, and progressive regulatory framework supporting spectrum management and wireless connectivity. Germany, France, Sweden, and the United Kingdom are key contributors, with their automotive OEMs and Tier-1 suppliers creating sustained demand for RF Filter components in connected and autonomous vehicle platforms. Europe’s commitment to smart manufacturing and Industry 4.0 initiatives further amplifies requirements for reliable, high-frequency filtering in industrial wireless systems. The region’s telecommunications operators are progressively extending 5G coverage, creating incremental demand for BAW and SAW filters in network equipment. Additionally, European research institutions are actively engaged in next-generation filter material science and packaging innovations, ensuring the region remains a meaningful contributor to global RF Filter technological advancement through the forecast period.

Latin America

Latin America is an emerging growth frontier RF Filter (BAW, SAW, IPD) Market, with its trajectory closely tied to the progressive rollout of 4G LTE consolidation and nascent 5G network deployments across Brazil, Mexico, Colombia, and Chile. While the region currently accounts for a comparatively modest share of global RF Filter consumption, expanding smartphone penetration, rising mobile data traffic, and government-supported digital infrastructure programs are gradually elevating demand for advanced filter technologies. Brazil serves as the region’s largest market, benefiting from a sizeable consumer electronics installed base and active telecom investment activity. Supply chain dependencies on imports from Asia-Pacific and North America remain a structural characteristic of Latin America’s RF Filter market, though increasing trade partnerships and foreign direct investment in electronics assembly are slowly enhancing local value-chain participation. The region’s long-term market potential remains promising as wireless connectivity becomes foundational to economic development strategies.

Middle East & Africa

The Middle East & Africa region represents an nascent but steadily evolving segment of Global RF Filter (BAW, SAW, IPD) Market. The Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are spearheading 5G network deployments as part of ambitious national digital transformation agendas, creating initial demand pools for advanced RF Filter solutions in both consumer and enterprise applications. South Africa serves as the primary market anchor on the African continent, where expanding mobile broadband infrastructure is driving incremental filter component procurement. While manufacturing capabilities within the region remain limited, positioning Middle East & Africa predominantly as a consumption rather than production market, ongoing investments in technology parks, smart city projects, and telecommunications modernization are expected to gradually deepen the region’s engagement with the RF Filter value chain. Long-term demand growth will be closely correlated with the pace of telecom infrastructure investment and digital adoption across both sub-regions through 2034.

Report Scope

This market research report provides a comprehensive analysis of the RF Filter (BAW, SAW, IPD) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of RF Filter (BAW, SAW, IPD) Market?

-> RF Filter (BAW, SAW, IPD) Market was valued at USD 3.21 billion in 2025 and is expected to reach USD 6.89 billion by 2034, growing at a CAGR of 7.7% during the forecast period from 2026 to 2034.

Which key companies operate RF Filter (BAW, SAW, IPD) Market?

-> Key players include Murata Manufacturing Co., Ltd., Qorvo, Inc., TDK Corporation, Broadcom Inc., and Skyworks Solutions, Inc., among others.

What are the key growth drivers?

-> Key growth drivers include rapid global rollout of 5G networks, proliferating adoption of smartphones and connected IoT devices, and the increasing complexity of multi-band RF front-end architectures. The growing demand for high-performance filters operating across sub-6 GHz and mmWave frequency bands also continues to accelerate technology investment.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by strong manufacturing bases and rapid 5G deployment, while North America remains a significant market due to advanced telecommunications infrastructure and leading semiconductor companies.

What are the emerging trends?

-> Emerging trends include BAW filter adoption for higher frequency bands, advanced IPD integration for multi-band and multi-mode devices, and SAW filter innovation for cost-efficient compact form factors suited to next-generation wireless communication systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...