Market Insights

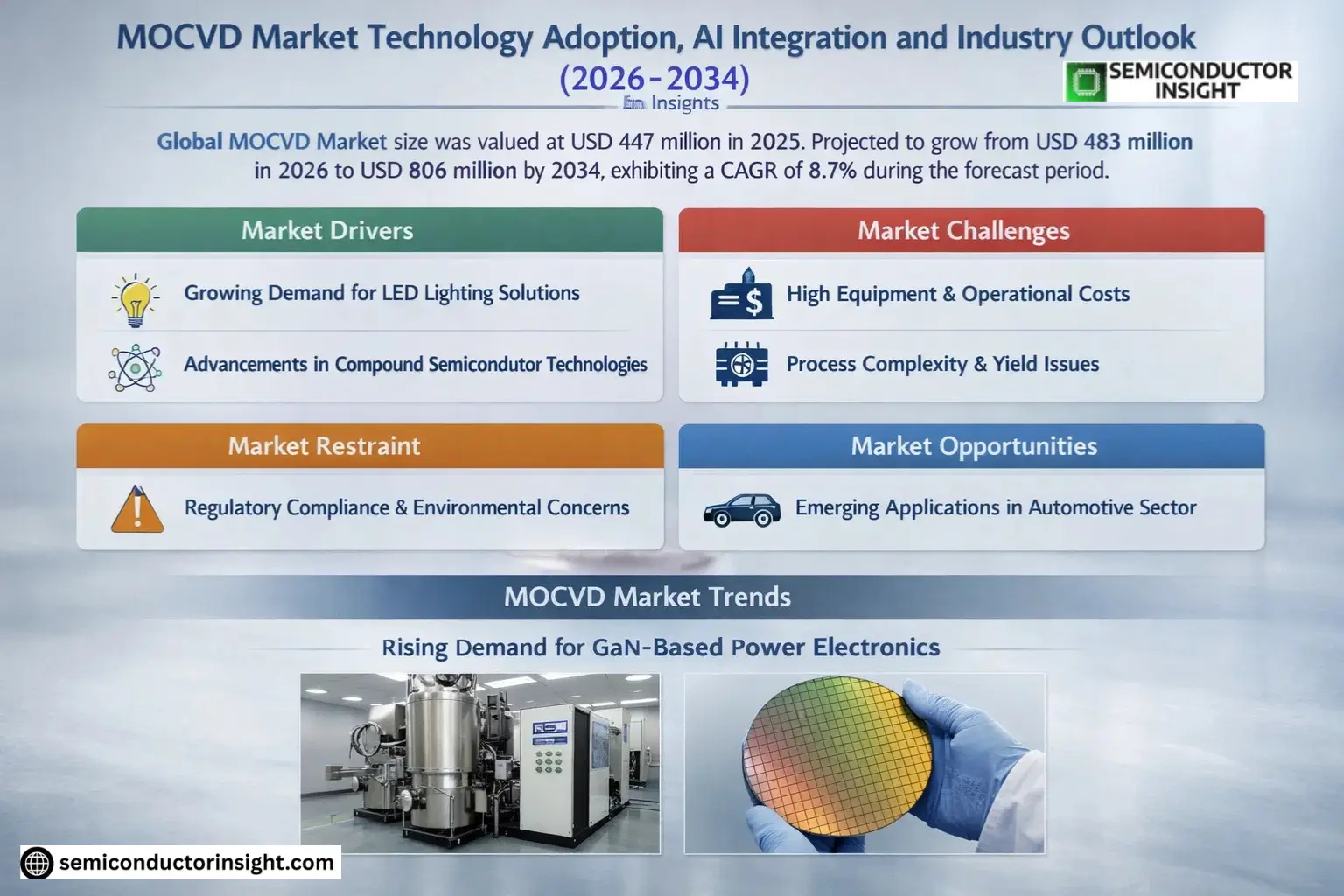

Global MOCVD Market size was valued at USD 447 million in 2025. The market is projected to grow from USD 483 million in 2026 to USD 806 million by 2034, exhibiting a CAGR of 8.7% during the forecast period.

Metal-Organic Chemical Vapor Deposition (MOCVD) is a critical semiconductor manufacturing technology used to produce high-performance compound materials such as gallium nitride (GaN), indium phosphide (InP), and gallium arsenide (GaAs). These materials form the foundation for advanced optoelectronic and power electronic devices, including LEDs, laser diodes, RF components, and power transistors. The process enables precise control over layer thickness, doping levels, and material composition at an atomic scale.

Market growth is driven by increasing demand for energy-efficient lighting solutions, expansion of 5G infrastructure requiring high-frequency RF devices, and rapid adoption of GaN-based power electronics in electric vehicles and renewable energy systems. Technological advancements in mini/micro-LED displays for consumer electronics and automotive applications are creating new opportunities. Key industry players like AIXTRON and Veeco Instruments continue to innovate with multi-wafer reactor designs and AI-driven process optimization tools to improve yield rates and throughput efficiency.

MARKET DRIVERS

Growing Demand for LED Lighting Solutions

MOCVD Market is experiencing significant growth due to increasing adoption of energy-efficient LED lighting across residential, commercial, and industrial sectors. Government initiatives promoting sustainable lighting solutions have further accelerated demand. Global LED market is projected to grow at 12% CAGR, directly benefiting MOCVD equipment manufacturers.

Advancements in Compound Semiconductor Technologies

Technological innovations in compound semiconductor manufacturing are driving MOCVD Market expansion. The development of GaN and SiC-based devices for power electronics and RF applications requires precise MOCVD deposition processes. Semiconductor foundries are investing heavily in next-generation MOCVD systems to meet the demand for these high-performance chips.

Additionally, the expansion of 5G infrastructure worldwide is creating new opportunities for MOCVD systems used in RF device manufacturing.

MARKET CHALLENGES

High Equipment and Operational Costs

The capital-intensive nature of MOCVD systems presents a significant barrier to market entry. A single MOCVD reactor can cost between $1.5-3 million, with additional expenses for maintenance and precursor materials. This high cost structure limits adoption among smaller semiconductor manufacturers.

Other Challenges

Process Complexity and Yield Issues

Maintaining consistent epitaxial growth quality across large wafer areas remains technically challenging in MOCVD applications. Process parameter optimization requires extensive expertise, and even minor defects can significantly impact device performance and yield rates.

MARKET RESTRAINT

Regulatory Compliance and Environmental Concerns

Stringent environmental regulations governing hazardous precursor materials used in MOCVD processes may limit market growth. Proper handling and disposal of metalorganic compounds and toxic byproducts adds operational complexity and compliance costs for manufacturers.

MARKET OPPORTUNITIES

Emerging Applications in Automotive Sector

The increasing adoption of electric vehicles is creating new opportunities for MOCVD technology in power electronics manufacturing. GaN-based devices produced using MOCVD are becoming essential components in EV power converters and charging systems. The automotive power electronics market is projected to exceed $10 billion by 2028.

MOCVD Market Trends

Rising Demand for GaN-Based Power Electronics

MOCVD Market is experiencing significant growth due to increasing adoption of gallium nitride (GaN) in power electronics. GaN-based devices enable higher efficiency and faster switching speeds, making them ideal for electric vehicle power systems and renewable energy applications. This trend is driving investments in larger-scale MOCVD systems capable of 8-inch wafer processing.

Other Trends

Mini/Micro LED Production Scaling

Display manufacturers are accelerating the transition from conventional LEDs to Mini/Micro LED technology, requiring more precise MOCVD systems. The demand for higher pixel density displays in consumer electronics is pushing for improvements in uniformity and defect control during epitaxial growth.

Regional Manufacturing Concentration

East Asia maintains dominance in MOCVD equipment deployment, accounting for over 70% of global installations. This concentration reflects the region’s leadership in LED production and semiconductor manufacturing. Western markets are focusing more on specialized applications like RF devices and optical communications, driving demand for customized MOCVD solutions.

Process Monitoring Advancements

Equipment manufacturers are incorporating real-time in-situ monitoring capabilities to improve yield rates. Advanced sensors and AI-based analytics are being integrated into modern MOCVD systems to maintain tighter control over layer thickness and composition.

Vertical Integration Strategies

Leading MOCVD suppliers are expanding their service capabilities to include spare parts ecosystems and localized technical support. This vertical integration helps reduce downtime for high-volume production facilities and improves equipment utilization rates across the semiconductor industry.

COMPETITIVE LANDSCAPE

Key Industry Players

MOCVD Market Dominated by Specialized Equipment Manufacturers

Global MOCVD Market is highly concentrated, with AIXTRON and Veeco Instruments commanding a combined 65% market share in 2025. These established players dominate the LED production segment through advanced multi-wafer reactor systems and proprietary gas injection technologies. The competitive landscape features strong technological barriers, with average customer qualification cycles exceeding 18 months for new entrants.

Emerging Chinese manufacturers like Advanced Micro-Fabrication Equipment and Topecsh are gaining traction in the GaN power device segment through cost-competitive solutions. Niche players such as NuFlare Technology specialize in laser diode applications, while Taiyo Nippon Sanso leverages its gas expertise for integrated solutions. The market sees increasing competition in 8-inch wafer capable systems as power electronics demand grows.

List of Key MOCVD Companies Profiled

- AIXTRON SE

- Veeco Instruments Inc.

- Advanced Micro-Fabrication Equipment Inc.

- Topecsh

- Taiyo Nippon Sanso Corporation

- NuFlare Technology Inc.

- Applied Materials Inc.

- LayTec AG

- Tokyo Electron Limited

- DAS Environmental Experts GmbH

- TurboDisc

- SVCS Process Innovation

- ASM International

- CVD Equipment Corporation

- Thomas Swan Scientific Equipment Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

GaN-based MOCVD dominates due to its critical role in LED manufacturing and power electronics:

|

| By Application |

|

LED Production remains the most established application segment:

|

| By End User |

|

Integrated Device Manufacturers are the primary adopters:

|

| By Wafer Size |

|

6 inch wafers are gaining significant traction:

|

| By Chamber Configuration |

|

Multi-chamber systems are becoming industry standard:

|

Regional Analysis: Asia-Pacific MOCVD Market

China Dominates MOCVD Technology Adoption

The Chinese government’s substantial subsidies for semiconductor equipment purchases and local production incentives have significantly accelerated MOCVD technology deployment. Special economic zones offer tax benefits for manufacturers adopting advanced deposition technologies.

Chinese firms have achieved remarkable vertical integration from MOCVD equipment to final LED packaging. This ecosystem enables rapid technology transfer and optimization of deposition processes for specific end-use applications.

Leading Chinese fabs are implementing machine learning algorithms to predict and control MOCVD process parameters, significantly reducing trial-and-error iterations and improving epitaxial layer uniformity across wafer surfaces.

Beyond traditional LED manufacturing, Chinese companies are pioneering MOCVD applications in microLED displays, power electronics, and RF components for 5G infrastructure, driving demand for next-generation systems.

South Korea

South Korea maintains technological leadership in high-end MOCVD systems through continuous R&D investments by domestic equipment manufacturers. The country’s advanced display industry demands cutting-edge MOCVD solutions for microLED and OLED production. Close collaboration between semiconductor foundries and equipment suppliers enables rapid implementation of process innovations. Korean firms are particularly focused on developing atomic layer precision control systems for next-generation compound semiconductors.

Japan

Japanese MOCVD Market benefits from decades of expertise in precision manufacturing and materials science. The country remains strong in specialty applications such as laser diodes and optical communication devices. Aging production facilities are gradually being upgraded with newer MOCVD models featuring advanced in-situ monitoring capabilities. Japanese manufacturers emphasize energy efficiency and reduced precursor consumption in next-gen system designs.

Taiwan

Taiwan’s robust semiconductor foundry ecosystem drives steady demand for MOCVD equipment, particularly for power electronics applications. The island’s strategic position in the global supply chain facilitates technology transfer between international equipment vendors and local manufacturers. Taiwanese firms are actively implementing Industry 4.0 solutions in MOCVD operations, including predictive maintenance and remote monitoring capabilities.

Southeast Asia

Southeast Asian nations are emerging as attractive locations for MOCVD system deployment as manufacturers diversify production bases beyond China. Countries like Malaysia and Vietnam are building semiconductor infrastructure with MOCVD technology playing a crucial role in local value chain development. The region benefits from competitive labor costs and growing government support for high-tech manufacturing investments.

Report Scope

This market research report provides a comprehensive analysis of the MOCVD Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of MOCVD Market?

-> MOCVD Market size was valued at USD 447 million in 2025. The market is projected to grow from USD 483 million in 2026 to USD 806 million by 2034, exhibiting a CAGR of 8.7% during the forecast period.

What is the expected growth rate (CAGR) of MOCVD Market?

-> The market is expected to grow at a CAGR of 8.7% during the forecast period (2025-2034).

Which key companies operate in MOCVD Market?

-> Key players include AIXTRON Technologies, Advanced Micro-Fabrication Equipment, Topecsh, Veeco Instruments, Taiyo Nippon Sanso, and NuFlare Technology.

What are the key applications of MOCVD?

-> Major applications include LEDs, power devices, lasers, RF devices, with LEDs being the dominant segment.

Which region leads in MOCVD Market share?

-> East Asia shows highest market concentration due to strong LED and semiconductor manufacturing presence.

What are key technological trends in MOCVD?

-> Emerging trends include larger wafer capability, in-situ monitoring, higher throughput systems, and platform modularization.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...