Flexible Data Placement (FDP) SSD Firmware Market Insights

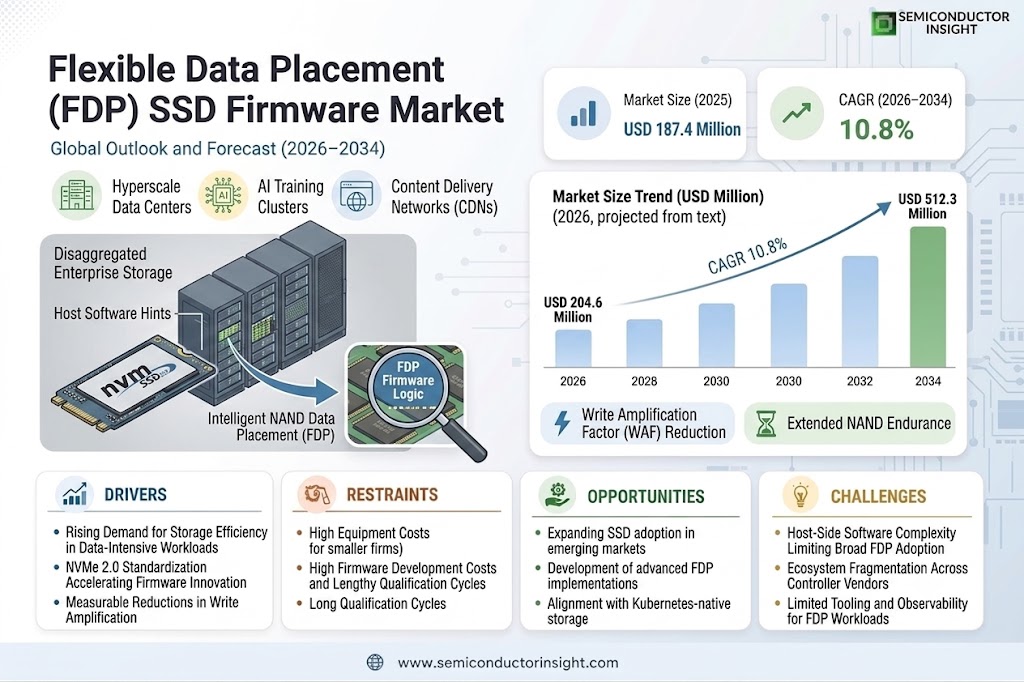

Flexible Data Placement (FDP) SSD Firmware Market size was valued at USD 187.4 million in 2025. The market is projected to grow from USD 204.6 million in 2026 to USD 512.3 million by 2034, exhibiting a CAGR of 10.8% during the forecast period.

Flexible Data Placement (FDP) SSD firmware refers to a specialized layer of software embedded within solid-state drives that enables host systems to direct data placement at a granular level within the NAND flash memory. This technology, standardized under the NVM Express (NVMe) specification, allows storage controllers to optimize write amplification, improve endurance, and enhance overall drive performance by giving the host greater control over how data is organized and managed across memory cells. FDP encompasses firmware-level implementations supporting features such as reclaim unit management, placement identifiers, and media error recovery , all critical to next-generation enterprise and data center storage architectures.

The market is gaining strong momentum driven by the rapid expansion of hyperscale data centers, the surging adoption of NVMe-based storage solutions, and the growing need to reduce write amplification factor (WAF) in high-throughput workloads. Furthermore, the industry-wide transition from Open-Channel SSDs and ZNS (Zoned Namespace) to FDP as a more host-friendly, standards-compliant alternative is accelerating firmware development cycles. Key industry players including Samsung Electronics, Western Digital, Micron Technology, SK Hynix, and Kioxia are actively developing and deploying FDP-compliant firmware solutions, reinforcing competitive momentum across the global market.

MARKET DRIVERS

Rising Demand for Storage Efficiency in Data-Intensive Workloads

Flexible Data Placement (FDP) SSD Firmware Market is gaining significant momentum as hyperscale data centers and cloud service providers seek more efficient NVMe storage solutions. FDP, ratified as part of the NVMe 2.0 specification, enables host software to provide placement hints to the SSD firmware, allowing the drive to organize data more intelligently across its NAND flash media. This architectural improvement directly reduces write amplification factor (WAF), which is a persistent challenge in high-throughput enterprise storage environments. As workloads grow more complex across AI training clusters, real-time analytics platforms, and content delivery networks, the ability of FDP-enabled SSD firmware to optimize internal data management has become a compelling operational advantage.

NVMe 2.0 Standardization Accelerating Firmware Innovation

The formal standardization of Flexible Data Placement within the NVMe 2.0 specification has provided SSD firmware developers with a clear and interoperable framework, removing a key barrier to enterprise adoption. Unlike proprietary stream-based approaches that required vendor-specific host integration, FDP offers a standardized interface that both SSD manufacturers and operating system vendors can implement consistently. Major technology companies have already begun contributing open-source FDP support to Linux kernel NVMe drivers, which accelerates the ecosystem’s readiness for commercial deployment. This standards-driven momentum is a primary driver propelling investments in FDP SSD firmware development across both established storage vendors and emerging fabless SSD controller startups.

➤ FDP-enabled SSD firmware has demonstrated measurable reductions in write amplification in controlled enterprise benchmarks, translating directly into extended NAND endurance and lower total cost of ownership for large-scale flash deployments.

Beyond endurance benefits, the Flexible Data Placement SSD Firmware Market is also driven by the growing alignment between storage firmware capabilities and software-defined storage architectures. As Kubernetes-native storage, disaggregated storage systems, and NVMe-oF (NVMe over Fabrics) deployments scale, the ability to pass placement context from the application layer down to the firmware layer creates a tightly optimized I/O pipeline. This convergence of software and firmware intelligence is reshaping how enterprises evaluate SSD procurement decisions, increasingly favoring drives with robust FDP firmware support as a long-term strategic asset.

MARKET CHALLENGES

Host-Side Software Complexity Limiting Broad FDP Adoption

Despite the technical promise of the Flexible Data Placement SSD Firmware Market, one of the most significant challenges constraining adoption is the complexity of implementing FDP support at the host software level. FDP is not a passive firmware feature , it requires active cooperation from the host operating system, file system, and application stack to generate meaningful placement hints. Without well-tuned host-side software, an FDP-capable drive may operate without realizing the WAF reduction benefits it was engineered to deliver. Many enterprise IT teams and independent software vendors lack the specialized NVMe firmware expertise required to implement and validate FDP hint generation, creating an adoption gap between hardware availability and effective utilization.

Other Challenges

Ecosystem Fragmentation Across Controller Vendors

While the NVMe 2.0 specification defines the FDP framework, individual SSD controller vendors implement FDP firmware with varying levels of feature completeness, performance optimization, and host compatibility. This fragmentation means that enterprises cannot always assume uniform FDP behavior across drives from different vendors, complicating qualification processes and supply chain diversification strategies. Storage administrators must invest additional time and resources in validating FDP behavior specific to each firmware version and controller platform, increasing the operational burden of managing a heterogeneous FDP SSD fleet.

Limited Tooling and Observability for FDP Workloads

The absence of mature diagnostic and observability tooling for FDP SSD firmware remains a practical challenge for both storage vendors and enterprise operators. Monitoring write amplification reduction, placement efficiency, and reclaim unit utilization in real time requires firmware-level telemetry that is not yet standardized across all FDP implementations. This visibility gap makes it difficult for storage architects to quantify FDP’s operational ROI in production environments, which in turn slows procurement decisions and limits the market’s ability to demonstrate clear and repeatable value propositions to potential adopters of Flexible Data Placement SSD Firmware solutions.

MARKET RESTRAINTS

High Firmware Development Costs and Lengthy Qualification Cycles

The Flexible Data Placement SSD Firmware Market faces a meaningful structural restraint in the form of high development costs and extended qualification timelines associated with enterprise-grade firmware. Developing, validating, and certifying FDP firmware across multiple NAND generations, controller platforms, and target operating environments demands substantial engineering investment. For smaller SSD controller companies and firmware independent software vendors, the resource requirements to deliver a fully compliant and robustly tested FDP firmware stack can be prohibitive. Hyperscale customers and OEM partners typically enforce rigorous multi-month qualification programs before approving new SSD firmware for production deployment, further extending the time-to-revenue cycle for FDP firmware innovations.

Legacy Storage Infrastructure Slowing Enterprise Transition

A significant portion of enterprise storage infrastructure currently operates on NVMe 1.x or SATA/SAS-based platforms that are architecturally incompatible with Flexible Data Placement SSD Firmware capabilities. Organizations with long hardware refresh cycles, particularly in regulated industries such as financial services, healthcare, and government, face substantial capital and operational costs when transitioning to NVMe 2.0-compatible storage infrastructure. The coexistence of legacy and modern storage tiers within the same data center environment creates firmware management complexity and limits the ability of IT teams to standardize on FDP-capable SSD fleets. This installed base inertia acts as a restraint on the pace of Flexible Data Placement SSD Firmware Market growth across traditional enterprise segments.

MARKET OPPORTUNITIES

AI and Machine Learning Workloads Creating New FDP Firmware Demand

The rapid proliferation of AI model training and inference infrastructure presents a high-value growth opportunity for the Flexible Data Placement SSD Firmware Market. AI workloads are characterized by large sequential writes during checkpoint operations, random reads during data ingestion, and mixed I/O profiles during fine-tuning , all patterns that benefit meaningfully from FDP-guided data placement strategies. As GPU cluster operators seek to minimize storage bottlenecks and reduce SSD wear-out rates in cost-sensitive AI infrastructure deployments, FDP-enabled firmware becomes an increasingly attractive differentiator. SSD vendors that develop AI-workload-optimized FDP firmware profiles stand to capture significant share in the rapidly expanding AI infrastructure storage segment.

Open-Source Ecosystem Collaboration Expanding FDP Integration Opportunities

The growing participation of major cloud and platform vendors in open-source FDP development , including contributions to Linux kernel NVMe subsystems and open-source storage management tools , is creating substantial opportunities for the Flexible Data Placement SSD Firmware Market to expand its addressable ecosystem. As FDP support becomes natively available in widely deployed Linux distributions and container storage interfaces, the barrier to host-side implementation is progressively lowered, enabling a broader set of enterprises and cloud-native application developers to leverage FDP-capable SSD firmware without deep NVMe expertise. Firmware vendors that actively engage with open-source communities and contribute reference FDP implementations position themselves to influence specification evolution while accelerating market penetration across the global enterprise storage landscape.

Trends

Rising Adoption of NVMe-Based Storage Driving FDP SSD Firmware Development

Flexible Data Placement (FDP) SSD Firmware Market is witnessing accelerating momentum as enterprises and hyperscale data center operators increasingly shift toward NVMe-based storage architectures. The widespread adoption of NVMe protocols has created a strong foundation for FDP firmware deployment, enabling host systems to exercise granular control over data placement within NAND flash memory. This shift is primarily driven by the need to reduce write amplification factor (WAF) in high-throughput workloads, which directly translates into improved drive endurance and lower total cost of ownership. As data center operators scale their infrastructure, FDP-compliant firmware is emerging as a critical tool for optimizing storage performance at the firmware level, reinforcing the technology’s strategic relevance across enterprise storage ecosystems.

Other Trends

Transition from Open-Channel SSDs and ZNS to FDP Architectures

A significant trend reshaping Flexible Data Placement (FDP) SSD Firmware Market is the industry-wide migration away from Open-Channel SSDs and Zoned Namespace (ZNS) solutions toward FDP as a more host-friendly and standards-compliant alternative. Unlike its predecessors, FDP offers a balanced approach by giving host systems meaningful control over data organization without requiring them to manage low-level flash operations directly. This transition is shortening firmware development cycles and encouraging broader hardware-software co-optimization strategies among storage vendors. Key industry players including Samsung Electronics, Western Digital, Micron Technology, SK Hynix, and Kioxia are actively advancing FDP-compliant firmware portfolios, intensifying competitive dynamics across the global market.

Standardization Under NVMe Specification Accelerating Market Maturity

The formalization of Flexible Data Placement under the NVM Express (NVMe) specification has been instrumental in driving market maturity. Standardization provides firmware developers with a clear technical framework encompassing reclaim unit management, placement identifiers, and media error recovery , all essential components for next-generation enterprise storage architectures. This regulatory clarity is reducing interoperability barriers and enabling a broader ecosystem of compatible hardware and software solutions to emerge, further expanding the addressable market for FDP SSD firmware globally.

Hyperscale Data Center Expansion Reinforcing Long-Term Demand

The rapid expansion of hyperscale data centers globally continues to serve as a primary demand driver for Flexible Data Placement (FDP) SSD Firmware Market. As cloud service providers scale operations to meet surging data storage and processing requirements, the need for firmware solutions that optimize NAND flash utilization and extend drive lifespan has grown considerably. FDP firmware addresses these operational imperatives by enabling intelligent data organization at a granular level, reducing unnecessary write cycles and improving overall storage efficiency , making it a preferred choice for large-scale storage deployments in modern data infrastructure environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Flexible Data Placement (FDP) SSD Firmware Market , Competitive Intelligence & Leading Manufacturer Profiles

Flexible Data Placement (FDP) SSD Firmware Market is characterized by the strong dominance of vertically integrated NAND flash manufacturers who control both the memory fabrication and firmware development stack. Samsung Electronics leads the competitive field, leveraging its proprietary NAND architecture and robust NVMe firmware engineering capabilities to deploy FDP-compliant solutions across enterprise and hyperscale data center segments. The company’s deep integration between hardware design and firmware development provides a significant competitive moat, enabling rapid iteration on placement identifier logic, reclaim unit management, and write amplification optimization , core pillars of FDP firmware performance. Western Digital and Micron Technology also command substantial market share, each investing heavily in NVMe-native firmware platforms that align with the evolving FDP specification ratified under the NVM Express standard. These leading players are actively collaborating with hyperscale cloud operators to validate FDP firmware implementations at scale, further entrenching their positions in this high-growth market.

Beyond the tier-one NAND manufacturers, the FDP SSD firmware market features a competitive layer of specialized storage solution providers, SSD controller IC vendors, and firmware-focused technology firms. SK Hynix and Kioxia are making notable strides in FDP-compliant firmware development, particularly targeting enterprise NVMe SSD product lines destined for cloud-native and AI infrastructure deployments. Controller silicon vendors such as Marvell Technology and Phison Electronics play a pivotal enabling role, supplying SSD controller platforms with integrated firmware frameworks that support FDP primitives, allowing OEM and ODM partners to build standards-compliant drives without developing firmware from scratch. Additionally, system integrators and white-box SSD vendors including YMTC and Solidigm are emerging as competitive participants, accelerating product roadmaps that incorporate FDP to address write amplification challenges in high-throughput workloads.

List of Key Flexible Data Placement (FDP) SSD Firmware Companies Profiled

- Samsung Electronics Co., Ltd.

- Western Digital Corporation

- Micron Technology, Inc.

- SK Hynix Inc.

- Kioxia Holdings Corporation

- Marvell Technology, Inc.

- Phison Electronics Corporation

- Solidigm (formerly Intel NAND Solutions Group)

- YMTC (Yangtze Memory Technologies Co., Ltd.)

- Silicon Motion Technology Corporation

- Innodisk Corporation

- ADATA Technology Co., Ltd.

- Sage Microelectronics Corp.

- Memblaze Technology Co., Ltd.

- ScaleFlux, Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

NVMe FDP-Compliant Firmware stands as the dominant type segment, propelled by the widespread standardization of the NVM Express specification across enterprise storage ecosystems.

|

| By Application |

|

Hyperscale Data Centers represent the leading application segment, driven by the relentless scaling of global digital infrastructure and the corresponding demand for storage solutions that maximize NAND flash endurance under sustained, high-throughput workloads.

|

| By End User |

|

Cloud Service Providers (CSPs) emerge as the dominant end user segment, commanding significant influence over FDP SSD firmware development priorities and deployment timelines globally.

|

| By Interface Protocol |

|

NVMe over PCIe leads the interface protocol segment, serving as the foundational connectivity standard upon which the majority of FDP SSD firmware implementations are currently designed and validated.

|

| By NAND Flash Technology |

|

3D TLC NAND represents the leading flash technology segment for FDP firmware deployment, striking an optimal balance between storage density, write endurance, and cost efficiency that resonates strongly with enterprise and hyperscale storage buyers.

|

Regional Analysis: Flexible Data Placement (FDP) SSD Firmware Market

North America

North America’s hyperscale data centers are among the earliest and most aggressive adopters of Flexible Data Placement SSD firmware technologies. Operators in this region are under constant pressure to reduce total cost of ownership while maximizing storage efficiency, making FDP-enabled firmware a strategically valuable tool. The region’s scale of deployment ensures rapid maturation of FDP firmware standards and interoperability protocols across heterogeneous storage environments.

The United States leads global research and development investments in NVMe-based firmware engineering, with multiple industry consortia and standards bodies headquartered in the region actively defining FDP specifications. Collaboration between major SSD manufacturers and cloud-native software companies creates a fertile environment where Flexible Data Placement firmware innovations are rapidly prototyped, validated, and commercialized ahead of other global regions.

Rising enterprise demand for AI-optimized storage infrastructure is a powerful catalyst for Flexible Data Placement SSD firmware adoption across North America. Organizations deploying large-scale machine learning pipelines and real-time inference engines increasingly require firmware-level write management capabilities that FDP uniquely provides. This demand is particularly pronounced among financial services, healthcare informatics, and autonomous systems sectors operating across the United States and Canada.

North America’s evolving data center sustainability mandates and energy efficiency regulations are indirectly reinforcing adoption of Flexible Data Placement SSD firmware, as FDP technologies help reduce unnecessary write operations and extend drive endurance. Industry standards organizations based in the region are also codifying FDP as part of broader NVMe specification revisions, lending institutional credibility and procurement confidence to enterprise buyers across the market.

Europe

Europe represents a strategically significant region withFlexible Data Placement (FDP) SSD Firmware Market, shaped by the continent’s strong emphasis on data sovereignty, digital infrastructure investment, and green technology mandates. Countries such as Germany, the Netherlands, and the Nordic nations are at the forefront of deploying energy-efficient data center architectures where FDP-compatible SSD firmware plays a critical role in reducing write amplification and prolonging flash endurance. The European Union’s regulatory push toward sustainable digital infrastructure, including its data center energy efficiency directives, has created a compelling business case for firmware technologies that reduce unnecessary storage operations. Furthermore, European telecommunications carriers and cloud operators are progressively transitioning toward NVMe-native storage ecosystems, opening substantial demand channels for advanced Flexible Data Placement firmware solutions. The region’s enterprise sector, particularly in manufacturing automation, financial services, and smart mobility, is also emerging as a meaningful end-user segment driving firmware-level storage optimization requirements through the forecast period.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing region Flexible Data Placement (FDP) SSD Firmware Market, fueled by the rapid expansion of digital infrastructure across China, South Korea, Japan, Taiwan, and India. The region is home to several of the world’s largest NAND flash manufacturers and SSD controller developers, giving it a unique supply-side advantage in advancing FDP firmware capabilities at the component level. South Korea and Taiwan, in particular, serve as critical hubs where semiconductor engineering talent and manufacturing scale converge to accelerate firmware development cycles. Meanwhile, China’s aggressive buildout of sovereign cloud infrastructure and domestic data center capacity is generating substantial demand for intelligent storage management technologies including FDP-enabled firmware. India’s rapidly growing digital economy, supported by government-led data localization policies and expanding hyperscale investments, is also beginning to contribute meaningfully to regional demand for Flexible Data Placement SSD firmware solutions targeting enterprise and cloud workloads.

South America

South America occupies a developing but progressively important position in Global Flexible Data Placement (FDP) SSD Firmware Market. Brazil serves as the region’s primary demand anchor, with its expanding cloud infrastructure market and growing base of digital-native enterprises creating foundational conditions for FDP firmware adoption. The region’s financial services sector, including a vibrant fintech ecosystem, is increasingly adopting enterprise-grade SSD storage solutions where firmware optimization is valued for its impact on transactional throughput and data durability. Chile and Colombia are emerging as secondary growth markets, supported by new data center construction projects and improving digital connectivity. However, South America’s overall adoption pace remains tempered by economic variability, import dependency on advanced semiconductor products, and relatively limited local firmware engineering expertise, factors that will require sustained investment and technology transfer partnerships to overcome throughout the forecast horizon of the Flexible Data Placement SSD firmware landscape.

Middle East & Africa

The Middle East and Africa region represents an early-stage but increasingly strategic market within the Flexible Data Placement (FDP) SSD Firmware landscape. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are spearheading the region’s digital infrastructure transformation through ambitious smart city programs, sovereign cloud initiatives, and national AI strategies that collectively demand advanced storage technologies. FDP-enabled SSD firmware solutions are gaining attention among regional hyperscale operators and government data center projects seeking to optimize storage efficiency and manage lifecycle costs at scale. South Africa anchors the African continent’s demand, serving as a regional hub for financial services and telecommunications infrastructure where enterprise SSD adoption is gradually maturing. While the broader Middle East and Africa market faces challenges including infrastructure gaps and reliance on imported storage technology, the region’s long-term trajectory in the Flexible Data Placement SSD firmware market remains constructive, supported by sovereign wealth-backed digitalization investments and growing partnerships with global technology vendors.

Report Scope

This market research report provides a comprehensive analysis of the Flexible Data Placement (FDP) SSD Firmware Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Flexible Data Placement (FDP) SSD Firmware Market?

-> Global Flexible Data Placement (FDP) SSD Firmware Market was valued at USD 187.4 million in 2025 and is projected to grow from USD 204.6 million in 2026 to USD 512.3 million by 2034, exhibiting a CAGR of 10.8% during the forecast period.

Which key companies operate Flexible Data Placement (FDP) SSD Firmware Market?

-> Key players include Samsung Electronics, Western Digital, Micron Technology, SK Hynix, and Kioxia, among others.

What are the key growth drivers?

-> Key growth drivers include the rapid expansion of hyperscale data centers, surging adoption of NVMe-based storage solutions, and the growing need to reduce write amplification factor (WAF) in high-throughput workloads. The industry-wide transition from Open-Channel SSDs and ZNS (Zoned Namespace) to FDP as a more host-friendly, standards-compliant alternative is also accelerating firmware development cycles.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America remains a dominant market driven by large-scale hyperscale data center deployments and strong enterprise NVMe SSD adoption.

What are the emerging trends?

-> Emerging trends include FDP standardization under NVMe specifications, host-managed data placement optimization, reclaim unit management, placement identifier frameworks, and the transition from Open-Channel SSDs and Zoned Namespace (ZNS) solutions to FDP-compliant firmware architectures across enterprise and data center storage environments.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...