Digital Pathology (Whole Slide) Image Sensor Market Insights

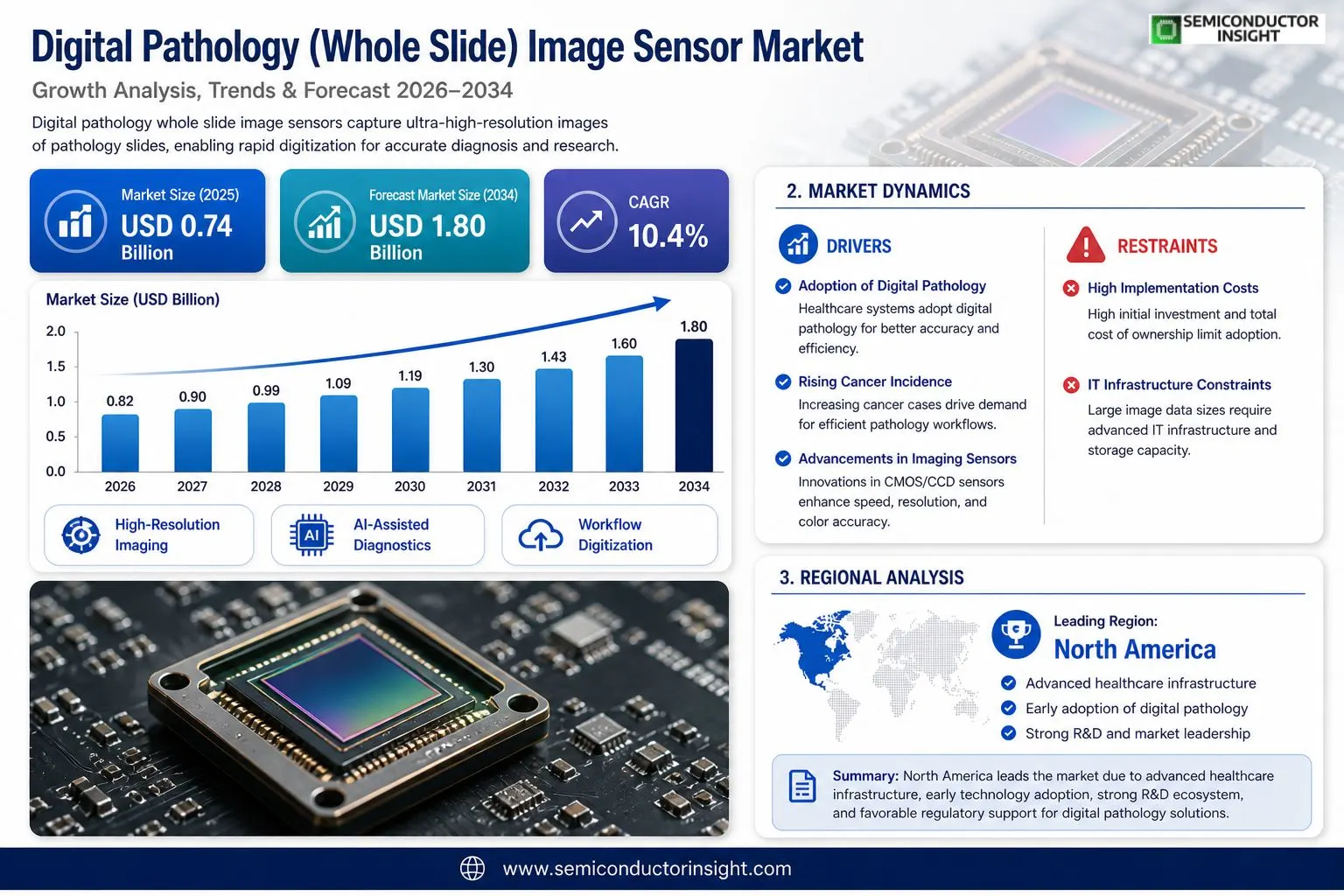

Global Digital Pathology (Whole Slide) Image Sensor Market size was valued at USD 0.74 billion in 2025. The market is projected to grow from USD 0.82 billion in 2026 to USD 1.80 billion by 2034, exhibiting a CAGR of 10.4% during the forecast period.

Digital pathology (whole slide) image sensors are highly specialized optical and electronic components engineered to capture ultra‑high‑resolution images of pathology slides for diagnostic, research, and workflow optimization applications. These sensors enable rapid digitization of tissue samples, allowing pathologists to analyze detailed histological structures with precision while integrating data into digital workflows. The technology encompasses advanced CMOS and CCD sensor architectures that support large field‑of‑view scanning, high dynamic range, and accurate color reproduction, all of which are critical for clinical interpretation.

The market is expanding steadily because healthcare systems worldwide are accelerating the adoption of digital pathology to improve diagnostic accuracy and address shortages in trained pathologists. Furthermore, the rise in cancer incidence is increasing demand for efficient pathology workflows, while advancements in whole slide imaging systems continue to drive sensor innovation. Significant industry developments are supporting this growth; for example, in 2023 and 2024, companies such as Leica Biosystems, Hamamatsu Photonics, and Philips intensified their investments in high‑resolution sensor technologies to enhance scanning speed and image fidelity. While digital adoption still faces challenges such as high implementation costs, increasing regulatory approvals and broader integration of AI‑assisted diagnostics are strengthening market momentum because they improve both clinical efficiency and data consistency.

MARKET DRIVERS

Rising Adoption of Digital Pathology Workflows in Clinical and Research Settings

Digital Pathology (Whole Slide) Image Sensor Market is experiencing significant momentum driven by the accelerating shift from conventional glass slide-based pathology to fully digitized workflows. Whole slide imaging (WSI) systems, which depend on high-performance image sensors, are increasingly being integrated into hospital pathology departments, academic medical centers, and pharmaceutical research laboratories. The need for faster, more reproducible diagnostic processes has made high-resolution image sensors a foundational component of modern pathology infrastructure. Regulatory clearances from agencies such as the U.S. FDA for primary diagnostic use of whole slide imaging systems have further legitimized and accelerated institutional adoption.

Integration of Artificial Intelligence and Machine Learning with Whole Slide Imaging

One of the most transformative drivers shaping Digital Pathology (Whole Slide) Image Sensor Market is the deep integration of artificial intelligence and computational pathology platforms. AI-powered image analysis tools require high-fidelity, high-throughput image sensors capable of capturing gigapixel-level whole slide images with minimal optical distortion. As AI algorithms for tumor grading, biomarker quantification, and disease classification become more sophisticated, demand for sensors with superior dynamic range, color accuracy, and spatial resolution continues to intensify. Leading whole slide scanner manufacturers are investing in next-generation CMOS and TDI (Time Delay Integration) sensor technologies to meet these computational demands.

➤ The convergence of AI-driven computational pathology and advanced whole slide image sensor technology is redefining diagnostic accuracy benchmarks, positioning Digital Pathology (Whole Slide) Image Sensor Market at the intersection of medical imaging innovation and precision medicine.

Growing cancer incidence rates globally are also amplifying demand for efficient, scalable pathology solutions. With oncology representing one of the largest application segments for digital pathology, the pressure on pathology laboratories to process higher volumes of tissue samples with consistent quality is directly translating into investments in whole slide imaging infrastructure and, by extension, advanced image sensor components. Telepathology applications, which enable remote diagnosis and specialist consultation, further reinforce demand for reliable, high-performance image acquisition sensors capable of transmitting diagnostically accurate digital slides across healthcare networks.

MARKET CHALLENGES

High Capital Expenditure and Total Cost of Ownership in Whole Slide Imaging Systems

Despite strong growth prospects, Digital Pathology (Whole Slide) Image Sensor Market faces considerable challenges related to the high upfront costs associated with whole slide scanning systems. The image sensors embedded in these platforms represent a significant portion of the overall system cost, and their precision manufacturing requirements contribute to elevated price points that can restrict adoption among smaller diagnostic laboratories and healthcare facilities in cost-sensitive markets. Beyond acquisition costs, ongoing maintenance, calibration, and periodic sensor replacement further add to the total cost of ownership, creating financial barriers particularly in emerging economies where healthcare infrastructure investment remains constrained.

Other Challenges

Data Management and IT Infrastructure Demands

Whole slide images generated by high-resolution image sensors produce extremely large file sizes, often ranging from one to several gigabytes per slide. Managing, storing, and transmitting these data volumes requires robust IT infrastructure, including high-capacity servers, fast networking, and scalable storage solutions. Many healthcare institutions, particularly those in lower-resource settings, lack the IT ecosystem necessary to support a full digital pathology deployment, which indirectly limits the addressable market for whole slide image sensors. Interoperability between different scanner platforms and laboratory information systems also remains an ongoing technical challenge that affects broader market penetration.

Workflow Integration and Change Management

The transition from traditional histopathology workflows to digital pathology environments requires significant change management efforts within clinical laboratories. Pathologists and laboratory technicians must be trained to operate whole slide imaging systems and interpret digitized slides, which involves reskilling investments and temporary workflow disruptions. Resistance to workflow change among established pathology professionals, combined with the need to validate digital diagnostic outputs against legacy analog methods, represents a persistent non-technical barrier slowing the pace of adoption and, consequently, the expansion of Digital Pathology (Whole Slide) Image Sensor Market in certain institutional segments.

MARKET RESTRAINTS

Regulatory Complexity and Validation Requirements Across Global Markets

Regulatory heterogeneity across major geographies represents a notable restraint for Digital Pathology (Whole Slide) Image Sensor Market. While the United States and parts of Europe have established clearer regulatory pathways for digital pathology systems used in primary diagnosis, many other regions continue to operate under frameworks that do not yet formally recognize whole slide imaging for routine clinical use. This regulatory fragmentation creates uncertainty for manufacturers seeking to deploy image sensor-enabled WSI systems across international markets, extending time-to-market timelines and increasing compliance costs. The rigorous clinical validation studies required to demonstrate diagnostic equivalency between digital and optical microscopy further slow the pace at which new sensor technologies can be introduced into regulated clinical environments.

Technical Limitations in Sensor Performance for Specialized Tissue Types

Certain specialized pathology applications, including the imaging of thick tissue sections, immunofluorescence-stained slides, and rare staining protocols, continue to present technical challenges for current whole slide image sensor technologies. Achieving optimal focus, color fidelity, and signal-to-noise ratios across the full diversity of histological preparations requires continuous sensor innovation. In cases where existing sensor capabilities fall short of clinical requirements for specific tissue types or staining methodologies, laboratories may revert to or maintain parallel traditional microscopy workflows, partially restraining the completeness of digital pathology adoption and limiting the full-market potential available to image sensor manufacturers in Digital Pathology (Whole Slide) Image Sensor Market.

MARKET OPPORTUNITIES

Expansion of Digital Pathology in Pharmaceutical Research and Drug Development

The pharmaceutical and biotechnology sector represents a substantial and rapidly expanding opportunity for Digital Pathology (Whole Slide) Image Sensor Market. Drug development pipelines depend heavily on histopathological analysis of tissue samples during preclinical and clinical trial phases, and the adoption of whole slide imaging within these workflows is accelerating to improve throughput, reproducibility, and data auditability. Image sensors with enhanced throughput capabilities that can support high-volume batch scanning are increasingly valued by contract research organizations and large pharmaceutical companies seeking to digitize their pathology operations. The growing emphasis on biomarker-driven precision oncology trials is further expanding the application scope for high-performance whole slide image sensors within this segment.

Emerging Market Penetration and Telepathology Applications in Underserved Regions

Developing regions across Asia-Pacific, Latin America, and Sub-Saharan Africa present meaningful long-term growth opportunities for Digital Pathology (Whole Slide) Image Sensor Market, particularly as healthcare digitization initiatives gain policy support and funding. In areas facing acute shortages of trained pathologists, telepathology platforms enabled by whole slide imaging technology allow remote diagnostic consultations, effectively extending specialist pathology services to underserved populations. Governments and international health organizations increasingly recognize digital pathology infrastructure as a scalable solution to address diagnostic capacity gaps, creating a favorable policy environment for market expansion. As the cost of high-performance image sensor components gradually declines with advances in semiconductor manufacturing, whole slide imaging systems are expected to become accessible to a wider range of institutional buyers across these high-growth geographies.

Trends

Accelerating Adoption of Digital Pathology Workflows in Healthcare Systems

Healthcare systems worldwide are rapidly transitioning toward digitized pathology workflows, and this shift is among the most defining trends shaping Digital Pathology (Whole Slide) Image Sensor Market. Mounting pressure on pathology departments , driven by a global shortage of trained pathologists and an increasing volume of diagnostic cases , has compelled hospitals and diagnostic laboratories to adopt whole slide imaging systems at an accelerated pace. Digital pathology image sensors, engineered with advanced CMOS and CCD architectures, enable high-throughput tissue slide digitization with ultra-high resolution, large field-of-view scanning, and accurate color reproduction. These capabilities allow pathologists to interpret histological structures with greater precision while seamlessly integrating findings into broader digital health ecosystems, reducing turnaround times and improving diagnostic consistency across institutions.

Other Trends

Rising Cancer Incidence Driving Demand for Efficient Pathology Solutions

The sustained global rise in cancer incidence is a critical demand driver for Digital Pathology (Whole Slide) Image Sensor Market. As oncology case volumes expand, pathology departments require faster and more reliable diagnostic tools. Whole slide imaging systems equipped with high-resolution image sensors streamline tissue analysis workflows, enabling pathologists to manage higher caseloads without compromising diagnostic accuracy. This trend is prompting healthcare providers to prioritize investments in digital pathology infrastructure, further stimulating sensor technology innovation across the market.

Integration of AI-Assisted Diagnostics with Whole Slide Imaging

The convergence of artificial intelligence with whole slide imaging represents a transformative trend in Digital Pathology (Whole Slide) Image Sensor Market. AI-assisted diagnostic platforms rely on high-fidelity image data captured by advanced sensors to perform computational analysis of tissue samples, supporting pathologists in identifying disease markers with greater speed and objectivity. Broader regulatory approvals for AI-integrated pathology solutions are reinforcing this trend, improving clinical efficiency and data consistency across diagnostic workflows.

Intensified Industry Investment in High-Resolution Sensor Technologies

Leading companies in the digital pathology space have significantly intensified their investment in high-resolution sensor technologies. In 2023 and 2024, industry participants including Leica Biosystems, Hamamatsu Photonics, and Philips directed substantial resources toward enhancing scanning speed and image fidelity in whole slide imaging systems. These investments reflect a broader industry commitment to advancing sensor architectures that meet the evolving demands of clinical and research pathology applications.

Regulatory Approvals and Overcoming Implementation Cost Barriers

While high implementation costs have historically tempered adoption rates in Digital Pathology (Whole Slide) Image Sensor Market, increasing regulatory approvals for whole slide imaging systems are progressively addressing these barriers. As regulatory frameworks mature across key markets, healthcare institutions gain greater confidence in deploying digital pathology platforms. This regulatory momentum, combined with ongoing advancements in sensor performance and workflow integration capabilities, is strengthening the overall market outlook and supporting broader clinical adoption of whole slide imaging technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Digital Pathology (Whole Slide) Image Sensor Market: Competitive Dynamics and Leading Innovators Shaping the Future of Diagnostic Imaging

Global Digital Pathology (Whole Slide) Image Sensor Market is characterized by a moderately consolidated competitive landscape, with a handful of established technology leaders commanding significant market share while a broader set of specialized players drive innovation across niche segments. Hamamatsu Photonics, Leica Biosystems (a Danaher company), and Philips collectively represent some of the most influential forces in this space, having made substantial investments in high-resolution CMOS and CCD sensor architectures designed to deliver superior scanning speed, wide field-of-view capabilities, and accurate color reproduction essential for clinical-grade whole slide imaging. These companies benefit from deep integration across the digital pathology value chain , spanning sensor manufacturing, scanner systems, and AI-assisted diagnostic software , enabling them to offer comprehensive solutions to hospital networks, research institutions, and clinical laboratories worldwide. Their continued R&D focus through 2023 and 2024 has further reinforced competitive barriers, as proprietary sensor technologies become increasingly differentiated in terms of image fidelity and workflow efficiency.

Beyond the dominant players, the competitive landscape features a dynamic mix of optical sensor specialists, life science imaging companies, and emerging digital pathology solution providers that address specific workflow and performance requirements. Companies such as Sony Semiconductor Solutions and Teledyne Technologies leverage their advanced imaging sensor expertise to supply critical components to whole slide scanner manufacturers, while Olympus Corporation and Zeiss (Carl Zeiss AG) bring strong optical engineering heritage to the sector. Meanwhile, firms like Aperio (Leica Biosystems), Ventana Medical Systems (Roche), and 3DHISTECH are actively expanding their whole slide imaging portfolios in response to growing cancer screening demand and the accelerating integration of AI-driven diagnostic tools. The increasing number of regulatory approvals for digital pathology platforms across North America, Europe, and Asia-Pacific is intensifying competitive activity, encouraging both established incumbents and new entrants to invest in next-generation image sensor technologies that meet the rigorous standards required for primary diagnosis and clinical decision-making.

List of Key Digital Pathology (Whole Slide) Image Sensor Companies Profiled

- Hamamatsu Photonics K.K.

- Leica Biosystems (Danaher Corporation)

- Philips Digital Pathology Solutions

- Ventana Medical Systems (Roche)

- Sony Semiconductor Solutions Corporation

- Teledyne Technologies Incorporated

- Olympus Corporation

- Carl Zeiss AG (ZEISS)

- 3DHISTECH Ltd.

- Mikroscan Technologies Inc.

- Grundium Oy

- Objective Pathology Services

- ON Semiconductor (onsemi)

- Imperx Inc.

- Photonis Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

CMOS Image Sensors represent the leading segment in the digital pathology whole slide imaging sensor market, driven by a combination of technological superiority and operational advantages that make them the preferred choice for next-generation whole slide imaging (WSI) systems.

CCD sensors, while comparatively mature in their development trajectory, continue to serve niche applications where exceptional signal-to-noise ratios and uniform pixel response are prioritized over scanning speed, particularly in highly specialized research and academic settings. |

| By Application |

|

Clinical Diagnostics stands as the dominant application segment, reflecting the central role that whole slide image sensors play in transforming conventional anatomical pathology workflows into fully digitized, AI-compatible diagnostic pipelines.

Drug discovery and pharmaceutical research represent a rapidly expanding application area as biopharmaceutical companies increasingly rely on digital pathology workflows to accelerate histopathological analysis during preclinical and clinical trial phases. Teleconsultation is also gaining traction as healthcare systems seek to bridge the gap created by Global shortage of trained pathologists. |

| By End User |

|

Hospitals & Clinical Laboratories constitute the leading end-user segment, underpinned by the accelerating transition from traditional glass slide-based pathology to fully digital workflows within mainstream healthcare delivery systems.

Pharmaceutical and biotechnology companies represent a strategically significant end-user group as they leverage whole slide imaging for tissue-based biomarker research and companion diagnostic development. Academic and research institutes continue to drive sensor innovation by providing a testing ground for emerging imaging technologies and novel AI-based analytical approaches. |

| By Scanning Technology |

|

Brightfield Scanning remains the dominant scanning technology segment, owing to its direct compatibility with the most widely used histological staining protocols such as hematoxylin and eosin staining, which remain the cornerstone of routine clinical pathology practice worldwide.

Multispectral and hyperspectral scanning technologies are attracting considerable research interest as they enable simultaneous capture of tissue information across multiple wavelength bands, opening new avenues for quantitative pathology and AI-based tissue phenotyping that go well beyond the capabilities of conventional staining approaches. |

| By Integration Mode |

|

AI-Integrated Digital Pathology Platforms are rapidly emerging as the most strategically significant integration mode segment, reflecting a broader industry shift toward intelligent, data-driven pathology workflows that leverage whole slide image sensor outputs as the foundational input for machine learning-based diagnostic decision support.

The convergence of sensor hardware innovation with AI software platforms and cloud infrastructure is fundamentally reshaping how pathology services are delivered, making integration mode an increasingly critical dimension for market participants seeking to differentiate their offerings and capture evolving customer needs. |

Regional Analysis: Digital Pathology (Whole Slide) Image Sensor Market

North America

Regulatory clearances from agencies such as the FDA have been pivotal in advancing the clinical adoption of whole slide imaging in North America. Laboratories are increasingly leveraging approved digital pathology platforms for primary diagnosis, quality assurance, and tumor board consultations, embedding high-performance image sensors into standard clinical practice with growing institutional confidence and reimbursement pathways becoming more clearly defined.

North America leads globally in the convergence of artificial intelligence with whole slide image sensor technology. Research hospitals and commercial pathology labs are actively deploying AI-assisted image analysis tools that rely on high-fidelity sensor outputs for automated tissue classification, biomarker quantification, and predictive oncology applications, creating a compounding demand cycle for next-generation imaging sensor capabilities across the region.

The expansion of telepathology services across North America, accelerated by shifts in healthcare delivery models post-pandemic, has substantially increased demand for reliable whole slide image sensor systems. Rural and underserved healthcare facilities increasingly rely on digitized slides transmitted to centralized expert pathologists, reinforcing the strategic importance of robust, high-resolution image sensor technology in sustaining diagnostic accuracy across distributed networks.

Pharmaceutical companies and contract research organizations headquartered across North America are significant consumers of digital pathology whole slide imaging solutions for preclinical and clinical trial applications. The demand for high-throughput, reproducible tissue analysis in drug development pipelines drives sustained investment in advanced image sensor platforms, with biopharma partnerships further stimulating innovation and commercial deployment across the region.

Europe

Europe represents the second most significant regional market within the digital pathology whole slide image sensor industry, characterized by a strong tradition of pathology excellence and progressive national digitization strategies. Countries including Germany, the Netherlands, the United Kingdom, and the Nordic nations have emerged as frontrunners in implementing institution-wide digital pathology programs, with several national health systems actively transitioning toward fully digital laboratory environments. European regulatory frameworks under the In Vitro Diagnostic Regulation have introduced more structured pathways for validating and deploying digital pathology tools clinically, creating both compliance imperatives and growth opportunities for image sensor technology providers. Academic-industry collaborations across Europe remain particularly active, with research consortia exploring the application of whole slide imaging in precision oncology, rare disease diagnosis, and population health studies. The presence of globally recognized pathology equipment manufacturers and imaging technology companies within the region further strengthens Europe’s capacity for innovation and market expansion through 2034.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market for digital pathology whole slide image sensor technology, propelled by rapid healthcare modernization, expanding diagnostic infrastructure, and significant government investment in hospital digitization across major economies. China, Japan, South Korea, and Australia are the primary contributors to regional market momentum, each presenting distinct growth narratives. China’s large patient population and aggressive healthcare reform agenda are catalyzing widespread adoption of digital pathology platforms across tertiary hospitals and centralized diagnostic centers. Japan’s precision medicine initiatives and technologically sophisticated healthcare ecosystem support advanced whole slide imaging deployments, while South Korea’s strong semiconductor and imaging technology base creates a favorable environment for local innovation. Australia’s geographically dispersed healthcare network drives demand for telepathology solutions dependent on high-quality image sensors, further reinforcing regional growth trajectories in the digital pathology whole slide image sensor market.

South America

South America occupies an emerging position within Global digital pathology whole slide image sensor market, with growth primarily concentrated in Brazil, Argentina, and Colombia. The region is witnessing gradual but meaningful adoption of digital pathology solutions within private hospital networks, university research centers, and cancer reference institutions that recognize the diagnostic and operational advantages of whole slide imaging technology. Brazil, as the region’s largest healthcare market, is driving the majority of demand, supported by growing awareness among pathologists, increasing availability of training programs, and the entry of international digital pathology vendors into local distribution channels. Infrastructure challenges, including inconsistent connectivity in certain areas and budget constraints within public health systems, present barriers to broader adoption; however, the expanding private healthcare sector and international funding for oncology research programs are providing incremental momentum for whole slide image sensor market development across the region.

Middle East & Africa

The Middle East and Africa region represents an nascent but progressively developing market within the digital pathology whole slide image sensor landscape. The Gulf Cooperation Council countries, particularly the United Arab Emirates and Saudi Arabia, are leading adoption within the Middle East, underpinned by ambitious national healthcare transformation programs, investment in smart hospital infrastructure, and growing medical tourism ecosystems that demand cutting-edge diagnostic capabilities. Digital pathology whole slide imaging is being incorporated into newly constructed and technologically advanced hospital facilities across the Gulf, reflecting a broader commitment to world-class diagnostics. In Africa, adoption remains at an early stage, though initiatives focused on improving cancer diagnosis in Sub-Saharan Africa are creating awareness of digital pathology’s potential to address specialist workforce shortages through telepathology applications. As healthcare investment continues to rise across both sub-regions, the Middle East and Africa market for digital pathology whole slide image sensor technology is expected to gather increasing momentum through the 2026–2034 forecast period.

Report Scope

This market research report provides a comprehensive analysis of the Digital Pathology (Whole Slide) Image Sensor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of image sensor technologies in powering advancements across industries such as healthcare diagnostics, clinical pathology, research laboratories, and digital imaging.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, sensor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Digital Pathology (Whole Slide) Image Sensor Market?

-> Global Digital Pathology (Whole Slide) Image Sensor Market size was valued at USD 0.74 billion in 2025. The market is projected to grow from USD 0.82 billion in 2026 to USD 1.80 billion by 2034, exhibiting a CAGR of 10.4% during the forecast period.

Which key companies operate in Digital Pathology (Whole Slide) Image Sensor Market?

-> Key players include Leica Biosystems, Hamamatsu Photonics, and Philips, among others, which have intensified investments in high-resolution sensor technologies to enhance scanning speed and image fidelity.

What are the key growth drivers?

-> Key growth drivers include accelerating adoption of digital pathology by healthcare systems worldwide, rising cancer incidence increasing demand for efficient pathology workflows, advancements in whole slide imaging systems, increasing regulatory approvals, and broader integration of AI-assisted diagnostics that improve clinical efficiency and data consistency.

Which region dominates the market?

-> Asia-Pacific is among the fastest-growing regions, while North America and Europe remain dominant markets driven by advanced healthcare infrastructure and early adoption of digital pathology technologies.

What are the emerging trends?

-> Emerging trends include AI-assisted diagnostics integration, advanced CMOS and CCD sensor architectures, large field-of-view scanning capabilities, high dynamic range imaging, and accurate color reproduction technologies critical for clinical interpretation of histological structures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...