MARKET INSIGHTS

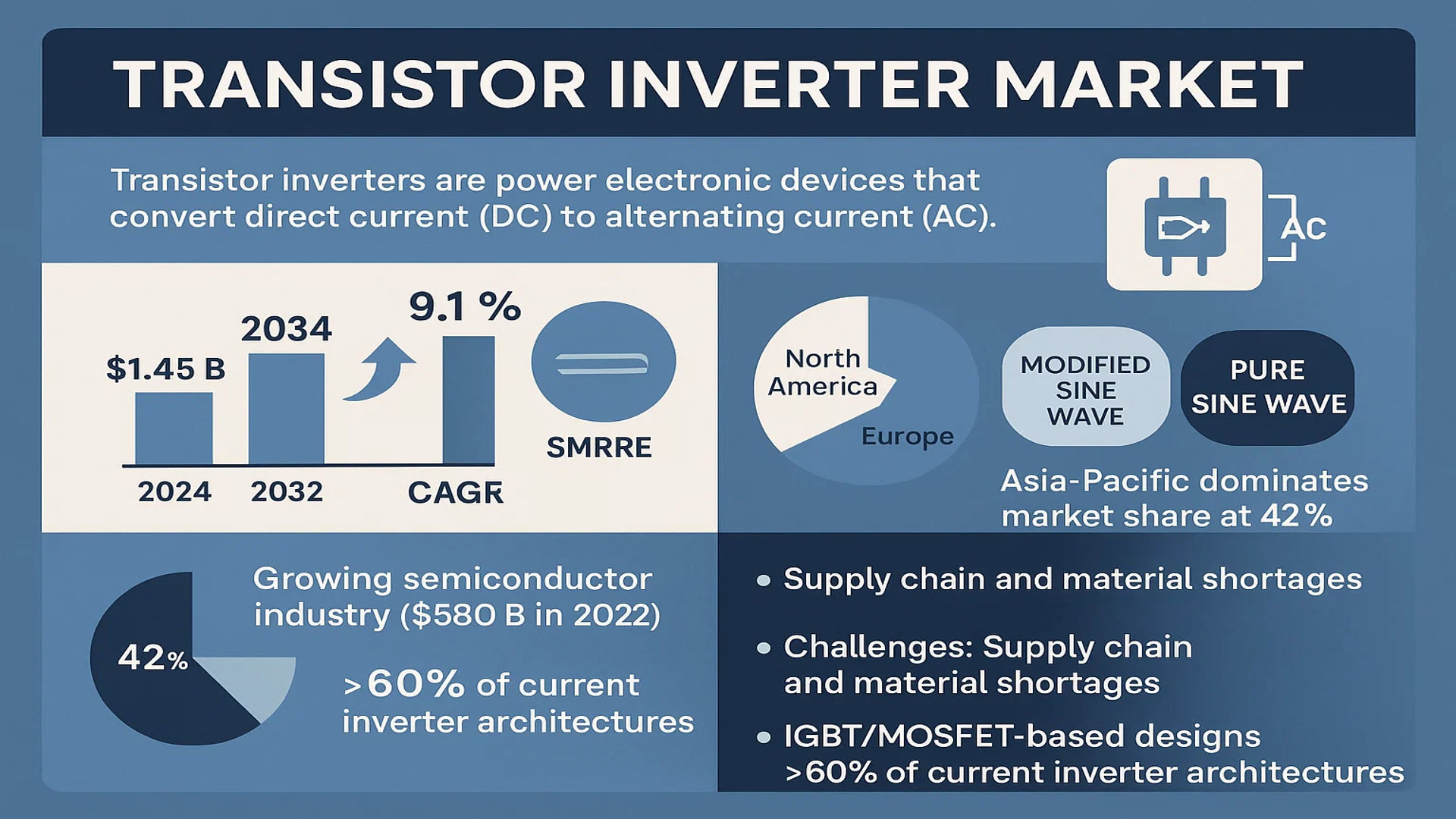

The global Transistor Inverter Market size was valued at US$ 1.45 billion in 2024 and is projected to reach US$ 2.67 billion by 2032, at a CAGR of 9.1% during the forecast period 2025-2032.

Transistor inverters are power electronic devices that convert direct current (DC) to alternating current (AC). These semiconductor-based systems are fundamental components in applications ranging from industrial motor drives to renewable energy systems and consumer electronics. The market is segmented into modified sine wave and pure sine wave inverters, with the latter gaining traction due to superior power quality and compatibility with sensitive electronics.

While the Asia-Pacific region currently dominates market share at 42%, North America and Europe are witnessing accelerated adoption in electric vehicle charging infrastructure. The growing semiconductor industry, which reached USD 580 billion globally in 2022, provides a strong foundation for inverter component availability. However, supply chain disruptions and material shortages pose challenges, particularly for IGBT and MOSFET-based designs that constitute over 60% of current inverter architectures.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Energy-Efficient Electronics Strengthens Transistor Inverter Adoption

The global push toward energy efficiency is accelerating demand for advanced power conversion technologies like transistor inverters. With electronic devices consuming approximately 15% of global electricity, manufacturers are increasingly adopting efficient inverter solutions to reduce power losses. The transition from traditional mechanical inverters to solid-state transistor-based systems has demonstrated efficiency improvements of up to 30%, making them indispensable in modern power electronics. This shift is particularly evident in consumer electronics, where strict energy regulations continue to tighten worldwide.

Expanding Renewable Energy Sector Fuels Market Expansion

Global renewable energy capacity additions reached approximately 295 GW in 2022, creating unprecedented demand for power conversion equipment. Transistor inverters serve as critical components in solar photovoltaic systems and wind power installations, converting DC to AC power with minimal energy loss. The solar inverter market alone is projected to maintain a compound annual growth rate of over 5% through 2030, directly benefiting transistor inverter manufacturers. As governments worldwide accelerate renewable energy deployment to meet decarbonization targets, this segment continues to drive significant market growth.

Automotive Electrification Creates New Application Horizons

The electric vehicle revolution is reshaping power electronics demand, with transistor inverters playing a pivotal role in traction motor control systems. With electric car sales surpassing 10 million units globally in 2022, automotive inverters have emerged as a high-growth segment. Advanced wide-bandgap semiconductor materials are enabling inverter systems that are up to 30% smaller and 50% more efficient than conventional designs. This technological evolution, combined with the automotive industry’s rapid electrification timeline, positions transistor inverters for sustained market expansion.

MARKET RESTRAINTS

Supply Chain Vulnerabilities Challenge Production Consistency

The semiconductor shortage crisis exposed critical vulnerabilities in the transistor inverter supply chain. With approximately 70% of power semiconductor production concentrated in Asia, geopolitical tensions and trade restrictions have created substantial market uncertainties. Lead times for certain high-performance IGBT modules extended beyond 52 weeks during the peak of the shortage, forcing manufacturers to delay production schedules. This concentration risk continues to restrain market growth potential as companies work to establish more resilient supply networks.

Thermal Management Limitations Impact Performance Thresholds

While transistor inverters offer superior efficiency, thermal dissipation remains a significant technical constraint. Power densities in modern inverters frequently exceed 100W/cm², pushing existing cooling solutions to their operational limits. Approximately 20% of inverter failures are attributed to thermal stress, creating reliability concerns in mission-critical applications. The industry faces mounting pressure to develop advanced thermal interface materials and cooling architectures that can support next-generation power requirements without compromising size or cost targets.

MARKET OPPORTUNITIES

Wide Bandgap Semiconductor Adoption Opens New Frontiers

The transition to silicon carbide (SiC) and gallium nitride (GaN) power devices represents a transformative opportunity for the transistor inverter market. Wide bandgap semiconductors enable inverter systems that operate at higher temperatures, voltages, and switching frequencies. Industry adoption rates for these advanced materials are accelerating, with SiC-based inverter sales growing at nearly 30% annually. This technological shift is particularly impactful in electric vehicle powertrains and industrial motor drives, where efficiency gains translate directly into competitive advantages.

Smart Grid Modernization Drives Innovation Demand

Global investments in smart grid infrastructure surpassed $50 billion in 2023, creating significant opportunities for intelligent inverter solutions. Modern grid-tied inverters increasingly incorporate advanced features like reactive power control, fault ride-through capability, and grid-forming functionality. This evolution aligns with renewable integration requirements and distributed energy resource management needs. As utilities worldwide prioritize grid modernization, the demand for sophisticated transistor inverter systems with enhanced communication and control capabilities continues to expand.

MARKET CHALLENGES

Design Complexity Increases Time-to-Market Pressures

The relentless demand for higher power density and efficiency has dramatically increased inverter design complexity. Developing optimized gate driver circuits, achieving effective electromagnetic interference (EMI) suppression, and implementing robust protection mechanisms require extensive engineering resources. Many manufacturers report product development cycles extending beyond 24 months for advanced inverter platforms, making it challenging to keep pace with rapidly evolving market requirements and technology standards.

Cost Competition Intensifies Across Application Segments

While premium applications like automotive and industrial sectors tolerate higher inverter costs, consumer markets remain extremely price-sensitive. Chinese manufacturers have captured significant market share by offering inverter solutions at 30-40% lower price points than European and American counterparts. This pricing pressure forces established players to optimize manufacturing processes and supply chain strategies while maintaining quality standards, creating ongoing profitability challenges across the industry.

TRANSISTOR INVERTER MARKET TRENDS

Rising Demand for Energy-Efficient Power Conversion Solutions Driving Market Growth

The global transition toward energy-efficient technologies continues to bolster demand for transistor inverters, particularly in industrial and consumer applications. The market, valued at several million dollars in 2024, is projected to exhibit steady growth as industries prioritize power optimization and renewable energy integration. With a compound annual growth rate (CAGR) expected to remain in the single digits, manufacturers are focusing on high-performance insulated-gate bipolar transistors (IGBTs) and silicon carbide (SiC) MOSFETs, which offer superior switching efficiency compared to traditional silicon-based components. The semiconductor industry’s resilience, despite global economic fluctuations, ensures a stable supply chain for these critical components, with regional markets such as the Americas and Europe showing double-digit growth in semiconductor sales.

Other Trends

Expansion of Renewable Energy Infrastructure

As governments and corporations accelerate investments in renewable energy, transistor inverters—key components in solar and wind power systems—are witnessing heightened adoption. The shift from centralized power generation to distributed energy resources necessitates advanced inverters capable of handling variable loads with minimal energy loss. For instance, modern pure sine wave inverters are increasingly favored in photovoltaic systems due to their ability to deliver stable AC power with reduced harmonic distortion. Meanwhile, the Asia-Pacific region, despite a recent temporary slowdown, remains a dominant force in semiconductor production, supporting local and global inverter manufacturing.

Technological Advancements in Semiconductor Materials

Innovations in semiconductor materials, including the wider adoption of gallium nitride (GaN) and silicon carbide, are reshaping the transistor inverter landscape. These materials enable higher switching frequencies and lower thermal losses, making them ideal for electric vehicles (EVs) and high-power industrial applications. While SiC-based inverters currently account for a smaller market share, their penetration is growing rapidly due to superior breakdown voltage and efficiency in high-temperature environments. Concurrently, the integration of smart features—such as real-time monitoring and AI-driven predictive maintenance—is transforming inverters into intelligent power management systems, further expanding their applications in IoT-enabled environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Semiconductor Firms Compete Through Innovation and Strategic Expansion

The global transistor inverter market remains highly competitive, dominated by established semiconductor manufacturers and emerging specialized players. Infineon Technologies leads the market with its advanced power semiconductor solutions, holding an estimated 18% revenue share in 2024. The company’s strong position stems from its vertically integrated manufacturing capabilities and broad product portfolio catering to automotive, industrial, and consumer electronics applications.

ABB and Vishay Intertechnology constitute the second-tier leaders, collectively accounting for approximately 25% market share. Both companies have strategically expanded their transistor inverter offerings through acquisitions and technological partnerships. ABB’s recent $2.9 billion investment in power electronics R&D highlights the growing importance of energy-efficient inverter solutions.

Meanwhile, mid-sized competitors like Powerex and Littelfuse are gaining traction by focusing on niche applications. Powerex has successfully penetrated the renewable energy sector, while Littelfuse’s acquisition of IXYS Corporation significantly strengthened its power semiconductor portfolio. These developments indicate an industry trend towards specialization within the transistor inverter space.

The competitive landscape continues evolving as Chinese manufacturers like Jiangsu Yangjie Runau Semiconductor increase production capabilities. With China accounting for 40% of global semiconductor consumption, domestic suppliers are well-positioned to capture market share through cost-competitive offerings. However, quality concerns and geopolitical factors may constrain their global expansion in the short term.

List of Key Transistor Inverter Manufacturers

- Infineon Technologies AG (Germany)

- ABB Ltd. (Switzerland)

- Vishay Intertechnology, Inc. (U.S.)

- Powerex Inc. (U.S.)

- Littelfuse, Inc. (U.S.)

- Rosen Technology (Germany)

- Jiangsu Yangjie Runau Semiconductor Co. (China)

- NFE Corporation (Japan)

- TTI, Inc. (U.S.)

- Poseico Electronics (South Korea)

Segment Analysis:

By Type

Pure Sine Wave Segment Leads the Market Due to Superior Performance in Sensitive Electronics

The market is segmented based on type into:

- Modified Sine Wave

- Subtypes: Low Frequency, High Frequency, and others

- Pure Sine Wave

- Subtypes: Single Phase, Three Phase, and others

- Others

By Application

Electronics Industry Segment Dominates Owing to Expanding Consumer Electronics Market

The market is segmented based on application into:

- Electronics Industry

- Subtypes: Consumer Electronics, Industrial Electronics, and others

- Communications Industry

- Subtypes: Telecommunication Equipment, Networking Devices, and others

- Others

By Power Rating

Medium Power Segment Shows Significant Growth for Industrial Applications

The market is segmented based on power rating into:

- Low Power (up to 1 kW)

- Medium Power (1 kW to 5 kW)

- High Power (above 5 kW)

By Technology

IGBT Technology Holds Major Share Due to High Efficiency in Power Conversion

The market is segmented based on technology into:

- MOSFET

- IGBT

- Bipolar Transistor

- Others

Regional Analysis: Transistor Inverter Market

North America

The North American transistor inverter market is driven by technological advancements and substantial investments in renewable energy integration. The U.S. leads the region with a robust semiconductor industry, accounting for approximately 32% of global semiconductor sales. The increasing demand for energy-efficient power conversion systems in industries such as automotive, telecommunications, and industrial automation is propelling market growth. Government initiatives like the CHIPS and Science Act, which allocates $52 billion for domestic semiconductor manufacturing, further solidify market expansion. However, supply chain disruptions and high production costs remain challenges for manufacturers.

Europe

Europe’s transistor inverter market is characterized by stringent energy efficiency regulations and a strong emphasis on sustainability. The EU’s commitment to achieving net-zero emissions by 2050 has accelerated the adoption of advanced inverter technologies in solar and wind energy applications. Germany and France dominate the regional market, supported by their well-established automotive and industrial sectors. The demand for pure sine wave inverters is rising in residential and commercial applications due to their superior performance. While the market is growing, competition from Asian manufacturers and complex regulatory frameworks pose challenges for local players.

Asia-Pacific

As the largest and fastest-growing market for transistor inverters, the Asia-Pacific region benefits from rapid industrialization and urbanization. China, Japan, and South Korea are key contributors, leveraging their strong semiconductor manufacturing capabilities. The region’s dominance in consumer electronics and electric vehicle production fuels demand for efficient power conversion solutions. However, price sensitivity and the prevalence of low-cost alternatives hinder the widespread adoption of high-end inverter technologies. Despite this, government incentives for renewable energy projects and smart grid development continue to drive long-term growth.

South America

South America’s transistor inverter market is emerging, with Brazil and Argentina leading regional demand. The growth is primarily driven by expanding telecommunications infrastructure and increasing investments in renewable energy projects. While the market is still in its nascent stage, the rising adoption of solar energy systems offers significant opportunities. Economic instability and inconsistent regulatory policies, however, create uncertainties for investors. Local manufacturers face challenges in competing with imported products, but partnerships with global players could help bridge the technological gap.

Middle East & Africa

The Middle East & Africa region is witnessing gradual growth in the transistor inverter market, driven by infrastructure development and renewable energy initiatives. Countries like Saudi Arabia, the UAE, and South Africa are investing heavily in solar power plants and smart city projects. While the lack of local manufacturing capabilities and reliance on imports slow down market expansion, increasing foreign investments and government support for clean energy are expected to accelerate adoption. The market’s long-term potential remains high, particularly in off-grid and hybrid power solutions.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Transistor Inverter markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Modified Sine Wave, Pure Sine Wave), application (Electronics Industry, Communications Industry, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis for key markets.

- Competitive Landscape: Profiles of leading market participants including ABB, Infineon, Vishay, and Powerex, covering product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of semiconductor design advancements, power efficiency improvements, and integration with smart grid technologies.

- Market Drivers & Restraints: Evaluation of factors including renewable energy adoption, industrial automation growth, and supply chain challenges.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, component suppliers, system integrators, and investors.

The research methodology combines primary interviews with industry experts and analysis of verified market data from authoritative sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Transistor Inverter Market?

-> Transistor Inverter Market size was valued at US$ 1.45 billion in 2024 and is projected to reach US$ 2.67 billion by 2032, at a CAGR of 9.1% during the forecast period 2025-2032.

Which key companies operate in Global Transistor Inverter Market?

-> Key players include ABB, Infineon, Vishay, Powerex, Littelfuse, and Rosen Technology, collectively holding over 45% market share.

What are the key growth drivers?

-> Key growth drivers include rising demand for renewable energy systems, industrial automation, and increasing adoption of power electronics in consumer devices.

Which region dominates the market?

-> Asia-Pacific accounts for 42% of global demand, led by China’s electronics manufacturing sector, while North America shows strong growth in industrial applications.

What are the emerging trends?

-> Emerging trends include wide-bandgap semiconductors (SiC/GaN), smart inverters with IoT connectivity, and miniaturization of power electronics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...