MARKET INSIGHTS

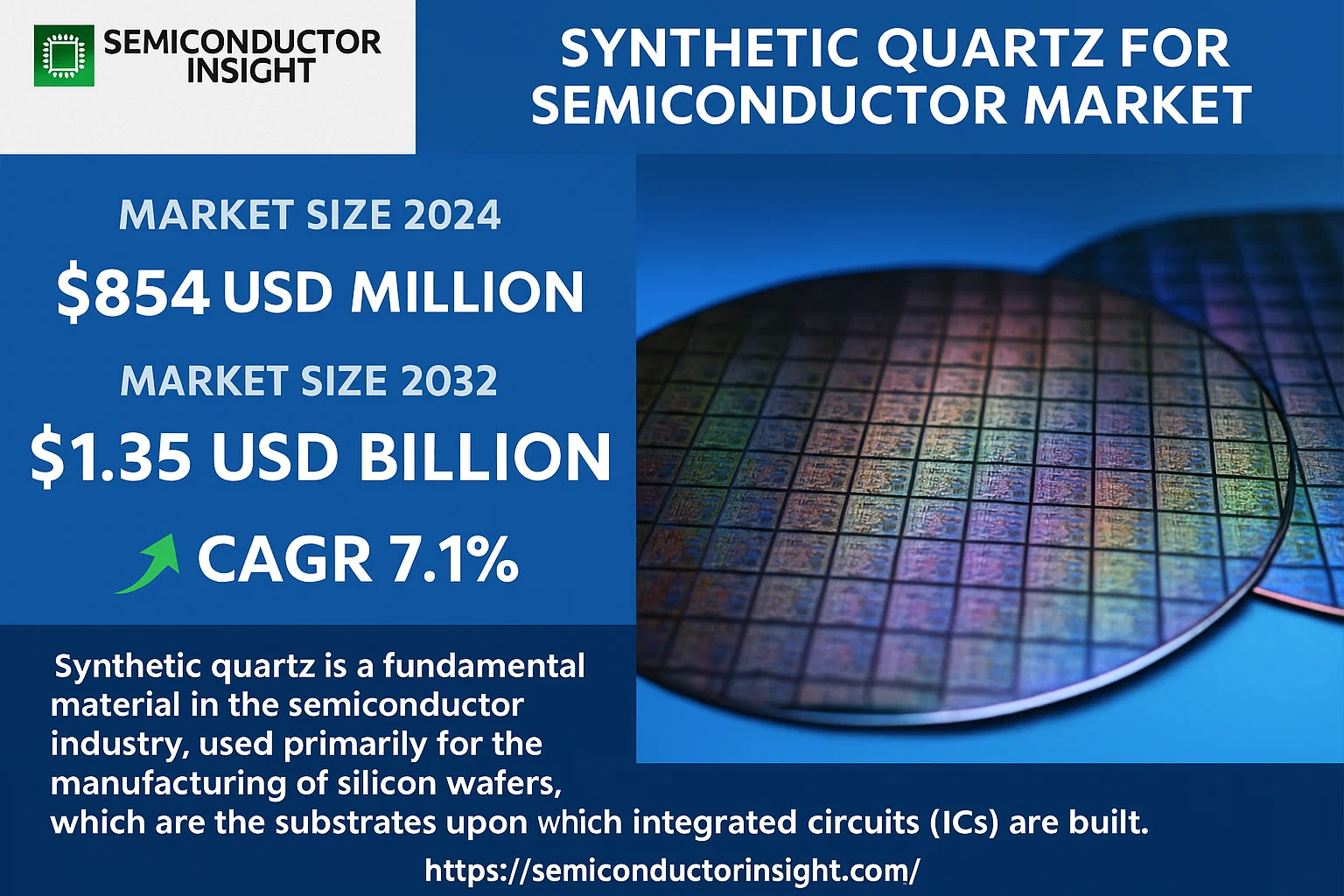

Global Synthetic Quartz for Semiconductor Market size was valued at USD 854 million in 2024 and is projected to reach USD 1.35 billion by 2032, exhibiting a CAGR of 7.1% during the forecast period.

Synthetic quartz is a fundamental material in the semiconductor industry, used primarily for the manufacturing of silicon wafers, which are the substrates upon which integrated circuits (ICs) are built. The market for synthetic quartz has seen significant growth over the years, driven by the increasing demand for semiconductors in various applications, including consumer electronics, automotive, healthcare, and industrial sectors.

The market is experiencing rapid growth due to several factors, including increased investment in semiconductor manufacturing capacity globally, the ongoing digital transformation across industries, and the rising demand for high-performance computing and artificial intelligence applications. Additionally, the growing demand for and advancements in semiconductor fabrication technologies such as extreme ultraviolet lithography (EUV) are contributing to market expansion. Initiatives by the key players in the market are also expected to fuel the market growth. For instance, in the semiconductor industry, companies like TSMC, Samsung, and Intel are investing heavily in advanced fabrication facilities that require high-purity quartz components.

MARKET DRIVERS

Rising Demand for Advanced Semiconductor Nodes

The global push towards smaller semiconductor process nodes, such as 5nm and 3nm, is a primary driver for the synthetic quartz market. These advanced fabrication processes require extreme precision and thermal stability during photolithography, where high-purity synthetic quartz components like photomasks and lenses are essential. The material’s superior properties, including low thermal expansion and high ultraviolet transmission, make it indispensable for producing next-generation chips used in artificial intelligence, high-performance computing, and 5G devices.

Expansion of the Semiconductor Industry

Global investments in new semiconductor fabrication plants, particularly in regions like the United States, Taiwan, South Korea, and Europe, are significantly boosting demand for synthetic quartz. Government initiatives and private investments totaling hundreds of billions of dollars are expanding manufacturing capacity. This expansion directly increases the consumption of synthetic quartz for critical equipment such as etching chambers, diffusion tubes, and wafer carriers, which must withstand harsh processing environments.

➤ The market for synthetic quartz is projected to grow at a CAGR of approximately 7-9% over the next five years, driven by sustained demand from the semiconductor sector.

Additionally, the ongoing miniaturization of electronic components and the proliferation of Internet of Things (IoT) devices are creating sustained, long-term demand for the high-performance materials provided by synthetic quartz, ensuring its position as a critical enabler of modern electronics manufacturing.

MARKET CHALLENGES

High Production Costs and Complex Manufacturing

The synthesis of high-purity quartz involves energy-intensive processes, such as the hydrothermal method, which requires precise control of high temperature and pressure. The capital expenditure for establishing manufacturing facilities is substantial, and the expertise needed for consistent production is limited to a few specialized companies globally. This results in high product costs, which can be a significant barrier for smaller semiconductor manufacturers and can impact the overall cost structure of chip production.

Other Challenges

Supply Chain Vulnerabilities

The market is characterized by a concentrated supply base, with a few key players dominating production. This concentration creates vulnerabilities, where geopolitical tensions, trade restrictions, or logistical disruptions can lead to supply shortages and price volatility, directly impacting semiconductor fabrication schedules and costs.

Technical Performance Requirements

As semiconductor technology advances, the specifications for synthetic quartz become increasingly stringent. Meeting demands for even lower defect densities, higher purity levels (e.g., >99.99%), and improved thermal stability requires continuous R&D investment, posing a constant challenge for material suppliers to keep pace with the evolving needs of chipmakers.

MARKET RESTRAINTS

Cyclical Nature of the Semiconductor Industry

The synthetic quartz market is heavily dependent on the capital expenditure cycles of the semiconductor industry. During periods of economic downturn or reduced demand for end-user electronics, semiconductor manufacturers delay or cancel investments in new equipment and capacity expansion. This leads to a direct and immediate reduction in demand for synthetic quartz components, creating significant revenue volatility for material suppliers and restraining steady market growth.

Emergence of Alternative Materials

While synthetic quartz has dominant properties, ongoing research into alternative materials, such as specialized ceramics or advanced glasses, presents a restraint. These materials are being developed to offer comparable or superior performance in specific applications, potentially at a lower cost. Although substitution is not yet widespread, the threat of alternative solutions encourages price competition and requires quartz suppliers to continuously demonstrate the unique value of their product.

MARKET OPPORTUNITIES

Growth in Compound Semiconductors and Power Electronics

The increasing adoption of gallium nitride (GaN) and silicon carbide (SiC) for power electronics and electric vehicles presents a significant growth avenue. The manufacturing of these compound semiconductors involves high-temperature processes where synthetic quartz components, such as crucibles and reactors, are critical. This emerging segment offers suppliers the opportunity to diversify their customer base beyond traditional silicon-based chipmakers.

Advanced Packaging Technologies

Innovations in semiconductor packaging, including 2.5D and 3D integration, require new tools and processes that utilize high-performance materials. Synthetic quartz is finding applications in temporary carrier wafers and interposer fabrication for these advanced packages. As the industry moves beyond Moore’s Law through packaging innovations, the demand for specialized quartz products is expected to create substantial new market opportunities.

Synthetic Quartz for Semiconductor Market Trends

Accelerated Growth Driven by Semiconductor Demand

The global Synthetic Quartz for Semiconductor market is experiencing robust expansion, with its value projected to grow from $854 million in 2024 to approximately $1350 million by 2032, reflecting a compound annual growth rate (CAGR) of 7.1%. This growth is fundamentally linked to the pervasive demand for semiconductors across critical sectors such as consumer electronics, automotive, and industrial automation. As the essential substrate material for silicon wafers, synthetic quartz is indispensable to the fabrication of integrated circuits, positioning it at the core of technological advancement.

Other Trends

Rising Demand for High-Purity and Specialized Quartz

A dominant trend is the escalating requirement for high-purity synthetic quartz capable of withstanding extreme temperatures and aggressive chemical environments inherent in advanced semiconductor manufacturing. This is directly tied to the industry’s relentless push for device miniaturization and enhanced performance. Concurrently, there is a significant trend toward the development and adoption of specialized quartz types, such as fused quartz and synthetic fused silica, which offer superior properties like minimal thermal expansion and high transmission of ultraviolet light, which are critical for advanced lithography processes.

Geographical Shifts and Application-Driven Expansion

The Asia-Pacific region, particularly manufacturing powerhouses like China, South Korea, and Taiwan, dominates the consumption of synthetic quartz, driven by its concentration of semiconductor fabrication plants. Furthermore, major technological shifts are creating new growth vectors. The global rollout of 5G infrastructure and the proliferation of Internet of Things (IoT) devices are significantly increasing the semiconductor content in numerous applications. Similarly, the automotive industry’s transformation, marked by the rise of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), is fueling demand for more sophisticated semiconductors, thereby stimulating the market for high-quality synthetic quartz substrates used in their production.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Concentration and Strategic Dynamics in the High-Purity Arena

The global synthetic quartz market for semiconductors is characterized by a high level of concentration, with a few major global players commanding significant market share. Heraeus, a German technology group, consistently ranks as a dominant force. Its advanced fused silica products are critical for extreme ultraviolet (EUV) lithography, positioning it as a key enabler for the most advanced semiconductor nodes. Similarly, Japanese giants like Tosoh and Shin-Etsu Chemical have established a strong foothold through decades of material science expertise and deep integration with the semiconductor supply chain. The market structure is oligopolistic, where competition revolves around technological superiority, product purity, consistency, and the ability to scale production to meet the massive demands of leading foundries and integrated device manufacturers.

While the top-tier players shape the market’s direction, several other significant companies compete effectively in niche segments or specific geographic regions. AGC, another major Japanese corporation, and CoorsTek from the US provide vital materials for various semiconductor fabrication steps. Nikon and Ohara leverage their expertise in optics to produce high-grade quartz for lithography lenses. In China, Feilihua Quartz and Yangtze Optical Fibre and Cable (YOFC) have become increasingly important suppliers, supported by the country’s push for semiconductor self-sufficiency. These and other players compete by focusing on specialized quartz types, such as those produced by Chemical Vapor Deposition (CVD) or Vapor-phase Axial Deposition (VAD), and by forming strategic partnerships with equipment manufacturers.

List of Key Synthetic Quartz for Semiconductor Companies Profiled

- Heraeus

- AGC

- Tosoh

- Feilihua

- Nikon

- Shin-Etsu

- Ohara

- CoorsTek

- Yangtze Optical Fibre and Cable

- Raesch Quarz

- Momentive Performance Materials

- QSIL

- Pacific Quartz

- Jiangsu Pacific Quartz

- Nippon Electric Glass

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

CVD is the dominant production method, favored for its ability to produce quartz with exceptionally high purity and excellent transmission properties for ultraviolet light, which is critical for advanced photolithography processes. The VAD segment is also significant, offering specific material properties required for high-performance applications, while the ‘Others’ category includes specialized processes catering to niche requirements for tailored thermal and optical characteristics in demanding semiconductor manufacturing environments. |

| By Application |

|

Photomask Substrate represents the leading application segment due to the fundamental role quartz plays as the base material for photomasks, which are essential for transferring circuit patterns onto silicon wafers. The extreme dimensional stability and optical clarity of synthetic quartz are paramount for this use. The Lithography Lens segment is also crucial, driven by the need for lenses with minimal thermal expansion and high transmission in advanced lithography tools like extreme ultraviolet (EUV) systems. The ‘Others’ category includes emerging applications in specialized wafer processing equipment. |

| By End User |

|

Semiconductor Foundries are the primary consumers of synthetic quartz, driven by massive, continuous production volumes and the relentless pursuit of process node miniaturization which demands the highest quality materials. Their demand is closely linked to global chip production capacity expansions. Integrated Device Manufacturers also represent a significant segment, with in-house fabrication requiring consistent high-purity quartz supplies. Semiconductor Equipment Manufacturers are key end users as they incorporate quartz components into lithography, etching, and deposition tools supplied to foundries and IDMs. |

| By Purity Grade |

|

Ultra-High Purity synthetic quartz is the leading segment, as it is a non-negotiable requirement for manufacturing advanced semiconductor devices where even trace impurities can cause critical defects and reduce yield. This grade is essential for applications in EUV lithography and leading-edge logic and memory chip production. The High Purity segment serves a broad range of mainstream semiconductor applications, while Standard Grade materials are typically used in less critical applications or older technology nodes where cost sensitivity is a higher priority than ultimate performance. |

| By Supply Chain Role |

|

Component Fabricators constitute the most critical segment within the supply chain, transforming raw synthetic quartz ingots into finished components like photomask blanks and precision lenses. These specialized fabricators require advanced machining and polishing capabilities to meet the stringent specifications of the semiconductor industry. Raw Material Suppliers are essential for providing the foundational high-purity materials, while Direct Supply to OEMs is a significant model for large-scale equipment manufacturers who integrate quartz components directly into their complex lithography and processing systems. |

Regional Analysis: Synthetic Quartz for Semiconductor Market

Asia-Pacific

The region hosts the world’s most advanced semiconductor foundries and memory chip manufacturers. This dense concentration of high-volume fabs creates an unparalleled, consistent demand for high-performance synthetic quartz components essential for maintaining yield and process control in complex manufacturing processes, driving local market growth.

A highly integrated and resilient supply chain for semiconductor materials has been established. Synthetic quartz producers are often located in close proximity to major fab clusters, enabling just-in-time delivery, collaborative R&D on material specifications, and rapid response to the evolving technical requirements of chipmakers.

Strong governmental backing through subsidies, tax incentives, and national semiconductor strategies significantly boosts the market. Policies aimed at reducing reliance on external suppliers encourage domestic production of critical materials like synthetic quartz, fostering a supportive environment for both established players and new entrants.

The relentless push towards smaller process nodes, 3D NAND, and advanced packaging technologies demands quartz materials with exceptional purity, thermal stability, and minimal defectivity. The region’s leadership in developing these cutting-edge semiconductor technologies directly fuels the need for correspondingly advanced synthetic quartz solutions.

North America

North America maintains a significant position in the synthetic quartz market, anchored by a strong semiconductor equipment manufacturing base and leading-edge R&D activities. The presence of major semiconductor capital equipment companies, which are primary consumers of high-purity quartz for chamber components, ensures steady demand. The market is characterized by a focus on innovation and custom, high-specification products for the most advanced semiconductor tools. Collaboration between national laboratories, universities, and private industry fosters developments in quartz material science to meet future challenges, such as those posed by extreme ultraviolet lithography. While its manufacturing volume is less than Asia-Pacific, North America’s influence on setting global technical standards and driving material innovation remains substantial.

Europe

Europe’s market for synthetic quartz is driven by its specialized semiconductor industry, which focuses on power electronics, automotive chips, and specialized microcontrollers. Leading research institutions and equipment suppliers demand high-quality quartz for applications requiring longevity and reliability under harsh operating conditions. The region benefits from strong environmental and quality regulations that align well with the high-purity standards of synthetic quartz production. Collaborative projects within the European Union aim to strengthen the semiconductor value chain, indirectly supporting the market for critical materials. The presence of global quartz manufacturers with advanced R&D facilities in Europe ensures a consistent supply of tailored solutions for the region’s unique technological needs.

South America

The synthetic quartz market in South America is nascent but developing, primarily serving a growing local electronics assembly industry and limited fab operations. Demand is currently met largely through imports, as local production capabilities for high-purity semiconductor-grade materials are limited. However, increasing regional investments in technology infrastructure and a gradual expansion of industrial bases present future growth opportunities. The market dynamics are influenced by broader economic conditions and the pace of technological adoption in neighboring industrial sectors. While not a major global player, the region represents a potential growth market as global semiconductor supply chains continue to diversify geographically.

Middle East & Africa

The market for synthetic quartz in the Middle East & Africa is presently the smallest globally, with demand stemming from a limited number of industrial and electronics manufacturing projects. The region’s focus has historically been on resource extraction rather than high-tech manufacturing. However, strategic national visions in several Gulf countries are now promoting economic diversification into technology and advanced industries, which could eventually stimulate demand for semiconductor materials. Any market growth is expected to be gradual, initially relying on imported materials until a local industrial base is sufficiently established to support upstream material production.

Report Scope

This market research report provides a comprehensive analysis of the Synthetic Quartz for Semiconductor Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Synthetic Quartz for Semiconductor Market?

-> Global Synthetic Quartz for Semiconductor Market was valued at USD 854 million in 2024 and is projected to reach USD 1350 million by 2032, exhibiting a CAGR of 7.1% during the forecast period.

Which key companies operate in Synthetic Quartz for Semiconductor Market?

-> Key players include Heraeus, AGC, Tosoh, Feilihua, Nikon, Shin-Etsu, Ohara, CoorsTek, and Yangtze Optical Fibre and Cable, among others.

What are the key growth drivers?

-> Key growth drivers include the overall growth of the semiconductor industry, demand from consumer electronics and automotive sectors, rollout of 5G and IoT technology, and increased investments in R&D.

Which region dominates the market?

-> Asia-Pacific is the dominant market, with major manufacturing hubs in countries like China, South Korea, and Taiwan driving demand.

What are the emerging trends?

-> Emerging trends include the growing demand for high-purity quartz, development of specialized quartz types like fused silica, and a focus on sustainable manufacturing practices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...