MARKET INSIGHTS

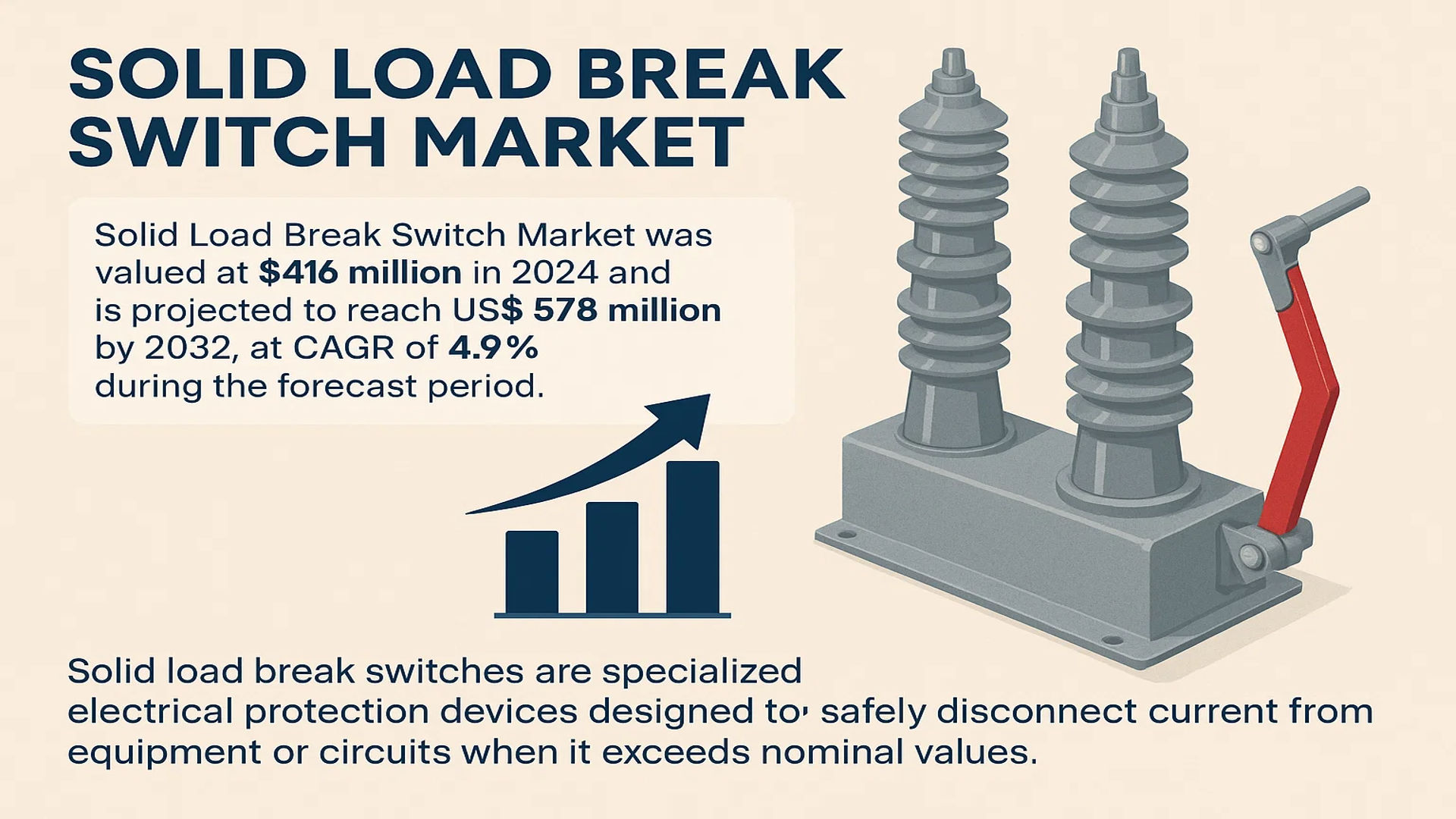

The global Solid Load Break Switch Market was valued at 416 million in 2024 and is projected to reach US$ 578 million by 2032, at a CAGR of 4.9% during the forecast period.

Solid Load Break Switches are specialized electrical protection devices designed to safely disconnect current from equipment or circuits when it exceeds nominal values. They operate by being triggered by magnetic fields within the main power system and automatically re-close once power demand normalizes, thereby effectively reducing current peaks in low-impedance circuits and enhancing grid stability.

The market is experiencing steady growth driven by several key factors, including global upgrades in power infrastructure and an increased demand for reliable electricity supply. The acceleration of urbanization and industrial automation has created a strong need for compact, efficient, and maintenance-friendly switchgear in medium and low voltage distribution systems. Furthermore, the expansion of renewable energy projects, such as wind and solar power plants, is a significant growth driver because these installations require stable power access points and sophisticated energy management solutions. While the market concentration is not high internationally, key players such as Schneider Electric, Siemens, and G&W Electric maintain strong positions, alongside prominent Asian manufacturers including Shinsung, ENTEC, and BH SYSTEM.

MARKET DYNAMICS

MARKET DRIVERS

Global Power Infrastructure Modernization to Propel Market Expansion

The ongoing modernization of global power infrastructure serves as a primary catalyst for the solid load break switch market. Aging electrical grids in developed regions require upgrades to enhance reliability and accommodate increasing electricity demand, which is projected to grow by over 2.5% annually worldwide. These switches provide critical protection mechanisms in medium voltage networks, preventing equipment damage during overload conditions. The transition toward smart grid technologies further accelerates adoption, as utilities seek advanced switching solutions that integrate with digital monitoring systems. Government initiatives supporting grid resilience, particularly in North America and Europe where infrastructure investment exceeds $100 billion annually, create substantial demand for reliable switching equipment. The inherent advantages of solid insulation—including compact design, reduced maintenance requirements, and superior environmental resistance—position these devices as preferred solutions in modernized power networks.

Renewable Energy Integration to Accelerate Market Growth

The rapid expansion of renewable energy generation facilities drives significant demand for solid load break switches worldwide. Solar and wind power projects require robust switching equipment for safe interconnection with main grids, particularly as global renewable capacity is expected to increase by over 2400 GW within the next decade. These switches provide reliable isolation and protection in substations and distribution networks serving renewable installations. Their solid insulation design offers superior performance in diverse environmental conditions encountered in solar farms and offshore wind facilities. The modular nature of these switches allows for flexible configurations in renewable energy applications, while their maintenance-free operation reduces lifecycle costs in remote locations. As countries intensify their renewable energy commitments, with over 90% of new power capacity additions coming from renewables, the demand for specialized switching equipment continues to escalate.

Urbanization and Industrial Automation to Boost Market Development

Rapid urbanization and industrial automation trends worldwide create substantial opportunities for solid load break switch adoption. Urban areas, which will house nearly 70% of the global population by 2050, require compact and reliable electrical distribution equipment to support high-density power networks. The space-saving design of solid insulated switches makes them ideal for urban substations and underground distribution systems. Meanwhile, industrial automation drives demand for uninterrupted power supply with advanced protection features. Manufacturing facilities increasingly adopt automated processes that require precise electrical protection, with global industrial automation investments exceeding $400 billion annually. Solid load break switches provide the necessary reliability and safety for critical industrial operations, while their minimal maintenance requirements align with the operational efficiency goals of modern industrial facilities. The convergence of these trends across developing and developed markets ensures sustained market growth.

MARKET RESTRAINTS

High Initial Investment Costs to Limit Market Penetration

The substantial initial investment required for solid load break switches presents a significant barrier to market expansion, particularly in cost-sensitive regions and applications. These devices incorporate advanced materials and manufacturing processes that result in higher upfront costs compared to conventional air-insulated alternatives. The premium pricing, often 20-30% above traditional switches, deters budget-conscious utilities and industrial customers despite long-term operational benefits. This cost sensitivity is especially pronounced in developing economies where electricity infrastructure projects face stringent budget constraints. While lifecycle cost analysis demonstrates economic advantages through reduced maintenance and extended service life, the initial capital expenditure remains a decisive factor for many procurement decisions. The manufacturing complexity involving specialized epoxy resin compounds and precision casting processes contributes to the elevated production costs, which are ultimately passed to end-users.

Technical Complexity and Standardization Issues to Hinder Market Adoption

Technical complexities associated with solid load break switch technology create adoption barriers across various market segments. The integration of these devices into existing power systems requires specialized engineering expertise due to their unique operating characteristics and interface requirements. Unlike conventional switches, solid insulated devices demand precise coordination with protection systems and may require custom solutions for specific applications. This technical complexity escalates installation costs and extends project timelines, particularly when retrofitting existing infrastructure. Additionally, the lack of global standardization in design specifications and performance requirements complicates procurement and integration processes. Different regions maintain varying technical standards for medium voltage switchgear, forcing manufacturers to develop multiple product variants and limiting economies of scale. These factors collectively restrain market growth by increasing implementation complexity and reducing interoperability between systems from different manufacturers.

Supply Chain Vulnerabilities to Impact Market Stability

Global supply chain vulnerabilities present significant challenges for the solid load break switch market, affecting both manufacturing and deployment timelines. The production of these specialized devices relies on critical raw materials including high-grade epoxy resins, silver-based contact materials, and specialized semiconductor components. Supply disruptions for any of these materials, which experienced price increases of 15-25% during recent global supply chain constraints, directly impact manufacturing capacity and product costs. Geographic concentration of raw material production, particularly in specific Asian markets, creates dependency risks for manufacturers worldwide. Additionally, the sophisticated manufacturing equipment required for producing solid insulated switches faces extended delivery times and technical support challenges. These supply chain issues not only affect production schedules but also project implementation timelines, as utilities and industries face extended waiting periods for equipment delivery, potentially delaying crucial infrastructure projects.

MARKET CHALLENGES

Skilled Workforce Shortage to Challenge Market Implementation

The global shortage of skilled electrical engineers and technicians proficient in solid insulated switchgear technology poses a significant challenge to market growth. These devices require specialized knowledge for proper installation, commissioning, and maintenance—expertise that is not widely available in the workforce. The retirement of experienced power engineers, particularly in developed markets where over 30% of the utility workforce is approaching retirement age, exacerbates this knowledge gap. Training new personnel on the intricacies of solid insulation technology demands substantial time and resources, while the rapid technological evolution requires continuous skill upgrades. This shortage not only affects installation quality but also impacts after-sales service capabilities, potentially undermining customer confidence in adopting new technology. The challenge is particularly acute in emerging markets where technical education infrastructure may not adequately address modern power equipment requirements.

Other Challenges

Regulatory Compliance Hurdles

Navigating diverse international regulatory frameworks and certification requirements presents substantial challenges for market participants. Each region maintains unique standards for medium voltage switchgear, requiring extensive testing and certification processes that can take 12-18 months per market. These regulatory hurdles increase time-to-market and development costs, particularly for manufacturers seeking global market presence. The evolving nature of electrical safety standards, with frequent updates and regional variations, demands continuous investment in compliance activities.

Technology Adoption Resistance

Conservative attitudes within the power industry toward new technologies create adoption resistance despite demonstrated advantages. Many utilities maintain preference for conventional switchgear based on decades of operational experience, creating inertia against innovation adoption. This resistance is particularly evident in critical infrastructure applications where reliability concerns outweigh potential benefits, slowing market penetration despite technical superiority.

MARKET OPPORTUNITIES

Smart Grid Investments to Create Substantial Growth Opportunities

Global investments in smart grid technologies present significant growth opportunities for the solid load break switch market. With worldwide smart grid investments exceeding $300 billion annually and projected to grow at 8% CAGR, these advanced networks require switching equipment with digital capabilities and remote operation features. Solid load break switches, with their compact design and compatibility with automation systems, are ideally positioned to benefit from this trend. The integration of sensors and communication modules enables real-time monitoring and control, aligning with smart grid operational requirements. Utilities increasingly prioritize equipment that supports grid automation and self-healing capabilities, creating demand for advanced switching solutions. The modular design of solid insulated switches facilitates easy integration with smart grid architectures, while their reliability ensures uninterrupted operation in automated networks. This convergence of technology trends creates substantial market opportunities across all geographic regions.

Emerging Market Electrification to Drive Future Market Expansion

The ongoing electrification of emerging economies offers substantial growth potential for solid load break switch manufacturers. Rapid infrastructure development in Asia, Africa, and Latin America requires modern electrical distribution equipment to support expanding power networks. These regions, where electricity access is increasing by approximately 3% annually, represent untapped markets for advanced switching solutions. The compact nature of solid insulated switches makes them particularly suitable for urban areas with space constraints, while their environmental resistance benefits applications in diverse climatic conditions. Government initiatives aimed at improving electrification rates and grid reliability further stimulate demand, with emerging markets accounting for over 60% of global power infrastructure investments. The scalability of manufacturing operations allows suppliers to address varying market requirements, from utility-scale projects to industrial applications, ensuring broad-based market opportunities.

Technological Innovation to Unlock New Application Areas

Continuous technological innovation in materials and design creates new application opportunities for solid load break switches across various sectors. Advancements in epoxy resin formulations and manufacturing processes enable higher voltage ratings and improved performance characteristics, expanding addressable market segments. The development of eco-friendly insulating materials aligns with sustainability initiatives, particularly in regions with stringent environmental regulations. Innovations in contact technology and arc interruption mechanisms enhance switching performance, enabling applications in more demanding operating conditions. The integration of digital twins and predictive maintenance capabilities through IoT connectivity creates additional value propositions for end-users. These technological advancements not only improve product performance but also reduce total cost of ownership, addressing price sensitivity concerns. The ongoing R&D investments by leading manufacturers, exceeding 5% of annual revenues, ensure continuous product evolution and market expansion into new application areas.

SOLID LOAD BREAK SWITCH MARKET TRENDS

Global Power Infrastructure Modernization Driving Market Expansion

The global solid load break switch market is experiencing robust growth, primarily fueled by extensive modernization and expansion of power infrastructure worldwide. Aging electrical grids in developed economies require replacement with more reliable and efficient equipment, while emerging economies are building new infrastructure to support rapid urbanization and industrialization. The global push toward grid reliability is evidenced by investment figures exceeding $300 billion annually in power infrastructure upgrades. Solid load break switches, with their encapsulated design using materials like epoxy resin or silicone rubber, provide superior protection against environmental factors and fault currents, making them ideal for both indoor and outdoor applications. This trend is particularly strong in regions with extreme weather conditions, where equipment durability is paramount. Furthermore, the increasing electrification of transportation and heating systems is creating additional demand for robust distribution equipment capable of handling higher loads and more frequent switching operations.

Other Trends

Renewable Energy Integration

The rapid expansion of renewable energy projects is creating significant demand for solid load break switches in power distribution networks. Solar and wind farms require reliable switching equipment for connection to the grid and for managing power flow in complex distribution systems. These applications demand switches that can perform frequent operations, withstand harsh environmental conditions, and provide safe isolation for maintenance. The global renewable energy capacity addition of approximately 340 GW in 2024 alone has directly contributed to the growing adoption of solid insulation technology in switchgear. Manufacturers are developing specialized products for renewable applications, including switches with higher short-circuit withstand capabilities and enhanced safety features for maintenance personnel working on energized systems.

Technological Advancements and Smart Grid Integration

Technological innovation represents a major trend shaping the solid load break switch market, with manufacturers increasingly incorporating smart grid capabilities and advanced materials into their products. The integration of sensors, communication modules, and monitoring systems allows utilities to remotely monitor switch status, predict maintenance needs, and optimize grid operations. This digital transformation is part of the broader smart grid market, which is projected to grow at a compound annual growth rate of over 8% through 2030. Additionally, material science advancements have led to improved insulating compounds that offer better thermal stability, higher dielectric strength, and reduced environmental impact. These innovations are particularly important as utilities seek to reduce their carbon footprint and improve the sustainability of their operations. The development of modular designs has also gained traction, allowing for easier installation, maintenance, and customization to specific application requirements.

Regional Market Dynamics and Industrial Applications

Market growth patterns show significant regional variation, with Asia-Pacific emerging as the fastest-growing region due to massive infrastructure investments and rapid industrialization. Countries like China, India, and Southeast Asian nations are investing heavily in power infrastructure, with projected investments exceeding $150 billion in transmission and distribution systems over the next five years. Meanwhile, North America and Europe are focusing on grid modernization and reliability improvements, driven by increasing electricity demand and the need to integrate distributed energy resources. The industrial sector represents the largest application segment, accounting for approximately 45% of market revenue, as manufacturing facilities require reliable power distribution for continuous operations. The commercial segment is growing rapidly as well, particularly in data centers and large commercial complexes where power reliability is critical for business operations.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Product Innovation and Regional Expansion Define Market Competition

The global solid load break switch market exhibits a fragmented and semi-consolidated competitive structure, characterized by a mix of multinational industrial giants, specialized regional manufacturers, and emerging players. While no single entity holds a dominant market share, a few key players exert significant influence through their technological expertise, extensive distribution networks, and strong brand recognition in the power sector. Competition is intensifying due to the critical need for grid modernization and the integration of renewable energy sources, pushing companies to innovate continuously.

Schneider Electric (France) and Siemens AG (Germany) are universally recognized as global leaders, leveraging their comprehensive portfolios in power distribution and automation. Their dominance is attributed to decades of experience, massive investments in smart grid technologies, and a formidable presence across both developed and developing economies. They are consistently at the forefront of introducing digitally enabled and environmentally sustainable switchgear solutions.

In the Americas, G&W Electric (U.S.) and Hubbell Incorporated (U.S.) are pivotal competitors, known for their robust and reliable products tailored for the North American utility market. Similarly, Asian manufacturers have carved out substantial market share. Companies like Shinsung (South Korea), ENTEC ELECTRIC & ELECTRONIC CO.,LTD (South Korea), and BH SYSTEM (South Korea) are celebrated for their cost-effective and technologically advanced offerings, making them strong contenders in the Asia-Pacific region and beyond. Precise Corporation Public Company (Thailand) and Togami Electric (Japan) further contribute to the region’s strong manufacturing base.

Furthermore, these companies are actively strengthening their market positions through significant investments in research and development, aimed at enhancing product efficiency and durability. Strategic initiatives such as geographical expansions into emerging markets, targeted mergers and acquisitions, and the launch of new product lines designed for specific applications like solar farms and wind power plants are expected to significantly alter market shares over the coming years. This dynamic environment ensures that innovation and customer-centric solutions remain the primary drivers of competition.

List of Key Solid Load Break Switch Companies Profiled

- Schneider Electric (France)

- Siemens AG (Germany)

- G&W Electric (U.S.)

- Shinsung (South Korea)

- ENTEC ELECTRIC & ELECTRONIC CO.,LTD (South Korea)

- BH SYSTEM (South Korea)

- Precise Corporation Public Company (Thailand)

- Togami Electric (Japan)

- Hubbell Incorporated (U.S.)

- Zhejiang Yutai Electric (China)

- Rockwill Electric (China)

- Joongwon (South Korea)

Segment Analysis:

By Type

Outdoor Segment Dominates the Market Due to Superior Environmental Resilience and Grid Modernization Initiatives

The market is segmented based on type into:

- Outdoor

- Indoor

By Application

Utilities Segment Leads Due to Critical Role in Power Distribution and Grid Reliability

The market is segmented based on application into:

- Utilities

- Industrial

- Commercial

By Voltage Rating

Medium Voltage Segment Holds Significant Share Owing to Widespread Use in Distribution Networks

The market is segmented based on voltage rating into:

- Low Voltage

- Medium Voltage

- High Voltage

By Insulation Type

Epoxy Resin Insulation is Prevalent Due to Excellent Dielectric Properties and Mechanical Strength

The market is segmented based on insulation type into:

- Epoxy Resin

- Silicone Rubber

- Others

Regional Analysis: Solid Load Break Switch Market

Asia-Pacific

The Asia-Pacific region dominates the global solid load break switch market, accounting for the largest market share by both volume and value. This leadership is driven by massive investments in power infrastructure, rapid urbanization, and industrial expansion, particularly in China and India. China’s State Grid Corporation continues its extensive grid modernization projects, creating sustained demand for reliable switchgear. India’s ambitious “Power for All” initiative and the expansion of its renewable energy capacity, which aims to reach 500 GW by 2030, are significant drivers. While cost sensitivity initially favored conventional switchgear, there is a marked and accelerating shift toward solid insulation technology due to its superior reliability, compact size, and reduced maintenance requirements, especially in space-constrained urban environments. Key regional players like Shinsung (South Korea), ENTEC (South Korea), and BH SYSTEM (South Korea) are major contributors, alongside Precise Corporation (Thailand) and Togami Electri (Japan). The manufacturing prowess of these companies, combined with strong local supply chains, ensures competitive pricing and widespread availability across the region.

North America

The North American market is characterized by a strong focus on grid reliability, resilience, and the integration of renewable energy sources. Significant investments, such as those outlined in the U.S. Infrastructure Investment and Jobs Act, are earmarked for upgrading aging power infrastructure, which directly fuels demand for advanced switchgear like solid load break switches. The region has stringent utility standards and a high emphasis on product safety and performance, favoring established, technologically advanced manufacturers. Key players with a strong presence include G&W Electric, Hubbell Incorporated, and Schneider Electric (through its North American operations). The growth of distributed energy resources (DERs), such as community solar farms and microgrids, is a particularly potent driver, as these applications require compact, safe, and frequently operated switching solutions that solid load break switches provide. The market is mature and values innovation, with a steady adoption rate for new technologies that enhance grid intelligence and durability.

Europe

Europe’s market is propelled by the European Union’s stringent regulations on electrical equipment safety and a strong political and industrial drive toward carbon neutrality, which necessitates massive upgrades to the power grid to accommodate renewable energy. The EU’s Green Deal and various national energy strategies are creating substantial opportunities for modern switchgear. The region has a well-established and highly competitive landscape dominated by global giants like Siemens and Schneider Electric, which invest heavily in research and development for smart and eco-efficient products. The demand is particularly high for switches that offer enhanced safety features, reduced environmental impact (e.g., using SF6-free designs), and compatibility with digital substation and smart grid applications. While the market is advanced, growth is steady, driven by the replacement of aging infrastructure and the specific needs of the region’s ambitious energy transition projects.

South America

The market in South America is emerging, presenting a mix of opportunities and challenges. Countries like Brazil and Argentina are undertaking efforts to expand and stabilize their power grids, often in partnership with international development banks. These projects create demand for reliable medium-voltage distribution equipment. However, the market’s growth is frequently tempered by economic volatility, fluctuating currency values, and sometimes inconsistent regulatory enforcement. This economic reality often makes initial cost a primary decision factor, which can slow the adoption of more advanced—and initially more expensive—solid insulation technology compared to traditional air-insulated or oil-insulated alternatives. Nevertheless, as urban centers expand and industrial activity grows, the long-term benefits of solid load break switches, such as their durability and lower lifetime maintenance costs, are gradually gaining recognition among utilities and large industrial consumers.

Middle East & Africa

The market in the Middle East & Africa is nascent but holds significant long-term potential. Development is primarily concentrated in the Gulf Cooperation Council (GCC) nations, such as Saudi Arabia and the UAE, where economic diversification strategies under visions like Saudi Vision 2030 are driving massive investments in industrial cities, renewable energy mega-projects, and modern urban infrastructure. These developments require robust electrical distribution networks, creating demand for high-quality switchgear. In contrast, growth in many African nations is constrained by limited funding for large-scale infrastructure projects and less developed regulatory frameworks. Across the region, the demand is strongest for equipment that offers extreme durability and can perform reliably in harsh environmental conditions, which is a key value proposition of solid insulated switchgear. While the market is not yet a major volume consumer globally, it represents a key growth frontier for international suppliers.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Solid Load Break Switch markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of smart grid systems, advanced insulation materials, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Solid Load Break Switch Market?

-> Solid Load Break Switch Market was valued at 416 million in 2024 and is projected to reach US$ 578 million by 2032, at a CAGR of 4.9% during the forecast period.

Which key companies operate in Global Solid Load Break Switch Market?

-> Key players include Schneider Electric, Siemens, G&W Electric, Shinsung, ENTEC ELECTRIC & ELECTRONIC CO.,LTD, BH SYSTEM, Precise Corporation Public Company, and Togami Electri, among others.

What are the key growth drivers?

-> Key growth drivers include global power infrastructure upgrades, renewable energy expansion, urbanization, and increasing demand for reliable and compact switchgear solutions.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by significant infrastructure investments, while Europe and North America remain mature markets with strong technological adoption.

What are the emerging trends?

-> Emerging trends include integration with smart grid technologies, adoption of environmentally friendly insulation materials, modular designs for customization, and enhanced safety features.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...