Smart Vision Sensor Market Insights

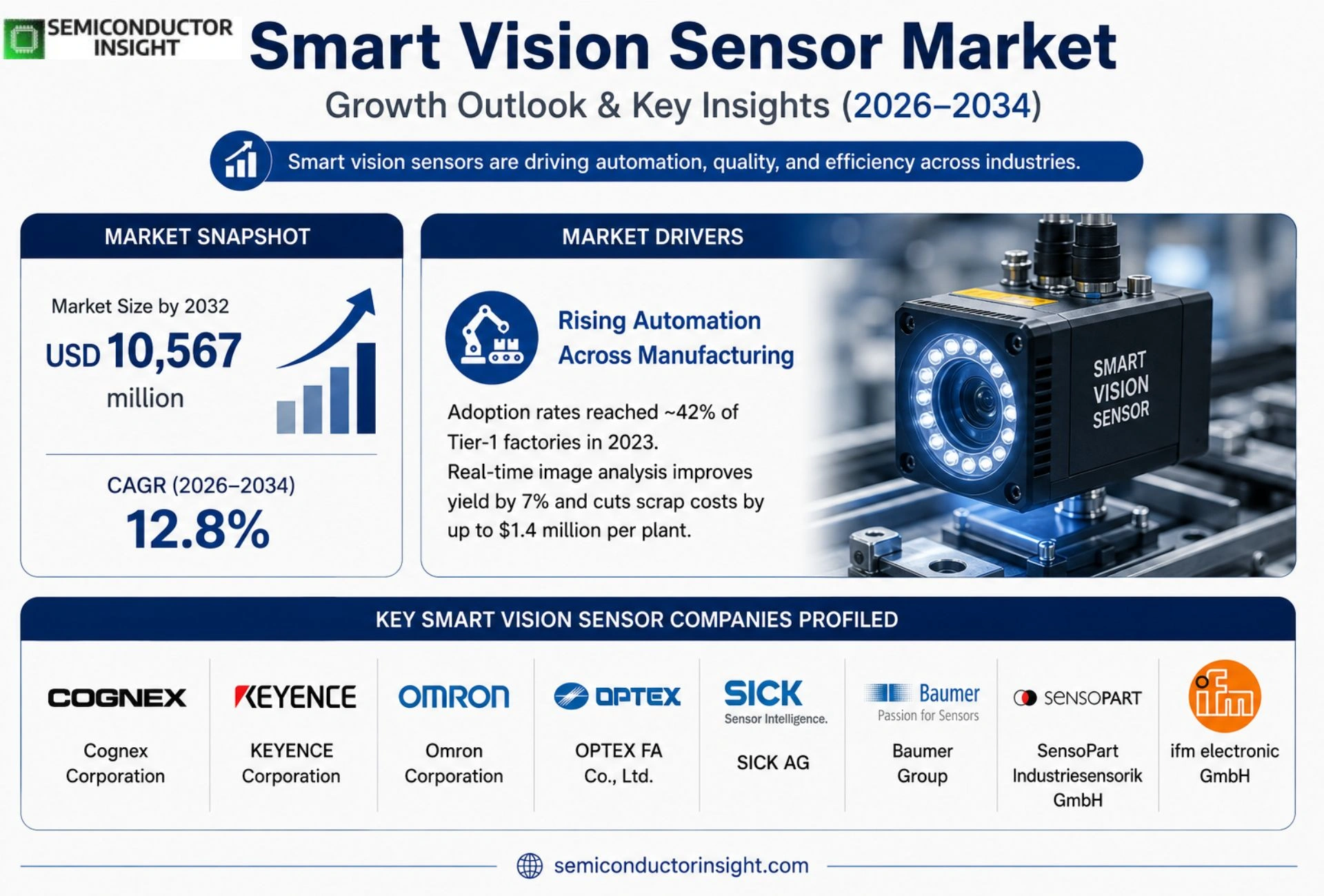

Global Smart Vision Sensor market size was valued at USD 4,594 million in 2025. The market is projected to grow from USD 4,594 million in 2025 to USD 10,567 million by 2032, exhibiting a CAGR of 12.8% during the forecast period.

Smart vision sensors are integrated visual‑sensing and decision‑making devices designed for industrial automation environments. Their core purpose is to combine image acquisition, optical illumination, image processing, rule‑based algorithms or artificial‑intelligence inference, industrial communication and result output into compact hardware. This integration replaces manual visual inspection and multiple single‑point photoelectric sensors for tasks such as presence detection, assembly verification, defect inspection, dimensional measurement, positioning guidance, counting, sorting, OCR and barcode reading.

The market is expanding because manufacturers are seeking higher quality consistency, flexible production lines and closed‑loop automation control. As product varieties increase and defect patterns become finer, traditional inspection methods struggle to meet speed and traceability requirements. Consequently, factories are adopting smart vision sensors to generate immediate OK/NG signals that can be fed directly into PLCs, robots or MES systems. Leading vendors,including Cognex Corporation, KEYENCE Corporation, OMRON Corporation and SICK AG,are accelerating development of edge‑AI capabilities, 3D sensing technologies and native support for industrial protocols such as PROFINET and EtherNet/IP.

MARKET DRIVERS

Rising Automation Across Manufacturing

Smart Vision Sensor Market is gaining traction as manufacturers seek to replace legacy inspection lines with vision‑enabled robotics. Adoption rates have climbed to roughly 42 % of Tier‑1 factories in 2023, reflecting a clear shift toward closed‑loop quality control. Companies that embed real‑time image analysis see an average yield improvement of 7 % and a reduction in scrap costs by up to $1.4 million per plant, underscoring the financial incentive behind the move.

AI‑Enhanced Sensing in Transportation

Automotive OEMs are integrating smart vision modules into ADAS and autonomous driving stacks, prompting a surge in component orders that lifted sensor shipments by 18 % year‑over‑year. The capability to process edge‑side AI workloads reduces latency, a factor that directly influences safety certification timelines. Consequently, firms that master on‑sensor inference are positioned to capture premium pricing tiers.

➤ Industry analysts note that the convergence of edge AI and vision hardware is reshaping value chains, compelling traditional optics suppliers to form strategic alliances with semiconductor firms.

Beyond factories and vehicles, logistics operators are deploying vision sensors on conveyor belts and sorting hubs, delivering a 15 % boost in parcel throughput while maintaining error rates below 0.2 %. This operational efficiency translates into tighter margins and stronger competitive positioning for early adopters.

MARKET CHALLENGES

Escalating Component Costs

High‑resolution image sensors combined with on‑chip AI accelerators command price points that remain several times higher than conventional cameras. Small‑ to mid‑size manufacturers report cost barriers that limit broader rollout, especially in price‑sensitive segments such as consumer electronics.

Other Challenges

Integration Complexity

Design teams must reconcile disparate data formats, power budgets, and mechanical footprints, often extending development cycles by 3‑4 months. This added time‑to‑market erodes the competitive advantage that smart vision promises.

MARKET RESTRAINTS

Power Consumption Constraints

While on‑sensor AI reduces upstream processing load, the combined power draw of high‑frame‑rate imaging and neural inference can exceed 8 W per unit. Facilities operating on limited power budgets must allocate additional cooling infrastructure, inflating overall system cost.

Regulatory scrutiny over energy efficiency is tightening in regions such as the EU, where new directives encourage manufacturers to achieve a 10 % reduction in average device power consumption by 2026. This regulatory pressure adds a layer of compliance risk for vendors still reliant on legacy architectures.

Moreover, the need for high‑bandwidth connections,often 10 GbE or greater,creates bottlenecks in older factory networks. Upgrading these backbones represents a capital expense that many enterprises hesitate to commit to without clear ROI evidence.

MARKET OPPORTUNITIES

Edge AI Integration in Emerging Sectors

The agricultural sector is piloting smart vision sensors on harvesters to monitor fruit ripeness and detect pest infestations. Early field trials show a 12 % increase in yield quality, suggesting a sizable upside for agritech firms that can tailor sensor stacks to rugged, low‑light environments.

Healthcare imaging devices are another frontier; compact vision modules capable of on‑device anomaly detection reduce reliance on centralized servers, enhancing patient data privacy. Anticipated adoption in portable diagnostic equipment could unlock a market segment worth $800 million within five years.

Finally, the rollout of 5G networks provides the bandwidth required for real‑time streaming of high‑resolution visual data from remote sites. Vendors that align their sensor platforms with 5G edge‑computing frameworks stand to benefit from a wave of new use cases ranging from smart city surveillance to autonomous drone fleets.

Smart Vision Sensor Market Trends

Edge AI Integration Accelerates Adoption

Manufacturers are embedding lightweight neural networks directly onto sensor chips, allowing inspection decisions to be made without a host PC. This shift reduces engineering effort, shortens time‑to‑value, and aligns with the broader move toward decentralized automation. End‑users report that on‑device inference eliminates the bottleneck of transmitting high‑resolution frames to a central server, which in turn improves line throughput and lowers latency. The practical outcome is a tighter feedback loop between vision and motion control, enabling real‑time defect segregation on high‑speed conveyors.

Other Trends

Industrial Connectivity Standards

Recent product releases show a concerted push toward native support for PROFINET, EtherNet/IP, OPC UA, and IO Link. Buyers now expect a smart vision sensor to appear as a field‑bus node that can be addressed by PLCs or MES systems without custom middleware. This expectation is reshaping bills of materials; a single device can replace several legacy photo‑electric switches, a separate controller, and a proprietary communication module. The net effect is a reduction in wiring complexity and a clearer path for remote diagnostics and predictive maintenance.

3D Sensing Expands Functional Reach

Beyond traditional 2‑D imaging, 3‑D point‑cloud generation is becoming a standard feature in new sensor families. Companies are leveraging structured light and laser profiling to capture depth information that resolves occlusion and measures volume directly on the production floor. This capability is especially valuable in automotive body‑panel inspection, flexible packaging, and semiconductor wafer handling, where variations in thickness or curvature dictate pass/fail criteria. By embedding depth perception, manufacturers can automate tasks that previously required manual calipers or multiple camera setups, thereby improving repeatability and reducing labor costs.

COMPETITIVE LANDSCAPE

Key Industry Players

Smart Vision Sensor Market: Competitive Overview

The market is anchored by a handful of global suppliers whose product portfolios combine AI‑enabled image processing with industrial‑grade connectivity. Cognex Corporation leads with its extensive AI‑vision line, leveraging deep‑learning inference engines that can be programmed on‑site via browser tools. KEYENCE follows closely, offering compact vision sensors that embed rule‑based and AI algorithms in a single housing, a model that resonates with manufacturers seeking rapid deployment on assembly lines. Japanese firms such as Omron and OPTEX FA provide strong after‑sales networks in Asia, emphasizing ease‑of‑integration and long‑life mechanical design, while German players like SICK AG and Baumer Group differentiate themselves through robust fieldbus support (PROFINET, EtherNet/IP) and certified safety ratings. This concentration of capability creates a tiered structure: tier‑1 vendors dominate high‑volume automotive and semiconductor segments, whereas tier‑2 specialists carve out niches in food‑pharma traceability and logistics sorting.

Beyond the headline names, a diverse set of midsize manufacturers enriches the ecosystem with specialized 3‑D sensing and edge‑AI hardware. SensoPart Industriesensorik, ifm electronic, and Balluff focus on structured‑light 3‑D sensors targeting robotic workcells. Companies such as Banner Engineering and Datalogic address barcode and OCR functions that complement vision intelligence. Emerging Asian newcomers,Hangzhou Hikrobot, Guangdong OPT Machine Vision Tech, and Zhejiang HuaRay,are repurposing legacy industrial camera platforms into integrated smart sensors, accelerating adoption in flexible manufacturing cells. Their aggressive pricing and rapid feature cycles exert pressure on incumbents to broaden software licensing models and offer turnkey integration services.

List of Key Smart Vision Sensor Companies Profiled

- Cognex Corporation

- KEYENCE Corporation

- Omron Corporation

- OPTEX FA Co., Ltd.

- SICK AG

- Baumer Group

- SensoPart Industriesensorik GmbH

- ifm electronic GmbH

- Balluff GmbH

- Banner Engineering Corp.

- Datalogic S.p.A.

- Pepperl+Fuchs SE

- Leuze electronic GmbH + Co. KG

- Zebra Technologies Corporation

- IDS Imaging Development Systems GmbH

- IMAGO Technologies GmbH

- ABB Ltd.

- Turck Holding GmbH

- Wenglor sensoric group

- Festo SE & Co. KG

- Teledyne Technologies Incorporated

- TKH Group N.V.

- Zivid AS

- WEG S.A.

- Overview AI, Inc.

- Autonics Corporation

- Hangzhou Hikrobot Co., Ltd.

- Guangdong OPT Machine Vision Tech Co., Ltd.

- Zhejiang HuaRay Technology Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Leading Segment – AI‑Enabled Cameras

|

| By Application |

|

Leading Segment – Electronics Assembly Verification

|

| By End User |

|

Leading Segment – System Integrators

|

| By Technology |

|

Leading Segment – Edge AI Inference

|

| By Connectivity |

|

Leading Segment – Industrial Ethernet (PROFINET/EtherNet/IP)

|

Regional Analysis: Smart Vision Sensor Market

North America

Leading car manufacturers are embedding smart vision sensors into driver‑assistance platforms, capitalising on the region’s rigorous safety testing protocols. This encourages tier‑one suppliers to accelerate firmware updates, ensuring compatibility across multiple vehicle platforms and reinforcing North America’s leadership in sensor‑driven safety solutions.

Factories in the Midwest are upgrading legacy lines with vision‑guided robotics, driven by the need for higher quality control. The proximity of semiconductor fabs simplifies component sourcing, allowing manufacturers to iterate designs swiftly and maintain competitive lead times.

Universities and research institutes in the region collaborate closely with sensor startups, creating pipelines that move concepts from lab benches to commercial products within months. This synergy reduces development risk for larger players and sustains a vibrant pipeline of differentiated technologies.

A diversified network of component manufacturers across Canada and the United States buffers the market against geopolitical shocks, ensuring steady availability of optical lenses and processing chips that are critical for sensor performance.

Europe

European manufacturers are leveraging stringent environmental directives to embed smart vision sensors into energy‑efficient production lines. The focus on circular economy principles forces equipment makers to adopt sensors that enable real‑time monitoring of material flows, reducing waste and extending equipment lifespan. Meanwhile, automotive firms in Germany and France are piloting sensor‑enhanced driver‑assist features to meet upcoming emission standards, prompting a cascade of software updates across the supply chain. The region’s collaborative standards bodies also promote interoperability, allowing smaller suppliers to integrate with larger platform providers without extensive redesign work.

Asia‑Pacific

In Asia‑Pacific, rapid urbanisation and expanding consumer electronics markets are driving demand for compact, low‑cost vision sensors. Manufacturers in China, Japan, and South Korea are scaling production through advanced wafer‑level packaging, which reduces form factor while preserving image fidelity. The proliferation of smart city initiatives creates a fertile testing ground for surveillance and traffic‑management applications, encouraging local firms to tailor sensor algorithms to diverse lighting conditions. Although cost sensitivity dominates procurement decisions, emerging quality benchmarks are nudging the market toward higher‑performance solutions.

South America

South American adopters are focusing on agricultural automation, where smart vision sensors support precision harvesting and crop‑health assessment. Countries such as Brazil are integrating sensors into fleet management systems for large‑scale logistics, enhancing route optimisation and load monitoring. The region’s growing investment in digital infrastructure is gradually narrowing the technology gap with more mature markets, but challenges around skilled workforce availability still temper the speed of adoption.

Middle East & Africa

In the Middle East and Africa, security and oil‑&‑gas sectors are early consumers of robust vision sensing solutions. Oil platforms employ sensors for pipeline inspection, relying on their resilience to harsh environments. Meanwhile, metropolitan security projects in the Gulf are experimenting with AI‑enabled cameras that fuse vision data with other sensor inputs, creating layered detection capabilities. Infrastructure development initiatives across the region provide a platform for incremental sensor deployment, yet the market remains fragmented, with a few multinational players predominating.

Report Scope

This market research report provides a comprehensive analysis of the Smart Vision Sensor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Vision Sensor Market?

-> Smart Vision Sensor Market was valued at USD 4,594 million in 2025 and is expected to reach USD 10,567 million by 2032, growing at a CAGR of 12.8%

Which key companies operate in Smart Vision Sensor Market?

-> Key players include Cognex Corporation, KEYENCE Corporation, OMRON Corporation, OPTEX FA Co., Ltd., SICK AG, Baumer Group, SensoPart Industriesensorik GmbH, ifm electronic GmbH, Balluff GmbH, Banner Engineering Corp., Datalogic S.p.A., Pepperl+Fuchs SE, Leuze electronic GmbH + Co. KG, Zebra Technologies Corporation, IDS Imaging Development Systems GmbH, IMAGO Technologies GmbH, ABB Ltd., Turck Holding GmbH, wenglor sensoric group, Festo SE & Co. KG, Teledyne Technologies Incorporated, TKH Group N.V., Zivid AS, WEG S.A., Overview AI, Inc., Autonics Corporation, DONG IL TECHNOLOGY Co., Ltd., Hangzhou Hikrobot Co., Ltd., Guangdong OPT Machine Vision Tech Co., Ltd., Zhejiang HuaRay Technology Co., Ltd., Mech‑Mind Robotics Technologies Ltd., Orbbec Inc., ADLINK Technology Inc., LUSTER LightTech Co., Ltd., di‑soric GmbH & Co. KG, Rockwell Automation, Inc.

What are the key growth drivers?

-> Key growth drivers include rising manufacturing demand for quality consistency, flexible production, and closed‑loop automation control; increasing product variety and stricter traceability requirements; the need for faster, more stable inspection solutions; and expanding adoption of AI‑enabled vision for defect classification and process monitoring.

Which region dominates the market?

-> Asia dominates Smart Vision Sensor market, driven primarily by strong demand in China, Japan, and South Korea, where extensive investments in electronics manufacturing, semiconductor packaging, logistics automation, and vehicle electrification are accelerating adoption.

What are the emerging trends?

-> Emerging trends include edge AI integration for on‑device inference, 3D sensing technologies such as structured light and laser profiling, enhanced industrial connectivity via PROFINET, EtherNet/IP, OPC UA, and IO‑Link, as well as the shift toward AI‑trained configuration tools that reduce the need for extensive engineering expertise.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...