Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market Insights

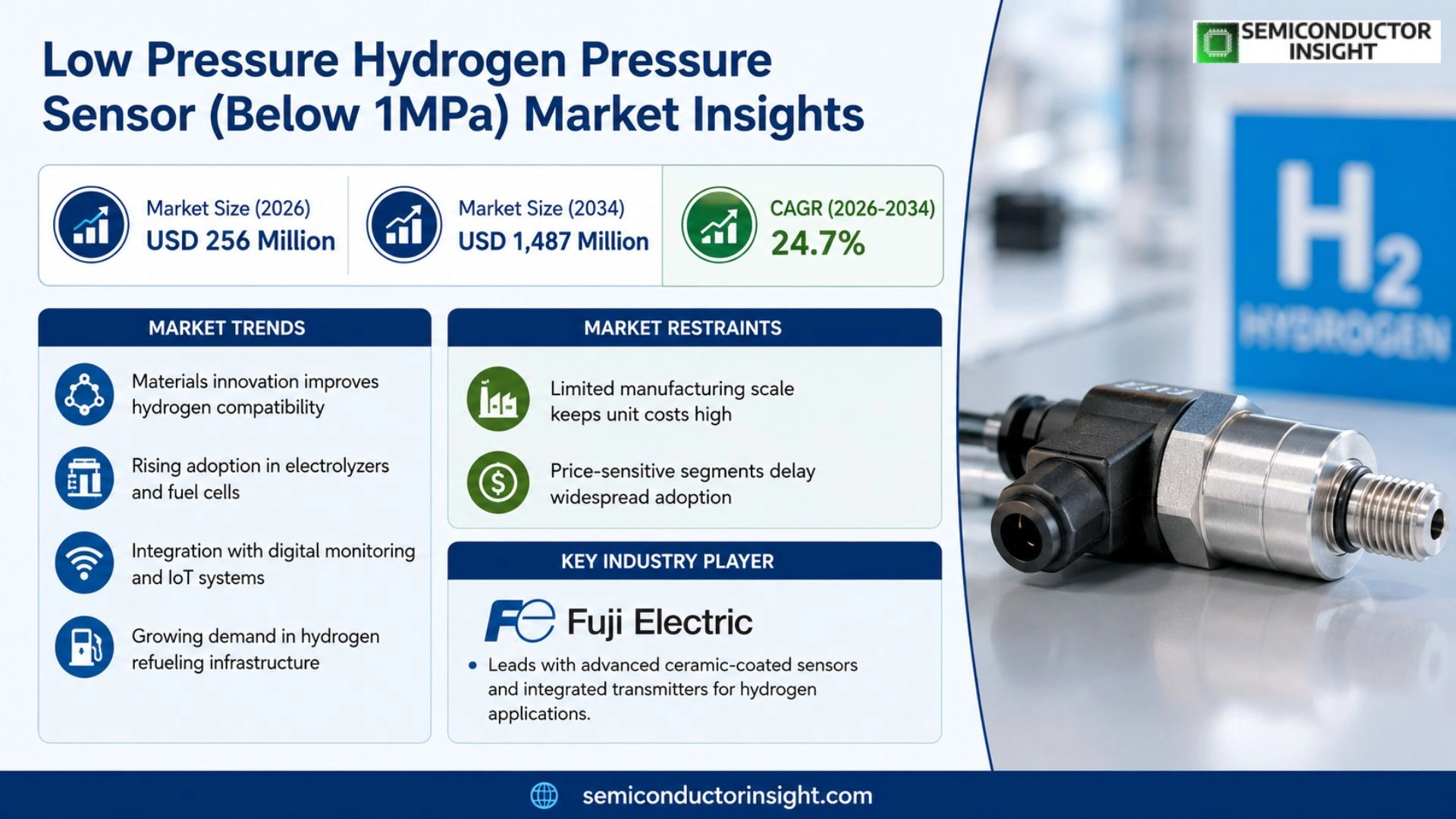

Global Low Pressure Hydrogen Pressure Sensor (Below 1MPa) market size was valued at USD 38.17 million in 2025 and is expected to reach USD 197 million by 2032, showing a CAGR of 26.7% over the period.

Low‑pressure hydrogen pressure sensors are devices engineered for hydrogen production, storage, fuel‑cell systems and test platforms. They provide stable, fast pressure acquisition below 1 MPa while mitigating hydrogen permeation and embrittlement through gold‑plated diaphragms, ceramic barriers, high‑nickel stainless steel or titanium wetted parts, and oil‑free welded structures combined with thin‑film, piezoresistive or micro‑capacitive sensing elements.

The market expands because investment in electrolyzer projects rises, regional hydrogen strategies accelerate, and manufacturers such as Fuji Electric, NAGANO KEIKI, Baker Hughes and KELLER introduce customized OEM elements and digital transmitters that meet stringent safety and precision requirements.

MARKET DRIVERS

Growing Adoption of Fuel‑Cell Technologies

The surge in fuel‑cell deployments for automotive and stationary power applications is prompting equipment manufacturers to seek sensors that can reliably monitor hydrogen levels under 1 MPa. Precision in pressure detection translates directly into longer system lifespans and reduced downtime, which is why OEMs are specifying dedicated low‑pressure hydrogen pressure sensors for new designs.

Stringent Safety Regulations

Regulatory bodies across Europe, North America, and parts of Asia have tightened safety standards for hydrogen infrastructure. Compliance now often requires real‑time pressure feedback at sub‑megapascal levels, creating a clear commercial incentive for suppliers that can deliver certified low‑pressure sensors with fast response times.

➤ Manufacturers that integrate calibrated Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market solutions into their product lines can achieve up to a 12 % reduction in warranty claims.

Beyond compliance, the competitive landscape rewards firms that can differentiate their hardware through embedded diagnostics. Sensors equipped with self‑test functions and predictive analytics are being bundled into turnkey packages, allowing end users to anticipate leaks before they become safety incidents.

MARKET CHALLENGES

Cost Pressures from Commodity Materials

The sensor market is feeling the pinch of raw‑material price volatility, especially for palladium and specialty alloys used in hydrogen‑sensitive diaphragms. When component costs rise, customers often delay upgrades, favoring legacy devices that lack the latest low‑pressure capabilities.

Other Challenges

Integration Complexity

Designing a sensor that fits into existing control architectures without extensive recalibration demands significant engineering effort. Companies without in‑house expertise must either partner with niche specialists or invest in long‑term development programs, both of which strain budgets.

MARKET RESTRAINTS

Limited Manufacturing Scale

Current production volumes for sub‑1 MPa hydrogen pressure sensors remain modest. Small batch runs keep unit costs high, making it difficult for new entrants to achieve economies of scale. Consequently, price‑sensitive segments such as small‑scale refueling stations often postpone adoption.

Certification Bottlenecks

Achieving certification under multiple regional safety standards can take 12‑18 months. The lengthy approval timeline discourages fast‑moving startups and creates a barrier to entry for firms attempting to launch innovative sensor designs quickly.

Finally, the perception of hydrogen as a high‑risk gas continues to shape procurement policies. Even when technical specifications are met, decision‑makers may favor proven, higher‑pressure solutions simply because they are more familiar, slowing the market’s overall momentum.

MARKET OPPORTUNITIES

Emerging Micro‑Grid Applications

Micro‑grids that incorporate hydrogen storage are beginning to require granular pressure data to balance load and generation efficiently. Supplying sensors that can operate continuously at pressures below 1 MPa opens a niche where value‑added services such as remote monitoring can be monetized.

Strategic Partnerships with OEMs

Collaborations between sensor manufacturers and fuel‑cell OEMs are fostering co‑development programs that embed low‑pressure sensing directly into core modules. These alliances shorten time‑to‑market for next‑generation products and create a recurring revenue stream through firmware upgrades and calibration services.

Additionally, the rollout of hydrogen‑fueled public transport in several metropolitan areas presents a geographic expansion prospect. Cities that commit to hydrogen buses and shuttle fleets will need large numbers of compliant pressure sensors, offering a predictable demand pipeline for suppliers ready to scale.

Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market Trends

Materials Innovation Drives Adoption

The most visible shift in the Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market stems from advances in barrier‑material engineering. Gold‑plated diaphragms, dual‑layer gold‑ceramic coatings, and high‑nickel stainless‑steel or titanium wetted parts now form the baseline for new product generations. These selections directly mitigate hydrogen permeation and embrittlement, two failure modes that previously limited sensor longevity in electrolyzer and fuel‑cell loops. As manufacturers embed these materials, the resulting units sustain zero‑drift and temperature stability over thousands of start‑stop cycles, a performance envelope that aligns tightly with the reliability expectations of hydrogen‑production equipment providers.

Other Trends

Digital Calibration and Interface Diversity

Beyond material upgrades, the market is witnessing a rapid convergence on digital calibration protocols combined with mixed‑signal output formats. Sensors that support 4‑20 mA, RS485, USB, and even Ethernet are being offered as drop‑in replacements for legacy analog devices. This flexibility enables system integrators to embed sensors within broader SCADA and IIoT frameworks, turning a simple pressure reading into actionable data for predictive maintenance. The shift reduces field‑service intervals and creates a secondary revenue stream for OEMs through subscription‑based calibration verification services.

Demand Concentration in Process‑Control Nodes

Demand concentration has moved away from high‑pressure storage tanks toward the lower‑pressure control points that sit upstream of compression and downstream of regeneration stages. Electrolyzer stacks, differential‑pressure regulators, and fuel‑cell balance‑of‑plant loops now rely on precise low‑pressure readings to optimize efficiency and safety interlocks. This reallocation of sensor deployment reflects a broader industry realization: stable operation of the entire hydrogen value chain hinges on accurate, resilient measurement at these critical junctions. Consequently, manufacturers that can deliver customized form factors,ranging from OEM sensing elements to fully packaged transmitters,are gaining preferential access to multi‑billion‑dollar project contracts in Europe, East Asia, and North America.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Overview of Low‑Pressure Hydrogen Sensors (<1 MPa)

Fuji Electric leads the low‑pressure hydrogen sensor segment, leveraging its long‑standing expertise in high‑temperature ceramic coatings and silicon‑on‑sapphire transducers. The company’s portfolio spans OEM sensing elements to fully integrated transmitters that output 4‑20 mA, RS485 and USB, satisfying the stringent zero‑drift and temperature‑compensation requirements of electrolyzer and fuel‑cell stacks. Fuji’s manufacturing footprint in Japan and Europe enables rapid delivery to project sites, while its dedicated validation labs have accumulated more than a decade of hydrogen‑media testing, giving it a decisive edge over broader‑scope sensor makers. The market structure reflects a tiered model: a handful of technology‑centric leaders supply core sensing platforms, while a larger pool of specialized firms focus on niche form factors, customized calibrations or cost‑optimized modules for regional integrators.

Beyond the tier‑one players, several niche manufacturers have carved out sustainable positions by concentrating on material barriers or application‑specific designs. NAGANO KEIKI and Daho Tronic, both headquartered in Japan, differentiate themselves with gold‑plated diaphragms and dual‑layer ceramic barriers that suppress hydrogen permeation in vacuum‑diff‑pressure loops. European firms such as KELLER Pressure and Variohm Eurosensor emphasize robust stainless‑steel and titanium wetted parts, targeting safety‑critical refueling stations in the EU. Micro Sensor, ESI Technology and STS Sensor Technik from Korea and Germany respectively, offer micro‑capacitive and piezoresistive modules tailored for compact laboratory benches, where rapid calibration cycles are valued. Chinese supplier Jiangmen Ever‑smart delivers cost‑effective OEM elements for large‑scale electrolyzer farms, while the French EFE focuses on modular differential‑pressure transmitters that integrate directly into process‑control PLCs. The competitive advantage of these companies lies less in raw accuracy and more in proven long‑term reliability under cyclic start‑stop conditions, an attribute that equipment OEMs prioritize when qualifying system safety.

List of Key Low Pressure Hydrogen Pressure Sensor Companies Profiled

- Fuji Electric Co., Ltd.

- NAGANO KEIKI CO., LTD.

- Daho Tronic Ltd.

- Baker Hughes Company

- KELLER Pressure AG

- Variohm Eurosensor Ltd.

- Micro Sensor Co., Ltd.

- ESI Technology Ltd.

- STS Sensor Technik Sirnach AG

- Jiangmen Ever‑smart Intelligent Control Instrument Co., Ltd.

- L’Essor Français Electronique (EFE)

- ESI Technology Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Thin‑film

|

| By Application |

|

Electrolyzer differential‑pressure control

|

| By End User |

|

Electrolyzer manufacturers

|

| By Material |

|

Gold‑plated diaphragmes

|

| By Integration Mode |

|

Industrial pressure transmitters

|

Regional Analysis: Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market

Europe

Recent EU directives tighten leakage tolerances for hydrogen distribution, prompting manufacturers to certify sensors against tighter error bands. The alignment of these standards with IEC‑62474 facilitates cross‑border component trade, encouraging suppliers to harmonize design specifications for the Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market.

European micro‑electronics hubs are increasingly integrating MEMS fabrication with sensor packaging, reducing lead times for bespoke pressure transducers. Partnerships between raw‑material producers and device assemblers create a semi‑closed loop that cushions the sector from global semiconductor volatility.

Refinery retrofits and emerging hydrogen‑fuel‑cell power plants cite the precise voltage‑drift characteristics of low‑pressure sensors as a key enabler for safety‑critical control loops, driving procurement cycles that favor vendors with proven field performance.

Leading European firms leverage deep domain expertise to differentiate on long‑term stability and integration flexibility, while newcomers focus on cost‑effective silicon‑on‑glass designs, intensifying a competitive landscape that rewards both innovation and price discipline.

North America

The United States and Canada are forging a parallel trajectory, with federal hydrogen incentives funneling capital into storage and distribution pilots that demand low‑pressure monitoring. A notable shift is the deployment of sensors in distributed‑generation stations where modularity and ruggedness outweigh ultra‑high precision. Industry consortia have begun aligning with ASTM standards, creating a de‑facto reference that eases cross‑supply‑chain negotiations. Meanwhile, the concentration of venture capital in the Silicon Valley ecosystem fuels start‑ups that experiment with novel polymer‑based diaphragms, promising lower production costs. These dynamics, combined with the region’s expansive natural‑gas retrofit initiatives, generate a hybrid market where legacy players and agile newcomers coexist, each targeting distinct niche applications within the broader Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market.

Asia‑Pacific

Asia‑Pacific exhibits a heterogeneous landscape: Japan’s mature fuel‑cell ecosystem contrasts with China’s aggressive scaling of hydrogen refueling infrastructure. Both economies prioritize sensor reliability under diverse climatic conditions, prompting R&D on temperature‑compensated ceramic membranes. Government roadmaps in South Korea and Australia allocate funding for hydrogen corridors, embedding sensor specifications within project tender documents. The region also benefits from a dense network of contract manufacturers capable of rapid prototype turnover, enabling OEMs to iterate designs in response to field feedback. As industrial hydrogen consumption expands beyond petrochemicals into steel decarbonisation, the demand for low‑pressure pressure transducers is expected to ripple across traditional and emerging sectors alike.

South America

Brazil’s nascent hydrogen agenda is anchored in its renewable‑energy surplus, with pilot projects exploring wind‑to‑hydrogen conversion for remote mining operations. Sensor requirements are shaped by the need for rugged enclosures that tolerate high humidity and dust ingress. Local industrial conglomerates are beginning to source Low Pressure Hydrogen Pressure Sensor (Below 1MPa) components from European partners, while also investing in technology transfer agreements to develop in‑house calibration capabilities. The emphasis on cost‑efficiency and durability reflects the broader market reality in South America, where capital constraints drive a preference for proven, low‑maintenance solutions.

Middle East & Africa

In the Middle East, the United Arab Emirates and Saudi Arabia are leveraging abundant solar resources to underpin green‑hydrogen projects, and these initiatives increasingly call for precise pressure monitoring at modest pressures to safeguard electrolyzer performance. The region’s oil‑centric engineering expertise is being repurposed to fabricate sensor housings that meet stringent corrosion‑resistance criteria. African markets, still in early adoption phases, are watching these developments closely; pilot installations in South Africa’s renewable‑hydrogen testbeds highlight a cautious yet growing appetite for sensors that can operate reliably in austere environments. Together, these trends illustrate a slowly consolidating demand base that, while modest in volume, signals long‑term strategic relevance for the Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market.

Report Scope

This market research report provides a comprehensive analysis of the Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market?

-> Global Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market was valued at USD 38.17 million in 2025 and is expected to reach USD 197 million by 2032.

Which key companies operate in Low Pressure Hydrogen Pressure Sensor (Below 1MPa) Market?

-> Key players include Baker Hughes Company, NAGANO KEIKI CO., LTD., Fuji Electric Co., Ltd., Daho Tronic Ltd., KELLER Pressure AG, Micro Sensor Co., Ltd., and STS Sensor Technik Sirnach AG, among others.

What are the key growth drivers?

-> Key growth drivers include rapid expansion of electrolyzers, increasing global hydrogen demand driven by policy targets, fuel‑cell system integration, and the need for precise low‑pressure safety and efficiency controls.

Which region dominates the market?

-> Europe holds the largest market share due to a mature supplier base and early hydrogen infrastructure projects, while Asia‑Pacific exhibits the fastest growth rate.

What are the emerging trends?

-> Emerging trends include advanced gold‑plated and ceramic barrier diaphragms, digital calibration with IoT connectivity, and system‑level measurement solutions for integrated hydrogen plants.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...