Crankcase Pressure Sensor Market Insights

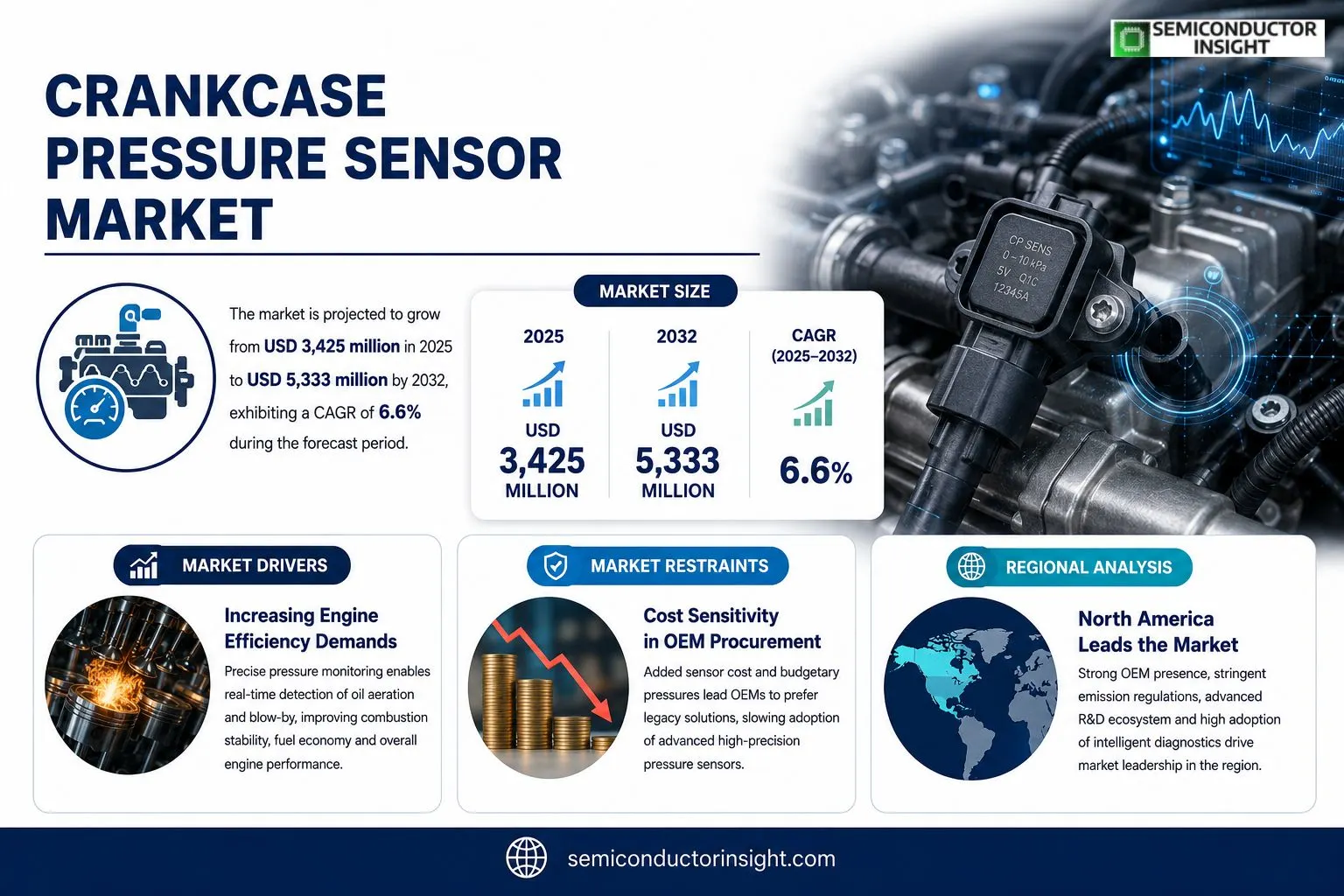

Global Crankcase Pressure Sensor market size was valued at USD 3,425 million in 2025. The market is projected to grow from USD 3,425 million in 2025 to USD 5,333 million by 2032, exhibiting a CAGR of 6.6% during the forecast period.

Crankcase pressure sensors are installed on automotive and industrial engines to monitor pressure variations inside the crankcase. By delivering precise pressure readings, they enable real‑time assessment of engine condition and help prevent failures caused by abnormal pressure spikes.The expansion stems from rising engine‑efficiency requirements, stricter emission regulations and growing adoption of intelligent diagnostics across vehicles. Upstream supplies such as silicon wafers and ceramic housings support scaling production, while downstream demand from automakers and equipment manufacturers fuels ongoing consumption.

MARKET DRIVERS

Increasing Engine Efficiency Demands

Automakers are redesigning powertrains to extract marginal gains in fuel consumption, and Crankcase Pressure Sensor Market benefits from this engineering focus. Precise measurement of crankcase pressure enables real‑time detection of oil aeration and blow‑by, which directly influences combustion stability and, consequently, mileage. The ability to fine‑tune valve timing and injection events based on sensor feedback is becoming a differentiator for premium models.

Regulatory Push for Emissions Control

Stringent emission standards across North America and Europe now require manufacturers to monitor internal engine parameters more closely. Crankcase pressure data helps certify compliance by limiting unburned hydrocarbons that escape through the crankcase ventilation system. Companies that integrate these sensors early gain certification advantages and avoid costly retrofits.

➤ “Accurate crankcase monitoring is no longer optional; it is a core pillar of next‑generation engine management.”

Beyond compliance, the data stream supports predictive maintenance strategies. Fleet operators, especially in logistics, are adopting condition‑based service models that rely on continuous sensor inputs to schedule oil changes only when necessary, reducing downtime and operating expense.

MARKET CHALLENGES

Technical Integration Hurdles

Embedding crankcase pressure sensors into existing engine architectures demands redesign of oil galleries and electronic wiring. OEMs face constraints related to space, heat resistance, and electromagnetic compatibility, which can slow adoption cycles, particularly for legacy platforms.

Other Challenges

Supply Chain Vulnerabilities

The sensor’s silicon and MEMS components depend on semiconductor foundries that are subject to capacity fluctuations. Any disruption can ripple through vehicle production schedules, prompting manufacturers to maintain higher safety stocks.

MARKET RESTRAINTS

Cost Sensitivity in OEM Procurement

While the functional benefits are clear, the added bill of materials still represents a measurable expense for volume‑driven manufacturers. Budgetary pressures compel OEMs to prioritize cost‑effective solutions, often favoring legacy sensor technologies that lack the advanced diagnostic capabilities of newer designs.

MARKET OPPORTUNITIES

Hybrid and Electrified Powertrain Support

The shift toward electrified drivetrains introduces new thermal and lubrication regimes where crankcase pressure monitoring can mitigate oil degradation and extend service intervals. Suppliers that tailor sensor packages for hybrid engines stand to capture a growing niche within the broader Crankcase Pressure Sensor Market.

Crankcase Pressure Sensor Market Trends

Automotive Efficiency and Emissions Regulation

The push for tighter emissions standards has turned crankcase pressure monitoring into a non‑negotiable element of engine control strategies. Manufacturers are redesigning combustion chambers and after‑treatment systems, and the sensors that relay real‑time pressure data have become essential for fine‑tuning fuel injection and valve timing. By delivering more accurate pressure feedback, these devices enable engines to operate closer to optimal combustion points, which reduces unburned hydrocarbons and improves fuel mileage. The ripple effect is evident in procurement plans: OEMs are specifying higher‑precision models for both passenger cars and heavy‑duty trucks, prompting suppliers to accelerate product‑grade upgrades.

Other Trends

Supply Chain and Material Innovation

Raw‑material costs for silicon wafers and specialty ceramics have shown modest volatility, yet suppliers are mitigating risk through strategic partnerships with wafer fabs and metal‑housing producers. This collaborative approach shortens lead times and improves yield consistency, directly influencing the gross margin profile of sensor manufacturers. Moreover, the adoption of advanced packaging techniquessuch as wafer‑level chip‑scale packaginghas reduced the bill of materials while enhancing resistance to oil‑vapour contamination, a common failure mode in marine applications.

Intelligent Diagnostics and Electrification

Vehicle‑level connectivity and over‑the‑air update capabilities have amplified the diagnostic value of crankcase pressure signals. Modern power‑train control units now cross‑reference pressure readings with vibration and temperature data to predict bearing wear before a failure manifests. In hybrid and electric drivetrains, where auxiliary internal‑combustion engines serve as range extenders, the sensor provides a safeguard that allows these engines to run intermittently without compromising system reliability. The convergence of sensor data with cloud‑based analytics platforms is encouraging OEMs to treat pressure information as a telemetry asset rather than a simple safety component.

Competitive Landscape Evolution

Market participants are differentiating themselves through three converging strategies: expanding portfolio breadth across piezoelectric, piezoresistive, and capacitive families; investing in IP‑protected algorithms that translate raw pressure curves into actionable alerts; and leveraging global manufacturing footprints to serve regional demand spikes, especially in Asia where new vehicle platforms are being launched at a rapid cadence. As production volumes climb toward the two‑hundred‑million‑unit threshold, economies of scale are sharpening price competition, while the need for robust, high‑accuracy sensors sustains a premium segment that rewards technical excellence. For buyers, the result is a richer selection of sensors that can be matched to specific engine architectures, regulatory environments, and service‑life expectations.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Competitive Overview of Crankcase Pressure Sensors

Sensata Technologies commands the upper tier of the crankcase pressure sensor arena, leveraging an extensive portfolio that spans piezo‑electric, piezoresistive and capacitive designs. Its deep integration with major automotive OEMs provides a stable revenue base, while strategic investments in silicon‑on‑glass processing have sharpened its cost curve. The company’s ability to supply both analog voltage and digital signal variants has cemented its role as a preferred partner for power‑train engineers seeking tight pressure regulation across internal‑combustion, hybrid and emerging electrified platforms. This breadth of offering, coupled with a global service network, results in a market structure where a handful of Tier‑1 suppliers collectively capture a sizable share, pressuring smaller firms to specialize or consolidate.Beyond the Tier‑1 circle, a mix of regional specialists and diversified electronics groups adds depth to the competitive field. Bosch Sensortec, Denso Corporation, Continental AG and TE Connectivityeach linked to strong automotive sensor divisionssustain a solid foothold through tailored product lines and strong aftermarket support. Meanwhile, companies such as Infineon Technologies, NXP Semiconductors, Honeywell International, Valeo, Mahle GmbH and the Chinese manufacturers KAISHENG, Ampron, KeFeng, as well as equipment giants John Deere and Caterpillar, focus on niche segments ranging from heavy‑machinery diagnostics to marine engine applications. Their strategic emphasis on ruggedised housings and IP‑rated designs enables them to capture markets where durability outweighs pure performance metrics, fostering a diversified supplier ecosystem.

List of Key Crankcase Pressure Sensor Companies Profiled

- Sensata Technologies

- Bosch Sensortec

- Denso Corporation

- Continental AG

- TE Connectivity

- Infineon Technologies

- NXP Semiconductors

- Honeywell International

- Valeo

- Mahle GmbH

- Ampron

- KAISHENG

- John Deere

- Caterpillar

- KeFeng

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Piezoelectric is emerging as the preferred technology because of its high sensitivity and robustness in harsh engine environments.

|

| By Application |

|

Automobile Engines remain the dominant application, driven by stringent emission standards and the rise of intelligent vehicle platforms.

|

| By End User |

|

OEMs drive innovation cycles, embedding sensors directly into engine control units to meet regulatory and performance goals.

|

| By Protection Level |

|

IP67/IP69K variants are gaining traction as engines operate in increasingly demanding environments, such as high‑performance heavy machinery and marine applications.

|

| By Signal Output |

|

Digital (CAN/LIN) output is becoming a strategic focus as vehicle architectures shift toward networked sensor ecosystems.

|

Regional Analysis: Crankcase Pressure Sensor Market

North America

Automotive firms are embedding multi‑sensor platforms that combine crankcase pressure data with vibration and temperature metrics, enabling more granular engine health models. This convergence reduces wiring complexity and opens up software‑driven calibration pathways, a trend gaining traction among Tier‑1 suppliers.

The EPA’s recent revisions to evaporative emission limits have compelled manufacturers to adopt higher‑precision pressure monitoring. Compliance timelines force rapid product cycles, pressuring suppliers to shorten development lead‑times while maintaining reliability standards.

Strategic alliances between major chassis makers and sensor specialists are redefining procurement models. Joint‑development agreements allow OEMs to co‑own intellectual property, thereby securing differentiated offerings for premium vehicle lines.

Recent semiconductor shortages prompted manufacturers to diversify material sources for MEMS‑based pressure chips. Dual‑sourcing strategies and localized fabrication hubs are now integral to risk‑mitigation roadmaps.

Europe

European automotive firms are navigating a regulatory environment that emphasizes low‑emission powertrains and electrification. While fully electric vehicles reduce reliance on crankcase pressure data, internal combustion engines (ICE) remain prevalent in commercial fleets, preserving a steady demand for robust sensors. Engineers are focusing on sensor designs that can operate under higher boost pressures associated with downsized turbocharged engines. Concurrently, collaborative research initiatives across Germany, France, and Italy aim to harmonize sensor calibration standards, facilitating cross‑border component interchangeability and reducing unit costs.

Asia-Pacific

The Asia‑Pacific landscape is defined by rapid vehicle production scaling in China, India, and Southeast Asia. Manufacturers in these markets prioritize cost‑effective sensor solutions that meet evolving local emission rules without compromising durability under diverse climate conditions. A notable shift toward domestic sensor fabs is reducing import reliance, while joint ventures between multinational OEMs and regional suppliers accelerate technology transfer. The confluence of high production volumes and emerging quality benchmarks is reshaping Crankcase Pressure Sensor Market’s pricing dynamics in this region.

South America

In South America, market activity is anchored by Brazil’s sizable automotive sector and Argentina’s growing light‑truck fleet. Economic volatility has tempered capital spending, yet fleet operators recognize the value of pressure‑based diagnostics to extend engine life amid rising fuel costs. Local suppliers are leveraging modular sensor architectures to serve both legacy ICE platforms and newer hybrid models, positioning themselves as flexible partners for OEMs seeking incremental upgrades without wholesale redesign.

Middle East & Africa

The Middle East & Africa region exhibits a dichotomy between oil‑rich nations with high‑end vehicle imports and emerging markets focused on affordable mobility solutions. Harsh desert climates demand sensors with enhanced temperature tolerance and dust‑proof housings. Strategic partnerships with European sensor firms are facilitating technology diffusion, while regional automotive assemblers are integrating pressure monitoring into off‑road and heavy‑duty applications, reflecting a niche but growing demand segment.

Report Scope

This market research report provides a comprehensive analysis of the Crankcase Pressure Sensor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- ✅ Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- ✅ Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- ✅ Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- ✅ Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- ✅ Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- ✅ Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- ✅ Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- ✅ Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Crankcase Pressure Sensor Market?

-> Crankcase Pressure Sensor Market was valued at USD 3425 million in 2025 and is expected to reach USD 5333 million by 2032, growing at a CAGR of 6.6% during the forecast period.

Which key companies operate in Crankcase Pressure Sensor Market?

-> Key players include Sensata Technologies, KAISHENG, Ampron, Caterpillar, KEFENG, Dorman, John Deere, and Ecufiles.

What are the key growth drivers?

-> Key growth drivers include the automotive industry’s rising demand for engine performance and safety, stricter emission and environmental regulations, the expansion of intelligent and electrified vehicle platforms, and increasing adoption of vehicle fault‑diagnosis and remote diagnostics technologies.

Which region dominates the market?

-> Asia‑Pacific leads the market owing to its large automotive manufacturing base, rapid adoption of advanced powertrain technologies, and strong investments in intelligent driving solutions.

What are the emerging trends?

-> Emerging trends include integration of crankcase pressure sensors in hybrid and electric powertrains, deployment of sensors for real‑time fault diagnosis in connected vehicles, and the development of low‑cost, high‑accuracy sensor designs driven by energy‑saving policies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...