IMU Sensor Module Market Insights

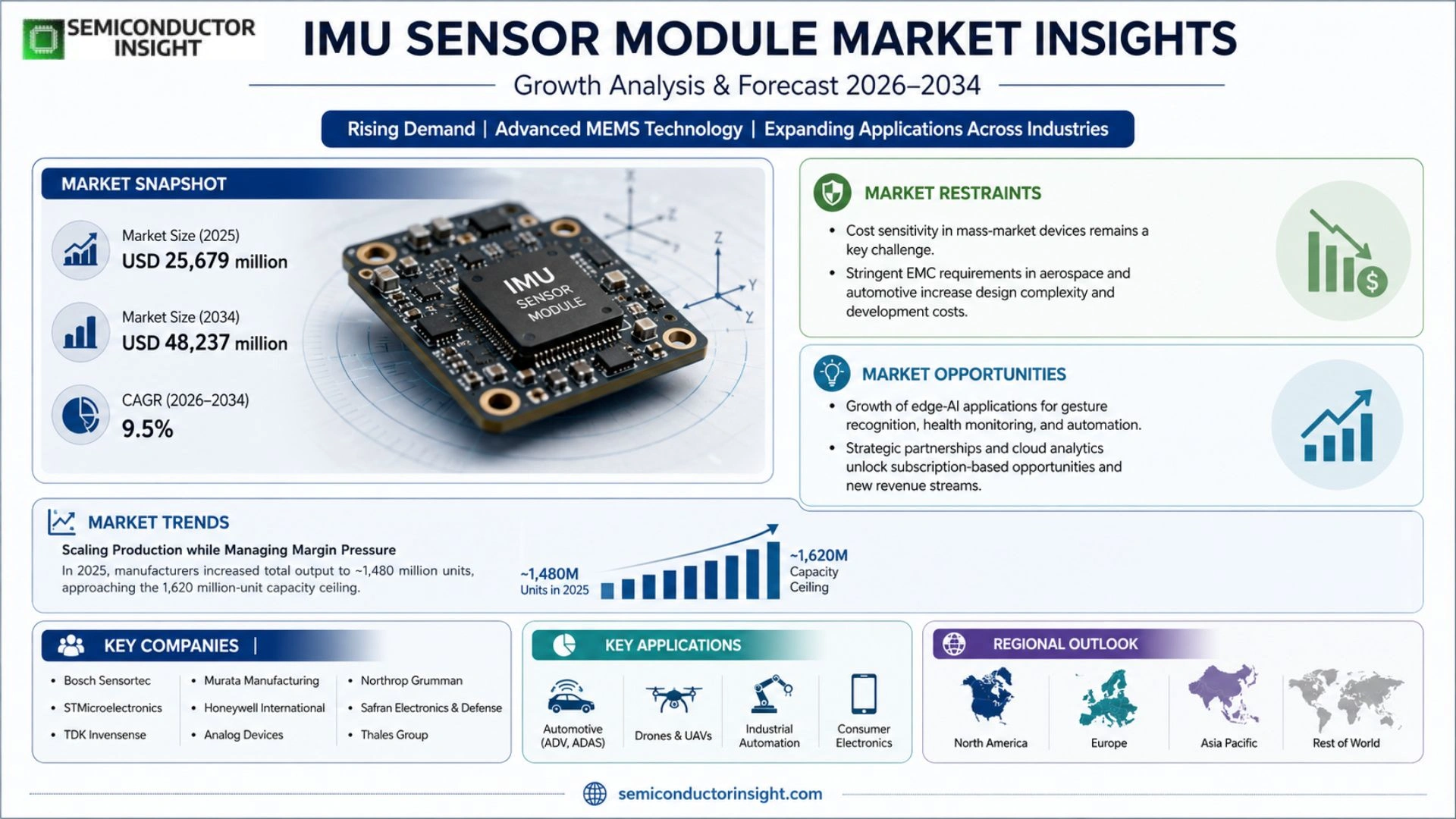

Global IMU Sensor Module market size was valued at USD 25,679 million in 2025. The market is projected to reach USD 48,237 million by 2034, exhibiting a CAGR of 9.5% during the forecast period.

An IMU Sensor Module (Inertial Measurement Unit) integrates an accelerometer, gyroscope and often a magnetometer to deliver real‑time linear acceleration, angular velocity and orientation data. This capability underpins motion tracking, attitude estimation and inertial navigation across robotics, drones, automotive ADAS and aerospace platforms.

The sector is expanding because demand for autonomous systems and advanced driver‑assistance continues to rise, while consumer electronics sustain high volume sales. Pricing pressure persists in low‑cost segments, yet high‑precision industrial and defense applications support premium pricing. Leading suppliers such as Bosch Sensortec, STMicroelectronics, TDK InvenSense and Honeywell International are accelerating product roadmaps and forming strategic alliances to capture emerging opportunities.

MARKET DRIVERS

Rising Demand for Advanced Motion Sensing

The proliferation of autonomous platforms,ranging from delivery drones to collaborative robots,requires an unprecedented level of precision in orientation and acceleration measurement. Manufacturers are therefore integrating higher‑performance IMU sensor modules to meet the tighter latency and accuracy thresholds set by next‑generation control algorithms.

Miniaturization and Power‑Efficiency Trends

Progress in MEMS fabrication has shrunk device footprints while slashing power draw, enabling IMU sensor modules to be embedded in wearables and IoT edge devices that previously could not accommodate bulky motion‑tracking hardware. Design engineers capitalize on these efficiencies to add inertial capabilities without compromising battery life.

➤ “The confluence of AI‑driven sensor fusion and ultra‑low‑power MEMS is redefining product form factors across automotive, consumer, and industrial segments.”

Regulatory emphasis on safety and predictive maintenance further motivates original equipment manufacturers to adopt richer inertial data streams. By leveraging the granular insights that modern IMU sensor modules provide, firms can demonstrate compliance while unlocking new service‑based revenue models.

MARKET CHALLENGES

Complex Calibration Requirements

Accurate output from an IMU sensor module hinges on meticulous calibration of gyroscope, accelerometer, and magnetometer axes. Small errors can cascade into significant drift, especially in high‑speed applications, compelling end‑users to invest in specialized calibration tooling and expertise.

Other Challenges

Supply‑Chain Volatility

Global shortages of high‑purity silicon wafers and rare‑earth materials intermittently constrain production capacity, leading to longer lead times and price fluctuations that strain budgeting cycles for large‑scale projects.

Furthermore, the steep learning curve associated with sensor‑fusion algorithms deters smaller firms from adopting sophisticated IMU solutions, limiting market penetration in niche verticals.

MARKET RESTRAINTS

Cost Sensitivity in Mass‑Market Devices

Although MEMS technology has driven prices down, the cumulative cost of an IMU sensor module,including packaging, testing, and firmware,remains a critical factor for ultra‑low‑cost consumer gadgets. Price‑pressured OEMs often opt for legacy components that trade performance for affordability.

In addition, stringent electromagnetic compatibility (EMC) requirements in aerospace and automotive sectors impose extra design safeguards, inflating development overhead and narrowing the pool of compliant modules.

MARKET OPPORTUNITIES

Growth of Edge‑AI Applications

The emergence of on‑device AI for gesture recognition, fall detection, and predictive analytics creates a fertile ground for IMU Sensor Module market. By embedding advanced processing capabilities directly alongside inertial hardware, vendors can deliver turnkey solutions that reduce system‑level integration effort.

Strategic partnerships between sensor manufacturers and cloud analytics providers also open avenues for subscription‑based services, turning raw motion data into actionable insights for fleet management, health monitoring, and industrial automation.

IMU Sensor Module Market Trends

Scaling Production while Managing Margin Pressure

IMU Sensor Module market has entered a phase where volume growth collides with tightening economics. In 2025, manufacturers pushed total output to roughly 1,480 million units, edging close to the 1,620 million‑unit capacity ceiling. Unit pricing settled near US$19, a level that squeezes gross margins to about 42 %. This combination forces suppliers to optimise fab yields and streamline assembly workflows. Companies that have entrenched themselves in MEMS wafer sourcing reap cost advantages, while those reliant on third‑party integration face sharper competitive pressure. The outcome is a bifurcated landscape: commodity‑grade modules dominate consumer segments, whereas precision‑engineered parts retain higher profitability in automotive and defense applications. For investors, the trade‑off between scale and margin dictates whether a firm can sustain earnings growth without sacrificing product quality.

Other Trends

Shift Toward High‑Accuracy Modules

Demand for mid‑ and high‑accuracy IMU sensors is accelerating as autonomous robotics and advanced driver‑assistance systems require tighter error budgets. Manufacturers are expanding calibration expertise and embedding more sophisticated sensor‑fusion algorithms directly into the module firmware. This move not only lifts the functional ceiling of the product but also creates a barrier to entry for low‑cost producers lacking R&D depth. Consequently, the value segment,anchored by tactical and navigation‑grade devices,is seeing increased pricing power, while the low‑accuracy tier contends with commoditisation. Suppliers that can bridge the gap by offering modular upgrade paths stand to capture buyers who wish to future‑proof their designs without a full redesign.

Geographic Realignment of Supply Chains

Regional dynamics are reshaping IMU Sensor Module ecosystem. North America continues to lead in high‑precision applications, yet China’s manufacturing base is expanding its share of volume production through aggressive capacity investments. This geographic shift pressures western firms to reconsider logistics and inventory strategies, especially as trade policies introduce new tariff variables. Companies that establish dual‑sourcing arrangements,leveraging both Chinese fabs for volume and European or U.S. facilities for high‑grade parts,benefit from risk mitigation and quicker time‑to‑market. Moreover, the emergence of localised design houses in Asia accelerates innovation cycles, compelling traditional OEMs to collaborate more closely with regional partners to retain relevance in fast‑moving markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive dynamics and concentration in IMU Sensor Module sector

IMU Sensor Module market is anchored by a handful of manufacturers that control both component sourcing and high‑volume assembly. Bosch Sensortec stands out for its end‑to‑end MEMS wafer capability, deep automotive ADAS relationships, and a product portfolio that spans the low‑cost consumer segment to premium navigation‑grade modules. Its strategic investments in silicon‑on‑glass technology have lowered unit costs while preserving the accuracy needed for automotive and industrial applications, allowing the company to capture a sizable share of the volume‑driven 6‑axis and 9‑axis segments. Parallel to Bosch, STMicroelectronics leverages a global fabrication network and a strong presence in consumer electronics, translating its scale into competitive pricing that keeps price pressure at bay in the crowded hobby‑drone market. Together, these leaders shape a bifurcated value chain where the commodity tier is dominated by high‑output facilities and the precision tier is fed by firms with niche calibration expertise and defense contracts.

Beyond the dominant tier, a diverse set of niche players adds depth to the competitive landscape. TDK Invensense and Murata Manufacturing specialize in compact, high‑frequency modules that serve wearables and handheld devices, differentiating themselves through proprietary sensor fusion algorithms. Honeywell International and Analog Devices occupy the high‑accuracy, tactical‑grade niche, supplying aerospace and defense customers that demand sub‑arc‑second stability. Meanwhile, Northrop Grumman, Safran Electronics & Defense, and Thales Group translate their systems‑integration heritage into ruggedized IMUs for unmanned aerial systems and space platforms. Emerging challengers such as Trimble Inc, Collins Aerospace, Epson, Sensonor, Innalabs, Navgnss, Norinco Group, Suteng Robotics, Benewake, Comnav Technology, and Unicore Communications are expanding their footprints by targeting verticals like precision agriculture, robotics, and IoT edge devices, often through strategic partnerships or focused R&D programs that accelerate time‑to‑market for custom‑configured 10‑axis+ modules.

List of Key IMU Sensor Module Companies Profiled

- Bosch Sensortec

- STMicroelectronics

- TDK Invensense

- Murata Manufacturing

- Honeywell International

- Analog Devices

- Northrop Grumman

- Safran Electronics & Defense

- Thales Group

- Trimble Inc

- Collins Aerospace

- Epson

- Sensonor

- Innalabs

- Navgnss

- Norinco Group

- Suteng Robotics

- Benewake

- Comnav Technology

- Unicore Communications

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

6‑axis IMU is the prevailing choice for most consumer‑grade products and mid‑range industrial devices.

|

| By Application |

|

Industrial robotics is emerging as the most influential application driver.

|

| By End User |

|

Industrial automation integrators shape the value‑added segment of the market.

|

| By Accuracy Grade |

|

High‑accuracy IMU underpins the most demanding aerospace and defense applications.

|

| By Sensor Configuration |

|

Combined accelerometer‑gyroscope (6‑axis) dominates mainstream system design.

|

Regional Analysis: IMU Sensor Module Market

Asia-Pacific

Concentrations of wafer‑fab capacity in Shenzhen, Seoul, and Tokyo enable high‑volume production of MEMS cores at competitive cost. The proximity of these plants to major automotive and consumer‑electronics assemblers shortens logistics, encouraging just‑in‑time deliveries for IMU Sensor Module suppliers.

Tier‑one automotive groups in the region are integrating multi‑axis IMU modules into advanced driver‑assistance systems, electric‑vehicle stability controls, and in‑cab motion monitoring, thereby expanding the functional scope of traditional sensor packages.

The proliferation of health‑tracking bands and AR headsets in markets such as India and Indonesia pushes manufacturers to prioritize low‑power, high‑precision IMU modules that can operate continuously without draining battery life.

Strategic alliances between component distributors and original equipment manufacturers streamline component sourcing, reduce lead times, and enhance visibility across IMU Sensor Module value chain.

North America

In North America, IMU Sensor Module Market is shaped by the maturation of autonomous‑vehicle testing corridors and the strong presence of defense contractors seeking high‑accuracy inertial navigation. The United States leverages its deep pool of algorithmic expertise to pair raw sensor data with sophisticated sensor‑fusion software, creating higher‑value solutions for industrial automation. Although manufacturing costs are higher than in Asia, the region compensates with robust intellectual‑property ecosystems and a willingness to invest in early‑stage technology pilots, particularly in aerospace and medical‑device applications. These dynamics encourage multinational firms to retain critical design and validation activities domestically while outsourcing volume production to lower‑cost regions.

Europe

European stakeholders focus on regulatory compliance and sustainability, influencing IMU Sensor Module specifications for automotive emissions control and railway safety systems. Germany and France host leading automotive suppliers that require modular sensor packages capable of seamless integration with existing vehicle networks. Meanwhile, the Nordic corridor emphasizes precision agriculture, where sensor reliability under harsh weather conditions becomes a decisive factor. Cross‑border collaborations under EU research frameworks foster joint‑development projects, allowing firms to share risk and accelerate time‑to‑market for next‑generation motion‑tracking technologies.

South America

South American markets are gradually embracing IMU Sensor Modules as local manufacturers explore low‑cost vehicle telematics and agricultural machinery upgrades. Brazil’s expanding renewable‑energy sector presents an opportunity for sensor‑enabled wind‑turbine monitoring, while Argentine startups experiment with drone‑based surveying that relies on accurate inertial measurement. The region’s limited domestic fabs push firms to import core components, but growing demand encourages regional assembly hubs that add value through customized firmware and integration services.

Middle East & Africa

In the Middle East and Africa, IMU Sensor Module Market is tied to infrastructure development and defense modernization programs. Saudi Arabia’s smart‑city projects demand motion sensors for building management and autonomous transport pilots, whereas South Africa’s mining industry seeks rugged IMU solutions for equipment health monitoring. Limited local production capabilities mean most modules are sourced from established Asian suppliers, yet partnerships are emerging that focus on adaptation to extreme temperature ranges and dust‑prone environments, creating niche opportunities for specialized module variants.

Report Scope

This market research report provides a comprehensive analysis of the IMU Sensor Module Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of IMU Sensor Module Market?

-> IMU Sensor Module Market was valued at USD 25,679 million in 2025 and is expected to reach USD 48,237 million by 2034, representing a compound annual growth rate of 9.5%

Which key companies operate in IMU Sensor Module Market?

-> Key players include Bosch Sensortec, STMicroelectronics, TDK InvenSense, Murata Manufacturing, Honeywell International, Analog Devices, Northrop Grumman, Safran Electronics & Defense, Thales Group, Trimble Inc, among others.

What are the primary growth drivers for IMU Sensor Module market?

-> Growth is driven by rising demand in robotics, drones, automotive ADAS, consumer electronics, and aerospace navigation systems, as well as the broader expansion of autonomous and spatial‑awareness technologies.

Which region shows the strongest market momentum?

-> The available data does not specify a single dominant region; however, the market is globally distributed across North America, Europe, and Asia with notable activity in each.

What emerging trends are shaping IMU Sensor Module market?

-> Emerging trends include integration with AI/IoT for smarter motion analytics, miniaturization for wearable and UAV applications, and the development of high‑precision navigation‑grade modules for autonomous vehicles and defense systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...