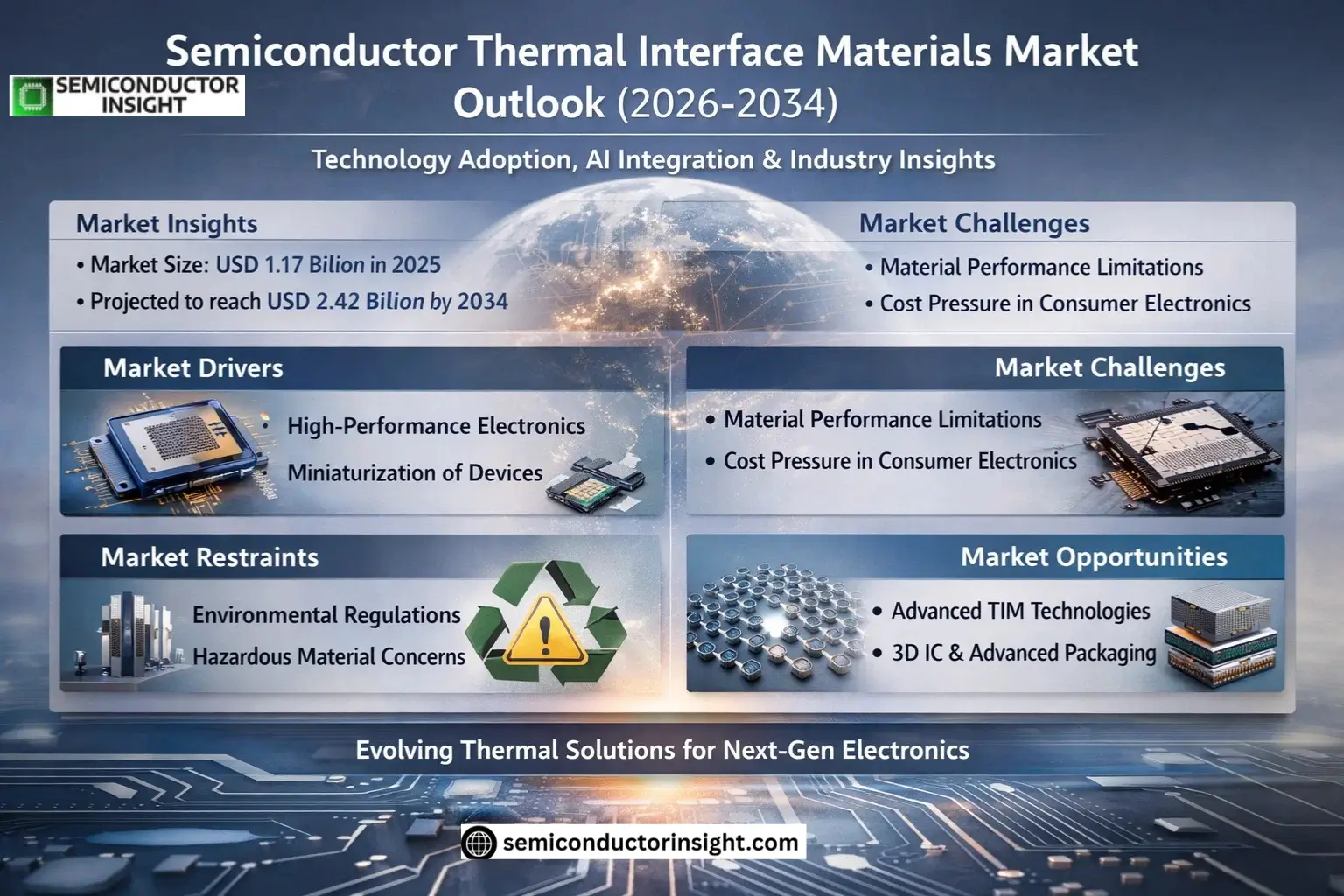

Market Insights

Global Semiconductor Thermal Interface Materials Market size was valued at USD 1.17 billion in 2025. The market is projected to grow from USD 1.31 billion in 2026 to USD 2.42 billion by 2034, exhibiting a CAGR of 11.1% during the forecast period.

Semiconductor thermal interface materials (TIMs) are specialized heat-conducting compounds designed to optimize thermal transfer between semiconductor components and heat sinks or cooling systems. These materials minimize interfacial resistance, ensuring efficient heat dissipation in high-performance electronics such as CPUs, GPUs, power modules, and LED assemblies. Key TIM categories include thermal greases, gap fillers, phase-change materials, and advanced carbon or metal-based solutions each engineered for specific conductivity requirements and mechanical properties.

The market growth is driven by escalating power densities in AI processors and 5G infrastructure, alongside stricter thermal management standards for electric vehicles and data centers. Recent innovations like graphene-enhanced TIMs and automated dispensing systems are addressing challenges in miniaturization and reliability. Leading suppliers such as Henkel, Dow, and Shin-Etsu Chemical dominate the competitive landscape through proprietary formulations tailored for emerging semiconductor packaging architectures.

MARKET DRIVERS

Growing Demand for High-Performance Electronics

Semiconductor Thermal Interface Materials Market is experiencing robust growth driven by increasing demand for advanced cooling solutions in high-performance electronics. With processors generating more heat in compact devices, efficient thermal management has become critical. The market is projected to grow at a CAGR of 7.2% through 2028, fueled by applications in 5G infrastructure, AI hardware, and electric vehicles.

Miniaturization of Semiconductor Devices

As semiconductor components shrink in size while increasing in power density, thermal interface materials play a vital role in heat dissipation. Leading chip manufacturers are adopting advanced thermal interface materials to prevent overheating in devices ranging from smartphones to data center servers.

Emerging technologies like 3D IC packaging and heterogenous integration are creating new demands for high-performance thermal interface solutions.

MARKET CHALLENGES

Material Performance Limitations

While thermal interface materials are critical for semiconductor applications, many existing materials struggle to meet the demanding thermal conductivity requirements of next-generation chips. The industry faces challenges in developing materials that combine high performance with long-term reliability under thermal cycling.

Other Challenges

Cost Pressure in Consumer Electronics

Price sensitivity in consumer electronics restricts adoption of premium thermal interface materials, forcing manufacturers to balance performance with cost constraints.

MARKET RESTRAINTS

Stringent Environmental Regulations

Environmental concerns regarding certain thermal interface materials containing hazardous substances are limiting material options. Regulatory frameworks like REACH and RoHS are pushing manufacturers to develop eco-friendly alternatives without compromising thermal performance.

MARKET OPPORTUNITIES

Advancements in TIM Technologies

Semiconductor Thermal Interface Materials Market presents significant opportunities with the development of innovative materials like graphene-based TIMs and phase change materials. These advanced solutions offer superior thermal conductivity (exceeding 20 W/mK) while addressing reliability concerns in high-temperature applications.

Semiconductor Thermal Interface Materials Market Trends

Advanced Packaging Driving TIM Innovation

Semiconductor Thermal Interface Materials Market is experiencing significant transformation due to the increasing adoption of advanced packaging technologies. As chip manufacturers move toward 3D IC architectures and heterogenous integration, thermal management requirements are becoming more stringent. TIM formulations are evolving to address higher heat fluxes while maintaining mechanical stability in compact designs. Manufacturers are focusing on materials with superior wetting properties to minimize interfacial thermal resistance in complex multi-chip modules.

Other Trends

Shift Toward Greener Formulations

Environmental regulations are prompting TIM suppliers to develop low-volatility, halogen-free materials with controlled siloxane emissions. This trend is particularly strong in consumer electronics and data center applications where material safety and sustainability are prioritized. Leading companies are investing in eco-friendly polymer matrices and high-performance ceramic fillers to meet both thermal and compliance requirements.

Application-Specific TIM Development

Demand is growing for specialized TIM solutions tailored to different semiconductor applications. Data center servers require ultra-stable materials that can withstand years of continuous operation, while mobile devices need thin, conformable TIMs for space-constrained designs. The market is seeing increased segmentation with product differentiation based on thermal conductivity ranges, application methods, and long-term reliability characteristics.

Supply Chain Consolidation

The semiconductor TIM industry is witnessing moderate consolidation as suppliers seek to strengthen their material science expertise and application engineering capabilities. Top players are acquiring specialized filler manufacturers and formulators to secure critical supply chains and enhance product performance. This trend reflects the growing importance of vertically integrated solutions in meeting the exacting requirements of semiconductor packaging.

COMPETITIVE LANDSCAPE

Key Industry Players

Thermal Management Innovation Drives Semiconductor TIM Market Consolidation

Semiconductor Thermal Interface Materials Market is moderately consolidated, with the top five suppliers controlling approximately 50% of global revenue. DuPont, Dow, and Henkel lead through comprehensive materials science portfolios and qualification advantages in high-power applications. These companies benefit from vertical integration of polymer matrices and advanced filler technologies, along with established relationships with major semiconductor packaging foundries and OEMs.

Specialty chemical players like Shin-Etsu Chemical and 3M compete through differentiated formulations for AI/ML workloads, while regional suppliers in China (Shenzhen FRD, Suzhou Tianmai) are gaining share in consumer electronics segments. Emerging carbon-based TIM providers face challenges in achieving production-scale consistency, though graphene-enhanced solutions show promise for next-gen packaging architectures.

List of Key Semiconductor Thermal Interface Materials Companies Profiled

- DuPont

- Dow Inc.

- Henkel AG & Co. KGaA

- Shin-Etsu Chemical Co., Ltd.

- 3M Company

- Parker Hannifin Corporation

- Fujipoly America Corporation

- Wacker Chemie AG

- Indium Corporation

- Shenzhen FRD Technology Co., Ltd.

- Suzhou Tianmai Thermal Material

- Hongfucheng New Materials

- Beijing Zhongshi Technology

- Shenzhen Born Industrial

- Shenzhen Aochuan Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Thermal Grease and Paste dominates due to:

|

| By Application |

|

Data Center Servers show strongest adoption due to:

|

| By End User |

|

Cloud Service Providers drive premium demand because:

|

| By Material Composition |

|

Silicone-based remains dominant due to:

|

| By Application Method |

|

Dispensable Fluid leads in adoption because:

|

Regional Analysis: Semiconductor Thermal Interface Materials Market

The concentration of OSAT facilities in Malaysia and China creates localized demand hubs for thermal interface materials. Proximity to semiconductor packaging operations enables just-in-time delivery and customized formulation development for regional clients.

Asian research institutions are developing phase-change thermal interface materials optimized for high-power computing applications. Nanocomposite formulations with hybrid ceramic-metallic fillers show particular promise for next-gen chip architectures.

Local thermal material producers maintain tight collaboration with Asian foundries to anticipate cooling requirements for advanced nodes. This co-development approach reduces qualification cycles for new interface solutions.

National semiconductor self-sufficiency programs across the region include dedicated thermal management R&D clusters. Japan and South Korea prioritize thermal material innovation in their national semiconductor technology roadmaps.

North America

The North American semiconductor thermal interface materials market benefits from strong R&D capabilities in advanced cooling solutions, particularly for AI accelerators and HPC applications. U.S. material science companies lead in developing proprietary thermal gel formulations with superior thermal conductivity. The region’s focus on high-performance computing creates demand for specialized interface materials capable of handling extreme thermal loads. Domestic reshoring of semiconductor manufacturing is driving new thermal material qualification requirements as fab construction accelerates.

Europe

Europe’s semiconductor thermal interface materials market is characterized by stringent environmental regulations driving development of halogen-free and sustainable formulations. German automotive semiconductor demand fuels innovation in high-reliability thermal interface solutions for harsh operating conditions. The region maintains strong expertise in thermally conductive adhesives for power electronics applications, with growing R&D focus on graphene-based interface materials for next-generation devices.

South America

The South American market for semiconductor thermal interface materials remains nascent but shows growth potential in Brazil’s emerging electronics manufacturing sector. Thermal material adoption is primarily driven by consumer electronics assembly operations with basic thermal management needs. Limited local production creates reliance on imported interface solutions, though regional distributors are expanding technical support capabilities for thermal material applications.

Middle East & Africa

While still a minor market, the Middle East shows increasing interest in semiconductor thermal interface materials through strategic investments in electronics manufacturing infrastructure. Emerging data center construction projects in Gulf states create specialized demand for server-grade thermal solutions. South Africa’s automotive electronics sector represents the most established thermal interface materials market in Africa.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Thermal Interface Materials Market , covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as consumer electronics, data centers, telecommunications, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, application method, interface position, and end-use industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging materials (graphene, metal-based TIMs), integration with advanced packaging technologies, and evolving thermal management standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, material trade-offs, and qualification requirements.

- Stakeholder Insights: Insights for material suppliers, semiconductor manufacturers, OEMs, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Thermal Interface Materials Market?

-> Semiconductor Thermal Interface Materials Market size was valued at USD 1.17 billion in 2025. The market is projected to grow from USD 1.31 billion in 2026 to USD 2.42 billion by 2034, exhibiting a CAGR of 11.1% during the forecast period.

What is the expected growth rate?

-> The market is expected to grow at a CAGR of 11.1% from 2025 to 2034.

Which key companies operate in Semiconductor Thermal Interface Materials Market?

-> Key players include DuPont, Dow, Henkel, Shin-Etsu Chemical, 3M, Parker Hannifin, Fujipoly, Wacker Chemie, and Indium Corporation, among others.

What are the key growth drivers?

-> Key growth drivers include higher heat flux from advanced logic/AI workloads, compact consumer device designs, adoption of high-performance packaging, and increasing data center deployments.

Which region dominates the market?

-> Asia is the dominant market due to electronics manufacturing concentration, with growing demand from China, Japan, South Korea, and Southeast Asia.

What are the key product segments?

-> Major product types include thermal pads, thermal greases/pastes, phase change materials, metal-based TIMs, and carbon-based TIMs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...