Market Insights

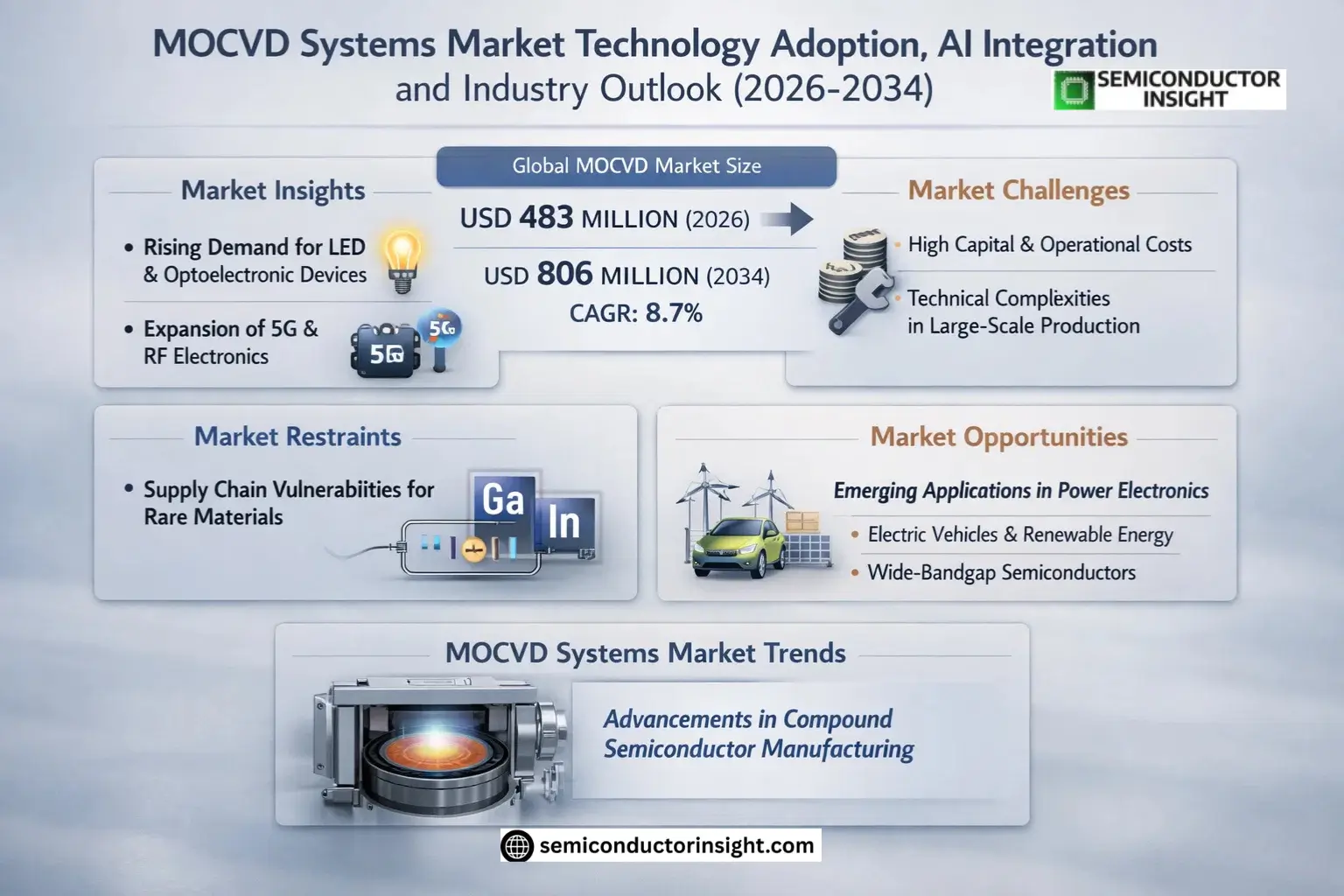

Global MOCVD Systems Market size was valued at USD 447 million in 2025. The market is projected to grow from USD 483 million in 2026 to USD 806 million by 2034, exhibiting a CAGR of 8.7% during the forecast period.

MOCVD (Metal-Organic Chemical Vapor Deposition) systems are critical tools in semiconductor manufacturing, enabling precise growth of compound semiconductor layers on substrates. These systems utilize metal-organic precursors and hydride gases to deposit high-quality thin films of materials such as gallium nitride (GaN), indium phosphide (InP), and gallium arsenide (GaAs). The technology plays a vital role in producing optoelectronic devices, including LEDs, laser diodes, and power electronics components.

The market growth is driven by increasing demand for energy-efficient lighting solutions, advancements in display technologies like Mini/Micro LED, and expanding applications in power electronics for electric vehicles and renewable energy systems. While the industry faces cyclical demand patterns tied to semiconductor capital expenditures, long-term prospects remain strong due to ongoing technological innovations and emerging applications in photonics and RF devices. Key players such as AIXTRON Technologies and Veeco Instruments continue to enhance system capabilities through improved throughput, larger wafer handling, and advanced process control features.

MARKET DRIVERS

Growing Demand for LED and Optoelectronic Devices

MOCVD Systems Market is primarily driven by the increasing adoption of LED lighting solutions worldwide. A significant shift from traditional lighting to energy-efficient LEDs, especially in automotive and general lighting applications, is boosting demand. The optoelectronics sector, including laser diodes and photodetectors, also heavily relies on MOCVD technology for semiconductor fabrication.

Expansion of 5G and RF Electronics

With the rapid deployment of 5G networks, the production of RF and power electronics using MOCVD systems has gained momentum. Gallium nitride (GaN) and silicon carbide (SiC) based devices manufactured via MOCVD are critical for high-frequency and high-power applications in telecommunications infrastructure.

Advancements in display technologies, particularly micro-LEDs for next-gen TVs and AR/VR devices, are creating additional growth opportunities for MOCVD equipment manufacturers.

MARKET CHALLENGES

High Capital and Operational Costs

MOCVD systems require substantial initial investments and maintenance, making adoption cost-prohibitive for small-scale semiconductor manufacturers. The complex process optimization and need for ultra-high purity precursors further increase operational expenses.

Other Challenges

Technical Complexities in Large-Scale Production

Achieving uniform deposition across large wafers remains a significant technical hurdle, particularly for emerging applications like power electronics and photovoltaics. Process control and yield optimization require continuous R&D investments.

MARKET RESTRAINTS

Supply Chain Vulnerabilities for Rare Materials

MOCVD Systems Market faces constraints due to geopolitical factors affecting the supply of critical raw materials such as gallium and indium. Price volatility of these rare metals directly impacts production costs and equipment pricing strategies.

MARKET OPPORTUNITIES

Emerging Applications in Power Electronics

The transition to electric vehicles and renewable energy systems is creating substantial opportunities for MOCVD systems in manufacturing wide-bandgap semiconductors. GaN and SiC power devices show 40% higher efficiency compared to traditional silicon-based components, driving market expansion.

MOCVD Systems Market Trends

Advancements in Compound Semiconductor Manufacturing

MOCVD Systems Market is experiencing significant growth driven by increasing demand for high-performance compound semiconductors. These systems enable precise deposition of materials like GaN and InP, which are critical for LED production, power electronics, and optoelectronic devices. Manufacturers are focusing on enhancing throughput and uniformity while reducing defects in epitaxial layers.

Other Trends

Mini/Micro LED Adoption Accelerates

The display industry’s shift toward Mini/Micro LED technology is creating substantial demand for advanced MOCVD Systems capable of handling smaller pixel pitches and higher pixel densities. This trend is particularly strong in consumer electronics for premium displays and automotive lighting applications.

Emerging Applications in Power Electronics

GaN-based power devices for electric vehicles and renewable energy systems are driving new requirements in MOCVD technology. Systems must now accommodate thicker epilayers and maintain precise doping control for high-voltage applications. The automotive sector’s electrification push is creating sustained demand for reliable power semiconductor manufacturing solutions.

Other Trends

Regional Manufacturing Hubs Expand

East Asia remains the dominant region for MOCVD System installations, with China accounting for significant LED production capacity. However, North America and Europe are showing increased activity in high-end laser diode and RF device manufacturing, creating regional specialization in system requirements and process technologies.

Process Monitoring and Automation Advancements

Leading MOCVD System manufacturers are incorporating real-time monitoring and closed-loop control systems to improve yield and consistency. The integration of AI-driven process optimization and multi-wafer handling capabilities is becoming standard for high-volume production environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced MOCVD Systems Shaping Semiconductor Manufacturing

MOCVD Systems Market is dominated by AIXTRON and Veeco Instruments, which collectively hold over 65% market share. These industry leaders maintain technological superiority through continuous R&D investments in multi-wafer reactors and automated process controls. The market exhibits high barriers to entry due to complex system integration requirements and long customer qualification cycles, resulting in an oligopolistic structure where top players enjoy strong pricing power and recurring revenue from service contracts.

Second-tier competitors like Advanced Micro-Fabrication Equipment and Topecsh have gained traction by specializing in niche applications such as GaN power devices and VCSEL production. Emerging Chinese manufacturers are increasing competition through government-backed initiatives, though they still lag in process expertise for high-end applications. The competitive landscape is further shaped by strategic collaborations between MOCVD suppliers and key semiconductor manufacturers to co-develop application-specific solutions.

List of Key MOCVD Systems Companies Profiled

- AIXTRON SE

- Veeco Instruments Inc.

- Advanced Micro-Fabrication Equipment Inc. (AMEC)

- Topecsh

- Taiyo Nippon Sanso Corporation

- NuFlare Technology Inc.

- DCA Instruments Oy

- ULVAC Technologies

- SVTA Technologies Inc.

- CVD Equipment Corporation

- ASM International NV

- Epigress AB

- JUSUNG Engineering Co., Ltd.

- Nanjing Advanced Semiconductor Technology

- Wafertrain

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

GaN-based MOCVD dominates due to extensive use in LED manufacturing and power electronics. Growth drivers include:

|

| By Application |

|

LED Applications represent the largest segment with critical factors including:

|

| By End User |

|

Semiconductor Manufacturers lead in adoption due to:

|

| By Substrate Size |

|

6 inch substrates show strongest growth potential due to:

|

| By Chamber Configuration |

|

Multi-chamber Systems are gaining prominence with key advantages:

|

Regional Analysis: MOCVD Systems Market

Asia-Pacific

Taiwan’s semiconductor ecosystem drives cutting-edge MOCVD adoption for 5G RF components and microLED displays, with TSMC and AU Optronics pioneering new deposition techniques.

China’s Yangtze River Delta hosts the world’s highest concentration of MOCVD systems, with specialized industrial parks supporting everything from R&D to mass production of gallium nitride devices.

South Korea’s semiconductor national project includes substantial subsidies for MOCVD equipment upgrades, particularly for power electronics and photonics applications in the Ulsan cluster.

Japanese manufacturers are adapting MOCVD systems for novel applications including UV-C disinfection devices and automotive LiDAR sensors, creating specialized market niches.

North America

The North American MOCVD Systems Market benefits from strong defense and aerospace sector demand for ruggedized compound semiconductors. Silicon Valley’s photonics startups are driving adoption of compact MOCVD systems for quantum computing and optical communications applications. Department of Defense funding for gallium nitride technology development ensures steady demand from research institutions and defense contractors. Canada’s emerging photonics corridor between Ottawa and Waterloo is establishing new MOCVD infrastructure for optoelectronic device development.

Europe

European MOCVD adoption focuses on specialized applications in automotive LiDAR and industrial sensors. Germany’s Fraunhofer Institutes lead in developing energy-efficient MOCVD processes, while the UK’s Compound Semiconductor Centre pioneers novel deposition techniques. The EU’s Chips Act includes provisions for compound semiconductor manufacturing, potentially boosting MOCVD system demand. Scandinavia shows increasing MOCVD adoption for power electronics in renewable energy systems.

Middle East & Africa

The Middle East is investing in MOCVD capabilities for next-generation photonics in telecommunications infrastructure. Israel’s robust semiconductor startup ecosystem drives demand for research-grade MOCVD systems. Saudi Arabia’s Vision 2030 includes compound semiconductor manufacturing goals, creating new opportunities for MOCVD vendors. South Africa maintains niche capabilities in specialized optoelectronic applications.

South America

Brazil dominates South America’s limited MOCVD landscape with government-funded research centers focusing on LED and sensor technologies. Argentina’s National Atomic Energy Commission operates specialized MOCVD systems for radiation-hardened semiconductor development. The region shows potential for growth in automotive and industrial semiconductor applications as supply chains diversify.

Report Scope

This market research report provides a comprehensive analysis of the MOCVD Systems Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

-> MOCVD Systems Market size was valued at USD 447 million in 2025. The market is projected to grow from USD 483 million in 2026 to USD 806 million by 2034, exhibiting a CAGR of 8.7% during the forecast period.

Which key companies operate in MOCVD Systems Market?

-> Key players include AIXTRON Technologies, Advanced Micro-Fabrication Equipment, Topecsh, Veeco Instruments, Taiyo Nippon Sanso, and NuFlare Technology.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy-efficient lighting, expansion of high-speed optical communication networks, and adoption of GaN power devices in automotive and renewable energy applications.

Which region dominates the market?

-> Asia-Pacific dominates the market with strong presence in LED, display, and power/RF value chains, while North America and Europe lead in high-end laser applications and R&D initiatives.

What are the emerging trends?

-> Emerging trends include transition to Mini/Micro LED technology, expansion of 3D sensing applications, and growing adoption of GaN power devices in fast charging and energy infrastructure.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...