Resistive RAM based non-volatile FPGA configuration chip Market Insights

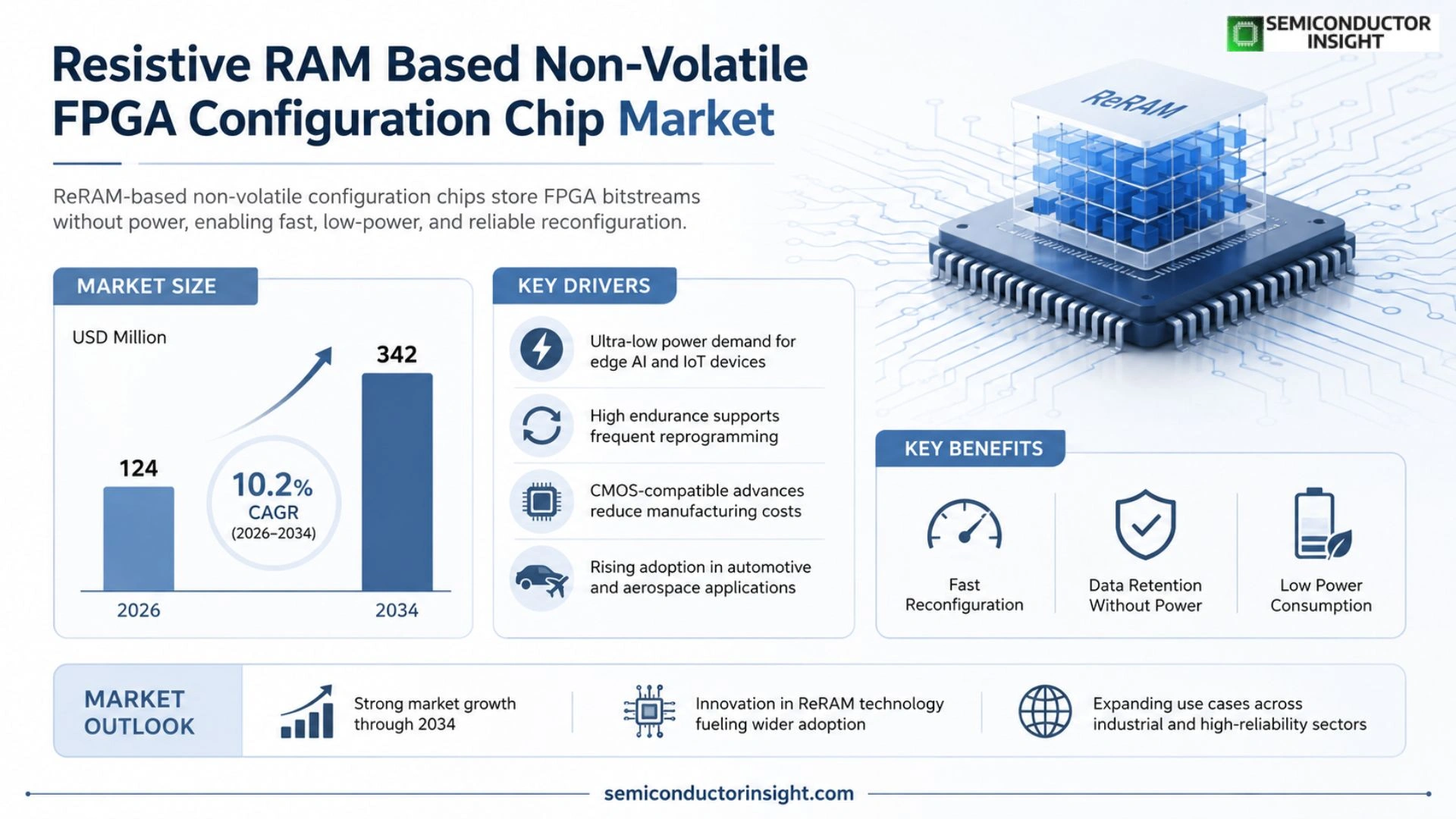

Global Resistive RAM based non-volatile FPGA configuration chip Market size was valued at USD 118 million in 2025. The market is projected to grow from USD 124 million in 2026 to USD 342 million by 2034, exhibiting a CAGR of 10.2% during the forecast period.

Resistive RAM (ReRAM) based non‑volatile FPGA configuration chips are specialized memory devices that retain the bitstream used to program field‑programmable gate arrays even when power is removed. By exploiting the fast switching speed and low energy consumption of ReRAM cells, these chips enable rapid reconfiguration while ensuring data integrity after power cycles.

The market is experiencing accelerated growth because semiconductor manufacturers are pursuing ultra‑low‑power solutions for edge AI and IoT workloads, and ReRAM’s high endurance supports frequent reprogramming cycles. Moreover, recent advances in CMOS‑compatible fabrication have lowered production costs, encouraging adoption across automotive and aerospace sectors. Key players such as Intel Corporation, AMD (Xilinx), Microchip Technology, and Rambus Inc. are expanding their portfolios through strategic partnerships and technology licensing agreements.

MARKET DRIVERS

Increasing Demand for Low‑Power Reconfigurable Logic

Resistive RAM based non-volatile FPGA configuration chip Market is being propelled by data‑center operators seeking ultra‑low power consumption while maintaining high performance. Recent product roadmaps show a shift toward in‑memory computing architectures that reduce data movement, directly benefiting resistive‑RAM‑enabled FPGAs.

Growth of 5G Infrastructure

Deployment of 5G base stations requires configurable hardware that can be updated remotely without power loss. Resistive RAM technology offers instant power‑on state retention, making it a preferred choice for edge‑compatible FPGA platforms.

➤ Industry analysts estimate a CAGR of 18% for the resistive‑RAM FPGA segment through 2032.

These drivers collectively create a fertile environment for vendors to invest in next‑generation non‑volatile configuration solutions, reinforcing the upward trajectory of the market.

MARKET CHALLENGES

Design Complexity and Integration Costs

Implementing resistive‑RAM cells within FPGA fabric demands precise process control and sophisticated design tools. The added verification steps increase time‑to‑market and elevate overall project expenditure.

Other Challenges

Supply Chain Constraints

Limited foundry capacity for emerging memory technologies can delay volume production, creating bottlenecks for early adopters of Resistive RAM based non-volatile FPGA configuration chip Market.

MARKET RESTRAINTS

Thermal Stability Limitations

Resistive RAM devices exhibit sensitivity to elevated temperatures, which can affect data retention and endurance. For high‑density FPGA configurations operating in harsh environments, this thermal constraint poses a significant design hurdle.

Furthermore, the need for specialized testing equipment to validate temperature‑dependent behavior adds cost, discouraging some manufacturers from fully embracing the technology.

MARKET OPPORTUNITIES

Emerging Edge‑AI Applications

Edge‑AI workloads require rapid reconfiguration and instant power‑up states, characteristics inherently offered by resistive‑RAM based non‑volatile FPGA configuration chips. The convergence of AI inference at the edge and low‑power constraints creates a sizable opportunity for market participants.

Strategic partnerships between memory fabs and FPGA designers are expected to accelerate product introductions, unlocking new revenue streams and expanding the addressable market for these advanced configuration solutions.

Resistive RAM based non-volatile FPGA configuration chip Market Trends

Growth Driven by Edge AI and Low‑Power Requirements

Resistive RAM based non-volatile FPGA configuration chip Market is witnessing a marked shift as semiconductor manufacturers prioritize ultra‑low‑power platforms for edge artificial‑intelligence and Internet‑of‑Things applications. ReRAM cells supply sub‑nanosecond switching and minimal static power, enabling FPGA devices to retain configuration data without auxiliary memory. This technical advantage shortens re‑programming cycles and reduces overall system energy consumption, making the technology attractive for battery‑constrained devices. Recent progress in CMOS‑compatible fabrication has also lowered production barriers, allowing broader adoption across automotive safety modules and aerospace control units. Industry observers note that the convergence of high endurance and energy efficiency is creating a sustainable demand curve that outpaces legacy flash‑based solutions.

Other Trends

Technology Integration and Cost Optimization

Manufacturers are integrating ReRAM‑based configuration chips directly into standard FPGA die stacks, a move that curtails board‑level component count and simplifies supply chains. The consolidation of the memory element with the processing fabric shortens signal paths, enhancing reliability while delivering modest cost savings. Concurrently, design houses are leveraging advanced packaging techniques such as fan‑out wafer level packaging to further compress form factor and improve thermal performance. These engineering choices reflect an industry‑wide effort to balance performance gains with the economic realities of high‑volume production.

Competitive Landscape and Strategic Partnerships

Key players, including Intel, AMD (Xilinx), Microchip Technology, and Rambus, are intensifying collaboration through licensing agreements and joint development programs. Such partnerships accelerate technology transfer, align product roadmaps, and expand ecosystem support for ReRAM‑enabled FPGA solutions. As the market matures, smaller innovators are also entering the space, focusing on niche applications that demand rapid reconfiguration and robust data retention. This evolving competitive environment is expected to foster continuous innovation, driving the segment forward while maintaining a focus on verified technical advantages.

COMPETITIVE LANDSCAPE

Key Industry Players

Resistive RAM based non‑volatile FPGA configuration chips: Market dynamics and competitive overview

Resistive RAM (ReRAM) based non‑volatile FPGA configuration chip market was valued at approximately USD 118 million in 2025 and is projected to expand to USD 342 million by 2034, driven by a 10.2% CAGR. Intel Corporation leads the segment by leveraging its own 3‑D‑Stacked ReRAM integration roadmap, while AMD (through Xilinx) capitalizes on its extensive FPGA portfolio to embed ReRAM cells for ultra‑low‑power edge AI applications. Microchip Technology strengthens its position by offering cost‑effective ReRAM configuration solutions for automotive safety modules, and Rambus Inc. differentiates with high‑end licensing of endurance‑optimized ReRAM IP. Collectively, these incumbents shape a market structure dominated by a few large semiconductor firms that combine in‑house fabrication with strategic technology partnerships, setting pricing benchmarks and driving adoption across aerospace, automotive, and industrial IoT domains.

Beyond the dominant quartet, a constellation of niche yet influential players contributes to the breadth of the ecosystem. Samsung Electronics and SK Hynix intensify competition through advanced CMOS‑compatible ReRAM process nodes, targeting high‑volume memory fabs. Micron Technology and Toshiba focus on hybrid memory modules that pair ReRAM with traditional flash to balance speed and endurance. GlobalFoundries offers foundry services for custom ReRAM FPGA chips, while NXP Semiconductors and Renesas Electronics explore automotive‑grade reliability with temperature‑robust ReRAM cells. Emerging innovators such as imec, InvenSense (now part of TDK), and Everspin Technologies supply specialized IP blocks and evaluation kits, enabling smaller design houses and startups to integrate ReRAM‑based configuration storage without massive capital investment.

List of Key Resistive RAM based non‑volatile FPGA configuration chip Companies Profiled

- Intel Corporation

- AMD (Xilinx)

- Microchip Technology

- Rambus Inc.

- Samsung Electronics

- SK Hynix

- Micron Technology

- Toshiba Corporation

- GlobalFoundries

- NXP Semiconductors

- Renesas Electronics

- imec

- InvenSense (TDK)

- Everspin Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Oxide‑based ReRAM is the leading type because it balances scalability with process compatibility.

|

| By Application |

|

Edge AI workloads dominate the application landscape, driven by the need for rapid on‑device inference.

|

| By End User |

|

Semiconductor manufacturers emerge as the primary end‑user, seeking to embed low‑power configuration memory.

|

| By Architecture |

|

Embedded configuration memory within the FPGA die is gaining traction for its integration benefits.

|

| By Market Drivers |

|

Low‑power demand is the dominant driver, shaping adoption across multiple verticals.

|

Regional Analysis: North America

The aerospace and defense industry in North America is undergoing a significant digital transformation, demanding more adaptable and secure FPGA solutions. Resistive RAM based non-volatile configuration chips play a crucial role in enabling rapid prototyping and in-field reconfiguration of critical systems. The need for robust and reliable hardware in these applications drives the adoption of these advanced memory technologies for enhanced operational capabilities.

The automotive sector is rapidly embracing connected and autonomous vehicle technologies, creating a surge in demand for high-performance and reliable FPGA solutions. Resistive RAM based non-volatile configuration chips are essential for enabling over-the-air updates, enhancing safety features, and accelerating the development of advanced driver-assistance systems (ADAS). The stringent requirements of automotive applications drive the need for robust and configurable memory solutions.

The telecommunications industry in North America is continuously evolving to meet the growing demand for high-bandwidth and low-latency networks. Resistive RAM based non-volatile FPGA configuration chips enable efficient infrastructure upgrades, facilitate network virtualization, and support the deployment of 5G and future wireless technologies. The need for flexible and adaptable solutions is paramount in this dynamic sector.

North America’s robust industrial sector leverages FPGA technology for advanced control systems, robotics, and data acquisition. Resistive RAM based non-volatile configuration chips enhance the flexibility and adaptability of these systems, enabling rapid prototyping, efficient system updates, and improved operational efficiency. The growing emphasis on Industry 4.0 initiatives fuels the demand for these advanced memory solutions.

Europe

Europe presents a steady and growing market for Resistive RAM based non-volatile FPGA configuration chips. The region’s strong emphasis on innovation and its established electronics manufacturing base contribute to consistent demand. Key applications include automotive, industrial automation, and aerospace & defense. European manufacturers are increasingly adopting these chips for their ability to enhance FPGA system flexibility and accelerate product development cycles. The focus on energy efficiency and security further drives technological advancements within this market.

Asia-Pacific

Asia-Pacific is poised to be the fastest-growing market for Resistive RAM based non-volatile FPGA configuration chips. The region’s burgeoning electronics industry, particularly in China and India, coupled with increasing investments in R&D, are driving significant demand. Key growth drivers include the expansion of the automotive sector, the increasing adoption of 5G technologies, and the growth of industrial automation. The region’s cost-competitive manufacturing environment further enhances its attractiveness for FPGA-based solutions.

South America

South America represents a smaller but emerging market for Resistive RAM based non-volatile FPGA configuration chips. The region’s growing industrial sector, particularly in Brazil and Argentina, is driving increasing demand for FPGA-based solutions. Key applications include telecommunications, industrial automation, and defense. While the market is relatively nascent, the increasing adoption of advanced technologies is expected to fuel future growth.

Middle East & Africa

The Middle East & Africa market for Resistive RAM based non-volatile FPGA configuration chips is characterized by moderate growth potential. The region’s increasing investments in infrastructure development, telecommunications, and defense are creating opportunities for FPGA-based solutions. The growing adoption of smart city initiatives and the expansion of the industrial sector are expected to contribute to future market expansion.

Report Scope

This market research report provides a comprehensive analysis of the Resistive RAM based non-volatile FPGA configuration chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Resistive RAM based non-volatile FPGA configuration chip Market?

-> Resistive RAM based non-volatile FPGA configuration chip Market is projected to grow from USD 124 million in 2026 to USD 342 million by 2034.

Which key companies operate in Resistive RAM based non-volatile FPGA configuration chip Market?

-> Key players include Intel Corporation, AMD (Xilinx), Microchip Technology, and Rambus Inc.

What are the key growth drivers?

-> Key growth drivers include demand for ultra‑low‑power solutions in edge AI and IoT, high endurance of ReRAM enabling frequent reprogramming, cost reductions from CMOS‑compatible fabrication, and increasing adoption in automotive and aerospace applications.

Which region dominates the market?

-> North America currently holds the largest market share, while Asia‑Pacific is the fastest‑growing region.

What are the emerging trends?

-> Emerging trends include integration of ReRAM with edge AI and IoT devices, 3D‑stacked architectures, and the development of CMOS‑compatible manufacturing processes that lower cost and improve scalability.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...