MARKET INSIGHTS

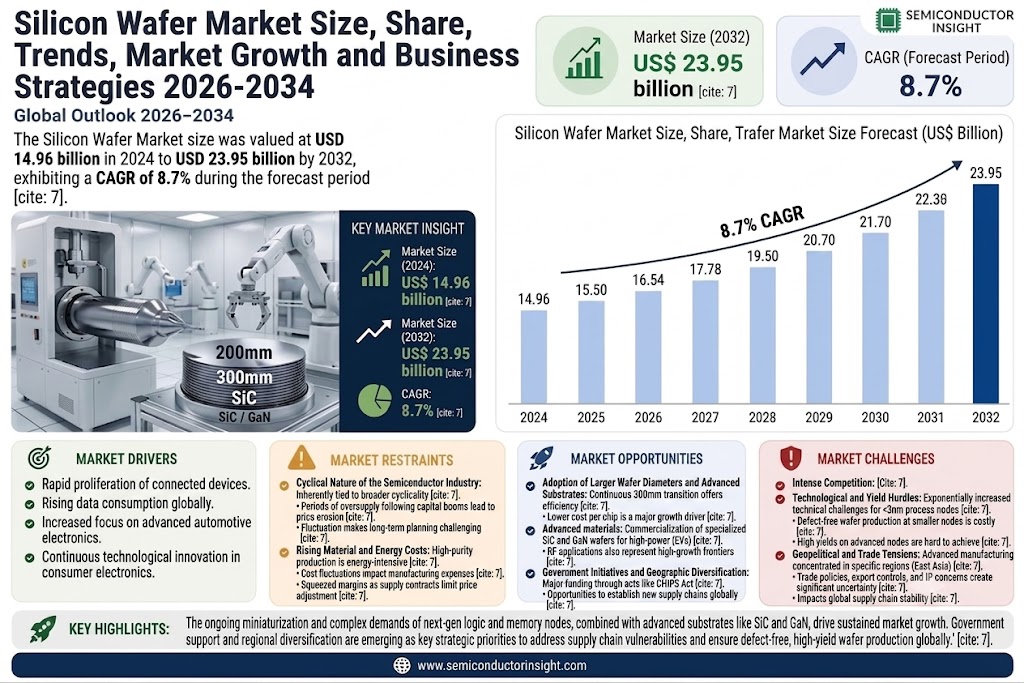

Global Silicon Wafer Market size was valued at USD 14.96 billion in 2024 to USD 23.95 billion by 2032, exhibiting a CAGR of 8.7% during the forecast period.

Silicon wafers are thin slices of semiconductor-grade crystalline silicon that serve as the foundational substrate for integrated circuits (ICs). These wafers are manufactured through a complex process involving crystal growth, slicing, lapping, etching, and polishing to achieve specific electrical properties and a pristine, defect-free surface. They are the essential base material upon which nearly all modern electronics are built, powering everything from everyday devices like smartphones and automobiles to advanced applications in artificial intelligence (AI) and the Internet of Things (IoT).

The market is experiencing robust growth driven by several key factors, including the pervasive digital transformation across industries and escalating demand for consumer electronics. Furthermore, the rapid expansion of data centers and high-performance computing is contributing significantly to market expansion. Strategic initiatives by key players are also expected to fuel market growth; for instance, in March 2024, GlobalWafers announced plans for a significant capacity expansion for 300mm wafers to meet soaring demand. Shin-Etsu Chemical, SUMCO, Siltronic AG, and SK Siltron are some of the key players that operate in the market with a wide range of portfolios.

MARKET DRIVERS

Proliferation of Electronics and Connected Devices

The relentless global demand for consumer electronics, including smartphones, laptops, and tablets, is a primary driver for the Silicon Wafer Market. The rapid adoption of IoT devices, smart home systems, and 5G infrastructure is further increasing the need for semiconductor chips, which are fabricated on silicon wafers. This demand is underpinned by technological advancements that require more powerful and efficient chips, pushing the market for larger diameter wafers like 300mm to achieve greater economies of scale.

Advancements in Automotive and Industrial Sectors

The automotive industry’s transformation towards electric vehicles (EVs), advanced driver-assistance systems (ADAS), and vehicle connectivity is creating substantial demand for semiconductors. Modern vehicles can contain over 3,000 chips, requiring a steady supply of high-quality silicon wafers. Similarly, industrial automation and the growth of Industry 4.0 are driving demand for sensors, power management ICs, and microcontrollers, all of which depend on the foundational silicon wafer.

➤ Global Silicon Wafer Market is projected to grow significantly, with shipments for 300mm wafers expected to continue their strong upward trajectory to meet the needs of high-performance computing and memory applications.

Furthermore, the expansion of data centers to support cloud computing, artificial intelligence, and big data analytics necessitates a continuous supply of advanced logic and memory chips. The AI boom, in particular, is driving innovation in chip design and manufacturing processes, solidifying the silicon wafer’s role as a critical enabling material for the digital economy.

MARKET CHALLENGES

High Capital Intensity and Supply Chain Complexity

silicon wafer manufacturing process is extremely capital-intensive. Constructing and maintaining state-of-the-art fabrication plants (fabs) requires multi-billion-dollar investments. Furthermore, the supply chain for high-purity polysilicon and the specialized equipment needed for wafer production is complex and geographically concentrated, making it vulnerable to disruptions, as witnessed during recent global events.

Other Challenges

Technological and Yield Hurdles

As chip manufacturers push towards smaller process nodes (e.g., 3nm, 2nm), the technical challenges in producing defect-free wafers increase exponentially. Achieving high yields on these advanced nodes is difficult and costly, impacting overall profitability and the ability to scale production efficiently.

Geopolitical and Trade Tensions

The concentration of advanced semiconductor manufacturing capacity in specific regions, notably East Asia, creates geopolitical risks. Trade policies, export controls, and intellectual property concerns can create significant uncertainty and barriers for the global silicon wafer supply chain, affecting market stability.

MARKET RESTRAINTS

Cyclical Nature of the Semiconductor Industry

Silicon Wafer Market is inherently tied to the cyclicality of the broader semiconductor industry. Periods of oversupply, often following massive capital investment booms, can lead to price erosion and reduced profitability for wafer manufacturers. This cyclicality makes long-term planning and investment challenging, as demand can fluctuate significantly based on global economic conditions and end-market inventory corrections.

Rising Material and Energy Costs

The production of high-purity silicon wafers is energy-intensive and requires significant amounts of raw materials. Fluctuations in the cost of energy, electricity, and precursor chemicals directly impact manufacturing costs. In an inflationary environment, these rising input costs can squeeze margins, especially when long-term supply contracts limit the ability to quickly adjust wafer prices.

MARKET OPPORTUNITIES

Adoption of Larger Wafer Diameters and Advanced Substrates

The ongoing transition to 300mm wafers remains a significant opportunity for market growth, as they offer superior production efficiency and lower cost per chip. Beyond this, the development and commercialization of advanced substrate materials, such as Silicon Carbide (SiC) and Gallium Nitride (GaN) wafers for high-power and high-frequency applications (e.g., EVs, RF devices), represent a high-growth frontier for specialized wafer manufacturers.

Government Initiatives and Geographic Diversification

Major government initiatives, like the CHIPS Act in the United States and similar policies in Europe and Asia, are allocating substantial funding to bolster domestic semiconductor manufacturing capabilities. This creates significant opportunities for wafer suppliers to establish new partnerships and supply chains in these regions, reducing geographic concentration risks and tapping into new sources of demand.

Silicon Wafer Market Trends

Robust Growth Fueled by Semiconductor Demand

Global Silicon Wafer Market continues to exhibit strong growth, with its value projected to surge from approximately USD 14.96 billion in 2024 to about USD 23.95 billion by 2032, representing a compound annual growth rate (CAGR) of 8.7%. This expansion is primarily driven by the pervasive and growing demand for semiconductors, which are fundamental components in a vast array of modern technologies. As the essential substrate material for integrated circuits, silicon wafers are found in everything from everyday devices like smartphones, home appliances, and automobiles to advanced applications in artificial intelligence (AI), the Internet of Things (IoT), and high-performance computing.

Other Trends

Market Concentration and Dominance of 300mm Wafers

The market is characterized by a high degree of concentration, with the top five global manufacturers including Shin-Etsu Chemical, SUMCO, and GlobalWafers accounting for approximately 82% of the revenue as of 2023. In terms of product segments, 300mm (12-inch) wafers dominate the landscape, holding a commanding share of about 75% of the market by value. This segment is critical for manufacturing high-performance chips, predominantly used in the Memory and Logic/MPU application sectors. Conversely, 200mm (8-inch) and smaller diameter wafers are primarily utilized for applications like Analog circuits and Discrete Devices & Sensors.

Shifting Geographical Dynamics

Regional market dynamics are also a key trend. Japan is currently the largest market for silicon wafers, holding a significant 43% share, followed by China at 20%. However, the center of gravity is expected to shift. China is projected to play an increasingly important role in the global semiconductor industry over the next five years. The market is witnessing the entry of new domestic players such as Sichuan Vastity Semiconductor and Anhui Yisemi Semiconductor, indicating a strategic push for greater self-sufficiency and supply chain resilience within the country. From an application perspective, the Memory segment is the largest, accounting for nearly half of the total Silicon Wafer Market, underscoring the immense demand for data storage and processing capabilities.

COMPETITIVE LANDSCAPE

Key Industry Players

A Concentrated Market with Global and Regional Leaders

Global Silicon Wafer Market is characterized by a high degree of concentration, with the top five vendors Shin-Etsu Chemical, SUMCO, GlobalWafers, Siltronic AG, and SK Siltron accounting for approximately 82% of the market revenue in 2023. This oligopolistic structure is driven by the significant capital expenditure, technological expertise, and stringent quality control requirements for manufacturing advanced wafers, particularly the dominant 300mm (12-inch) wafers that constitute about 75% of the market. Shin-Etsu Chemical and SUMCO, both headquartered in Japan the world’s largest Silicon Wafer Market are the undisputed leaders, leveraging decades of experience and continuous R&D investment to serve major global semiconductor foundries and integrated device manufacturers. GlobalWafers’ acquisition of Siltronic AG (subject to regulatory approvals) is a pivotal development poised to further consolidate the market’s top tier.

Beyond the dominant global players, a number of significant companies operate in specialized or regional niches. Companies like Taiwan’s Wafer Works Corporation and China’s National Silicon Industry Group (NSIG) are key regional suppliers, supported by government initiatives to bolster domestic semiconductor supply chains. Niche players such as France’s Soitec, specializing in engineered substrates like Silicon-on-Insulator (SOI) wafers, and FST Corporation, cater to specific high-performance application segments. The Chinese market, which holds about 20% global share, features a growing list of participants including Zhonghuan Advanced Semiconductor Materials, Zhejiang Jinruihong Technologies, and Hangzhou Semiconductor Wafer, with potential new entrants like Sichuan Vastity Semiconductor and Anhui Yisemi Semiconductor aiming to capture a share of the expanding domestic demand.

List of Key Silicon Wafer Companies Profiled

- Shin-Etsu Chemical

- SUMCO

- GlobalWafers

- Siltronic AG

- SK Siltron

- FST Corporation

- Wafer Works Corporation

- Soitec

- National Silicon Industry Group (NSIG)

- Zhonghuan Advanced Semiconductor Materials

- Zhejiang Jinruihong Technologies

- Hangzhou Semiconductor Wafer (CCMC)

- GRINM Semiconductor Materials

- Shanghai Advanced Silicon Technology (AST)

- Beijing ESWIN Technology Group

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

300mm Wafers have established a dominant position as the industry standard for high-volume, advanced semiconductor manufacturing. This leading segment is heavily favored for its superior cost-efficiency per chip and its critical role in producing complex devices like advanced logic processors and high-density memory chips. The production infrastructure is mature and heavily invested globally, creating a high barrier to entry and solidifying the dominance of established manufacturers. The technological roadmap for smaller process nodes is almost exclusively tied to 300mm wafer technology, ensuring its continued leadership for the foreseeable future, particularly for cutting-edge applications in artificial intelligence and high-performance computing. |

| By Application |

|

Memory stands out as the leading application segment, driven by the relentless global demand for data storage and processing power. The proliferation of cloud computing, big data analytics, and sophisticated consumer electronics has created an insatiable need for DRAM and NAND flash memory. This segment’s dominance is closely linked to the 300mm wafer segment, as memory production is highly optimized for large-diameter wafers to achieve the economies of scale required for cost-competitive manufacturing. The continuous innovation in memory technology, pushing towards higher densities and faster speeds, further cements its position at the forefront of silicon wafer consumption, underpinning the entire digital economy. |

| By End User |

|

Consumer Electronics remains the leading end-user segment, functioning as the primary driver of silicon wafer demand. This sector encompasses a vast array of ubiquitous devices such as smartphones, tablets, laptops, and home appliances, each containing multiple semiconductor chips. The constant cycle of product innovation, feature enhancement, and consumer replacement cycles ensures a steady and substantial demand for wafers. Furthermore, the integration of advanced technologies like AI assistants, high-resolution displays, and 5G connectivity into consumer devices continuously increases the semiconductor content per device, reinforcing the segment’s leadership and creating a dynamic and demanding market for wafer suppliers. |

| By Wafer Processing Stage |

|

Polished Wafers represent the leading and most fundamental segment in terms of processing stage. These wafers serve as the essential starting substrate for the vast majority of semiconductor device fabrication processes. The demand for polished wafers is broad-based and directly correlates with overall semiconductor production volumes across all application segments. While epitaxial, annealed, and Silicon-on-Insulator (SOI) wafers cater to specialized, high-performance applications requiring specific electrical properties, the sheer volume of standard integrated circuits manufactured on polished wafers secures their dominant market share. This segment’s stability is a bellwether for the health of the entire semiconductor industry. |

| By Manufacturing Footprint |

|

Foundries have emerged as the leading customer segment based on manufacturing footprint, a reflection of the prevailing fabless-foundry business model in the modern semiconductor industry. Major foundries are the primary volume buyers of silicon wafers, as they manufacture chips on behalf of countless fabless design companies. This centralizes demand and gives foundries significant purchasing power. The growth of this segment is fueled by the trend of companies focusing on chip design while outsourcing capital-intensive manufacturing. The technological race among leading foundries to achieve smaller process nodes directly drives the demand for high-quality, advanced specification wafers, particularly 300mm polished wafers, solidifying their leading position. |

Regional Analysis: Silicon Wafer Market

Asia-Pacific

The region’s market is defined by the overwhelming presence of the world’s leading pure-play foundries and integrated device manufacturers. This concentration drives demand for a vast and varied portfolio of wafers, from large-diameter 300mm wafers for leading-edge logic and memory to specialized substrates for power devices and sensors. The intense competition and high capital expenditure within these companies create a consistent pull for high-purity, defect-free silicon wafers.

Strategic national policies, particularly in China, South Korea, and Japan, heavily influence the market. Governments are providing substantial subsidies, tax incentives, and setting up national semiconductor investment funds to bolster domestic production capacity and reduce reliance on foreign technology. This state-backed drive is accelerating the construction of new fabs, which in turn generates long-term, stable demand for silicon wafer suppliers and strengthens the entire regional supply chain.

A key advantage is the deeply entrenched and highly efficient local supply chain. Proximity to wafer polishing, recycling, and reclaim facilities, as well as chemical and gas suppliers, minimizes logistical costs and lead times for semiconductor fabs. This integrated ecosystem allows for rapid response to demand fluctuations and fosters close collaboration between wafer producers and their customers on technical specifications and quality control.

There is a relentless focus on research and development aimed at pushing the boundaries of Moore’s Law. This drives demand for advanced wafer types, including epitaxial wafers for high-performance computing and RF applications, and silicon-on-insulator wafers for low-power chips. Collaborative R&D efforts between academia, research institutes, and industry players ensure the region remains at the cutting edge of wafer technology and materials science.

North America

North America, primarily the United States, remains a critical and technologically advanced region in the Silicon Wafer Market, characterized by its strong base of fabless semiconductor companies, integrated device manufacturers like Intel, and major technology firms. The market is heavily influenced by demand from the high-performance computing, automotive, and aerospace and defense sectors, which require highly specialized and reliable wafers. Recent policy shifts, such as the CHIPS and Science Act, are catalyzing significant investments in domestic manufacturing capacity, aiming to reduce dependency on Asian supply chains. This is expected to stimulate demand for silicon wafers from new and expanded fabrication facilities. The region also boasts leading R&D capabilities, with a focus on developing advanced packaging technologies and novel semiconductor materials that often utilize specialized silicon substrates. While its production volume is smaller than Asia-Pacific’s, North America’s focus on innovation, strategic reshoring initiatives, and strength in design-intensive segments ensure its continued importance in the global silicon wafer landscape.

Europe

Europe holds a distinct and stable position in the Silicon Wafer Market, with a focus on specialization rather than volume. The region is a leader in several niche segments, particularly power electronics, automotive semiconductors, and micro-electromechanical systems (MEMS), which drives demand for specialized wafers like those for silicon carbide (SiC) and silicon-on-insulator (SOI). Key players, including STMicroelectronics and Infineon, have strong manufacturing bases supported by initiatives like the European Chips Act, which aims to bolster the continent’s semiconductor ecosystem. The market is characterized by high-quality manufacturing standards and a strong emphasis on research institutions and collaborative projects. Demand is steady, fueled by the robust automotive industry’s transition to electric vehicles and the industrial automation sector. While Europe may not compete with Asia on scale for mainstream logic wafers, its technological leadership in specific high-value applications ensures a resilient and strategically important demand base for specialized silicon wafers.

South America

The Silicon Wafer Market in South America is relatively nascent and fragmented compared to other major regions. The demand is primarily driven by the consumption of electronic devices and industrial equipment, with local semiconductor fabrication being extremely limited. Consequently, the market is largely import-dependent, with wafers sourced from North America, Europe, and Asia-Pacific to supply assembly and packaging operations, as well as for R&D purposes in academic and limited industrial settings. Brazil is the most significant market in the region, but overall growth is constrained by economic volatility, limited high-tech infrastructure, and a lack of large-scale government initiatives comparable to those in other regions. The market potential lies in serving the growing consumer electronics sector and localized manufacturing for specific industrial applications, but it remains a minor player in the global production and consumption landscape for silicon wafers.

Middle East & Africa

The Middle East & Africa region represents an emerging and opportunistic market for silicon wafers, though it currently holds a very small share of global activity. Demand is almost entirely met through imports, supporting various electronics manufacturing, telecommunications, and energy sectors. A few countries, notably in the Gulf Cooperation Council (GCC), are making strategic investments to diversify their economies beyond oil and gas, which includes developing technology hubs and supporting local electronics production. These initiatives could gradually create a foundation for future growth in semiconductor-related industries. However, the region faces significant challenges, including a underdeveloped local supply chain, limited technical expertise, and a focus on downstream assembly rather than upstream wafer production. For the foreseeable future, the Middle East & Africa will remain a consumption-focused market with growth tied to economic diversification plans and foreign direct investment in technology infrastructure.

Report Scope

This market research report provides a comprehensive analysis of the Silicon Wafer Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Silicon Wafer Market?

-> Global Silicon Wafer Market was valued at USD 14960 million in 2024 and is projected to reach USD 23950 million by 2032, at a CAGR of 8.7% during the forecast period.

Which key companies operate in Silicon Wafer Market?

-> Key players include Shin-Etsu Chemical, SUMCO, GlobalWafers, SK Siltron, Siltronic AG, FST Corporation, National Silicon Industry Group (NSIG), Zhonghuan Advanced Semiconductor Materials, Wafer Works Corporation, Zhejiang Jinruihong Technologies, and Hangzhou Semiconductor Wafer (CCMC), among others. In 2023, the world’s top five vendors accounted for approximately 82 % of the revenue.

What are the key growth drivers?

-> Key growth drivers include the critical role of silicon wafers as the base material for integrated circuits, powering everything from consumer electronics and automotive applications to cutting-edge fields like AI and IoT.

Which region dominates the market?

-> Japan is the largest wafer market with about 43% of the market, followed by China with 20%.

What are the emerging trends?

-> Emerging trends include the dominance of 300mm wafers, which hold about a 75% market share, and the increasing importance of China in the semiconductor market, with new entrants such as Sichuan Vastity Semiconductor and Anhui Yisemi Semiconductor.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...

Be the first to review “Silicon Wafer Market Size, Share, Trends, Market Growth and Business Strategies 2026-2034”