MARKET INSIGHTS

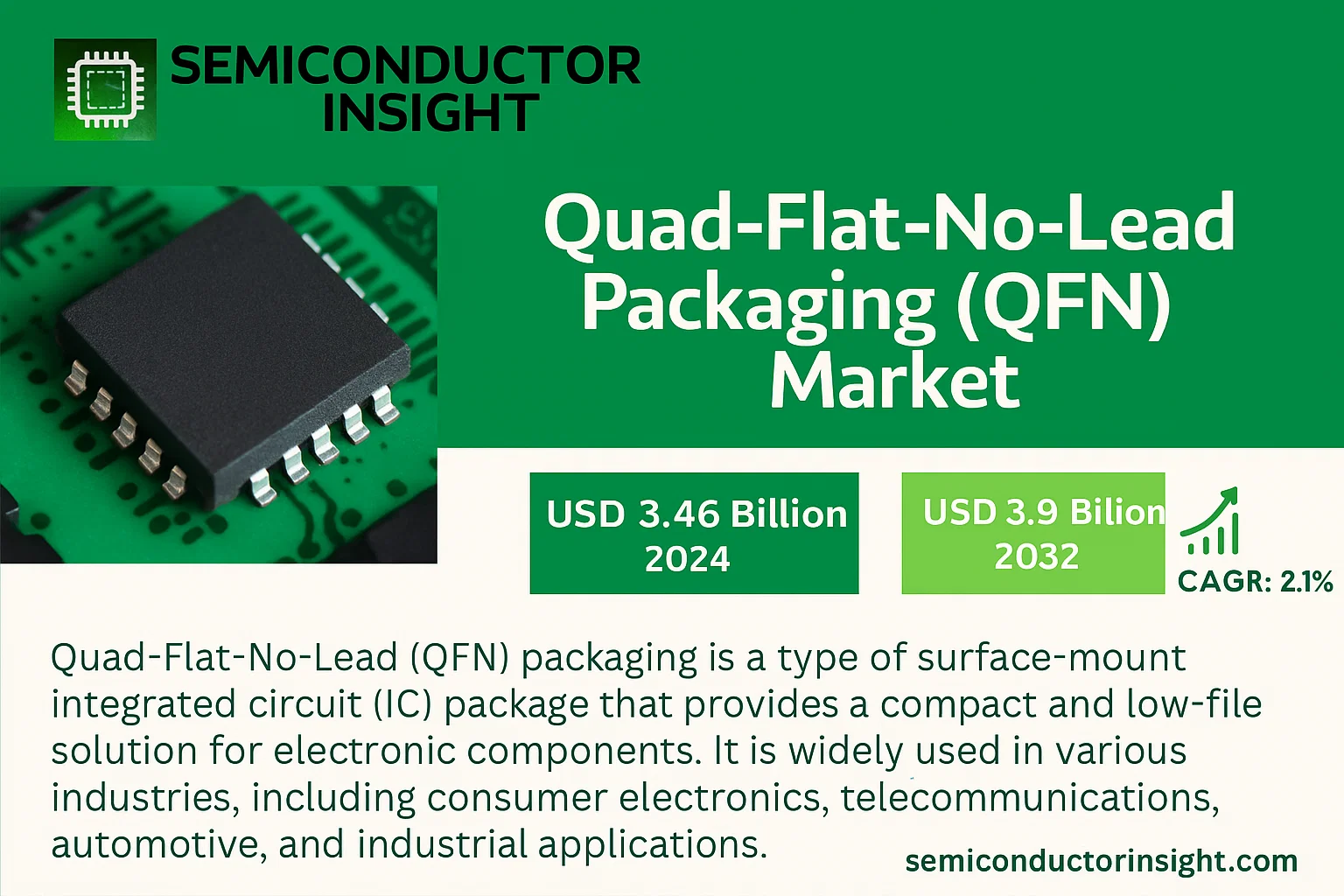

Global Quad-Flat-No-Lead Packaging (QFN) Market was valued at USD 3.46 billion in 2024 and is projected to reach USD 3.99 billion by 2032, exhibiting a CAGR of 2.1% during the forecast period.

Quad-Flat-No-Lead (QFN) packaging is a type of surface-mount integrated circuit (IC) package that provides a compact and low-profile solution for electronic components. It is widely used in various industries, including consumer electronics, telecommunications, automotive, and industrial applications.

QFN packages are designed to have no leads protruding from the sides. Instead, the electrical connections are made through metal pads on the bottom surface of the package. This design allows for a smaller package size and improved thermal and electrical performance compared to traditional leaded packages.

The QFN packaging has gained popularity in the electronics industry due to its compact size, good thermal performance, and reliability. It enables the development of smaller and more powerful electronic devices while optimizing space utilization on printed circuit boards (PCBs).

MARKET DRIVERS

Demand for Miniaturization in Electronics

The relentless push towards smaller, thinner, and more powerful electronic devices is a primary driver for the QFN market. The QFN package’s compact footprint, low profile, and excellent thermal and electrical performance make it an ideal choice for space-constrained applications like smartphones, wearables, and Internet of Things (IoT) sensors. This demand is propelling adoption across consumer electronics, automotive electronics, and telecommunications infrastructure.

Cost-Effectiveness and Performance Advantages

QFN packages offer a significant cost advantage over more complex packages like Ball Grid Arrays (BGAs) while providing superior heat dissipation through an exposed thermal pad. This combination of low cost and high performance is critical for high-volume manufacturing. The leadframe-based construction is less expensive than substrate-based packages, making QFN the preferred solution for cost-sensitive, high-performance integrated circuits such as power management ICs and RF amplifiers.

➤ The global automotive semiconductor market’s expansion, requiring robust and reliable packaging, is a significant tailwind for QFN adoption in applications like ADAS and infotainment systems.

Furthermore, the growth in 5G infrastructure and the proliferation of advanced driver-assistance systems (ADAS) require packages that can handle high-frequency signals and manage heat efficiently, further solidifying QFN’s market position.

MARKET CHALLENGES

Technical and Manufacturing Hurdles

Despite its advantages, the QFN package presents several manufacturing challenges. Achieving consistent and reliable solder joint formation during board assembly can be difficult due to the package’s leadless design, which is susceptible to issues like solder voiding and non-wetting. Inspection of these hidden solder joints requires advanced and costly X-ray systems, adding complexity to the production line.

Other Challenges

Handling and Warpage

The thin nature of QFN packages makes them susceptible to warpage during the high temperatures of the reflow soldering process. This can lead to poor coplanarity and defective connections. Additionally, their small size makes manual handling difficult, necessitating automated equipment throughout the supply chain.

Competition from Advanced Packages

QFN faces increasing competition from fan-out wafer-level packaging (FO-WLP) and other advanced packaging technologies that offer even higher I/O density and performance for the most cutting-edge applications, potentially limiting QFN’s market share in high-end segments.

MARKET RESTRAINTS

Limitations in High Pin-Count Applications

A key restraint for the QFN market is its inherent limitation regarding a very high number of I/O connections. While excellent for low to medium pin-count devices, the perimeter-only lead arrangement becomes impractical for complex systems-on-chips (SoCs) that require hundreds or thousands of interconnections. For these applications, array-based packages like BGAs or fan-out packages are necessary, constraining QFN’s addressable market.

Supply Chain and Material Cost Volatility

The semiconductor packaging industry is susceptible to fluctuations in the prices and availability of raw materials, particularly copper for leadframes and molding compounds. Geopolitical tensions and trade policies can disrupt this fragile supply chain, leading to increased costs and production delays for QFN packages, thereby acting as a market restraint.

MARKET OPPORTUNITIES

Expansion in Automotive and Industrial Electronics

The ongoing transformation in the automotive industry towards electrification and autonomy presents a substantial growth opportunity for QFN packages. Their reliability, thermal performance, and cost-effectiveness are well-suited for a wide range of automotive electronics, from engine control units to LiDAR sensors. Similarly, the growth of industrial automation and control systems relies on robust IC packaging, creating a stable demand driver.

Innovations in Package Variants

Continuous innovation in QFN design unlocks new opportunities. The development of dual-row and multi-row QFN packages increases the available I/O count within the same footprint, expanding their applicability. Furthermore, the emergence of thermally enhanced versions and packages with integrated passive devices (IPDs) allows QFN to compete in more performance-oriented markets, driving future growth.

Quad-Flat-No-Lead Packaging (QFN) Market Trends

Steady Market Expansion and Regional Concentration

The global Quad-Flat-No-Lead Packaging (QFN) market is on a trajectory of steady growth, demonstrating its entrenched role in modern electronics. The market was valued at $3.464 billion in 2024 and is projected to reach $3.987 billion by 2032, expanding at a Compound Annual Growth Rate (CAGR) of 2.1%. This growth is underpinned by the relentless demand for smaller, more powerful, and thermally efficient electronic devices across multiple industries. A key trend is the extreme concentration of the market, both geographically and among manufacturers. Asia-Pacific dominates the landscape, accounting for approximately 77% of the global market, followed by Europe and North America. This concentration is mirrored in the competitive landscape, where the top five players—including ASE(SPIL), Amkor Technology, and JCET Group—collectively hold about a 70% market share, creating a high-barrier, consolidated environment.

Other Trends

Product and Application Segmentation Trends

Within the QFN market, distinct trends are visible across product types and applications. The ‘Sawn Type’ QFN packaging leads the product segment with a dominant share of over 63%, favored for its precise manufacturing capabilities. In terms of package size, the ‘Above 5×5 to 7×7’ segment is the largest, capturing over 28% of the market, indicating a strong demand for packages that balance a compact footprint with sufficient space for higher pin counts and thermal dissipation. The application landscape is diversified, with consumer electronics, automotive, communications, and industrial sectors being the primary drivers. The push for miniaturization and enhanced performance in smartphones, automotive infotainment systems, and communication infrastructure continues to fuel adoption across these key segments.

Technological Drivers and Industry Demands

The fundamental design advantages of QFN packaging are central to its market trends. The leadless design, which uses metal pads on the package bottom for electrical connections, provides a smaller form factor and superior thermal and electrical performance compared to traditional leaded packages like QFP. This makes QFN an ideal solution for space-constrained printed circuit board (PCB) designs. The industry-wide demand for optimizing space utilization while managing heat in increasingly powerful integrated circuits is a powerful, sustained driver. As manufacturers continue to innovate within the QFN format to support new generations of semiconductors, the packaging technology remains a critical enabler for the broader electronics industry’s evolution.

COMPETITIVE LANDSCAPE

Key Industry Players

A Concentrated Market with Strong Asia-Pacific Dominance

The global QFN packaging market is characterized by a high level of concentration, with the top five players collectively accounting for approximately 70% of the market share. ASE (SPIL) stands as the leading force in this landscape, followed closely by other global giants like Amkor Technology and JCET Group. These major players possess extensive manufacturing capabilities, advanced technological expertise, and a broad global customer base spanning critical sectors such as automotive, consumer electronics, and communications. This high concentration indicates significant barriers to entry, with economies of scale, technological investments, and established supply chains being critical factors for maintaining a competitive edge.

Beyond the dominant leaders, the market includes several other significant players who maintain strong regional presences or specialize in particular segments. Companies such as Powertech Technology Inc. and Tongfu Microelectronics hold substantial market positions. Niche specialists and regional suppliers like UTAC, ChipMOS, and Tianshui Huatian Technology also contribute to the competitive dynamics, often focusing on specific package sizes (such as the popular ‘Above 5×5 to 7×7’ segment) or serving distinct geographic markets. The Asia-Pacific region is the undisputed hub for QFN manufacturing and consumption, accounting for approximately 77% of the global market, which influences the strategic focus and operational footprints of all key competitors.

List of Key Quad-Flat-No-Lead Packaging (QFN) Companies Profiled

- ASE (SPIL)

- Amkor Technology

- JCET Group

- Powertech Technology Inc. (PTI)

- Tongfu Microelectronics

- Tianshui Huatian Technology

- UTAC

- Orient Semiconductor Electronics (OSE)

- ChipMOS TECHNOLOGIES INC.

- King Yuan Electronics Corp. (KYEC)

- SFA Semicon

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Sawn Type represents the dominant segment, favored for its superior cost-effectiveness and high-volume production efficiency. This manufacturing process provides excellent package integrity and reliable performance, making it the preferred choice for a broad range of consumer and automotive applications where manufacturing scalability and consistent quality are paramount. The process ensures a clean and precise package outline. |

| By Application |

|

Consumer Electronics stands as the largest application segment, driven by the insatiable demand for miniaturized, high-performance components in smartphones, wearables, and portable devices. The QFN package’s compact footprint and excellent thermal dissipation characteristics are critical for enabling sleek product designs without compromising on processing power or battery life, solidifying its indispensable role in this fast-paced industry. |

| By End User |

|

Electronics OEMs/ODMs constitute the primary end-user segment, leveraging QFN packaging to integrate advanced functionality into their final products. These companies value the package’s design flexibility, which allows for customization to meet specific performance and space constraints, alongside its proven reliability which is essential for maintaining brand reputation and minimizing warranty claims in competitive markets. |

| By Package Size |

|

Above 5×5 to 7×7 mm packages are the leading category, striking an optimal balance between accommodating a higher number of I/O connections and maintaining a relatively compact form factor. This size range is particularly suited for complex analog and power management ICs used across automotive and communications applications, where both performance and space savings are critical design considerations. |

| By Lead Count |

|

Medium Lead Count packages are the most widely adopted, as they efficiently serve the core market need for a sufficient number of interconnects to handle standard microcontroller and interface IC functionalities. This segment offers the best compromise, providing the necessary connectivity for most applications without introducing the complexities and higher costs associated with very high-density packages, ensuring broad compatibility and manufacturability. |

Regional Analysis: Quad-Flat-No-Lead Packaging (QFN) Market

Asia-Pacific’s dominance is anchored by its dense network of semiconductor fabrication plants and advanced OSAT facilities. Countries like China and Taiwan have become global epicenters for producing consumer electronics, creating an insatiable demand for cost-effective and reliable packaging. The proximity of component suppliers, assembly lines, and end-product manufacturers creates a highly efficient and responsive supply chain, enabling rapid adoption and scaling of QFN packaging technologies for applications from smartphones to automotive control units.

The automotive sector’s rapid electrification and the consumer electronics industry’s push for thinner, lighter devices are major growth drivers. QFN packages are extensively used in power management ICs, microcontrollers, and RF components essential for these applications. The region’s strong foothold in manufacturing electric vehicles, 5G infrastructure, and smart home devices ensures a sustained and growing demand pipeline for QFN packaging solutions, with manufacturers continuously innovating to meet specific thermal and performance requirements.

Continuous R&D investment by key regional players focuses on enhancing QFN performance. Innovations include the development of multi-row QFNs for higher pin counts, improved thermal dissipation techniques using exposed pads, and adaptations for high-frequency applications. Collaboration between material science companies and packaging foundries in the region fosters a rapid cycle of innovation, allowing QFN technology to evolve to meet the increasing performance demands of next-generation electronic systems, keeping the region at the forefront of packaging technology.

A robust and mature supply chain for substrates, leadframes, and molding compounds is a critical advantage. Governments in countries like China, South Korea, and Japan actively support the semiconductor industry through subsidies, tax incentives, and national research initiatives, creating a favorable environment for sustained investment in packaging technologies. This supportive ecosystem reduces production costs, mitigates supply risks, and accelerates the commercialization of new QFN package designs, reinforcing the region’s competitive edge.

North America

North America remains a significant market for QFN packaging, characterized by its strong demand from the aerospace, defense, and high-performance computing sectors. The region’s market is driven by the need for reliable and thermally efficient packages for advanced microprocessors, graphics processing units, and specialized communication chips. The presence of major fabless semiconductor companies and integrated device manufacturers fuels the adoption of advanced QFN variants that offer superior electrical performance and miniaturization. While the volume of manufacturing is lower than in Asia-Pacific, the focus is on high-value, high-complexity applications, with stringent quality and reliability requirements that push the technological boundaries of QFN packaging.

Europe

Europe holds a strong position in the QFN market, primarily supported by its robust automotive industry and industrial automation sector. German and French automotive manufacturers, in particular, are major consumers of QFNs for engine control units, sensors, and infotainment systems. The region’s emphasis on quality and long-term reliability aligns well with the inherent strengths of QFN packages. Furthermore, the growing focus on renewable energy and smart grid technologies in Europe is creating new avenues for QFN adoption in power conversion and management systems. Collaborative R&D projects between academia and industry ensure that European players remain competitive in developing specialized QFN solutions for their key markets.

South America

The QFN market in South America is in a developing stage, with growth primarily linked to the increasing local assembly of consumer electronics and automotive components, particularly in Brazil and Mexico. The market is driven by the gradual modernization of industrial infrastructure and rising disposable incomes, which boost demand for smartphones, appliances, and vehicles that utilize QFN-packaged ICs. While the region relies heavily on imported semiconductor components, the establishment of local assembly plants by global electronics manufacturers is stimulating gradual market growth. The focus is on cost-effective QFN solutions for mid-range applications, with potential for expansion as the industrial base matures.

Middle East & Africa

The Middle East & Africa region represents an emerging market for QFN packaging, with growth prospects tied to infrastructure development and economic diversification efforts, especially in Gulf Cooperation Council countries. The increasing investment in telecommunications infrastructure, including 5G deployment, and the adoption of smart city technologies are creating nascent demand for electronic components. While the local semiconductor industry is minimal, the region serves as an important consumption market. The adoption of QFN packages is expected to grow in line with the expansion of the electronics retail market and the gradual development of localized technical assembly and servicing capabilities for imported electronic goods.

Report Scope

This market research report provides a comprehensive analysis of the Quad-Flat-No-Lead Packaging (QFN) Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Quad-Flat-No-Lead Packaging (QFN) Market?

-> Global Quad-Flat-No-Lead Packaging (QFN) Market was valued at USD 3464 million in 2024 and is projected to reach USD 3987 million by 2032, at a CAGR of 2.1% during the forecast period.

Which key companies operate in Quad-Flat-No-Lead Packaging (QFN) Market?

-> Key players include ASE(SPIL), Amkor Technology, JCET Group, Powertech Technology Inc., and Tongfu Microelectronics, among others. The top five players occupy a share of about 70%.

What are the key growth drivers?

-> Key growth drivers include the compact size, good thermal performance, and reliability of QFN packaging, which enables the development of smaller and more powerful electronic devices while optimizing space utilization on PCBs.

Which region dominates the market?

-> Asia-Pacific is the largest market, with a share of about 77%, followed by Europe and North America.

What are the emerging trends?

-> Emerging trends include the widespread adoption across consumer electronics, telecommunications, automotive, and industrial applications, driven by the demand for compact and low-profile IC packaging solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...