Process Automation Control Market Insights

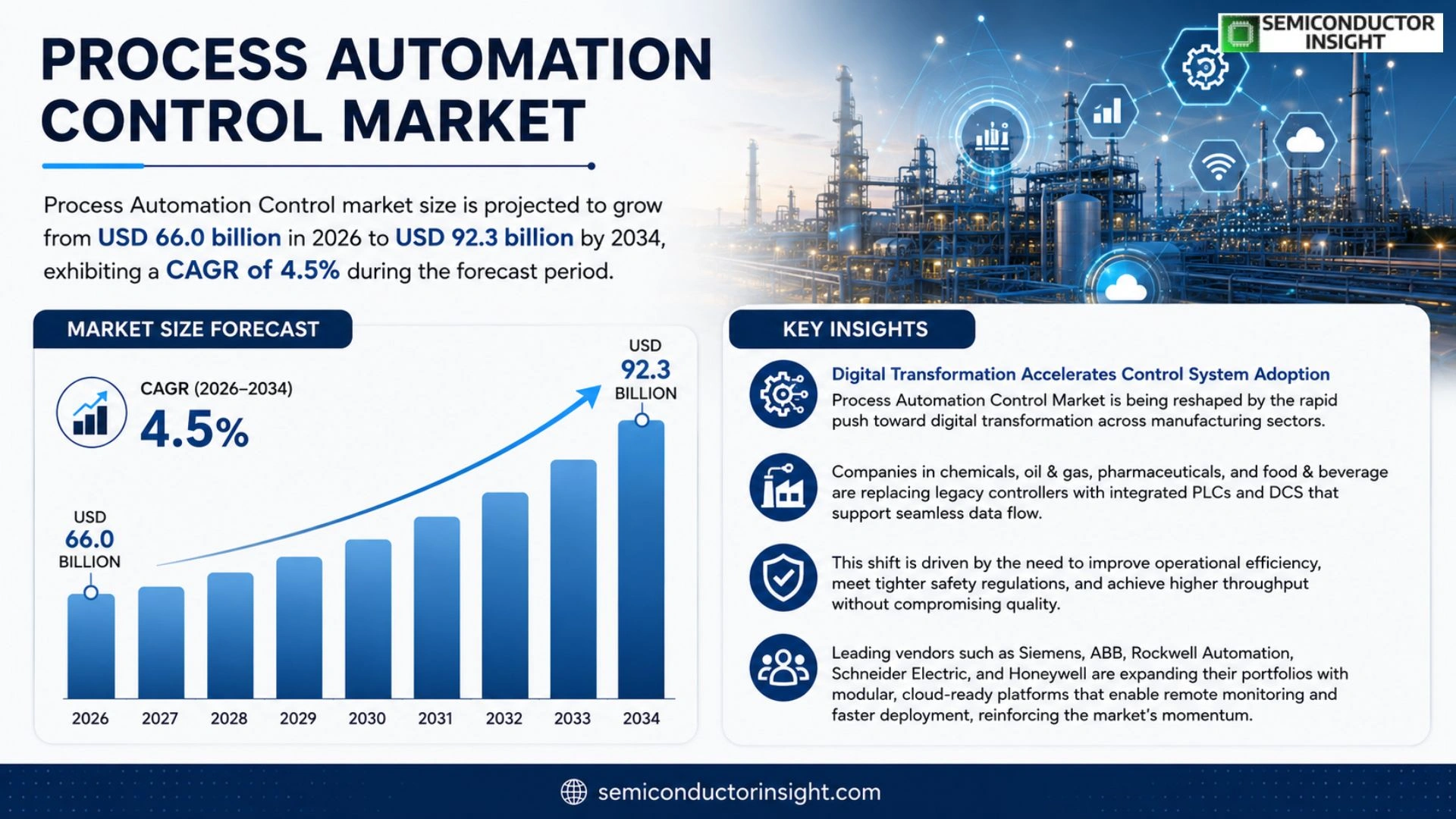

Global Process Automation Control market size was valued at USD 62.5 billion in 2025. The market is projected to grow from USD 66.0 billion in 2026 to USD 92.3 billion by 2034, exhibiting a CAGR of 4.5% during the forecast period.

Process automation control encompasses integrated hardware and software solutions that monitor, regulate, and optimize industrial processes across sectors such as chemicals, oil & gas, pharmaceuticals, and food & beverage. Core components include programmable logic controllers (PLCs), distributed control systems (DCS), supervisory control and data acquisition (SCADA) platforms, and advanced analytics that enable real‑time decision making.

The market is accelerating because manufacturers are investing heavily in digital transformation, while rising demand for operational efficiency and stringent safety regulations drive adoption of advanced control systems. Furthermore, the emergence of edge computing and AI‑enhanced analytics is expanding functionality, prompting leading vendors,such as Siemens AG, ABB Ltd., Rockwell Automation, Schneider Electric, and Honeywell International,to launch next‑generation solutions that further fuel growth.

MARKET DRIVERS

Digital Transformation Across Industries

The accelerating adoption of digital twins and IoT connectivity is fueling demand for advanced control solutions. Companies are investing in scalable architectures to enhance real‑time decision‑making, directly expanding Process Automation Control Market. This shift is evident in manufacturing, energy, and water treatment sectors where operational efficiency is a competitive imperative.

Regulatory Pressure for Safety and Emissions

Stringent environmental and safety regulations are compelling firms to upgrade legacy control systems. Modern platforms provide precise monitoring of emissions and process parameters, enabling compliance while reducing downtime. Such compliance drives capital allocation toward next‑generation automation, reinforcing growth Process Automation Control Market.

➤ “Enterprises that replace outdated PLCs with integrated control suites can achieve up to 15% reduction in energy consumption within the first year.”

Strategic partnerships between automation vendors and cloud providers are creating hybrid solutions that combine on‑premise reliability with scalable analytics. This collaborative ecosystem accelerates technology rollout, positioning the market for sustained expansion over the next five years.

MARKET CHALLENGES

High Initial Capital Expenditure

Deploying state‑of‑the‑art control hardware and software often requires significant upfront investment. For many mid‑size operators, the payback horizon can be uncertain, leading to cautious budgeting and slower adoption rates Process Automation Control Market.

Other Challenges

Talent Gap in Advanced Control Engineering

The scarcity of engineers proficient in both legacy systems and emerging AI‑driven control algorithms creates implementation bottlenecks, limiting the speed at which organizations can modernize.

MARKET RESTRAINTS

Legacy System Inertia

Many established facilities continue operating on decades‑old control infrastructure. The perceived risk and disruption associated with replacing these systems act as a restraint on market penetration, especially in regions where retrofit costs exceed short‑term financial incentives.

Additionally, interoperability concerns between newer open‑architecture platforms and proprietary legacy protocols often require custom integration, further increasing project complexity and deterring investment.

Supply chain volatility for critical components such as high‑performance processors and specialized sensors can also delay project timelines, adding another layer of restraint to market growth.

MARKET OPPORTUNITIES

Edge Computing and AI‑Enhanced Control

Edge analytics enable real‑time optimization of process parameters without relying on constant cloud connectivity. Coupled with machine‑learning models, these capabilities offer predictive maintenance and autonomous adjustments, opening new revenue streams for solution providers Process Automation Control Market.

Emerging markets in Southeast Asia and Latin America are experiencing rapid industrialization, creating a sizable demand for modular and cost‑effective control solutions. Vendors that tailor offerings to local standards and provide flexible financing models can capture significant market share.

Finally, the convergence of cybersecurity frameworks with control system design presents an opportunity to differentiate products. Solutions that embed robust threat detection and response mechanisms are poised to become preferred choices as the industry prioritizes secure automation.

Process Automation Control Market Trends

Digital Transformation Accelerates Control System Adoption

Process Automation Control Market is being reshaped by the rapid push toward digital transformation across manufacturing sectors. Companies in chemicals, oil & gas, pharmaceuticals, and food & beverage are replacing legacy controllers with integrated programmable logic controllers (PLCs) and distributed control systems (DCS) that support seamless data flow. This shift is driven by the need to improve operational efficiency, meet tighter safety regulations, and achieve higher throughput without compromising quality. Leading vendors such as Siemens, ABB, Rockwell Automation, Schneider Electric, and Honeywell are expanding their portfolios with modular, cloud‑ready platforms that enable remote monitoring and faster deployment, reinforcing the market’s momentum.

Other Trends

Edge Computing and Real‑Time Analytics

Edge computing is emerging as a pivotal enabler for Process Automation Control Market, allowing critical data to be processed locally on the plant floor. By minimizing latency, edge devices support real‑time analytics that can instantly adjust process variables, leading to reduced downtime and energy consumption. Distributed control architectures now incorporate AI‑driven algorithms that analyze sensor streams at the edge, providing operators with actionable insights before a fault escalates. This capability is especially valuable in high‑risk environments where milliseconds can determine safety outcomes, prompting manufacturers to invest heavily in edge‑ready SCADA and DCS solutions.

AI‑Enhanced Predictive Maintenance

Predictive maintenance, powered by advanced AI models, is another cornerstone of Process Automation Control Market’s evolution. By continuously learning from historical performance data, AI can forecast equipment wear patterns and schedule interventions proactively. This reduces unplanned outages and extends asset life, delivering tangible cost savings. Vendors are integrating these predictive functions directly into control consoles, allowing plant managers to visualize health scores alongside traditional process metrics. The convergence of AI with existing control hardware fosters a more resilient production ecosystem, positioning the market for sustained growth as organizations prioritize reliability and sustainability.

COMPETITIVE LANDSCAPE

Key Industry Players

Process Automation Control Market Competitive Overview

Process Automation Control market is dominated by a handful of multinational technology firms that command the majority of high‑value contracts in chemicals, oil & gas, pharmaceuticals, and food & beverage sectors. Siemens AG leads with its Integrated Control Suite, while ABB Ltd. leverages its Distributed Control System portfolio to capture large‑scale projects. Rockwell Automation’s FactoryTalk and Schneider Electric’s EcoStruxure platforms are tightly integrated with PLC and SCADA offerings, reinforcing their position in North America and Europe. Honeywell International adds advanced analytics and safety instrumented systems, expanding its footprint in regulated industries. Together, these incumbents shape a tiered market structure where Tier‑1 vendors provide end‑to‑end hardware‑software solutions, and Tier‑2 integrators focus on niche verticals or specialized engineering services.

Beyond the Tier‑1 giants, a diverse set of niche players contributes to innovation and regional market depth. Mitsubishi Electric and Yokogawa Electric deliver strong PLC and DCS solutions in Asia‑Pacific, while Emerson Electric’s DeltaV platform remains popular in process industries. Beckhoff Automation and B&R Automation (an ABB subsidiary) differentiate with open‑architecture control hardware that appeals to OEMs. Indie‑focused firms such as Inductive Automation (Ignition), Opto 22, and Automation Anywhere drive the shift toward cloud‑native and low‑code SCADA environments. Aspen Technology, while primarily a process optimization software vendor, increasingly embeds control‑oriented analytics, widening the competitive set for advanced, AI‑enhanced automation deployments.

List of Key Process Automation Control Companies Profiled

- Siemens AG

- ABB Ltd.

- Rockwell Automation

- Schneider Electric

- Honeywell International

- Mitsubishi Electric

- Yokogawa Electric

- Emerson Electric

- Beckhoff Automation

- B&R Automation

- Inductive Automation

- Aspen Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Programmable Logic Controllers (PLCs)

|

| By Application |

|

Continuous Flow

|

| By End User |

|

Chemicals

|

| By Deployment Model |

|

Hybrid Deployment

|

| By Functional Focus |

|

Process Optimization

|

Regional Analysis: North America

United States

The manufacturing industry in the US is a primary driver of demand for Process Automation Control. Businesses are seeking to improve production throughput, reduce downtime, and enhance product quality through the implementation of advanced control systems. The integration of IIoT devices and cloud-based platforms is further accelerating this trend.

The oil and gas sector in the US relies heavily on Process Automation Control for optimizing extraction, refining, and transportation processes. The focus is on enhancing safety, improving operational efficiency, and reducing environmental impact through advanced control technologies.

The pharmaceutical industry in the US demands high levels of precision and control in its manufacturing processes. Process Automation Control plays a crucial role in ensuring product quality, compliance with stringent regulations, and enhancing operational efficiency.

The increasing need for efficient water and wastewater management systems is driving the adoption of Process Automation Control in the US. Implementing automated control systems helps optimize water distribution, reduce energy consumption, and ensure regulatory compliance.

Europe

The European Process Automation Control market is characterized by a strong emphasis on sustainability and energy efficiency. Stringent environmental regulations across the continent are driving investments in automation solutions that optimize resource utilization and minimize environmental impact. The market is also witnessing growth in sectors like food & beverage and chemicals, where process control is critical for maintaining product quality and safety. Collaborative research and development initiatives are fostering innovation in areas like digital twins and advanced analytics for process optimization.

Asia-Pacific

Asia-Pacific represents a rapidly expanding market for Process Automation Control, driven by strong industrial growth in countries like China and India. Government initiatives promoting manufacturing and infrastructure development are fueling demand for automation solutions across various sectors. The adoption of smart manufacturing and Industry 4.0 concepts is accelerating the uptake of advanced control systems. However, the market faces challenges related to fragmented infrastructure and varying levels of technological sophistication across different countries in the region.

South America

Process Automation Control market in South America is experiencing steady growth, particularly in Brazil and Argentina, due to increasing investments in infrastructure and industrial sectors. The demand for automation solutions is driven by the need to improve operational efficiency, reduce costs, and enhance productivity in industries like mining, agriculture, and energy. Government support for industrial development and increasing awareness of the benefits of automation are contributing to the market’s expansion.

Middle East & Africa

Process Automation Control market in the Middle East & Africa is witnessing growth fueled by investments in oil & gas, petrochemicals, and infrastructure projects. The region’s focus on energy diversification and industrialization is driving demand for automation solutions that enhance operational efficiency and optimize resource utilization. The increasing adoption of digital technologies and smart manufacturing concepts is further accelerating market growth.

Report Scope

This market research report provides a comprehensive analysis of the Process Automation Control Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Process Automation Control Market?

-> Process Automation Control market size was valued at USD 62.5 billion in 2025. The market is projected to grow from USD 66.0 billion in 2026 to USD 92.3 billion by 2034.

Which key companies operate Process Automation Control Market?

-> Key players include Siemens AG, ABB Ltd., Rockwell Automation, Schneider Electric, and Honeywell International, among others.

What are the key growth drivers?

-> Key growth drivers include digital transformation investments, demand for operational efficiency, stringent safety regulations, and the emergence of edge computing and AI‑enhanced analytics.

Which region dominates the market?

-> The reference does not specify a single dominant region; adoption is strong across major industrial regions worldwide.

What are the emerging trends?

-> Emerging trends include integration of edge computing, AI‑driven advanced analytics, and next‑generation control solutions such as PLCs, DCS, and SCADA platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...