MARKET INSIGHTS

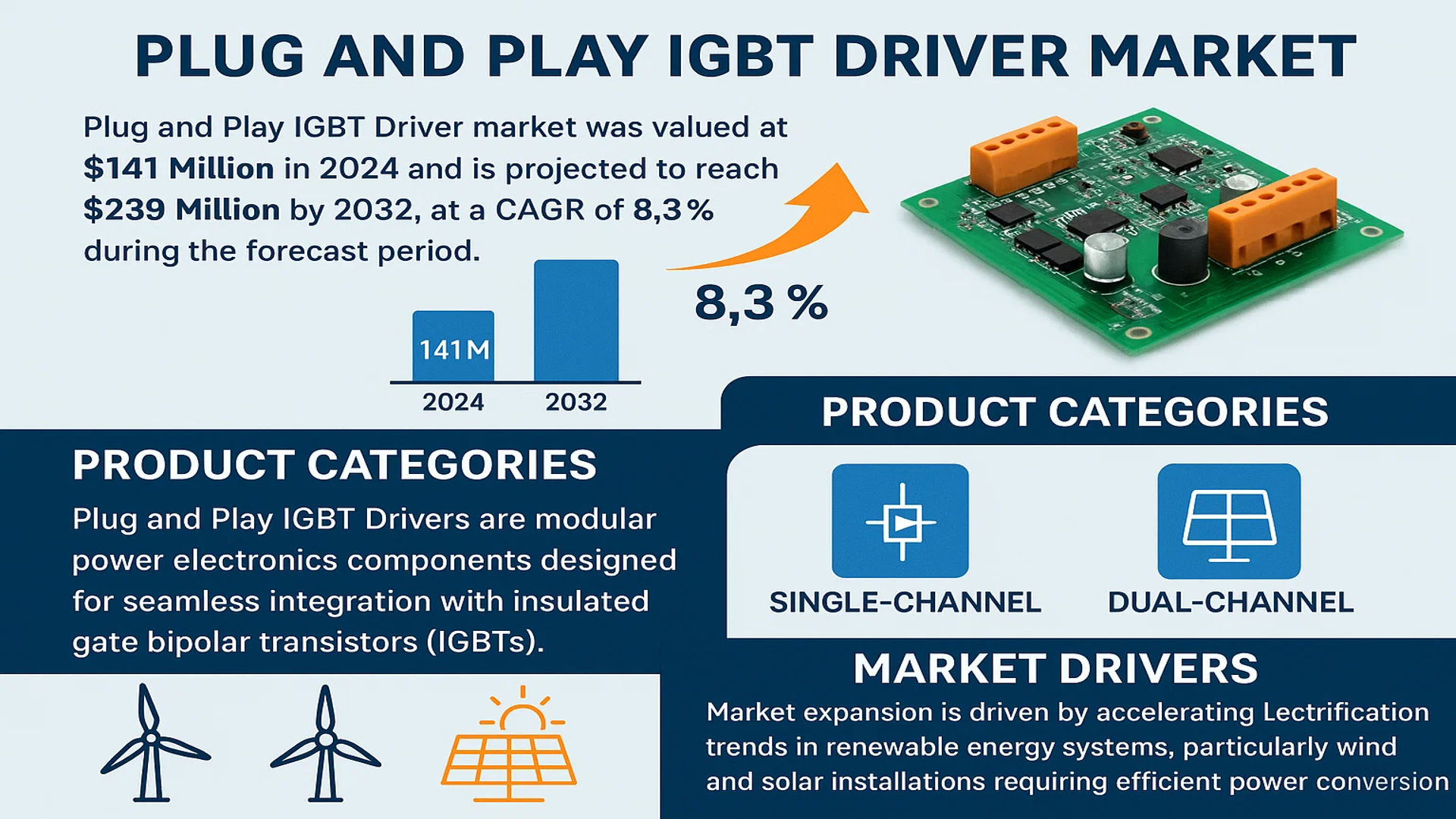

The global Plug and Play IGBT Driver Market was valued at 141 million in 2024 and is projected to reach US$ 239 million by 2032, at a CAGR of 8.3% during the forecast period.

Plug and Play IGBT Drivers are modular power electronics components designed for seamless integration with insulated gate bipolar transistors (IGBTs). These drivers simplify system implementation by offering standardized interfaces, reducing development time while enhancing reliability in high-voltage switching applications. Key product categories include Single-Channel and Dual-Channel variants, catering to diverse power management requirements across industries.

Market expansion is driven by accelerating electrification trends in renewable energy systems, particularly wind and solar installations requiring efficient power conversion. The automotive sector’s shift toward electric vehicles (EVs) further propels demand, as IGBT drivers enable precise motor control in traction inverters. Industrial automation adoption, particularly in Asia-Pacific manufacturing hubs, contributes significantly to volume growth. Major players like Power Integrations and Microchip are advancing driver IC technologies with integrated protection features, addressing reliability concerns in harsh operating environments.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Energy-Efficient Power Electronics to Propel Market Expansion

The global push toward energy efficiency across industries is driving significant demand for plug and play IGBT drivers. With industries increasingly adopting power electronics to reduce energy consumption, these drivers play a critical role in optimizing insulated gate bipolar transistor performance. The power electronics market is projected to grow robustly, creating parallel demand for reliable driver solutions. Industrial automation and renewable energy sectors particularly benefit from the precise switching capabilities of advanced IGBT drivers, which contribute to system-wide efficiency improvements.

Automotive electrification trends further accelerate adoption, as electric vehicles rely heavily on power electronics for drivetrain efficiency. Leading automotive manufacturers are integrating plug and play solutions to streamline production while maintaining performance standards. The modular nature of these drivers allows for rapid implementation in various vehicle voltage classes, from hybrid systems to full battery electric platforms.

Expansion of Renewable Energy Infrastructure Creating Sustained Demand

Global renewable energy capacity additions reached record levels recently, with solar and wind installations driving substantial demand for power conversion equipment. Plug and play IGBT drivers have become essential components in inverters and converters used in renewable energy systems. Their ability to simplify complex power electronics integration reduces installation time and maintenance requirements in large-scale solar farms and wind turbines.

Grid modernization efforts further amplify this demand, as smart grid technologies require sophisticated power electronics with reliable driver components. The standardization benefits of plug and play solutions enable scalable deployments across distributed generation systems while maintaining consistent performance benchmarks. Project pipelines for utility-scale renewable projects indicate continued market growth potential for IGBT driver solutions.

➤ The transition toward higher voltage systems in renewable applications has specifically increased demand for drivers capable of handling 1200V+ applications with advanced protection features.

Industrial Automation Boom Driving Adoption Across Manufacturing Sectors

Manufacturing industries worldwide are undergoing rapid automation, significantly increasing deployment of motor drives and power control systems that utilize IGBT technology. The plug and play driver market benefits from this trend through both direct sales to equipment manufacturers and replacement demand in existing facilities. Industrial motor drive systems accounted for nearly 40% of power electronics revenue recently, representing a substantial addressable market for driver solutions.

Industry 4.0 initiatives emphasize the importance of modular, easily maintainable components in smart factories. Plug and play drivers align perfectly with this philosophy by reducing system downtime during maintenance or upgrades. Their standardized interfaces and diagnostic capabilities facilitate predictive maintenance strategies that are becoming standard in advanced manufacturing environments.

MARKET RESTRAINTS

High Initial Costs Limit Adoption in Price-Sensitive Applications

While plug and play IGBT drivers offer substantial long-term benefits, their premium pricing structure creates adoption barriers in cost-conscious market segments. The sophisticated protection circuits, isolation technologies, and advanced diagnostic capabilities that differentiate these solutions contribute to manufacturing costs that can be 30-50% higher than conventional drivers. This pricing differential makes justification challenging in applications where basic functionality meets requirements.

Emerging markets present particular challenges, where upfront cost often outweighs lifecycle value considerations. Manufacturers face ongoing pressure to develop cost-optimized versions without compromising performance, particularly for medium-power applications where price sensitivity is highest.

Other Constraints

Technical Complexity in High-Frequency Applications

High-speed switching applications push the limits of current plug and play driver capabilities. Maintaining signal integrity and minimizing propagation delays becomes increasingly challenging above certain frequency thresholds. These technical limitations require ongoing R&D investment from manufacturers to expand addressable applications.

Thermal Management Challenges

As power densities increase across applications, thermal performance becomes a critical limitation. Plug and play form factors must balance compact sizing with effective heat dissipation, creating design tradeoffs that can impact reliability in demanding operating conditions.

MARKET CHALLENGES

Supply Chain Volatility Impacts Component Availability

The semiconductor supply chain disruptions that began recently continue affecting plug and play IGBT driver production. Critical components including isolation ICs and advanced packaging materials face allocation constraints that delay deliveries. Lead times for complete driver modules have extended significantly, forcing manufacturers to implement inventory buffer strategies that increase working capital requirements.

Geopolitical factors compound these challenges, as trade policies and export controls create uncertainty around semiconductor sourcing. The industry’s reliance on specialized foundries for key components leaves it vulnerable to fab capacity fluctuations and regional disruptions.

Other Challenges

Design Standardization Complexities

While plug and play solutions aim for standardization, application-specific requirements often necessitate customization. Balancing standardization benefits with the need for application optimization creates ongoing design challenges. Customer demands for tailored solutions reduce economies of scale that could lower production costs.

Cybersecurity Concerns in Connected Systems

As industrial systems incorporate more connectivity, cybersecurity vulnerabilities in power electronics subsystems become significant concerns. Driver modules with advanced diagnostics and remote monitoring capabilities must implement robust security protocols, adding development complexity.

MARKET OPPORTUNITIES

Advancements in Wide Bandgap Semiconductors Creating New Application Possibilities

The emergence of silicon carbide and gallium nitride power devices presents substantial growth opportunities for next-generation IGBT drivers. These wide bandgap semiconductors operate at higher frequencies and temperatures than traditional silicon, requiring specialized driver solutions. Early adoption in electric vehicle fast charging and high-efficiency power supplies demonstrates the potential for plug and play drivers optimized for these emerging technologies.

Manufacturers investing in compatible driver architectures can capture first-mover advantage in these high-growth segments. The superior switching characteristics of wide bandgap devices particularly benefit from advanced driver features like adjustable gate drive strength and precise timing control.

Edge Computing Integration Enables Smarter Power Management

The convergence of power electronics with edge computing creates opportunities for intelligent plug and play drivers with enhanced monitoring capabilities. By incorporating local processing power, these smart drivers can perform real-time analytics for predictive maintenance and performance optimization. This evolution aligns with broader industrial IoT trends, where distributed intelligence improves system reliability.

Leading manufacturers are already developing solutions that communicate critical parameters to asset management systems while maintaining the simplicity of plug and play installation. The market potential spans industrial, energy, and transportation applications where equipment uptime is critical.

Strategic partnerships between power electronics and industrial IoT firms accelerate this transition. Collaborative development efforts focus on standardizing data interfaces and protocols to ensure interoperability across ecosystems. The resulting solutions promise to transform power electronics maintenance strategies while preserving the installation simplicity that defines plug and play products.

PLUG AND PLAY IGBT DRIVER MARKET TRENDS

Increasing Demand for Energy-Efficient Power Electronics to Drive Market Growth

The global Plug and Play IGBT Driver market is witnessing significant growth due to the rising adoption of energy-efficient power electronic systems across various industries. With a valuation of 141 million USD in 2024, the market is projected to expand at a CAGR of 8.3%, reaching 239 million USD by 2032. The demand is primarily fueled by industries such as renewable energy (wind and solar power), rail transportation, and industrial automation, where IGBT drivers enhance system efficiency and reduce power losses. The increasing focus on electrification in automotive applications, particularly in electric vehicles (EVs), further amplifies this growth trajectory.

Other Trends

Rise of Single-Channel and Dual-Channel IGBT Drivers

The market is experiencing notable segmentation between single-channel and dual-channel IGBT drivers. While single-channel drivers dominate applications requiring precise individual control, such as consumer electronics and smaller industrial systems, dual-channel drivers are gaining traction in high-power applications like rail transit and large-scale renewable energy installations. The single-channel segment is expected to reach a significant market value in the coming years, driven by its cost-effectiveness and ease of integration in compact systems.

Regional Growth and Market Competition

Geographically, China and the U.S. are leading the charge in Plug and Play IGBT Driver adoption. China’s aggressive investments in renewable energy and high-speed rail infrastructure position it as a high-growth market, while the U.S. benefits from technological advancements in automotive and industrial automation sectors. Additionally, key industry players such as Power Integrations, Microchip, and IXYS are strengthening their market presence through product innovations and strategic collaborations. The competitive landscape remains dynamic, with the top five companies collectively commanding a substantial revenue share in 2024.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Alliances Drive Market Competition

The global Plug and Play IGBT Driver market is characterized by a dynamic competitive landscape, featuring a mix of established semiconductor leaders and specialized manufacturers. With the market projected to reach $239 million by 2032, companies are aggressively expanding their portfolios to capitalize on growing demand across renewable energy, industrial automation, and electric vehicles.

Power Integrations dominates the market, leveraging its patented SCALE IGBT driver technology and strong foothold in high-voltage applications. The company’s recent partnership with major wind turbine manufacturers has further solidified its leadership in renewable energy solutions. Close behind, Microchip Technology has gained significant traction through its adaptive gate driver ICs, particularly in the automotive sector where precision and reliability are paramount.

Meanwhile, IXYS (acquired by Littelfuse) and Firstack are competing aggressively through technological differentiation. IXYS focuses on ruggedized drivers for harsh industrial environments, while Firstack has made strides in compact dual-channel solutions for space-constrained applications like consumer electronics and IoT devices.

The competitive intensity is further amplified by regional players such as Beijing POWER-SEM and Poweralia, who are capturing market share through cost-competitive offerings tailored for Asian manufacturing hubs. These companies benefit from localized supply chains and government incentives supporting domestic semiconductor production.

With the market growing at 8.3% CAGR, key players are investing heavily in R&D to develop intelligent drivers with built-in protection features and diagnostic capabilities. Strategic acquisitions have also emerged as a preferred growth strategy, as seen in Microchip’s recent purchase of a German driver IC specialist to bolster its European presence.

List of Key Plug and Play IGBT Driver Companies Profiled

- Power Integrations (U.S.)

- Firstack (China)

- Microchip Technology (U.S.)

- IXYS (Germany) – Littelfuse subsidiary

- Poweralia (Spain)

- SEMICODE (South Korea)

- SemiSouth (U.S.)

- TeknoCEA (France)

- Bronze Technologies (Italy)

- Beijing POWER-SEM (China)

Segment Analysis:

By Type

Single-Channel Type Segment Dominates Due to Cost-Effective Deployment in Compact Systems

The market is segmented based on type into:

- Single-Channel Type

- Dual-Channel Type

By Application

Industrial Automation Segment Leads Owing to Rising Demand for Smart Manufacturing Solutions

The market is segmented based on application into:

- Industrial Automation

- Wind Power and Solar Energy

- Rail Transit

- Automotives

- Home Appliances and Consumer Electronics

- Others

By End-User

Energy Sector Exhibits Strong Adoption Driven by Renewable Power Generation Needs

The market is segmented based on end-user into:

- Energy Sector

- Manufacturing Industries

- Transportation

- Consumer Electronics

- Others

Regional Analysis: Plug and Play IGBT Driver Market

Asia-Pacific

The Asia-Pacific region dominates the global Plug and Play IGBT Driver market, driven by rapid industrialization and substantial investments in renewable energy projects. Countries like China, Japan, and India are at the forefront, with China alone accounting for over 40% of regional demand due to its extensive industrial automation sector and renewable energy push. The region benefits from strong local manufacturing capabilities and cost-efficient production, making it a hub for key players like Beijing POWER-SEM and Poweralia. Rising adoption in wind and solar power applications, coupled with expanding rail transit networks, further fuels market growth. However, intense price competition and evolving technological standards present ongoing challenges for manufacturers.

North America

North America remains a technologically advanced market with stringent quality standards, where companies like Power Integrations and Microchip lead innovation. The U.S. market is primarily driven by demand from industrial automation and electric vehicle sectors, supported by government initiatives promoting clean energy adoption. Canada’s growing wind energy projects contribute to steady demand for high-performance IGBT drivers. While the market shows maturity in certain segments, ongoing upgrades in power infrastructure and smart grid development continue to create opportunities. Intense competition from Asian manufacturers and higher product costs relative to other regions remain noteworthy market constraints.

Europe

European markets emphasize energy efficiency and sustainability, driving demand for advanced Plug and Play IGBT Drivers in wind power and industrial applications. Germany leads regional adoption, supported by its strong automotive and renewable energy sectors. EU regulations promoting energy-efficient technologies accelerate market growth, particularly for dual-channel driver solutions. Companies like IXYS and SEMICODE benefit from the region’s focus on precision engineering. However, slower industrial growth in some Southern European countries and complex certification processes somewhat limit market expansion compared to Asia’s rapid pace.

South America

The South American market shows gradual but promising growth, with Brazil and Argentina emerging as key demand centers. Increasing investments in power infrastructure and renewable energy projects drive market opportunities, though economic volatility affects adoption rates. Local manufacturers face challenges competing with imported Asian products on price, limiting domestic production growth. The automotive sector shows growing potential as electric vehicle initiatives gain traction, but the market remains constrained by limited technical expertise and infrastructure bottlenecks in some countries.

Middle East & Africa

This region represents an emerging market with strong long-term growth potential, particularly in renewable energy applications. Gulf Cooperation Council (GCC) countries lead adoption, driven by solar power projects and industrial diversification efforts. However, limited local manufacturing and reliance on imports currently restrict market expansion. Infrastructure development initiatives across Africa present future opportunities, though the market faces challenges including inconsistent power supply and technical skill gaps that affect product implementation and maintenance capabilities.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Plug and Play IGBT Driver markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Plug and Play IGBT Driver market was valued at USD 141 million in 2024 and is projected to reach USD 239 million by 2032, at a CAGR of 8.3%.

- Segmentation Analysis: Detailed breakdown by product type (Single-Channel Type, Dual-Channel Type), application (Home Appliances, Wind Power, Rail Transit, Automotives, Industrial Automation), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market is a key contributor, while China shows rapid growth potential.

- Competitive Landscape: Profiles of leading market participants including Power Integrations, Microchip, IXYS, SEMICODE, and Beijing POWER-SEM, covering their product portfolios, market share (top 5 players held significant revenue share in 2024), and strategic developments.

- Technology Trends & Innovation: Assessment of smart driver integration, energy-efficient designs, and compatibility advancements with next-gen power electronics.

- Market Drivers & Restraints: Growth driven by renewable energy adoption and industrial automation, while supply chain complexities pose challenges.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, system integrators, and investors in the power electronics ecosystem.

The report employs primary research (industry expert interviews) and secondary research (verified market data) to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Plug and Play IGBT Driver Market?

-> Plug and Play IGBT Driver Market was valued at 141 million in 2024 and is projected to reach US$ 239 million by 2032, at a CAGR of 8.3% during the forecast period.

Which key companies operate in this market?

-> Major players include Power Integrations, Microchip, IXYS, SEMICODE, Beijing POWER-SEM, Firstack, and TeknoCEA.

What are the key growth drivers?

-> Renewable energy adoption, industrial automation growth, and electric vehicle proliferation are primary drivers.

Which region dominates the market?

-> Asia-Pacific leads in growth, while North America remains technologically advanced with significant market share.

What are the emerging trends?

-> Smart driver integration, miniaturization, and compatibility with wide-bandgap semiconductors are key trends.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...