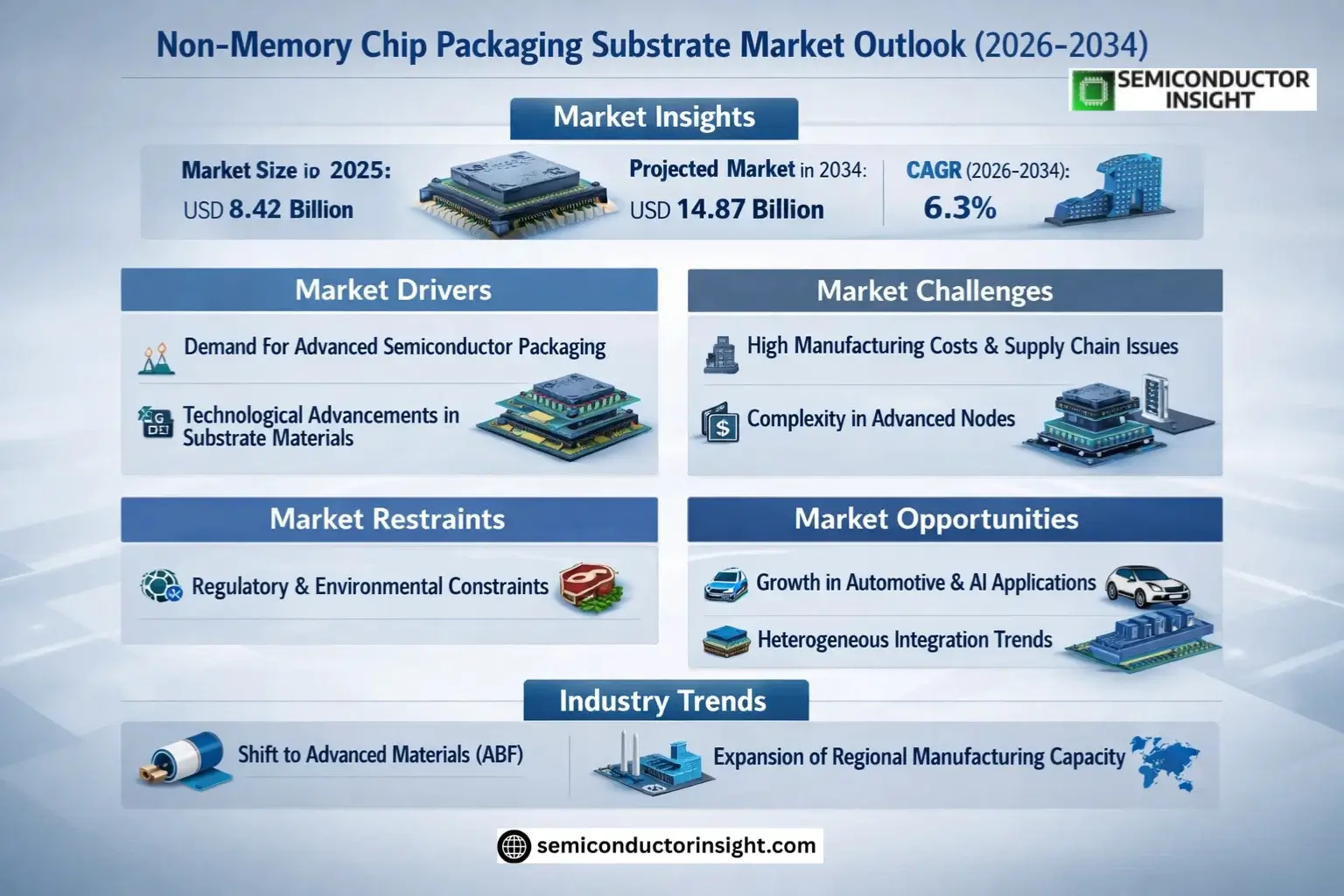

Market Insights

Global Non-Memory Chip Packaging Substrate Market size was valued at USD 8.42 billion in 2025. The market is projected to grow from USD 9.15 billion in 2026 to USD 14.87 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Non-Memory Chip Packaging Substrate Market are critical components used in semiconductor packaging for logic chips, communication ICs, sensors, and other non-memory applications. These substrates provide electrical connectivity, thermal management, and mechanical support for integrated circuits while enabling miniaturization and performance optimization in advanced packaging solutions such as flip-chip and wafer-level packaging.

The market growth is driven by increasing demand for high-performance computing, 5G infrastructure deployment, and automotive electronics. Key players like Ibiden, Shinko Electric Industries, and Samsung Electro-Mechanics are investing in advanced substrate technologies to meet the requirements of next-generation semiconductor devices with finer pitch interconnects and improved thermal dissipation capabilities.

MARKET DRIVERS

Growing Demand for Advanced Semiconductor Packaging

Non-Memory Chip Packaging Substrate Market is experiencing robust growth driven by increasing demand for high-performance computing and AI applications. The rise of 5G, IoT, and automotive electronics has accelerated the adoption of advanced packaging solutions. Major chip manufacturers are shifting toward substrate-level packaging to meet the miniaturization and power efficiency requirements of modern semiconductors.

Technological Advancements in Packaging Substrates

Innovations in substrate materials, such as high-density interconnect (HDI) and organic substrates, are enabling higher signal integrity and thermal performance. Non-Memory Chip Packaging Substrate Market is benefiting from the transition to finer pitch and multilayer substrates that support complex chip architectures.

Additionally, the increasing complexity of system-on-chip (SoC) designs has amplified the need for sophisticated substrate solutions that can handle multiple functions while maintaining reliability.

MARKET CHALLENGES

High Manufacturing Costs and Supply Chain Constraints

The production of Non-Memory Chip Packaging Substrates requires specialized materials and precision manufacturing, leading to high costs. Supply chain disruptions have exacerbated material shortages, particularly for high-performance substrates. Additionally, stringent quality control standards in semiconductor packaging add to the operational complexity.

Other Challenges

Technological Complexity in Advanced Nodes

As chip designs move to 3nm and below, substrate manufacturers face difficulties in ensuring signal integrity and thermal dissipation, requiring R&D investments to keep pace with evolving chip architectures.

MARKET RESTRAINTS

Regulatory and Environmental Constraints

Stringent environmental regulations on materials used in substrate manufacturing, such as lead-free and halogen-free requirements, limit the use of traditional materials. Compliance with global standards adds costs and restricts substrate innovation.

MARKET OPPORTUNITIES

Expansion in Automotive and AI Applications

The rise of electric vehicles (EVs) and autonomous driving systems presents significant opportunities for the Non-Memory Chip Packaging Substrate Market. Advanced driver-assistance systems (ADAS) and AI inference chips demand high-reliability substrates that can withstand harsh environments while delivering superior performance.

Non-Memory Chip Packaging Substrate Market Trends

Advancements in Heterogeneous Integration Driving Demand

Non-Memory Chip Packaging Substrate Market is experiencing growth due to increasing demand for heterogeneous integration in advanced packaging. As semiconductor manufacturers focus on improving performance while reducing size, substrates for processors, sensors, and RF chips require more sophisticated designs. Major players are developing high-density interconnect (HDI) substrates to accommodate complex multi-chip modules.

Other Trends

Shift Toward Advanced Materials

Manufacturers are transitioning from conventional bismaleimide triazine (BT) resins to advanced materials like Ajinomoto Build-up Film (ABF) for high-performance computing applications. This shift improves thermal stability and signal integrity in logic chip packaging substrates for processors and ASICs.

Regional Manufacturing Capacity Expansion

Key Asian suppliers including Ibiden, Unimicron, and Samsung Electro-Mechanics are expanding production facilities to meet growing demand from consumer electronics and automotive sectors. The U.S. and Europe are seeing increased investments in domestic substrate manufacturing to reduce supply chain dependencies.

Other Trends

5G Infrastructure Driving RF Substrate Innovation

The rollout of 5G networks is accelerating demand for specialized communication chip packaging substrates with improved high-frequency performance. Substrate manufacturers are developing low-loss materials and fine-pitch interconnection technologies for mmWave applications.

Automotive Applications Creating New Opportunities

The automotive semiconductor market is driving innovation in sensor chip packaging substrates, particularly for ADAS and electrification systems. Requirements for high reliability and thermal performance are prompting developments in ceramic and organic-based substrate solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Asian Dominance in Non-Memory Chip Packaging Substrate Production

Global Non-Memory Chip Packaging Substrate Market is characterized by strong Asian dominance, with Japanese and South Korean manufacturers collectively holding over 60% market share. Ibiden leads the sector with its advanced FCBGA and FCCSP substrate technologies, particularly for high-performance computing applications. Samsung Electro-Mechanics and LG Innotek maintain strong positions with vertically integrated ecosystems catering to semiconductor giants. The market shows moderate consolidation, with the top five players accounting for approximately 45-50% of global revenue.

Taiwanese manufacturers like Unimicron and ASE Group are gaining traction through strategic partnerships with foundries, while Chinese players such as Hemei Jingyi Technology are expanding capacity rapidly through government-supported initiatives. Smaller specialty manufacturers like Shinko and Simmtech compete through technological differentiation in niche applications like automotive sensors and RF modules. Recent capacity expansions in Southeast Asia are reshaping regional supply chain dynamics.

List of Key Non-Memory Chip Packaging Substrate Companies Profiled

- Ibiden

- Shinko

- Kyocera

- LG Innotek

- Samsung Electro-Mechanics

- AT&S

- ASE Group

- Unimicron

- KINSUS

- Hemei Jingyi Technology

- NanYa PCB

- Simmtech

- Daeduck Electronics

- Triumph Electronics

- Zhen Ding Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Logic Chip Packaging Substrate dominates due to widespread use in processors and computing applications. Key drivers include:

|

| By Application |

|

Consumer Electronics leads application segments with robust growth prospects:

|

| By End User |

|

Semiconductor Manufacturers represent the primary customer base:

|

| By Material Type |

|

Organic Substrates maintain dominant position due to:

|

| By Technology |

|

FC-BGA (Flip Chip Ball Grid Array) remains leading technology because:

|

Regional Analysis: Asia-Pacific Non-Memory Chip Packaging Substrate Market

Taiwan’s packaging substrate market is propelled by TSMC’s advanced packaging requirements, particularly for CoWoS and InFO technologies. Local substrate manufacturers have developed specialized capabilities to support 2.5D/3D IC integration, creating a competitive moat against other regions in high-end substrates.

China has aggressively expanded its substrate manufacturing base through state-backed initiatives, focusing on reducing import dependence. Domestic players are making rapid progress in ABF substrate production, though still lagging in cutting-edge technologies required for advanced AI processors.

Japanese manufacturers maintain dominance in critical substrate materials like BT and ABF, supplying global packaging ecosystem. Their focus on next-generation materials for high-frequency and thermal management applications gives them pricing power in premium substrate segments.

Samsung and SK Hynix are driving South Korea’s shift toward high-value logic packaging substrates, leveraging their memory packaging expertise. The country is making strategic investments in substrate technologies suitable for AI accelerators and automotive semiconductors.

North America

North America’s non-memory chip packaging substrate market is innovation-driven, led by U.S. fabless companies and IDMs demanding cutting-edge packaging solutions. The region specializes in high-performance substrates for AI/ML accelerators and data center applications, with strong university-industry collaboration in advanced packaging R&D. However, limited domestic manufacturing capacity creates dependency on Asian suppliers, prompting government initiatives to rebuild substrate supply chains through CHIPS Act funding.

Europe

Europe maintains niche strengths in automotive and industrial substrate technologies, with German and Dutch companies leading in reliability-focused solutions. The region benefits from strong automotive semiconductor demand but faces challenges in scaling substrate production to match Asian competitors. Recent investments in organic substrate R&D aim to capitalize on Europe’s strengths in precision engineering and material science.

Middle East & Africa

The region is emerging as a potential substrate manufacturing hub with strategic investments in semiconductor infrastructure. Countries like Israel are developing specialized substrate capabilities for defense and telecom applications, while UAE’s investment in advanced packaging aims to diversify its technology sector. However, the ecosystem remains in early development stages compared to established markets.

South America

South America’s non-memory chip packaging substrate market remains nascent, with Brazil showing initial developments in substrate manufacturing for consumer electronics. The region primarily serves as an end-market rather than production base, importing most advanced packaging substrates from Asia to support local EMS and OEM operations.

Report Scope

This market research report provides a comprehensive analysis of the Non-Memory Chip Packaging Substrate Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Non-Memory Chip Packaging Substrate Market?

-> Non-Memory Chip Packaging Substrate Market size was valued at USD 8.42 billion in 2025. The market is projected to grow from USD 9.15 billion in 2026 to USD 14.87 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Which key companies operate in Non-Memory Chip Packaging Substrate Market?

-> Key players include Ibiden, Shinko, kyocera, LGInnotek, Samsung Electro Mechanics, AT&S, ASE Group, Unimicron, KINSUS, Hemei Jingyi Technology, among others. In 2025, the global top five players had a share approximately % in terms of revenue.

What are the key growth drivers?

-> Key growth drivers include increasing demand for processors and sensors, advancements in semiconductor packaging technologies, and growing applications in consumer electronics and communication equipment.

Which region dominates the market?

-> Asia is the dominant market, with China projected to reach USD million by 2034, while the U.S. market size is estimated at USD million in 2025.

What are the emerging trends?

-> Emerging trends include advancements in substrate materials, miniaturization of chip packages, and increasing adoption of advanced packaging technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...