Industrial Wireless Market Insights

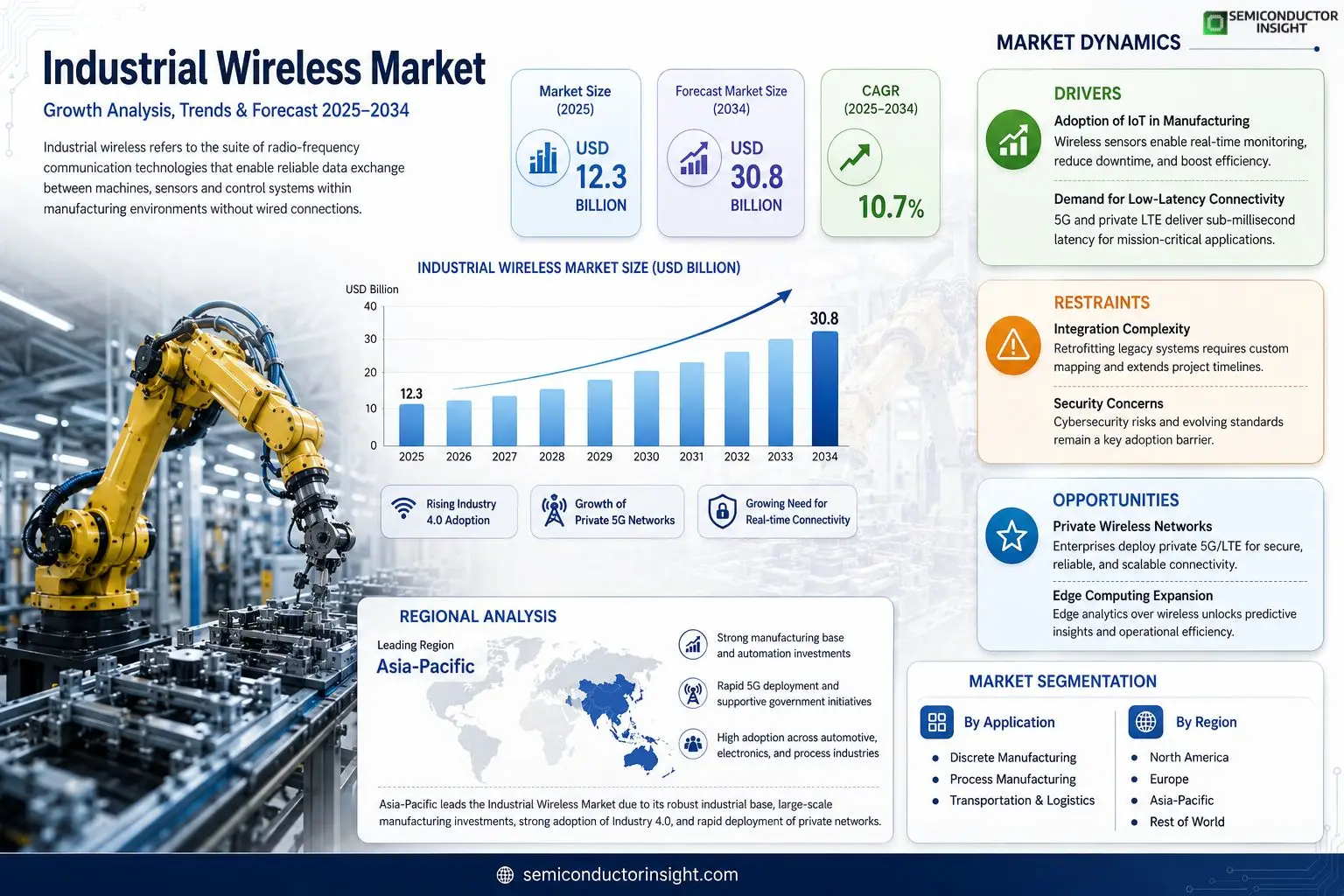

industrial wireless market size was valued at USD 12.3 billion in 2025. The market is projected to grow from USD 12.3 billion in 2025 to USD 30.8 billion by 2034, exhibiting a CAGR of 10.7% during the forecast period.

Industrial wireless refers to the suite of radio‑frequency communication technologies,such as Wi‑Fi 6/6E, Bluetooth Low Energy, Zigbee, LoRaWAN, private LTE and emerging 5G,that enable reliable data exchange between machines, sensors and control systems within manufacturing environments without wired connections.The market is experiencing rapid growth because manufacturers are accelerating Industry 4.0 initiatives, seeking real‑time monitoring and predictive maintenance while reducing cabling costs; however, challenges remain around spectrum congestion and security standards. Furthermore, the rollout of private‑cellular networks and increasing demand for edge computing are driving adoption across sectors like automotive assembly and process industries. Key players such as Siemens AG, Cisco Systems Inc., Huawei Technologies Co., Schneider Electric SE and Rockwell Automation are expanding their portfolios through strategic partnerships and product innovations.

MARKET DRIVERS

Adoption of IoT in Manufacturing

Industrial Wireless Market is being propelled by the rapid integration of Internet of Things (IoT) devices on factory floors. Manufacturers are leveraging wireless sensors to monitor equipment health, reduce downtime, and improve production efficiency. This digital transformation creates a robust demand for reliable, low‑power wireless solutions.

Demand for Low‑Latency Connectivity

Real‑time control systems in automation require sub‑millisecond latency, which traditional wired networks struggle to deliver at scale. Advances in 5G and private LTE are enabling Industrial Wireless Market to meet these exacting performance standards, encouraging further investment from heavy‑industry sectors.

➤ “Wireless reliability now rivals wired in most mission‑critical applications, a shift that reshapes plant architecture.”

As sustainability targets tighten, wireless solutions reduce material waste and energy consumption associated with cabling. Companies that adopt these technologies report up to 15% lower operational costs, reinforcing the growth trajectory of Industrial Wireless Market.

MARKET CHALLENGES

Integration Complexity

Deploying wireless networks alongside legacy equipment often requires extensive retrofitting and custom protocol mapping, which can delay projects and inflate budgets. This complexity is a notable hurdle for many traditional manufacturers.

Other Challenges

Regulatory Barriers

Stringent spectrum licensing and safety regulations in regions such as Europe and North America create additional compliance costs, limiting rapid rollout of new wireless infrastructures.

MARKET RESTRAINTS

High Initial Capital Expenditure

The upfront investment for robust industrial wireless infrastructure,including gateways, antennas, and network management platforms,can be prohibitive for small‑ and medium‑sized enterprises. Although total cost of ownership improves over time, the initial spend remains a key restraint for market adoption.

MARKET OPPORTUNITIES

Edge Computing Integration

Combining edge computing with wireless connectivity opens new use cases such as predictive maintenance and AI‑driven quality control. By processing data locally, manufacturers can reduce latency and bandwidth requirements, presenting a compelling growth avenue for Industrial Wireless Market.

Industrial Wireless Market Trends

Accelerating Industry 4.0 Adoption

Manufacturers are expanding their use of radio‑frequency communication technologies such as Wi‑Fi 6/6E, Bluetooth Low Energy, Zigbee, LoRaWAN, private LTE and emerging 5G to support real‑time monitoring, predictive maintenance, and flexible production lines. The shift away from wired connections reduces installation costs and enables faster reconfiguration of equipment, which aligns with the strategic objectives of Industrial Wireless Market. Companies are also integrating these wireless solutions with cloud‑native analytics platforms, allowing instant data insight and tighter control loops across the shop floor.

Other Trends

Spectrum Congestion and Security Standards

As more devices connect wirelessly, spectrum congestion becomes a tangible risk, especially in dense factory environments where multiple protocols operate concurrently. Security standards are evolving to address vulnerabilities; encryption, device authentication, and network segmentation are being mandated by leading equipment vendors. Industrial Wireless Market is responding with tighter certification processes and collaborative industry forums that promote interoperable and secure solutions.

Rise of Private Cellular Networks and Edge Computing

Private‑cellular networks are gaining traction because they offer dedicated spectrum, higher reliability, and deterministic latency – attributes essential for mission‑critical automation. At the same time, edge computing nodes are being deployed to process sensor data locally, reducing bandwidth demand and latency. This combination accelerates adoption in sectors such as automotive assembly and process industries, where immediate decision‑making is required. Leading players including Siemens, Cisco, Huawei, Schneider Electric, and Rockwell Automation are expanding portfolios through strategic partnerships, introducing modular hardware, and offering managed services that simplify deployment for end users.Overall, Industrial Wireless Market is moving toward a more integrated ecosystem where wireless connectivity, security, and edge intelligence coexist to enable the next generation of smart factories. Continuous innovation, together with clear regulatory guidance, is expected to sustain the momentum while addressing the operational challenges that arise from increasingly complex wireless environments.

COMPETITIVE LANDSCAPEKey Industry Players

Industrial Wireless Market Competitive Landscape Overview

The industrial wireless segment is presently dominated by a handful of multinational technology integrators that combine deep automation expertise with advanced radio‑frequency portfolios. Siemens AG leads the space by leveraging its Digital Industries division to embed Wi‑Fi 6, private LTE and emerging 5G into factory automation suites, while Cisco Systems extends its networking heritage into rugged, edge‑ready wireless gateways for high‑throughput data collection. Huawei Technologies contributes a vertically integrated chipset and end‑to‑end private‑cellular solutions that accelerate deployment timelines for large‑scale plants. Schneider Electric and Rockwell Automation complement the ecosystem with safety‑rated IoT gateways and edge controllers that tie wireless mesh networks to energy‑management platforms. These leaders shape market structure through strategic acquisitions, joint ventures with telecom operators, and extensive service networks that lock in long‑term contracts alongside tier‑1 OEMs.Niche yet influential participants expand specialization across verticals and emerging protocols. Honeywell and Emerson focus on process‑industry reliability, offering Bluetooth Low Energy and Zigbee modules hardened for hazardous environments. ABB and General Electric (GE Digital) drive private‑cellular adoption in heavy‑machinery contexts, while Nokia and Ericsson supply carrier‑grade 5G infrastructure tailored for low‑latency control loops. Intel and Qualcomm deliver semiconductor‑level innovations that underpin edge AI analytics, and Bosch adds sensor‑fusion capabilities that enrich data richness for predictive maintenance. Collectively, these companies inject competitive pressure, diversify technology choices, and foster rapid standard‑setting that benefits end‑users across automotive, chemical, and discrete manufacturing sectors.

List of Key Industrial Wireless Companies Profiled

- Siemens AG

- Cisco Systems Inc.

- Huawei Technologies Co.

- Schneider Electric SE

- Rockwell Automation

- Honeywell International Inc.

- Emerson Electric Co.

- ABB Ltd.

- General Electric (GE Digital)

- Nokia Corporation

- Ericsson AB

- Intel Corporation

- Qualcomm Inc.

- Bosch Group

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Private LTE & 5G is emerging as the dominant technological choice for high‑throughput industrial environments.

|

| By Application |

|

Predictive Maintenance drives the most compelling value proposition for industrial wireless solutions.

|

| By End User |

|

Automotive Assembly stands out as a leading end‑user segment because of its intensive automation and need for ultra‑reliable low‑latency communication.

|

| By Network Architecture |

|

Mesh Networks are gaining traction as the preferred architecture for sprawling factory floors.

|

| By Deployment Scenario |

|

Edge‑Centric Data Processing is the most impactful scenario for industrial wireless deployments.

|

Regional Analysis: North America

United States

The manufacturing sector is a primary adopter of industrial wireless technologies, leveraging them for real-time monitoring of production lines, predictive maintenance, and improved inventory management.

The demand for wireless sensors and gateways that can withstand harsh industrial conditions is particularly strong in this segment.

Industrial wireless plays a crucial role in optimizing logistics and supply chain operations, enabling real-time tracking of assets, improved route planning, and enhanced warehouse management.

The use of RFID and Bluetooth Low Energy (BLE) technologies is gaining traction for inventory visibility and asset tracking.

The energy and utilities sector is deploying industrial wireless solutions for remote monitoring of infrastructure, predictive maintenance of equipment, and improved grid management.

Wireless sensor networks are used to monitor pipelines, power grids, and other critical assets.

Healthcare facilities are leveraging industrial wireless for asset tracking, patient monitoring, and environmental control systems.

Wireless medical devices and sensors are increasingly being used to improve patient care and operational efficiency.

Europe

Europe is witnessing sustained growth in its industrial wireless market, propelled by stringent environmental regulations, a strong focus on energy efficiency, and the increasing adoption of Industry 4.0 principles. The European Union’s initiatives promoting digitalization and smart manufacturing are further driving demand. Countries like Germany, the United Kingdom, and France are leading the way in adopting industrial wireless technologies across various sectors. The emphasis on data security and privacy remains a key consideration in the European market, influencing the selection of wireless solutions. The development of 5G infrastructure across Europe is expected to accelerate the adoption of more advanced industrial wireless applications. Sustainability initiatives are also influencing investment in wireless technologies that can optimize energy consumption and reduce waste. The market is characterized by a strong emphasis on interoperability and open standards.

Asia-Pacific

The Asia-Pacific region represents the fastest-growing market for industrial wireless, driven by rapid industrialization, increasing manufacturing output, and government initiatives promoting technological advancement. China, Japan, and South Korea are key contributors to this growth. The region’s strong focus on automation and smart manufacturing is fueling the demand for wireless solutions across industries like automotive, electronics, and consumer goods. The availability of affordable wireless technologies and the increasing adoption of IoT devices are further contributing to market expansion. However, concerns around data security and cybersecurity pose a challenge to the growth of industrial wireless in the region. The adoption of private 5G networks is gaining momentum in Asia-Pacific.

South America

South America is an emerging market for industrial wireless, with significant potential for growth. The increasing focus on improving operational efficiency in sectors like mining, agriculture, and logistics is driving demand for wireless solutions. Brazil and Argentina are the leading markets in the region. Challenges include limited infrastructure and high import duties, which can hinder market growth. However, the increasing availability of affordable wireless technologies and the growing adoption of IoT are expected to drive future growth. The mining sector, in particular, is actively exploring the use of industrial wireless for remote monitoring and control.

Middle East & Africa

The Middle East and Africa region exhibits moderate growth potential for industrial wireless, with opportunities in sectors like oil and gas, construction, and logistics. The increasing investment in infrastructure projects and the growing adoption of smart city initiatives are driving demand. Countries like Saudi Arabia, the United Arab Emirates, and South Africa are leading the way in adopting industrial wireless technologies. Challenges include limited technological expertise and high upfront costs. However, government initiatives promoting digitalization and industrial diversification are expected to drive future growth. The oil and gas sector is a key adopter of wireless solutions for remote monitoring of pipelines and equipment.

Report Scope

This market research report provides a comprehensive analysis of the Industrial Wireless Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand‑supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Industrial Wireless Market?

-> Industrial Wireless Market was valued at USD 12.3 billion in 2025 and is expected to reach USD 30.8 billion by 2034, reflecting a CAGR of 10.7% during the forecast period.

Which key companies operate in Industrial Wireless Market?

-> Key players include Siemens AG, Cisco Systems Inc., Huawei Technologies Co., Schneider Electric SE, and Rockwell Automation.

What are the key growth drivers?

-> Key growth drivers include accelerated Industry 4.0 adoption, real‑time monitoring, predictive maintenance, reduction of cabling costs, rollout of private‑cellular networks, and increasing demand for edge computing.

Which region dominates the market?

-> Not disclosed in the reference.

What are the emerging trends?

-> Emerging trends include adoption of Wi‑Fi 6/6E, Bluetooth Low Energy, Zigbee, LoRaWAN, private LTE and 5G, integration with edge computing and AI/IoT for smarter industrial operations.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...