MARKET INSIGHTS

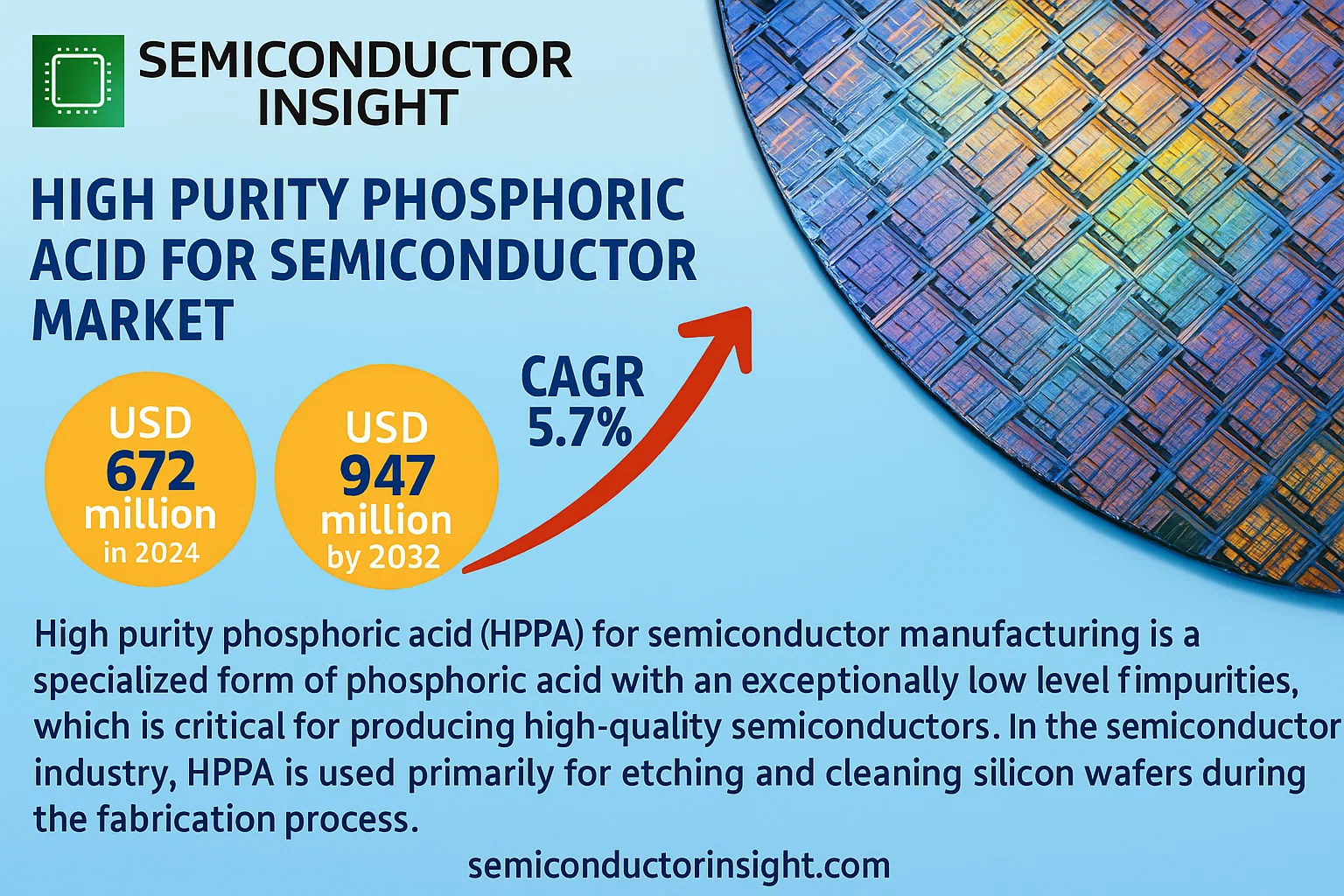

Global High Purity Phosphoric Acid for Semiconductor Market was valued at USD 672 million in 2024 and is projected to reach USD 947 million by 2032, exhibiting a CAGR of 5.7% during the forecast period.

High purity phosphoric acid (HPPA) for semiconductor manufacturing is a specialized form of phosphoric acid with an exceptionally low level of impurities, which is critical for producing high-quality semiconductors. In the semiconductor industry, HPPA is used primarily for etching and cleaning silicon wafers during the fabrication process. The purity of the acid ensures that no unwanted contaminants interfere with the delicate processes involved in creating microelectronic devices. This high level of purity helps maintain the integrity and performance of semiconductor components, which are essential for the functioning of various electronic devices.

The high purity phosphoric acid (HPPA) market for semiconductor applications is witnessing significant growth, driven by the expanding semiconductor industry and the increasing demand for advanced electronic devices. As technology continues to advance, there is a growing need for smaller, more powerful, and efficient semiconductor components, which in turn drives demand for HPPA. The high precision required in semiconductor manufacturing necessitates the use of HPPA to ensure the cleanliness and integrity of silicon wafers, making it a critical component in the production process. This trend is further supported by the ongoing development of new semiconductor technologies and the proliferation of electronic devices across various sectors, including consumer electronics, automotive, and telecommunications.

However, the market for HPPA also faces challenges, such as the high cost of production and the need for stringent quality control measures. The production of HPPA involves sophisticated processes to achieve the required purity levels, which can be resource-intensive and expensive. Additionally, fluctuations in the supply of raw materials and regulatory constraints on environmental impacts may affect market dynamics. Despite these challenges, ongoing innovations in production technologies and increasing investments in semiconductor research and development are expected to sustain the growth of the HPPA market. As the demand for cutting-edge electronic devices continues to rise, the importance of high purity phosphoric acid in maintaining the quality and performance of semiconductor products will likely remain strong.

We have surveyed the High Purity Phosphoric Acid for Semiconductor manufacturers, suppliers, distributors, and industry experts on this industry, involving the sales, revenue, demand, price change, product type, recent development and plan, industry trends, drivers, challenges, obstacles, and potential risks. This report aims to provide a comprehensive presentation of the global market for High Purity Phosphoric Acid for Semiconductor, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding High Purity Phosphoric Acid for Semiconductor.

MARKET DRIVERS

Escalating Global Semiconductor Demand

The relentless expansion of the digital economy, driven by artificial intelligence, 5G infrastructure, Internet of Things (IoT) devices, and electric vehicles, continues to fuel unprecedented demand for semiconductors. High Purity Phosphoric Acid (HPPA) is an essential wet chemical used in the etching and cleaning of silicon wafers during chip fabrication. As semiconductor manufacturers ramp up production capacity to meet this demand, the consumption of critical process chemicals like HPPA is increasing proportionally. The construction of new fabrication plants worldwide directly translates to higher volume requirements for ultra-pure chemicals.

Advancements in Semiconductor Manufacturing Nodes

The industry’s persistent march toward smaller and more complex semiconductor nodes, such as 3nm and 2nm processes, demands etchants with exceptional purity and precision. Impurities in process chemicals can cause catastrophic defects at these scales. HPPA used for selectively etching silicon nitride over silicon oxide must meet specifications with metallic impurity levels in the parts-per-trillion (ppt) range. This technological progression acts as a powerful driver, compelling suppliers to develop and provide ever-higher purity grades, thereby sustaining market growth.

➤ The global market for HPPA in semiconductors is projected to grow at a CAGR of approximately 6-8% over the next five years, closely mirroring the expansion of the advanced logic and memory chip sectors.

Furthermore, the increasing complexity of 3D NAND flash memory and DRAM chips requires more processing steps, many of which utilize HPPA for cleaning and planarization. This multi-patterning and multi-stacking trend effectively increases the consumption of HPPA per wafer, providing a steady, structural driver for the market beyond simple volume increases.

MARKET CHALLENGES

Stringent Purity and Consistency Requirements

Producing HPPA that consistently meets the ultra-high purity standards of leading-edge semiconductor fabs is a significant technical challenge. Even minute traces of metallic ions or particulate contaminants can drastically reduce chip yields. Manufacturers must invest heavily in advanced purification technologies, sophisticated filtration systems, and controlled production environments. Maintaining batch-to-batch consistency is equally critical, as variability can disrupt sensitive fabrication processes, leading to costly production halts and qualification delays with customers.

Other Challenges

Supply Chain and Raw Material Volatility

The production of HPPA is dependent on the supply and pricing of thermal phosphoric acid or elemental phosphorus, which are subject to geopolitical, logistical, and energy-cost fluctuations. Any disruption in this upstream supply chain can directly impact HPPA availability and cost stability for semiconductor manufacturers, who operate on tight just-in-time inventory models.

Intense Price Pressure and Competition

The market is characterized by strong competition among a few key global chemical suppliers. Semiconductor manufacturers exert significant pressure to reduce the cost-per-chemical, which squeezes profit margins for HPPA producers. This economic pressure challenges suppliers to continually optimize their manufacturing processes without compromising on the critical purity parameters.

MARKET RESTRAINTS

High Capital and Operational Expenditures

The establishment of a production facility capable of manufacturing electronic-grade HPPA requires immense capital investment in specialized equipment, cleanroom infrastructure, and analytical instruments for quality control. The operational costs are also substantial, encompassing high-energy consumption for purification processes, expensive raw materials, and rigorous testing protocols. These significant financial barriers limit the entry of new players and can restrain the rapid expansion of production capacity to meet sudden demand surges.

Environmental and Regulatory Hurdles

The production and handling of phosphoric acid are subject to stringent environmental regulations concerning wastewater discharge, chemical storage, and worker safety. Compliance with evolving global regulations, such as REACH in Europe and TSCA in the United States, adds complexity and cost. The need for sustainable and environmentally responsible manufacturing processes is becoming a key factor, potentially restraining operations for producers who cannot adapt to these stricter standards.

MARKET OPPORTUNITIES

Expansion in the Asia-Pacific Region

The geographical shift of semiconductor manufacturing to the Asia-Pacific region, particularly in Taiwan, South Korea, China, and Southeast Asia, presents a monumental growth opportunity. The concentration of new mega-fabs in this region creates a localized and booming demand for high-purity chemicals. Establishing production facilities or strengthening supply chain partnerships within Asia-Pacific allows HPPA suppliers to reduce logistics costs, improve responsiveness, and secure long-term supply contracts with major foundries and memory chip makers.

Development of Next-Generation Formulations

As semiconductor architectures evolve beyond traditional FinFETs to structures like Gate-All-Around (GAA) and complementary field-effect transistors (CFETs), new etching challenges emerge. This creates an opportunity for innovative suppliers to develop specialized, next-generation HPPA formulations with enhanced selectivity, lower defectivity, and compatibility with novel materials. Pioneering such tailored solutions can allow companies to capture premium market segments and establish strong technological leadership.

Circular Economy and Recycling Initiatives

There is a growing emphasis on sustainability within the semiconductor industry. Opportunities exist for companies to develop efficient closed-loop recycling and reprocessing systems for spent HPPA and other wet chemicals. By purifying and re-introducing recovered acid back into the manufacturing process, suppliers can offer more sustainable solutions, reduce waste disposal costs for fabs, and create a compelling value proposition aligned with corporate environmental goals.

High Purity Phosphoric Acid for Semiconductor Market Trends

Sustained Market Expansion Driven by Core Industry Demand

The global High Purity Phosphoric Acid (HPPA) for Semiconductor market, valued at $672 million in 2024, is on a steady growth trajectory, projected to reach $947 million by 2032, representing a compound annual growth rate (CAGR) of 5.7%. This growth is fundamentally driven by the relentless expansion of the global semiconductor industry. HPPA is a critical specialty chemical used primarily for etching and cleaning silicon wafers during semiconductor fabrication. Its exceptionally low impurity level is non-negotiable for producing high-performance microelectronic devices, as any contamination can severely compromise the integrity and functionality of the final semiconductor component.

Other Trends

Increasing Diversification by Purity Grade

The market is characterized by segmentation based on purity grades, primarily 0.75, 0.85, and ‘Above 85%’. The demand for higher purity grades (Above 85%) is accelerating, fueled by the manufacturing of advanced nodes and more complex integrated circuits. Each purity grade serves specific applications, with the highest grades reserved for the most sensitive etching processes where nanometer-scale precision is mandatory.

Application-Specific Growth and Regional Dynamics

Application-wise, the market is segmented into Cleaning, Etching, and Others. Etching remains the dominant application, consuming the largest volume of HPPA to define intricate circuit patterns on wafers. Geographically, Asia-Pacific holds the largest market share, a direct result of its concentration of semiconductor fabrication plants, particularly in China, Japan, South Korea, and Taiwan. This regional dominance is expected to continue, supported by massive investments in new semiconductor manufacturing capacity. Key players like Rin Kagaku Kogyo, Arkema, Solvay, and ICL Group are focusing on capacity expansion and technological innovation to meet stringent purity requirements and sustain their competitive positions.

COMPETITIVE LANDSCAPE

Key Industry Players

A concentrated market driven by technical expertise and supply chain integration

The global High Purity Phosphoric Acid (HPPA) market for semiconductors is characterized by a concentrated competitive landscape dominated by a handful of established global chemical giants and specialized electronic materials suppliers. The market leader, Solvay, commands a significant share due to its extensive chemical portfolio, deep R&D capabilities, and strong relationships with major semiconductor fabricators. Arkema and ICL Group are also key global players with substantial production capacities and a focus on high-purity materials for the electronics sector. This market structure is not highly fragmented, as the stringent quality requirements, complex production processes, and need for reliable supply chains create high barriers to entry. Competition is primarily based on product purity, consistency, technical support, and the ability to meet the rigorous specifications demanded by leading semiconductor manufacturers.

Beyond the top-tier players, a cohort of significant niche and regional companies caters to specific geographic markets or application segments. Japanese companies like Rin Kagaku Kogyo and Rasa Industries are prominent, known for their high-quality standards and strong presence in the Asia-Pacific region, which is the largest market for semiconductors. South Korea’s SoulBrain is a critical supplier integrated into the local semiconductor ecosystem. Specialized electronic materials companies such as CMC Materials (now part of Entegris) and Honeywell provide ultra-high-purity chemicals essential for advanced node semiconductor manufacturing. Regional players like China’s Hubei Xingfa Chemicals Group and OCI are expanding their footprint, leveraging local production to serve the growing domestic semiconductor industry. These companies compete by offering tailored solutions, competitive pricing, and robust logistical support.

List of Key High Purity Phosphoric Acid for Semiconductor Companies Profiled

- Solvay

- Arkema

- ICL Group

- CMC Materials (Entegris)

- Rin Kagaku Kogyo

- Rasa Industries

- Honeywell

- Hubei Xingfa Chemicals Group

- OCI

- SoulBrain

- BASF

- KMG Chemicals

- Mitsubishi Chemical Corporation

- Kanto Chemical Co., Inc.

- WD Chemie

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Above 85% Purity remains the dominant segment, driven by the semiconductor industry’s relentless pursuit of ultra-clean manufacturing environments. This higher grade offers superior contamination control, which is absolutely essential for fabricating advanced technology nodes where even minuscule impurities can compromise chip performance and yield. The stringent requirements for producing cutting-edge microprocessors and memory devices create a sustained and growing preference for the highest purity levels available. The segment benefits from continuous technological advancements in purification processes, although achieving this grade involves sophisticated and resource-intensive manufacturing, presenting a significant barrier to entry but solidifying its leadership position. |

| By Application |

|

Etching represents the most critical application segment, as high purity phosphoric acid is indispensable for precisely removing silicon nitride layers without damaging underlying materials during semiconductor fabrication. This application’s dominance is intrinsically linked to the complexity and volume of modern chip manufacturing processes, where precise material removal is a fundamental step. The reliability and selectivity of phosphoric acid in etching are paramount for achieving the fine geometries required in today’s electronic components. As semiconductor designs become more intricate, the demand for high-performance etching solutions that ensure dimensional accuracy and process stability continues to reinforce this segment’s leading role in the market. |

| By End User |

|

Foundries are the leading end-user segment, primarily due to their massive scale of production and their role as specialized manufacturers for a wide range of fabless semiconductor companies. The high-volume nature of foundry operations, coupled with their focus on advanced process technologies for multiple clients, creates a substantial and continuous demand for high purity phosphoric acid. These facilities require consistent, high-quality chemical inputs to maintain high yields and meet the diverse specifications of their customers’ chip designs. The competitive landscape among foundries, which drives the adoption of the latest manufacturing technologies, further solidifies their position as the primary consumers of HPPA. |

| By Technology Node |

|

Leading-Edge Nodes (Below 7nm) constitute the most demanding and high-growth segment. The fabrication of semiconductors at these extremely small scales imposes exceptionally strict requirements on material purity to prevent defects. The consumption of high purity phosphoric acid is particularly intensive in these processes due to the need for flawless etching and cleaning at an atomic level. Innovation in this segment is driven by the development of next-generation chips for applications like artificial intelligence, high-performance computing, and advanced mobile processors, where performance margins are extremely tight, making the quality of process chemicals a critical differentiator. |

| By Supply Chain Position |

|

Direct Supply to Fabs is the predominant model, favored for its ability to ensure supply chain security, consistent quality, and technical support directly from the manufacturer. This segment’s leadership is underpinned by the critical nature of HPPA, where any disruption or variance in quality can lead to significant production losses for semiconductor manufacturers. Long-term partnerships and direct technical collaboration between acid producers and fab operators are common, allowing for customized solutions and rapid response to process changes. The complexity of logistics and the need for stringent handling protocols further reinforce the preference for a streamlined, direct supply chain over more fragmented distribution channels. |

Regional Analysis: High Purity Phosphoric Acid for Semiconductor Market

Asia-Pacific

The concentration of world-leading semiconductor foundries and memory chip manufacturers in countries like Taiwan and South Korea creates a powerful pull for high purity phosphoric acid suppliers. This proximity fosters deep collaboration on product specifications and process integration, ensuring the chemical meets the exacting standards required for leading-edge node production, from wafer cleaning to precise etching applications.

A mature and highly specialized chemical industry exists within the region, with local producers deeply integrated into the semiconductor ecosystem. This allows for responsive supply chains, reduced logistical complexities, and enhanced ability to manage the stringent quality and consistency requirements for ultra-high purity grades essential for preventing defects in nanometer-scale semiconductor devices.

National strategies across the Asia-Pacific, particularly in China, Japan, and South Korea, heavily prioritize semiconductor self-sufficiency and technological leadership. This results in significant government subsidies, tax incentives, and direct investment in both fab construction and the supporting specialty chemicals sector, creating a stable and growing demand environment for high purity phosphoric acid.

The region is a hotbed for research into next-generation semiconductor processes, including advanced packaging and new transistor architectures. This continuous innovation cycle drives the development of new formulations and applications for high purity phosphoric acid, keeping regional suppliers at the cutting edge and tightly coupled with the evolving needs of chipmakers.

North America

North America maintains a significant and technologically advanced market for high purity phosphoric acid, anchored by major semiconductor corporations and specialized fabrication facilities in the United States. The region’s focus is predominantly on high-performance computing, automotive semiconductors, and defense applications, which demand the highest quality grades. A strong regulatory framework ensures stringent quality control and environmental compliance for chemical suppliers. While the manufacturing base is smaller than Asia-Pacific, the presence of leading semiconductor equipment companies and material science research institutions fosters a demand for innovative and ultra-pure chemical solutions, supporting a stable niche market.

Europe

The European market is characterized by a strong emphasis on research, quality, and specific automotive and industrial semiconductor applications. Countries like Germany, France, and Ireland host important R&D centers and fabs that require high purity phosphoric acid for specialized processes. The market benefits from strict EU regulations that prioritize supply chain sustainability and chemical safety, influencing sourcing decisions. Collaboration between automotive OEMs, chemical companies, and research institutes drives demand for tailored high-purity solutions, though the market size is more specialized compared to the leading region.

South America

The market for high purity phosphoric acid in South America is nascent but developing, primarily serving a growing consumer electronics assembly sector and some industrial applications. The region currently relies heavily on imports, as local production capabilities for semiconductor-grade chemicals are limited. However, increasing investment in technology infrastructure and a slowly expanding industrial base present potential for future growth, though it remains a minor player in the global landscape dominated by other regions.

Middle East & Africa

This region represents an emerging market with potential driven by strategic national initiatives to diversify economies beyond traditional sectors. Countries like Saudi Arabia and the UAE are investing in technology and industrial parks that could eventually incorporate semiconductor-related manufacturing. Current demand for high purity phosphoric acid is minimal and primarily linked to electronics imports and minor industrial uses. The market is characterized by long-term potential rather than immediate significant demand, with growth dependent on the success of broader technology adoption plans.

Report Scope

This market research report provides a comprehensive analysis of the High Purity Phosphoric Acid for Semiconductor Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of High Purity Phosphoric Acid for Semiconductor Market?

->High Purity Phosphoric Acid for Semiconductor Market was valued at USD 672 million in 2024 and is projected to reach USD 947 million by 2032, exhibiting a CAGR of 5.7% during the forecast period.

Which key companies operate in High Purity Phosphoric Acid for Semiconductor Market?

-> Key players include Rin Kagaku Kogyo, Arkema, Solvay, ICL Group, CMC Materials, Rasa Industries, Honeywell, Hubei Xingfa Chemicals Group, OCI, and SoulBrain, among others.

What are the key growth drivers?

-> Key growth drivers include the expanding semiconductor industry, increasing demand for advanced electronic devices, and the need for smaller, more powerful, and efficient semiconductor components.

Which region dominates the market?

-> Asia is a key region, with significant market performance from countries including China, Japan, South Korea, and Southeast Asia.

What are the emerging trends?

-> Emerging trends include ongoing innovations in production technologies, increasing investments in semiconductor R&D, and the proliferation of electronic devices across sectors like automotive and telecommunications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...