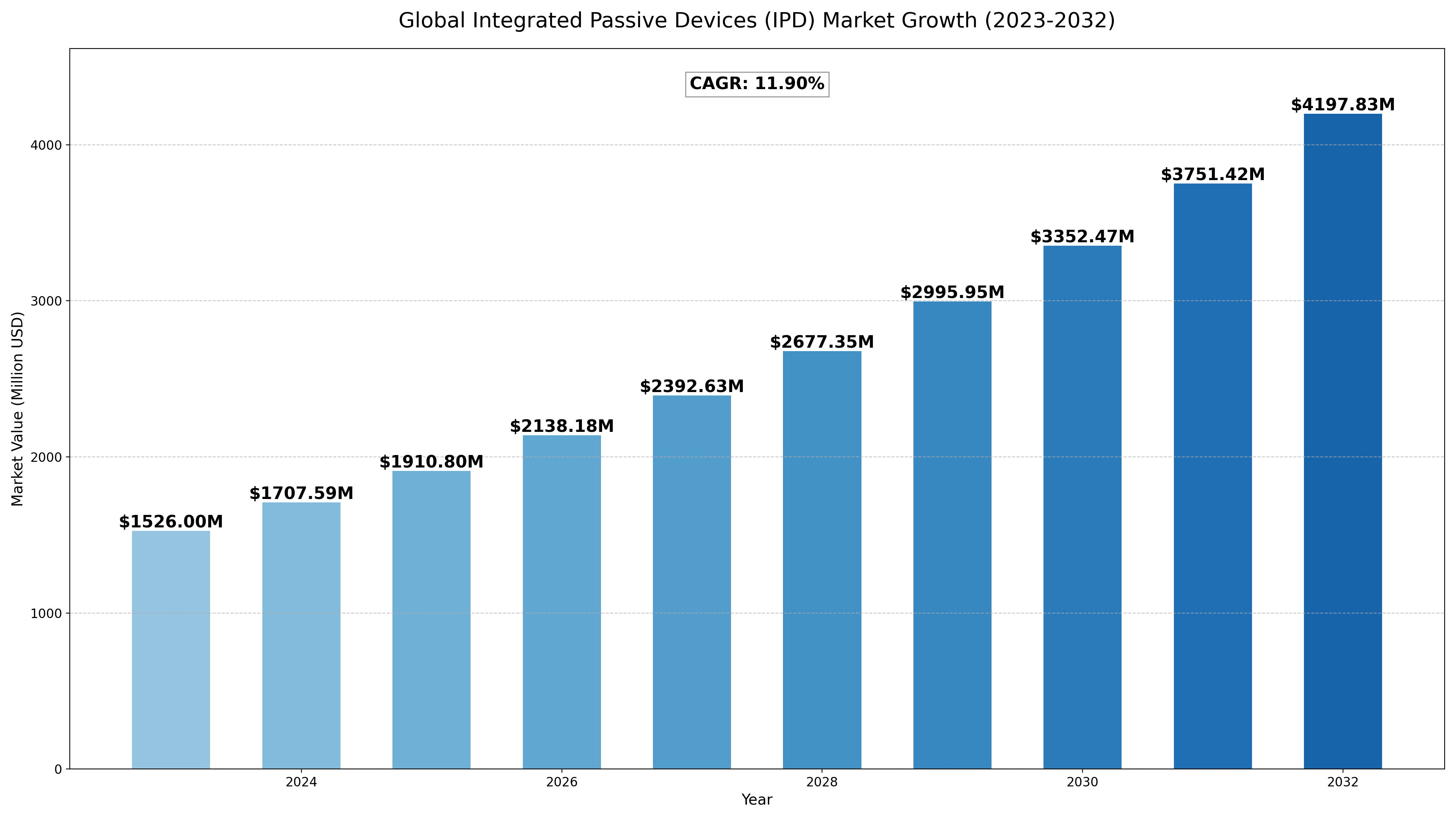

The Global Integrated Passive Devices (Ipd) Market size was estimated at USD 1526 million in 2023 and is projected to reach USD 4197.83 million by 2032, exhibiting a CAGR of 11.90% during the forecast period.

16

16

North America Integrated Passive Devices (Ipd) market size was estimated at USD 482.89 million in 2023, at a CAGR of 10.20% during the forecast period of 2025 through 2032.

Integrated Passive Devices (IPDs) are components that combine passive electronic elements—such as resistors, capacitors, inductors, and filters—into a single, compact package. These devices are commonly used in applications requiring space-saving, high performance, and reliability, such as in RF (radio frequency) systems, telecommunications, and automotive electronics. IPDs help reduce the number of discrete components, leading to improved efficiency and lower production costs.

Report Overview

Integrated Passive Devices (IPD’s) “or Integrated Passive Components (IPC’s) or Embedded Passive Components” are electronic components where resistors (R), capacitors (C), inductors(L)/coils/chokes, microstriplines, impedance matching elements, baluns or any combinations of them are integrated in the same package or on the same substrate. Sometimes integrated passives can also be called as embedded passives and still the difference between integrated and embedded passives is technically unclear.In both cases passives are realised in between dielectric layers or on the same substrate.

This report provides a deep insight into the global Integrated Passive Devices (Ipd) market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Integrated Passive Devices (Ipd) Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Integrated Passive Devices (Ipd) market in any manner.

Global Integrated Passive Devices (Ipd) Market: Market Segmentation Analysis

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- On Semiconductor

- STMicroelectronics

- Murata-IPDiA

- Johanson Technology

- Onchip Devices

- AFSC

- Infineon

- Qorvo

- AVX

- Xpeedic

- EMS and EMI Protection IPD

- RF IPD

- LED Lighting

- Digital & Mixed Signal IPD

- Automotive

- Consumer Electronics

- Healthcare

- Other

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Russia, Italy, Rest of Europe)

- Asia-Pacific (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific)

- South America (Brazil, Argentina, Columbia, Rest of South America)

- The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA)

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Integrated Passive Devices (Ipd) Market

- Overview of the regional outlook of the Integrated Passive Devices (Ipd) Market:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

- Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

- Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

- The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

- Includes in-depth analysis of the market from various perspectives through Porters five forces analysis

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

1. Drivers:

- Miniaturization and Integration in Electronics: One of the major drivers for the growth of the Integrated Passive Devices (IPD) market is the continuous demand for miniaturized electronic components. IPDs offer significant space-saving advantages by integrating passive components like resistors, capacitors, and inductors into a single package, making them ideal for modern electronic systems, especially in mobile devices, wearables, and automotive applications.

- Increased Demand in Consumer Electronics: With the growing popularity of smartphones, tablets, and wearable devices, the demand for smaller and more efficient components is increasing. IPDs are critical for improving performance and reducing space, which is essential in consumer electronics.

- Automotive and Electric Vehicle Adoption: The adoption of advanced driver-assistance systems (ADAS) and electric vehicles (EVs) is another key driver. IPDs play a crucial role in improving the power efficiency, reliability, and compactness of automotive electronics, contributing to the increasing integration of electric and autonomous features in vehicles.

- 5G and Communication Technologies: The rollout of 5G networks and the increasing demand for higher-speed communication technologies are driving the need for IPDs in RF (radio frequency) applications. IPDs help improve signal processing, reduce power consumption, and enhance performance in communication devices, including routers, base stations, and smartphones.

2. Restraints:

- High Manufacturing Costs: One of the major challenges facing the IPD market is the high cost of manufacturing these devices. The integration of multiple passive components in a single package requires advanced packaging technologies, which can increase production costs. This can be a barrier for small-scale manufacturers or for regions where cost constraints are a significant factor.

- Complexity in Design and Customization: While IPDs offer many benefits, designing and customizing these devices for specific applications can be complex. The level of integration required and the need to optimize performance for specific end-use cases can make the design process more challenging and time-consuming.

- Competition from Discrete Components: Despite the benefits of integration, discrete passive components (like individual resistors, capacitors, and inductors) remain popular due to their lower cost, simplicity, and availability. For some applications, particularly where flexibility is needed in component selection, discrete components may still be preferred over integrated alternatives.

3. Opportunities:

- Growth in IoT and Wearable Devices: The Internet of Things (IoT) and wearables market presents significant growth opportunities for IPDs. As IoT devices become more compact and require enhanced energy efficiency, the demand for IPDs in smart home devices, healthcare gadgets, and connected products is expected to rise.

- Adoption of 5G and Next-Generation Communication: The increasing adoption of 5G and next-generation communication systems offers vast opportunities for IPDs in the RF front end of communication systems. As data transmission speeds increase and connectivity becomes more advanced, IPDs are crucial for handling the complex signal processing required.

- Automotive Industry Evolution: The automotive industry’s shift toward electric vehicles (EVs) and autonomous driving systems is another opportunity for IPDs. They are used in various in-car electronic systems such as infotainment, navigation, and ADAS modules, which are increasingly becoming more integrated and efficient.

- Emerging Markets: The growing demand for consumer electronics and smart devices in emerging markets is driving the need for compact and cost-effective solutions, which creates a favorable environment for IPD adoption in these regions.

4. Challenges:

- Technological Challenges in Scaling Production: As IPDs become more integrated and sophisticated, scaling production to meet the growing demand without compromising quality or performance can be challenging. The technological complexity of advanced IPD manufacturing requires significant investments in research and development and high-quality production facilities.

- Supply Chain and Material Shortages: The global supply chain disruptions, particularly in the semiconductor industry, have had a significant impact on the availability of raw materials and production capacity. These shortages may limit the ability of manufacturers to meet the increasing demand for IPDs in various applications.

- Regulatory Challenges: The global market for electronic components is subject to various regulations, including environmental standards and safety certifications. Compliance with these regulations can be challenging for IPD manufacturers, especially when entering new regions with different regulatory frameworks.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...