Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market Insights

Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors market size was valued at USD 4,035 million in 2025. The market is projected to grow from USD 5,318 million in 2026 to USD 23,760 million by 2034, exhibiting a CAGR of 31.8% during the forecast period.

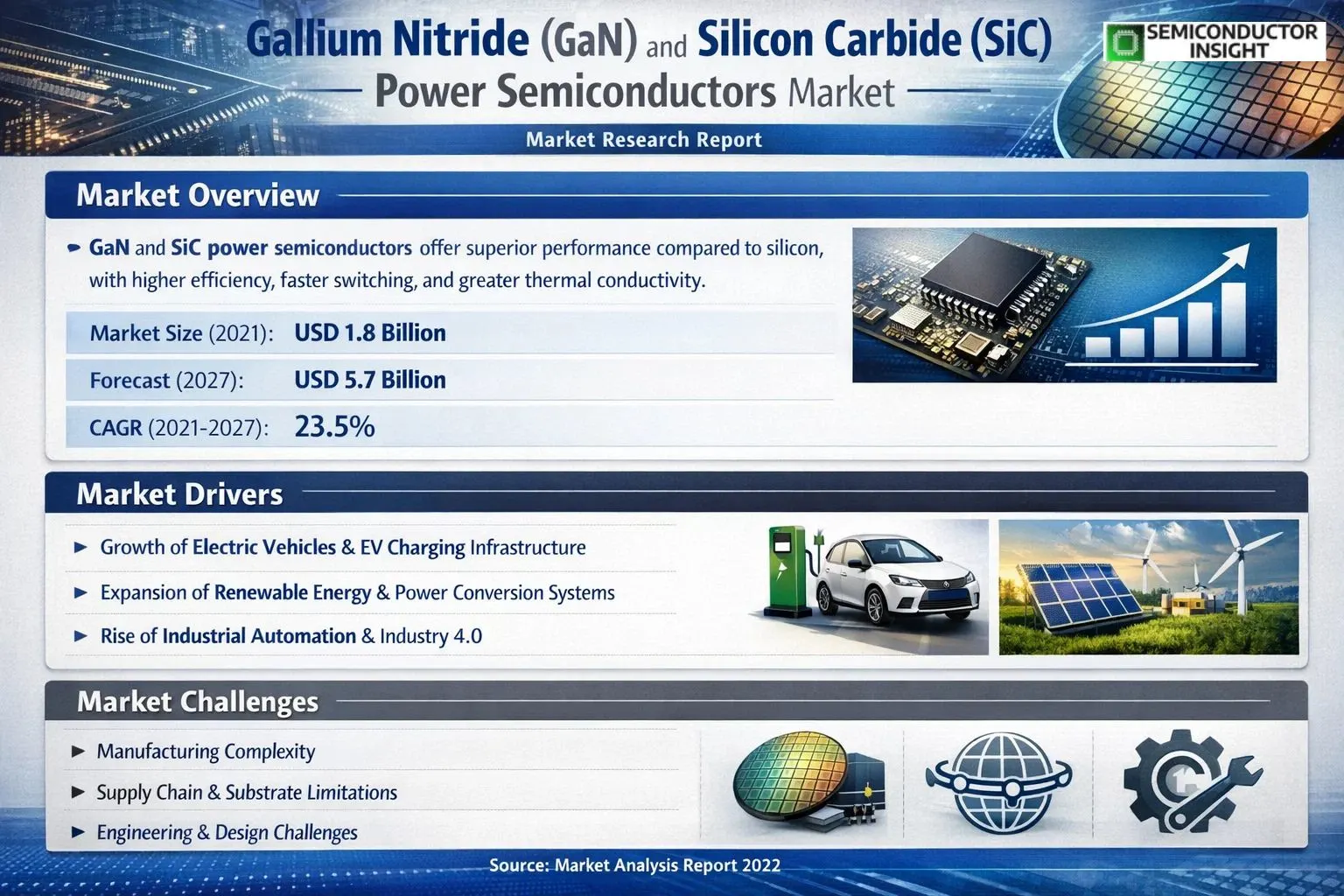

Gallium Nitride (GaN) and Silicon Carbide (SiC) power semiconductors are advanced wide bandgap semiconductor devices engineered to deliver superior performance in high-efficiency power electronics applications. GaN power semiconductors are fabricated using a third-generation semiconductor material that exhibits high electron mobility, high critical breakdown field, and high thermal conductivity, making them particularly effective in high-frequency power conversion, wireless communications, consumer electronics, data centers, and renewable energy systems. SiC power semiconductors, composed of silicon and carbon, offer high electron energy bandgap and electron saturation drift velocity, enabling operation at elevated temperatures and higher electric field strengths. These properties position SiC devices as a preferred solution in power electronics, new energy vehicles, automotive electronics, and industrial applications where thermal performance and reliability under harsh operating conditions are critical.

The market is experiencing robust expansion driven by accelerating adoption of electric vehicles, rapid growth in AI-powered data center infrastructure, and the global transition toward renewable energy grid integration. Infineon Technologies has advanced the GaN segment significantly by developing the world’s first 12-inch power GaN wafer, a milestone that is expected to reduce production costs and improve manufacturing scalability. Meanwhile, the SiC segment continues to benefit from the automotive industry’s shift toward high-efficiency traction inverters and on-board chargers. Leading companies such as Infineon, Wolfspeed (CREE), STMicroelectronics, ROHM, and Onsemi are key participants operating across both GaN and SiC segments with broad and competitive product portfolios.

MARKET DRIVERS

Accelerating Adoption in Electric Vehicles and EV Charging Infrastructure

The rapid global transition toward electric mobility stands as one of the most significant growth catalysts for Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market. Silicon Carbide-based power modules are increasingly being deployed in EV traction inverters, on-board chargers (OBCs), and DC-DC converters, owing to their superior thermal conductivity, high breakdown voltage, and ability to operate efficiently at elevated temperatures. Leading automotive manufacturers across North America, Europe, and Asia-Pacific have integrated SiC MOSFETs into their next-generation EV platforms to maximize driving range and reduce battery pack size. Simultaneously, GaN-based solutions are gaining traction in Level 2 and DC fast-charging infrastructure, where their high switching frequency enables compact, lightweight, and highly efficient charger designs.

Surging Demand from Renewable Energy and Power Conversion Systems

The global expansion of solar photovoltaic installations and wind energy generation systems is driving substantial demand within Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market. Wide-bandgap semiconductors, particularly SiC devices, are being widely adopted in solar inverters, grid-tie systems, and energy storage converters due to their low switching losses and high operating efficiency even at frequencies exceeding traditional silicon-based components. GaN transistors, with their low gate charge and high electron mobility, are increasingly being utilized in high-frequency power conversion stages within renewable energy systems. As countries intensify investments in clean energy infrastructure to meet net-zero commitments, the demand for efficient power electronics built on GaN and SiC platforms is expected to remain robust.

➤ Wide-bandgap semiconductors such as GaN and SiC are enabling system-level efficiency improvements of 2–5% over conventional silicon in high-power applications, translating to significant energy savings at scale across industrial and automotive end-use segments.

Beyond automotive and renewable energy, the industrial sector represents a growing application base for Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market. Motor drives, uninterruptible power supplies (UPS), industrial robotics, and factory automation systems are increasingly leveraging wide-bandgap devices to reduce heat dissipation, minimize cooling requirements, and improve overall system compactness. The ongoing push toward Industry 4.0 and smart manufacturing is further reinforcing demand, as next-generation industrial power systems require components capable of handling higher voltages and switching speeds with minimal energy loss. Government-backed energy efficiency mandates across key markets including the European Union, the United States, and China are additionally compelling industrial equipment manufacturers to transition from conventional silicon to GaN and SiC-based power components.

MARKET CHALLENGES

High Manufacturing Complexity and Elevated Production Costs of Wide-Bandgap Devices

Despite their clear performance advantages, Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market continues to face the persistent challenge of elevated production costs relative to conventional silicon-based alternatives. The fabrication of SiC wafers involves complex crystal growth processes that require precise control of temperature, pressure, and growth rates, making it inherently more expensive and time-intensive than standard silicon wafer production. GaN epitaxial growth on silicon or silicon carbide substrates demands sophisticated deposition techniques and tight process tolerances. These manufacturing complexities result in higher defect densities, lower wafer yields, and consequently, higher per-unit costs that can deter cost-sensitive applications and smaller manufacturers from adopting wide-bandgap power semiconductor solutions at scale.

Other Challenges

Limited Availability of Qualified Substrate Supply and Wafer Scalability

The supply chain for high-quality SiC substrates remains constrained, with only a limited number of producers globally capable of delivering defect-free, large-diameter wafers at commercial volumes. The industry transition from 150mm to 200mm SiC wafers, while underway, is progressing gradually, and the capital investment required for capacity expansion is substantial. For GaN-on-silicon platforms, while substrate availability is comparatively more accessible, achieving the necessary uniformity and crystal quality across large wafer areas remains technically demanding. These substrate availability and scalability constraints create bottlenecks that can limit the pace at which Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market can respond to rapidly growing end-market demand.

Design Complexity and Need for Specialized Engineering Expertise

Transitioning power system designs from silicon to GaN or SiC introduces considerable engineering challenges. Wide-bandgap devices switch at significantly higher frequencies, which introduces new electromagnetic interference (EMI) concerns, gate driver design requirements, and PCB layout sensitivities that engineers accustomed to silicon-based design methodologies may not be fully equipped to address. The shortage of engineers with hands-on experience in wide-bandgap semiconductor design and system integration represents a notable human capital challenge for the industry. This knowledge gap can extend product development timelines and increase non-recurring engineering (NRE) costs, particularly for small and medium-sized enterprises seeking to integrate GaN and SiC solutions into new product lines.

MARKET RESTRAINTS

Price Premium Over Conventional Silicon Power Devices Limiting Mass-Market Penetration

One of the primary restraints affecting Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market is the significant price differential that persists between wide-bandgap devices and their mature silicon counterparts. While the cost gap has been narrowing as manufacturing volumes increase and process technologies mature, GaN and SiC components continue to command a notable premium that restricts their adoption in highly cost-competitive, price-sensitive application segments. Consumer electronics, entry-level industrial equipment, and certain telecommunications applications where performance requirements can still be adequately met by silicon devices represent markets where the economics of wide-bandgap adoption remain challenging. Until price parity with advanced silicon is achieved across more voltage and current ratings, total addressable market expansion will remain partially constrained.

Reliability Concerns and Long-Term Field Performance Validation Gaps

The relative immaturity of GaN and SiC power semiconductor technology compared to decades-proven silicon devices introduces reliability and long-term field performance concerns that act as a restraint within Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market. Mission-critical applications in aerospace, defense, medical equipment, and heavy industrial sectors demand extensive qualification data, failure mode analysis, and long operational lifecycle validation before new semiconductor technologies can be broadly adopted. While SiC has a longer commercial deployment history than GaN in high-power applications, both technologies continue to accumulate the field reliability data necessary to fully satisfy conservative procurement standards. The time required to build this validated performance record and achieve broad qualification acceptance across regulated industries serves as a meaningful restraint on near-term market penetration.

Geopolitical tensions and export control policies affecting semiconductor supply chains represent an additional restraint for Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market. The concentration of certain raw material sources, substrate manufacturing capabilities, and advanced fabrication capacity within specific geographic regions creates supply chain vulnerabilities. Restrictions on the trade of critical semiconductor materials and manufacturing equipment between major economies can introduce procurement uncertainty for system integrators and OEMs reliant on a globally distributed supply base. These geopolitical dynamics are prompting greater emphasis on regional supply chain resilience, which, while strategically prudent, introduces near-term cost and availability pressures that can moderate market growth trajectories.

MARKET OPPORTUNITIES

Expansion into 5G Infrastructure and Data Center Power Management Applications

The global rollout of 5G telecommunications networks and the exponential growth of hyperscale data center capacity present compelling incremental opportunities for Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market. GaN-on-silicon transistors are being increasingly deployed in 5G base station power amplifiers and radio frequency front-end modules, where their high-frequency performance, efficiency, and compact form factor offer distinct advantages over incumbent technologies. In data centers, both GaN and SiC devices are finding growing application in server power supplies, voltage regulators, and uninterruptible power systems, enabling higher power density and reduced energy consumption in facilities where electricity costs and thermal management represent critical operational considerations. The sustained build-out of digital infrastructure globally positions this application vertical as a high-growth avenue for wide-bandgap power semiconductor suppliers.

Government Incentives and Policy-Driven Investments in Domestic Semiconductor Manufacturing

Strategic government initiatives across the United States, European Union, Japan, South Korea, and China aimed at strengthening domestic semiconductor manufacturing capabilities present significant near- and medium-term opportunities for Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market. Legislative frameworks providing direct subsidies, tax incentives, and grants for the establishment of wide-bandgap semiconductor fabrication facilities are accelerating capacity investments that were previously constrained by high capital requirements. These policy-driven investments are expected to improve substrate and device availability, gradually reduce unit production costs, and foster the development of more robust regional supply chains. Ecosystem development programs supporting materials research, packaging innovation, and workforce training are additionally strengthening the foundational infrastructure required to sustain long-term, broad-based growth across the GaN and SiC power semiconductor industry.

The emergence of advanced packaging technologies and system-in-package (SiP) integration methodologies represents a further opportunity set for Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market. Innovations in flip-chip bonding, embedded die packaging, and direct substrate bonding are enabling GaN and SiC power devices to be integrated more closely with gate drivers, passive components, and control circuitry, resulting in power modules with substantially higher power density, lower parasitic inductance, and improved thermal management characteristics. These packaging advances are expanding the performance envelope of wide-bandgap power modules, making them increasingly viable for space-constrained applications in aerospace, medical devices, and next-generation automotive platforms where both performance and form factor are critical design parameters.

MAIN TITLE HERE () Trends

Wide Bandgap Materials Redefining Power Electronics Performanc

Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market is witnessing a significant transformation driven by the accelerating global shift toward energy-efficient power conversion technologies. Both GaN and SiC are wide bandgap semiconductor materials that demonstrate superior electrical and thermal properties compared to conventional silicon-based devices. GaN power semiconductors offer high electron mobility and high-frequency switching capabilities, making them highly suitable for compact, lightweight power systems. SiC power semiconductors, on the other hand, excel in high-temperature and high-voltage environments, particularly in electric vehicle drivetrains, industrial motor drives, and grid-connected renewable energy systems. The convergence of these two advanced material technologies is reshaping the competitive dynamics of the global power semiconductor industry.

Other Trends

Large-Wafer Manufacturing and Cost Reduction Initiatives

A prominent trend in the GaN and SiC power semiconductors space is the industry-wide transition toward larger wafer sizes to improve production efficiency and reduce per-unit costs. Leading manufacturers have begun advancing toward 200mm SiC wafers, a move that significantly increases output volume while lowering fabrication costs. Similarly, in the GaN segment, progress toward 12-inch wafers has been demonstrated by major players, which is expected to further improve economies of scale. These developments are critical in making wide bandgap power semiconductors more commercially accessible across a broader range of end-use applications, including consumer electronics, data centers, and new energy vehicles.

Expanding Role in Electric Vehicles and On-Board Charging

The automotive sector represents one of the most influential application areas driving growth in the GaN and SiC Power Semiconductors Market. SiC-based traction inverters and on-board chargers (OBCs) are increasingly being adopted by electric vehicle manufacturers due to their ability to handle higher voltages and temperatures with greater efficiency. GaN power semiconductors are also gaining traction in OBC designs and AI server power supply units, where high switching frequency and compact form factor are essential. As electric vehicle penetration continues to rise globally, demand for wide bandgap power semiconductors in automotive electronics is expected to remain a key growth catalyst.

Industry Consolidation and Strategic Mergers

The GaN and SiC power semiconductor industry is entering a notable phase of consolidation. Mergers, acquisitions, and strategic partnerships among manufacturers are becoming increasingly common as companies seek to strengthen their supply chains, expand production capacities, and enhance technological capabilities. This consolidation trend is raising industry concentration levels, with established players such as Infineon, Wolfspeed (CREE), STMicroelectronics, ROHM, and Onsemi reinforcing their market positions through vertical integration and expanded wafer fabrication investments.

Rising Demand from Data Centers and Renewable Energy Applications

Beyond automotive, the GaN and SiC Power Semiconductors Market is benefiting from strong demand growth in data center infrastructure and renewable energy grid connections. GaN-based power supplies offer high power density and improved thermal management, making them increasingly preferred for AI server power units and hyperscale data centers. In photovoltaic inverters and energy storage systems, SiC devices are enabling higher conversion efficiencies and reduced system footprint. As governments and enterprises worldwide accelerate investments in clean energy infrastructure, the role of wide bandgap semiconductors in enabling efficient power management across these sectors will continue to expand.

COMPETITIVE LANDSCAPEKey Industry Players

Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market , Competitive Dynamics and Leading Innovators

Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors market is characterized by intense competition among a mix of established semiconductor giants and emerging regional players. Infineon Technologies leads the competitive landscape, having demonstrated its technological prowess by developing the world’s first 12-inch power GaN wafer, enabling significant cost efficiencies and improved production scalability. Wolfspeed (formerly Cree) holds a dominant position in the SiC segment, leveraging its vertically integrated manufacturing capabilities and extensive intellectual property portfolio. STMicroelectronics and ROHM Semiconductor are also prominent forces, maintaining strong footholds across automotive, industrial, and consumer electronics applications. Onsemi has aggressively expanded its SiC capacity to serve the rapidly growing electric vehicle and renewable energy sectors, while Mitsubishi Electric and Fuji Electric continue to command significant market share through their deep expertise in high-power industrial and traction applications. The market, valued at USD 4,035 million in 2025 and projected to reach USD 23,760 million by 2034 at a CAGR of 31.8%, reflects accelerating global demand driven by electric vehicle adoption, AI data center expansion, and energy grid modernization.

Beyond the global leaders, a robust cohort of specialized and regionally significant players is actively shaping the competitive dynamics of the GaN and SiC power semiconductors market. Chinese manufacturers, including BYD Semiconductor, Sanan Optoelectronics, China Resources Microelectronics, Hangzhou Silan Microelectronics, Yangzhou Yangjie Electronic Technology, StarPower Semiconductor, Zhuzhou CRRC Times Electric, BASiC Semiconductor, CETC 55, and CETC 13, are rapidly scaling operations to capture domestic and international demand, supported by strategic government initiatives and increasing localization of the semiconductor supply chain. Global Power Technology and Littelfuse further diversify the competitive field with targeted product offerings for niche industrial and protection applications. As wafer sizes scale toward 200mm for SiC and production volumes ramp for GaN, cost reduction trajectories are expected to intensify competition, prompting ongoing mergers, acquisitions, and strategic partnerships across the industry ecosystem.

List of Key Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Companies Profiled

- Infineon Technologies

- Wolfspeed (CREE)

- ROHM Semiconductor

- STMicroelectronics

- Onsemi

- Mitsubishi Electric Corporation

- Fuji Electric

- Littelfuse

- Global Power Technology

- BASiC Semiconductor

- BYD Semiconductor

- CETC 55

- CETC 13

- Zhuzhou CRRC Times Electric

- Sanan Optoelectronics

- China Resources Microelectronics

- Hangzhou Silan Microelectronics

- Yangzhou Yangjie Electronic Technology

- StarPower Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon Carbide (SiC) Power Semiconductors currently lead the market owing to their well-established presence in high-power, high-temperature industrial and automotive applications.

|

| By Application |

|

New Energy Vehicles (NEV) represent the most transformative and fastest-growing application segment, acting as a primary demand catalyst for both GaN and SiC power semiconductors globally.

|

| By End User |

|

Automotive OEMs & EV Manufacturers stand out as the dominant end-user category, driving the highest volume procurement of wide bandgap power semiconductors across both GaN and SiC technologies.

|

| By Voltage Rating |

|

Medium Voltage (650V – 1200V) devices dominate the market landscape, serving as the cornerstone voltage class across the most commercially significant power electronics applications.

|

| By Device Type |

|

SiC MOSFETs are the leading device type within the broader GaN and SiC power semiconductor ecosystem, underpinning the electrification strategies of automotive and industrial sectors worldwide.

|

Regional Analysis: Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market

Asia-Pacific

China continues to consolidate its leadership in the GaN and SiC Power Semiconductors Market through state-sponsored fabrication facilities and a rapidly maturing domestic device ecosystem. Strategic policy frameworks prioritizing electric vehicle infrastructure and grid modernization are generating sustained demand, positioning Chinese manufacturers as competitive global suppliers of wide-bandgap power semiconductor devices.

Japan maintains a strong competitive edge in precision SiC substrate and device engineering within the Gallium Nitride and Silicon Carbide Power Semiconductors Market. Leading Japanese conglomerates are advancing SiC MOSFET reliability and thermal performance, meeting stringent automotive and industrial power conversion requirements while continuing to expand their intellectual property portfolios in wide-bandgap semiconductor design.

South Korea and Taiwan are emerging as critical contributors to the GaN and SiC Power Semiconductors Market through their advanced foundry capabilities and tight integration with global fabless semiconductor firms. Both economies leverage established semiconductor ecosystems to accelerate GaN-on-Si and SiC device commercialization, especially for fast-charging, data center power supply, and next-generation telecommunications infrastructure applications.

The accelerating deployment of electric vehicles and utility-scale renewable energy installations across Asia-Pacific is generating compelling demand within the Gallium Nitride and Silicon Carbide Power Semiconductors Market. Wide-bandgap devices are critical enablers of high-efficiency onboard chargers, inverters, and bidirectional DC-DC converters, making the region a primary growth engine for power semiconductor innovation through 2034.

North America

North America represents a strategically significant region in Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market, underpinned by a strong base of fabless semiconductor firms, leading research universities, and well-established automotive and defense sectors. The United States government has made wide-bandgap semiconductor development a national priority, channeling investment through initiatives aimed at reducing dependence on foreign-sourced advanced components. Major domestic players are expanding SiC wafer capacity and forming strategic alliances to secure supply chains for the electric vehicle and renewable energy industries. The defense sector’s demand for high-frequency, high-power GaN devices in radar and electronic warfare systems further bolsters regional market growth. Canada also contributes through research initiatives in power electronics, while the region’s favorable regulatory environment for clean energy and EV adoption ensures that demand across automotive, industrial, and grid applications will continue to grow robustly through the 2026–2034 forecast horizon.

Europe

Europe holds a prominent position in Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market, driven by the region’s ambitious carbon neutrality targets, accelerating electric vehicle penetration, and a mature industrial automation landscape. Leading European semiconductor manufacturers and automotive suppliers are investing heavily in SiC-based power modules to support next-generation EV drivetrains and onboard charging systems. The European Union’s strategic autonomy agenda has prompted significant funding toward indigenous wide-bandgap semiconductor production capacity, reducing reliance on Asian and North American sources. Germany, Italy, France, and the Nordic countries are key contributors, with collaborative research ecosystems linking industry and academia to advance GaN and SiC device performance. The region’s stringent energy efficiency standards and grid modernization imperatives further accelerate the adoption of wide-bandgap power semiconductors across renewable energy inverters and smart grid infrastructure applications.

South America

South America is an emerging region in Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market, gradually gaining traction as renewable energy investments and industrial modernization programs gather momentum. Brazil leads the regional landscape, benefiting from its expanding solar and wind energy sectors where GaN and SiC power devices offer compelling efficiency advantages for power conversion equipment. While the region currently accounts for a modest share of global demand, increasing governmental emphasis on electrification of transportation and grid infrastructure upgrades is expected to create meaningful long-term opportunities for wide-bandgap semiconductor adoption. Limited local manufacturing capability means that South America largely relies on imports from Asia-Pacific and North America, but growing technology partnerships and foreign direct investment inflows are gradually laying the groundwork for a more self-sufficient regional power semiconductor ecosystem through the forecast period.

Middle East & Africa

The Middle East and Africa region represents a nascent but steadily evolving participant in Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market. Rapid urbanization, large-scale solar power project deployments, and growing data center infrastructure investments are beginning to generate demand for high-efficiency wide-bandgap power devices across the region. Gulf Cooperation Council countries, particularly Saudi Arabia and the UAE, are channeling significant capital into renewable energy megaprojects where SiC-based inverters deliver tangible performance advantages over conventional silicon solutions. Africa’s expanding electrification programs and the growing relevance of off-grid solar systems also present long-term demand prospects for GaN and SiC semiconductors. While the region faces challenges including limited indigenous semiconductor manufacturing and relatively nascent EV markets, ongoing economic diversification strategies and international technology collaborations position the Middle East and Africa for measured but consistent growth within the global GaN and SiC Power Semiconductors Market through 2034.

Report Scope

This market research report provides a comprehensive analysis of the Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market?

-> Global Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market was valued at USD 4035 million in 2025 and is expected to reach USD 23760 million by 2034, growing at a CAGR of 31.8% during the forecast period.

Which key companies operate in Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market?

-> Key players include Infineon, Wolfspeed (CREE), ROHM, STMicroelectronics, Onsemi, Mitsubishi Electric Corporation, Fuji Electric, Littelfuse, Global Power Technology, BASiC Semiconductor, BYD Semiconductor, CETC 55, CETC 13, Zhuzhou CRRC Times Electric, Sanan Optoelectronics, China Resources Microelectronics, Hangzhou Silan Microelectronics, Yangzhou Yangjie Electronic Technology, and StarPower Semiconductor, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of electric vehicles and on-board chargers (OBC), expansion of AI server power supplies and data centers, growing demand for renewable energy and new energy grid connections, increasing penetration of GaN and SiC devices in consumer electronics and industrial motor drives, and the shift toward larger wafer production (such as 200mm SiC wafers) to reduce costs and improve efficiency.

Which region dominates the market?

-> Asia is a dominant and fast-growing region in Gallium Nitride (GaN) and Silicon Carbide (SiC) Power Semiconductors Market, with key contributors including China, Japan, South Korea, and Southeast Asia, while North America and Europe also hold significant market shares driven by strong automotive, industrial, and renewable energy sectors.

What are the emerging trends?

-> Emerging trends include development of large-size GaN wafers (such as Infineon’s 12-inch power GaN wafer), transition to 200mm SiC wafers for higher capacity and lower cost, rapid penetration of GaN in consumer electronics and AI server power supplies, increasing use of SiC in electric vehicle traction inverters, and growing industry consolidation through mergers and acquisitions among GaN and SiC manufacturers.

Need proxies cheaper than the market?

https://op.wtf

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...