MARKET INSIGHTS

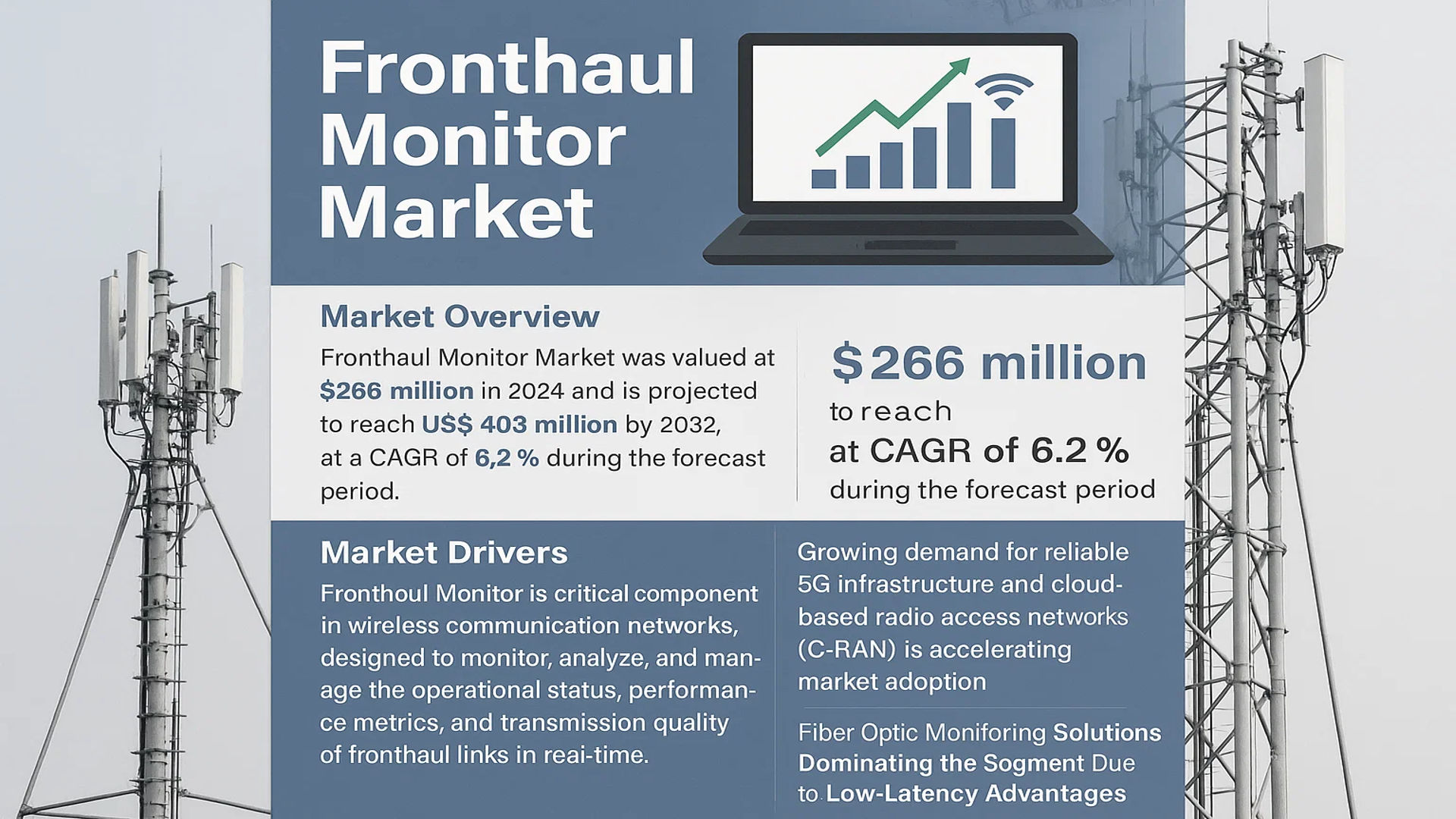

The global Fronthaul Monitor Market was valued at 266 million in 2024 and is projected to reach US$ 403 million by 2032, at a CAGR of 6.2% during the forecast period.

Fronthaul Monitor is a critical component in wireless communication networks, designed to monitor, analyze, and manage the operational status, performance metrics, and transmission quality of fronthaul links in real-time. These high-speed communication channels connect base stations (BS) with centralized (CU) or distributed units (DU), ensuring network stability and efficiency. The growing demand for reliable 5G infrastructure and cloud-based radio access networks (C-RAN) is accelerating market adoption.

The market is primarily driven by increasing investments in 5G deployment, with fiber optic monitoring solutions dominating the segment due to their low-latency advantages. However, challenges such as spectrum scarcity and interoperability issues persist. Key players like Keysight Technologies, VIAVI Solutions, and Nokia are leading innovation, with strategic partnerships enhancing product portfolios. For instance, in Q1 2024, VIAVI expanded its fiber monitoring solutions to support Open RAN architectures, reflecting industry shifts toward network virtualization.

MARKET DYNAMICS

MARKET DRIVERS

Accelerating 5G Network Deployments to Fuel Fronthaul Monitor Demand

The global rollout of 5G networks is creating substantial demand for fronthaul monitoring solutions, as telecommunications providers require robust monitoring systems to ensure the stability and performance of their high-speed fronthaul connections. With over 1.3 billion 5G connections projected worldwide by 2024, network operators are investing heavily in fronthaul infrastructure to support the low-latency, high-bandwidth requirements of next-generation applications. Fronthaul monitors play a critical role in maintaining signal integrity across distributed radio access networks (RANs), which is essential for delivering reliable 5G services. The transition towards cloud RAN (C-RAN) architectures further amplifies this need, as centralized baseband processing requires flawless fronthaul connectivity.

Increasing Fiber Optic Network Investments Driving Market Growth

Telecom operators and governments worldwide are making significant investments in fiber optic infrastructure to meet growing data transmission demands, directly benefiting the fronthaul monitoring market. Fiber optics now account for over 65% of global fronthaul connections due to their superior bandwidth capabilities compared to microwave alternatives. Countries like China and Japan have accelerated fiber deployments under national broadband initiatives, while European nations are modernizing legacy copper networks. These infrastructure upgrades create parallel demand for advanced monitoring systems capable of detecting minute signal degradations and preventing network outages before they impact service quality.

The shift towards open RAN architectures presents another growth vector, as multi-vendor environments require more sophisticated monitoring to maintain interoperability standards. Virtualization of network functions also demands real-time performance monitoring across heterogeneous hardware and software components.

MARKET RESTRAINTS

High Implementation Costs and Complexity Limit Market Penetration

While fronthaul monitoring solutions deliver significant operational benefits, their deployment faces headwinds from substantial capital expenditures and technical complexity. Comprehensive monitoring systems often require specialized hardware probes, software licenses, and skilled personnel for implementation – creating a substantial total cost of ownership that deters smaller network operators. The average price point for enterprise-grade fronthaul monitoring solutions remains nearly 40% higher than traditional backhaul monitoring tools, presenting a significant adoption barrier in cost-sensitive emerging markets.

Standardization Challenges in Multi-Vendor Environments

The lack of universal standards for fronthaul interfaces creates interoperability issues that complicate monitoring system deployments. Different equipment vendors implement proprietary protocols and interface specifications, forcing operators to deploy multiple monitoring solutions or compromise on visibility. This fragmentation is particularly problematic in Open RAN deployments where components from different manufacturers must work in harmony. Monitoring solutions must accommodate various splits (Option 7-2x, Option 8, etc.) and evolving specifications, requiring continuous software updates and hardware reconfigurations that increase operational overhead.

MARKET OPPORTUNITIES

AI-Driven Predictive Maintenance Opening New Frontiers

The integration of artificial intelligence and machine learning into fronthaul monitoring systems presents a transformative opportunity for market growth. Advanced analytics platforms can now predict potential network failures by analyzing patterns in performance metrics, enabling proactive maintenance before outages occur. Leading CSPs report up to 30% reductions in network downtime after implementing AI-powered monitoring solutions. These intelligent systems can automatically correlate data across physical and virtual network layers, providing end-to-end visibility that was previously unattainable with conventional monitoring tools.

Edge Computing Expansion Creating Monitoring Demand

The rapid growth of edge computing infrastructure generates new requirements for distributed fronthaul monitoring capabilities. As latency-sensitive applications drive computing resources closer to end-users, monitoring solutions must adapt to track performance across these decentralized architectures. This includes managing the interplay between mobile fronthaul and emerging edge connections, where high frequency trading, industrial IoT, and autonomous vehicle networks demand nanosecond-level synchronization accuracy.

MARKET CHALLENGES

Shortage of Skilled RF and Optical Engineering Talent

The fronthaul monitoring market faces significant human resource constraints, with a global shortage of engineers skilled in both radio frequency and optical network technologies. This talent gap makes it difficult for both vendors and operators to design, deploy, and maintain sophisticated monitoring systems. With fronthaul networks combining elements of wireless and fiber optic technologies, finding personnel with cross-domain expertise remains challenging, particularly in emerging markets where 5G deployments are expanding rapidly but local training infrastructure lags behind.

Security Vulnerabilities in Fronthaul Networks

Fronthaul links present unique security challenges that monitoring systems must address, including susceptibility to signal interception and jamming attacks. The centralized nature of C-RAN architectures makes fronthaul connections attractive targets for malicious actors, as compromising a single link could impact multiple base stations. Monitoring solutions must balance visibility requirements with security considerations, ensuring comprehensive performance tracking without creating additional attack surfaces. This becomes particularly complex in virtualized environments where traditional hardware-based security measures may not apply.

FRONTHAUL MONITOR MARKET TRENDS

5G Network Expansion Driving Demand for Advanced Fronthaul Monitoring Solutions

The global rollout of 5G networks is significantly boosting the fronthaul monitor market, as telecommunication providers require real-time performance tracking of high-bandwidth connections between distributed radio units and centralized baseband controllers. With 5G deployments growing at a compound annual growth rate (CAGR) of 6.2%, the demand for precision monitoring solutions has accelerated. Fiber optic monitoring solutions currently dominate the market segment, expected to reach significant valuation by 2032 due to their ability to handle massive data throughput with minimal latency. Network operators are particularly focused on monitoring jitter, latency, and packet loss – critical parameters for maintaining quality of service in 5G environments.

Other Trends

Cloud-RAN Architecture Adoption

The transition to Cloud-RAN (C-RAN) architectures is reshaping fronthaul monitoring requirements. As operators centralize baseband processing in cloud data centers, they require more sophisticated monitoring tools to manage the increased complexity of virtualized networks. This shift has led to the development of AI-powered monitoring systems capable of predictive maintenance and automated anomaly detection. The telecommunications industry accounts for the largest share of fronthaul monitor deployments, with major carriers investing heavily in monitoring solutions that can scale with their network expansion plans.

Edge Computing Integration Creating New Monitoring Challenges

The growth of edge computing infrastructure is introducing new fronthaul monitoring considerations. As processing moves closer to end-users to reduce latency, monitoring solutions must now track performance across more distributed network architectures. This has spurred innovation in monitoring equipment, with vendors developing solutions that can provide end-to-end visibility across both traditional fronthaul and emerging midhaul connections. While North America currently leads in market share, Asia-Pacific is showing the fastest growth, driven by rapid 5G deployment in China and other developing markets requiring robust monitoring solutions for their expanding networks.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Market Competition Intensifies as Telecom Leaders Expand Fronthaul Monitoring Capabilities

The global fronthaul monitor market exhibits a moderately concentrated competitive landscape, dominated by established telecommunications and network testing equipment providers. Keysight Technologies currently leads the market with approximately 18% revenue share in 2024, owing to its comprehensive test and measurement solutions tailored for 5G network architectures. Their FieldFox handheld analyzers and PathWave software have become industry standards for fronthaul monitoring applications.

VIAVI Solutions and EXFO follow closely, collectively holding around 22% market share. These companies have strengthened their positions through strategic acquisitions – VIAVI’s purchase of Cobham Wireless’s test and measurement business in 2021 significantly enhanced their 5G capabilities, while EXFO’s recent focus on artificial intelligence-driven monitoring solutions has given them an edge in predictive network maintenance.

The market also features strong competition from Spirent Communications and Anritsu, who are investing heavily in cloud-native monitoring solutions. Spirent’s recent launch of their VisionWorks 2.0 platform addresses critical challenges in O-RAN fronthaul monitoring, while Anritsu’s MP1900A signal quality analyzer continues to gain traction among network equipment manufacturers.

Emerging players like Artiza Networks and Xena Networks are making notable inroads by specializing in high-density testing solutions for massive MIMO deployments. These smaller but focused companies are forcing industry leaders to accelerate their innovation cycles through competitive pricing and customization offerings.

List of Leading Fronthaul Monitor Solution Providers

- Keysight Technologies (U.S.)

- VIAVI Solutions (U.S.)

- EXFO (Canada)

- Spirent Communications (U.K.)

- Anritsu Corporation (Japan)

- Nokia (Finland)

- Huawei (China)

- PRIMUS IT (Japan)

- Intel Corporation (U.S.)

- Artiza Networks (Japan)

- Xena Networks (Denmark)

- ZPSYS (Poland)

Segment Analysis:

By Type

Fiber Optic Monitoring Segment Dominates Due to High Demand for Reliable Fronthaul Networks

The fronthaul monitor market is segmented based on technology type into:

- Fiber Optic Monitoring

- Subtypes: CWDM, DWDM, and others

- Microwave/Millimeter Wave Monitoring

- Subtypes: E-band, V-band, and others

- Others

By Application

Telecommunications Industry Leads Market Adoption Due to 5G Network Expansion

The market is segmented based on application areas into:

- Telecommunications Industry

- Subsegments: 5G networks, 4G LTE, and others

- Satellite Communications Industry

- Industrial Automation

- Transportation Industry

- Others

By End User

Network Operators Account for Significant Market Share Owing to Infrastructure Modernization

The market is segmented by end user into:

- Network Operators

- Test Equipment Manufacturers

- Research Institutions

- Government Organizations

By Deployment Mode

Cloud-based Solutions Gaining Traction for Remote Monitoring Capabilities

The market is segmented by deployment mode into:

- On-premise Solutions

- Cloud-based Solutions

- Hybrid Solutions

Regional Analysis: Fronthaul Monitor Market

Asia-Pacific

The Asia-Pacific region leads the global fronthaul monitoring market, driven by rapid 5G deployment and extensive telecommunication infrastructure development. With China accounting for over 40% of global 5G base stations as of 2024 and India’s ambitious BharatNet project expanding rural connectivity, demand for fronthaul monitoring solutions has surged. Key manufacturers like Huawei and ZTE dominate regional supply chains, while governments prioritize network quality assurance through stricter performance benchmarks. However, varied technological maturity across countries creates uneven adoption rates, with developed markets favoring advanced monitoring systems and emerging economies still transitioning from legacy solutions.

North America

North America’s fronthaul monitoring market thrives on stringent telecom regulatory frameworks and massive private sector investments in Open RAN architectures. The U.S. FCC’s $1.9 billion Rip and Replace program has accelerated monitoring solution deployments, particularly for secure fronthaul links in sensitive communications. Major players like Keysight Technologies and VIAVI Solutions provide cutting-edge monitoring platforms that integrate AI-driven analytics, addressing carriers’ needs for real-time performance optimization. Canada’s focus on Arctic connectivity projects further expands applications for ruggedized monitoring systems capable of operating in extreme conditions.

Europe

European adoption of fronthaul monitoring solutions reflects the region’s balanced approach between technological innovation and regulatory compliance. The EU’s 5G Action Plan mandates comprehensive network monitoring, driving demand for solutions that meet ETSI standards. Nokia and Ericsson supply advanced monitoring platforms supporting cloud-RAN architectures, while startups develop specialized tools for O-RAN security validation. Germany and the UK lead in deployment volumes, though Eastern European markets show slower uptake due to budget constraints in network modernization projects.

Middle East & Africa

This emerging market demonstrates growing potential for fronthaul monitoring systems, particularly in Gulf Cooperation Council countries investing heavily in smart city infrastructures. UAE’s Operation 300bn industrial strategy prioritizes telecom infrastructure, creating opportunities for monitoring solution providers. However, the broader African market faces challenges including limited 5G spectrum allocation and reliance on Chinese vendors whose integrated solutions often bundle basic monitoring functions. South Africa and Nigeria represent key growth markets where mobile operators increasingly require standalone monitoring tools for network optimization.

South America

The region’s fronthaul monitoring market progresses gradually, shaped by economic fluctuations and uneven telecom development. Brazil accounts for over 60% of regional demand, driven by major carriers like TIM Brasil deploying extensive fiber fronthaul networks. While macroeconomic instability in Argentina and Venezuela constrains market growth, Colombia and Chile show promising adoption of monitoring solutions through public-private partnership models. Local manufacturers focus on cost-effective monitoring systems tailored for hybrid copper-fiber fronthaul architectures still common across the region.

Report Scope

This market research report provides a comprehensive analysis of the Global Fronthaul Monitor Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 266 million in 2024 and is projected to reach USD 403 million by 2032, growing at a CAGR of 6.2%.

- Segmentation Analysis: Detailed breakdown by product type (Fiber Optic Monitoring, Microwave/Millimeter Wave Monitoring) and application (Telecommunications, Satellite Communications, Industrial Automation, Transportation, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with the U.S. and China being key growth markets.

- Competitive Landscape: Profiles of leading market participants including Keysight Technologies, VIAVI Solutions, EXFO, Spirent Communications, Anritsu, Nokia, and Huawei, covering their product portfolios and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging monitoring technologies, integration with 5G networks, and advancements in fronthaul optimization.

- Market Drivers & Restraints: Evaluation of factors such as 5G network expansion, increasing mobile data traffic, and the need for network reliability versus challenges like high deployment costs.

- Stakeholder Analysis: Insights for network equipment providers, telecom operators, test & measurement companies, and investors regarding market opportunities.

The report employs primary and secondary research methods, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Fronthaul Monitor Market?

-> Fronthaul Monitor Market was valued at 266 million in 2024 and is projected to reach US$ 403 million by 2032, at a CAGR of 6.2% during the forecast period…

Which key companies operate in Global Fronthaul Monitor Market?

-> Key players include Keysight Technologies, VIAVI Solutions, EXFO, Spirent Communications, Anritsu, Nokia, and Huawei, among others.

What are the key growth drivers?

-> Key growth drivers include 5G network deployments, increasing mobile data traffic, and demand for reliable fronthaul network monitoring.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by rapid 5G adoption, while North America remains a significant market.

What are the emerging trends?

-> Emerging trends include AI-powered monitoring solutions, cloud-based fronthaul management, and integration with Open RAN architectures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...