Capsule Endoscopy Wireless Transceiver SoC Market Insights

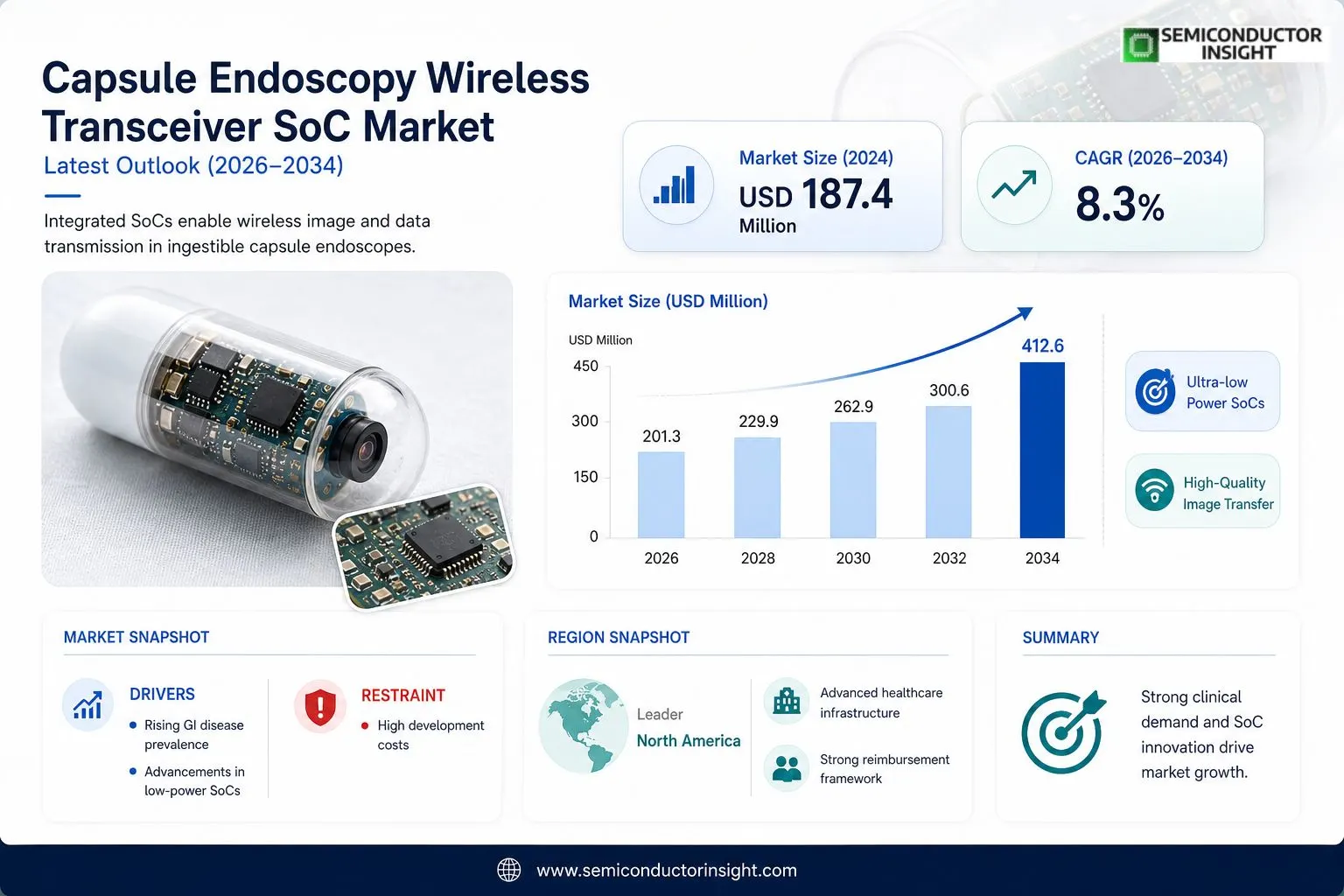

Global Capsule Endoscopy Wireless Transceiver SoC Market size was valued at USD 187.4 million in 2024. The market is projected to grow from USD 201.3 million in 2025 to USD 412.6 million by 2034, exhibiting a CAGR of 8.3% during the forecast period.

Capsule endoscopy wireless transceiver System-on-Chip (SoC) refers to highly integrated semiconductor devices specifically engineered to enable wireless image and data transmission within ingestible capsule endoscopes. These compact SoCs combine radiofrequency transceivers, image signal processors, power management circuits, and data encoding modules into a single chip, enabling real-time gastrointestinal imaging without conventional wired endoscopy procedures. The technology supports multiple frequency bands and low-power communication protocols essential for the miniaturized form factor of diagnostic capsules.

The market is experiencing steady expansion driven by the rising global prevalence of gastrointestinal disorders, including Crohn’s disease, colorectal cancer, and obscure gastrointestinal bleeding, which collectively affect hundreds of millions of patients worldwide. Growing physician and patient preference for minimally invasive diagnostic procedures further accelerates adoption. Furthermore, advancements in low-power RF communication and CMOS fabrication technologies continue to enhance SoC performance, supporting broader clinical deployment. Key players operating in this space include Medtronic plc, Given Imaging (Covidien), Olympus Corporation, Intromedic Co., Ltd., and CapsoVision Inc., each contributing differentiated SoC-integrated capsule platforms to the competitive landscape.

MARKET DRIVERS

Rising Prevalence of Gastrointestinal Disorders Accelerating Demand for Capsule Endoscopy Wireless Transceiver SoC

Global burden of gastrointestinal (GI) diseases, including Crohn’s disease, obscure gastrointestinal bleeding, small bowel tumors, and celiac disease, continues to rise significantly across both developed and emerging economies. This escalating patient pool is a primary driver for the Capsule Endoscopy Wireless Transceiver SoC Market, as clinicians increasingly rely on capsule endoscopy as a minimally invasive diagnostic tool. The wireless transceiver System-on-Chip (SoC) serves as the critical communication backbone within the capsule, enabling real-time or near-real-time transmission of high-resolution imaging data from within the GI tract to external recording devices. As diagnostic accuracy demands grow, the need for more sophisticated and energy-efficient transceiver SoC solutions has become a central focus for device manufacturers and semiconductor developers alike.

Technological Advancements in Low-Power SoC Architecture Driving Market Expansion

Continuous innovation in ultra-low-power semiconductor design has been a pivotal force propelling the Capsule Endoscopy Wireless Transceiver SoC Market forward. Modern SoC platforms now integrate advanced RF transceiver modules, image signal processors, and power management units within a single miniaturized chip, enabling longer battery life and improved signal integrity during the 8–12 hour diagnostic window typical of a capsule endoscopy procedure. The adoption of cutting-edge CMOS process nodes and system-level co-design methodologies has allowed chipmakers to deliver transceiver SoCs with substantially reduced power consumption while supporting higher data throughput for multi-frame-per-second imaging. These advancements directly translate into enhanced diagnostic utility and improved patient experience, reinforcing physician and hospital adoption of capsule endoscopy platforms globally.

➤ The integration of ultra-wideband (UWB) and MICS-band (Medical Implant Communication Service) wireless protocols within next-generation Capsule Endoscopy Wireless Transceiver SoC platforms is enabling more precise in-body localization alongside high-fidelity image data transmission, marking a significant technological inflection point for the market.

Government and institutional investments in healthcare infrastructure modernization, particularly in Asia-Pacific and the Middle East, are further amplifying demand for capsule endoscopy-based diagnostics, thereby strengthening the downstream market for wireless transceiver SoC components. Healthcare providers are prioritizing outpatient and ambulatory diagnostic solutions to reduce procedural costs and hospital burdens, and capsule endoscopy, powered by efficient transceiver SoC technology, fits squarely within this strategic shift. The alignment of clinical need, technological capability, and healthcare policy thus forms a robust and sustained demand driver for the Capsule Endoscopy Wireless Transceiver SoC Market.

MARKET CHALLENGES

Complex Regulatory Pathways and Stringent Biocompatibility Standards Posing Significant Hurdles

One of the most pressing challenges confronting participants in the Capsule Endoscopy Wireless Transceiver SoC Market is navigating the complex and multi-jurisdictional regulatory environment governing active implantable and ingestible medical devices. Regulatory bodies such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and equivalent authorities in Japan and China impose rigorous pre-market review processes, electromagnetic compatibility (EMC) testing, and biocompatibility assessments under standards such as ISO 10993. For SoC developers, achieving compliance requires substantial investment in testing, documentation, and quality management systems, which prolongs time-to-market and increases overall development costs. Smaller semiconductor companies with limited regulatory expertise face a particularly steep barrier to entry in this specialized market segment.

Other Challenges

Data Security and Wireless Interference Risks

The wireless transmission of sensitive patient imaging data from within the human body introduces meaningful cybersecurity and signal integrity concerns for the Capsule Endoscopy Wireless Transceiver SoC Market. As capsule endoscopy systems increasingly interface with hospital networks and cloud-based diagnostic platforms, the transceiver SoC must incorporate robust encryption and interference-mitigation capabilities to meet healthcare data protection mandates such as HIPAA and GDPR. Operating in the crowded 2.4 GHz ISM band or proprietary medical frequency bands requires sophisticated co-existence management, and in-body signal attenuation presents ongoing engineering challenges that demand continuous R&D investment from SoC designers.

High Development and Integration Costs Limiting Broader Adoption

The specialized nature of capsule endoscopy wireless transceiver SoC design , demanding extreme miniaturization, biocompatible packaging, multi-protocol RF support, and ultra-low power operation simultaneously , results in elevated non-recurring engineering (NRE) costs and relatively low production volumes compared to consumer electronics SoCs. This cost structure makes it difficult for device manufacturers to achieve price points that enable widespread adoption in cost-sensitive markets, particularly in lower-income regions where GI disease prevalence is also high. The limited number of qualified semiconductor foundries capable of producing these specialized chips further constrains supply chain flexibility and can introduce lead time vulnerabilities for capsule endoscopy system OEMs.

MARKET RESTRAINTS

Limited Reimbursement Coverage and Healthcare Budget Constraints Restricting Market Penetration

Despite the clinical efficacy of capsule endoscopy as a diagnostic modality, inconsistent reimbursement policies across major healthcare markets continue to act as a significant restraint on the broader adoption of systems incorporating advanced Capsule Endoscopy Wireless Transceiver SoC technology. In several markets, reimbursement coverage for capsule endoscopy procedures remains limited to specific indications, such as obscure GI bleeding, while broader applications in inflammatory bowel disease monitoring or routine colorectal screening receive less consistent payer support. This reimbursement uncertainty discourages hospitals and ambulatory care centers from investing in next-generation capsule endoscopy platforms, indirectly suppressing demand for the high-performance wireless transceiver SoC components that power them. Addressing this restraint requires coordinated advocacy by device manufacturers and clinical societies to expand evidence-based reimbursement frameworks.

Technical Constraints of In-Body Wireless Communication Limiting SoC Performance Ceilings

The human body presents a uniquely challenging environment for wireless signal propagation, and this physical reality imposes inherent performance constraints on the Capsule Endoscopy Wireless Transceiver SoC Market. Tissue absorption, signal scattering, and patient-to-patient anatomical variability result in unpredictable channel characteristics that limit achievable data rates and transmission reliability, regardless of SoC sophistication. While antenna design innovations and adaptive modulation schemes have partially mitigated these effects, the fundamental physics of in-body RF communication continue to cap the upper bounds of image resolution and frame rate that can be practically delivered in a commercial capsule endoscopy system. These technical ceilings restrain the pace of next-generation product differentiation and can limit the commercial justification for premium-priced advanced transceiver SoC solutions in this specialized market.

MARKET OPPORTUNITIES

Emerging Applications in AI-Assisted Diagnostics Creating New Value Propositions for Transceiver SoC Developers

The convergence of artificial intelligence (AI) and capsule endoscopy represents one of the most compelling growth opportunities for the Capsule Endoscopy Wireless Transceiver SoC Market. As AI-driven image analysis platforms are increasingly integrated into capsule endoscopy reading workflows to assist gastroenterologists in identifying polyps, bleeding sites, and mucosal abnormalities, the demand for higher-bandwidth, lower-latency wireless transceiver SoC solutions that can support enhanced image quality and faster data transfer is expected to grow commensurately. SoC developers that proactively architect their platforms to support AI-ready data pipelines , including on-chip pre-processing capabilities and seamless integration with cloud diagnostic platforms , are well positioned to capture premium design wins with leading capsule endoscopy OEMs navigating this technological transition.

Expanding Market Access in Asia-Pacific Through Localized Product Development and Strategic Partnerships

The Asia-Pacific region, led by China, Japan, South Korea, and India, represents a substantial and increasingly accessible opportunity for the Capsule Endoscopy Wireless Transceiver SoC Market. Rising healthcare expenditure, a large and growing patient population with high GI disease incidence, and supportive government policies promoting domestic medical device innovation are collectively creating a favorable environment for market expansion. Regional capsule endoscopy device manufacturers, several of which have achieved meaningful scale in their home markets, are actively seeking differentiated and cost-optimized wireless transceiver SoC solutions to power competitive product portfolios. Global SoC developers that establish local engineering support capabilities, engage in co-development partnerships with regional OEMs, and tailor their solutions to meet region-specific regulatory and cost requirements stand to benefit significantly from this accelerating market opportunity across the Asia-Pacific landscape.

Capsule Endoscopy Wireless Transceiver SoC Market Trends

Rising Demand for Minimally Invasive Gastrointestinal Diagnostics Driving Market Momentum

The Capsule Endoscopy Wireless Transceiver SoC Market is witnessing accelerated growth as healthcare providers and patients increasingly favor minimally invasive diagnostic approaches over conventional wired endoscopy procedures. The growing global burden of gastrointestinal disorders, including Crohn’s disease, colorectal cancer, and obscure gastrointestinal bleeding, which collectively affect hundreds of millions of patients worldwide, continues to fuel demand for advanced capsule endoscopy solutions. Wireless transceiver System-on-Chip technologies are central to this shift, enabling real-time gastrointestinal imaging through highly integrated semiconductor devices that combine radiofrequency transceivers, image signal processors, power management circuits, and data encoding modules within a single compact chip.

Other Trends

Advancements in Low-Power RF Communication and CMOS Fabrication

A prominent trend shaping the Capsule Endoscopy Wireless Transceiver SoC Market is the continuous evolution of low-power radiofrequency communication and complementary metal-oxide-semiconductor fabrication technologies. These advancements are directly enhancing SoC performance by enabling superior image signal processing and more reliable data transmission within the miniaturized form factor demanded by ingestible diagnostic capsules. As CMOS process nodes become increasingly refined, manufacturers are achieving greater energy efficiency and higher levels of chip integration, which are critical requirements for sustaining the operational lifespan of capsule endoscopes during gastrointestinal transit.

Multi-Frequency Band and Low-Power Protocol Adoption

Another key trend in the Capsule Endoscopy Wireless Transceiver SoC Market involves the broader adoption of multi-frequency band support and low-power communication protocols within SoC architectures. As clinical deployment expands globally, device manufacturers are prioritizing wireless transceiver designs that can operate across multiple frequency bands to ensure compatibility with diverse regulatory environments and hospital infrastructure. This trend supports broader market penetration and positions leading companies, including Medtronic plc, Olympus Corporation, Intromedic Co., Ltd., and CapsoVision Inc., to offer differentiated SoC-integrated capsule platforms suited to varied clinical settings.

Competitive Innovation Among Key Market Participants

The competitive landscape of the Capsule Endoscopy Wireless Transceiver SoC Market is being shaped by sustained innovation from established players such as Medtronic plc, Given Imaging, Olympus Corporation, Intromedic Co., Ltd., and CapsoVision Inc. These companies are actively developing differentiated capsule platforms that leverage next-generation wireless transceiver SoC capabilities to improve image resolution, transmission reliability, and overall diagnostic accuracy. As physician preference for non-invasive gastrointestinal diagnostics continues to grow, competitive investment in SoC integration technologies is expected to remain a defining trend across the forecast period, reinforcing the market’s expansion trajectory.

COMPETITIVE LANDSCAPE

Key Industry Players

Capsule Endoscopy Wireless Transceiver SoC Market: Competitive Dynamics and Leading Innovators Shaping the Future of Minimally Invasive GI Diagnostics

Global Capsule Endoscopy Wireless Transceiver SoC market, valued at USD 187.4 million in 2024 and projected to reach USD 412.6 million by 2034 at a CAGR of 8.3%, is characterized by a moderately consolidated competitive landscape where a handful of vertically integrated medical device companies command significant market share alongside specialized semiconductor and SoC design firms. Medtronic plc stands out as a dominant force in this space, leveraging its expansive global distribution network, robust R&D capabilities, and its PillCam platform to maintain a leading position in capsule endoscopy-integrated SoC deployment. Given Imaging, now operating under Covidien and subsequently integrated into Medtronic’s portfolio, has been instrumental in pioneering the wireless image transmission SoC technology that underpins much of the current clinical standard. Olympus Corporation, a long-standing leader in endoscopic solutions, continues to invest in compact SoC architectures that support high-resolution imaging and low-power RF communication protocols suitable for gastrointestinal capsule platforms.

Beyond the dominant incumbents, several niche yet strategically significant players are actively shaping the competitive dynamics of the Capsule Endoscopy Wireless Transceiver SoC market. Intromedic Co., Ltd. from South Korea has developed proprietary SoC-integrated capsule systems with differentiated RF transmission capabilities. CapsoVision Inc. offers a 360-degree imaging capsule solution built on advanced transceiver SoC design. Jinshan Science and Technology Group has established a notable presence in the Asia-Pacific region with cost-competitive SoC-enabled capsule platforms. On the semiconductor side, companies such as Texas Instruments and Analog Devices supply critical low-power RF transceiver components and mixed-signal SoC building blocks that are incorporated into capsule endoscopy systems by device manufacturers. RFMD (now part of Qorvo) and Silicon Laboratories also contribute specialized RF front-end and wireless transceiver ICs relevant to this segment. NaviCam, developed by Ankon Technologies, further intensifies competition with magnetically guided capsule endoscopy systems that integrate advanced wireless SoC modules for real-time data transmission in gastrointestinal diagnostics.

List of Key Capsule Endoscopy Wireless Transceiver SoC Companies Profiled

- Medtronic plc

- Given Imaging (Covidien / Medtronic)

- Olympus Corporation

- Intromedic Co., Ltd.

- CapsoVision Inc.

- Jinshan Science and Technology Group

- Texas Instruments Incorporated

- Analog Devices, Inc.

- Qorvo, Inc. (formerly RFMD)

- Silicon Laboratories Inc.

- Ankon Technologies (NaviCam)

- RF Micro Devices

- Check-Cap Ltd.

- Micro-Tech Endoscopy

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Multi-Band Wireless Transceiver SoC holds the leading position within the type segment, driven by its inherent technical superiority in supporting diverse clinical environments.

|

| By Application |

|

Small Bowel Imaging represents the dominant application segment, underpinned by the clinical complexity of diagnosing disorders localized to the small intestine.

|

| By End User |

|

Hospitals and Specialty Clinics constitute the leading end-user segment, reflecting their central role in the clinical deployment of capsule endoscopy systems.

|

| By Communication Technology |

|

RF-Based Communication leads the communication technology segment, as it represents the foundational wireless transmission approach most widely validated in clinical capsule endoscopy platforms.

|

| By Integration Level |

|

Fully Integrated SoC (All-in-One) emerges as the dominant integration-level segment, driven by the unique design constraints imposed by ingestible capsule endoscopy devices.

|

Regional Analysis: Capsule Endoscopy Wireless Transceiver SoC Market

North America’s leadership in the capsule endoscopy wireless transceiver SoC market is closely tied to its unmatched R&D ecosystem. Major semiconductor companies and specialized medical chip designers are investing heavily in ultra-low-power SoC architectures, enabling longer battery life and more reliable wireless transmission within the confined capsule form factor. Collaborative research between industry players and academic institutions continues to yield significant breakthroughs in signal processing and miniaturized antenna design.

The regulatory environment in North America, particularly under FDA oversight, provides medical device manufacturers with a structured yet demanding approval process that ultimately raises product quality standards. Comprehensive reimbursement coverage from both private insurers and public programs such as Medicare has made capsule endoscopy procedures more financially accessible, stimulating demand for advanced wireless transceiver SoC-enabled devices and encouraging broader clinical deployment across diverse patient populations.

High-density hospital networks, well-equipped gastroenterology clinics, and an increasing shift toward minimally invasive diagnostic procedures have created fertile ground for capsule endoscopy wireless transceiver SoC adoption across North America. The region’s strong emphasis on patient comfort and non-invasive diagnostic alternatives has positioned wireless capsule endoscopy as a preferred modality, driving sustained procurement of sophisticated SoC-integrated devices that meet demanding clinical performance benchmarks.

The North American venture capital landscape remains highly active in funding early-stage companies developing specialized wireless transceiver SoC technologies for capsule endoscopy applications. Strategic partnerships between established semiconductor giants and agile medical device startups are accelerating commercialization timelines. Government initiatives supporting digital health and MedTech innovation further reinforce North America’s position as the primary engine of growth and technological differentiation within Global capsule endoscopy wireless transceiver SoC market.

Europe

Europe represents a highly significant and mature regional market within Global Capsule Endoscopy Wireless Transceiver SoC landscape. Countries such as Germany, France, the United Kingdom, and the Netherlands are at the forefront of clinical adoption, supported by robust national healthcare systems and a strong culture of preventive gastrointestinal diagnostics. European regulatory bodies, particularly the European Medicines Agency and CE marking framework under the EU Medical Device Regulation, provide a harmonized yet stringent approval structure that encourages innovation while ensuring patient safety. The region’s semiconductor industry, though more fragmented than North America’s, hosts several specialized chip design firms advancing wireless communication protocols suited for in-body data transmission. Growing awareness of colorectal and small intestine disorders has spurred demand for non-invasive diagnostic solutions, indirectly bolstering the capsule endoscopy wireless transceiver SoC market. Furthermore, EU-funded research programs and cross-border collaborative initiatives between universities and MedTech companies continue to refine SoC miniaturization and power efficiency, strengthening Europe’s competitive position in this specialized market segment.

Asia-Pacific

The Asia-Pacific region is emerging as the most dynamic and rapidly evolving market for capsule endoscopy wireless transceiver SoC technologies, fueled by a combination of expanding healthcare expenditure, rising gastrointestinal disease prevalence, and accelerating MedTech manufacturing capabilities. China, Japan, South Korea, and India are the primary growth engines, each contributing distinct advantages to the regional ecosystem. Japan’s precision engineering heritage and South Korea’s semiconductor design expertise are directly applicable to advancing wireless transceiver SoC performance for capsule endoscopy applications. China’s massive domestic healthcare modernization push and government-led MedTech innovation programs are rapidly closing the technological gap with Western counterparts. India’s growing private hospital sector and increasing insurance penetration are expanding the addressable market for advanced diagnostic devices. Regional manufacturers are increasingly competing on both cost efficiency and technological sophistication, making Asia-Pacific a critical battleground for global capsule endoscopy wireless transceiver SoC market share over the forecast period through 2034.

South America

South America occupies a developing but progressively important position within Global Capsule Endoscopy Wireless Transceiver SoC Market. Brazil and Argentina serve as the primary demand centers, benefiting from relatively more developed healthcare infrastructures compared to other nations in the region. Growing urbanization, rising incidence of gastrointestinal disorders linked to dietary shifts, and gradual improvements in health insurance coverage are collectively building a foundation for increased adoption of capsule endoscopy technologies. However, challenges such as inconsistent regulatory frameworks across member nations, economic volatility, and limited local semiconductor manufacturing capabilities continue to constrain market acceleration. Most capsule endoscopy wireless transceiver SoC-enabled devices in South America are currently imported, leaving the region reliant on international supply chains. Efforts by regional health ministries to modernize diagnostic infrastructure and attract foreign MedTech investment are expected to gradually improve market conditions and drive incremental growth through the latter half of the forecast period.

Middle East & Africa

The Middle East and Africa region represents an early-stage but strategically noteworthy segment of Global Capsule Endoscopy Wireless Transceiver SoC Market. Gulf Cooperation Council nations, particularly the United Arab Emirates and Saudi Arabia, are leading regional adoption through ambitious national healthcare modernization programs and significant investment in advanced diagnostic equipment. These governments are actively pursuing partnerships with global MedTech leaders to upgrade hospital capabilities and introduce cutting-edge non-invasive diagnostic technologies, including capsule endoscopy systems powered by advanced wireless transceiver SoCs. In contrast, much of sub-Saharan Africa and parts of North Africa face considerable barriers including limited diagnostic infrastructure, shortage of trained gastroenterology specialists, and constrained public healthcare budgets. Nonetheless, international development initiatives and growing private healthcare investments in key African markets such as South Africa and Nigeria are slowly creating conditions conducive to longer-term market development within this segment of the capsule endoscopy wireless transceiver SoC industry.

Report Scope

This market research report provides a comprehensive analysis of the Capsule Endoscopy Wireless Transceiver SoC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Capsule Endoscopy Wireless Transceiver SoC Market?

-> Global Capsule Endoscopy Wireless Transceiver SoC Market size was valued at USD 187.4 million in 2024. The market is projected to grow from USD 201.3 million in 2025 to USD 412.6 million by 2034, exhibiting a CAGR of 8.3% during the forecast period.

Which key companies operate in Capsule Endoscopy Wireless Transceiver SoC Market?

-> Key players include Medtronic plc, Given Imaging (Covidien), Olympus Corporation, Intromedic Co., Ltd., and CapsoVision Inc., among others, each contributing differentiated SoC-integrated capsule platforms to the competitive landscape.

What are the key growth drivers?

-> Key growth drivers include the rising global prevalence of gastrointestinal disorders such as Crohn’s disease, colorectal cancer, and obscure gastrointestinal bleeding, growing preference for minimally invasive diagnostic procedures, and advancements in low-power RF communication and CMOS fabrication technologies.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region driven by expanding healthcare infrastructure and rising gastrointestinal disease burden, while North America remains a dominant market due to high adoption of advanced endoscopic technologies and well-established healthcare systems.

What are the emerging trends?

-> Emerging trends include highly integrated SoC architectures combining radiofrequency transceivers, image signal processors, power management circuits, and data encoding modules into a single chip, adoption of low-power communication protocols, and the expanding use of multi-frequency band support to enhance real-time gastrointestinal imaging capabilities in miniaturized diagnostic capsules.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...