MARKET INSIGHTS

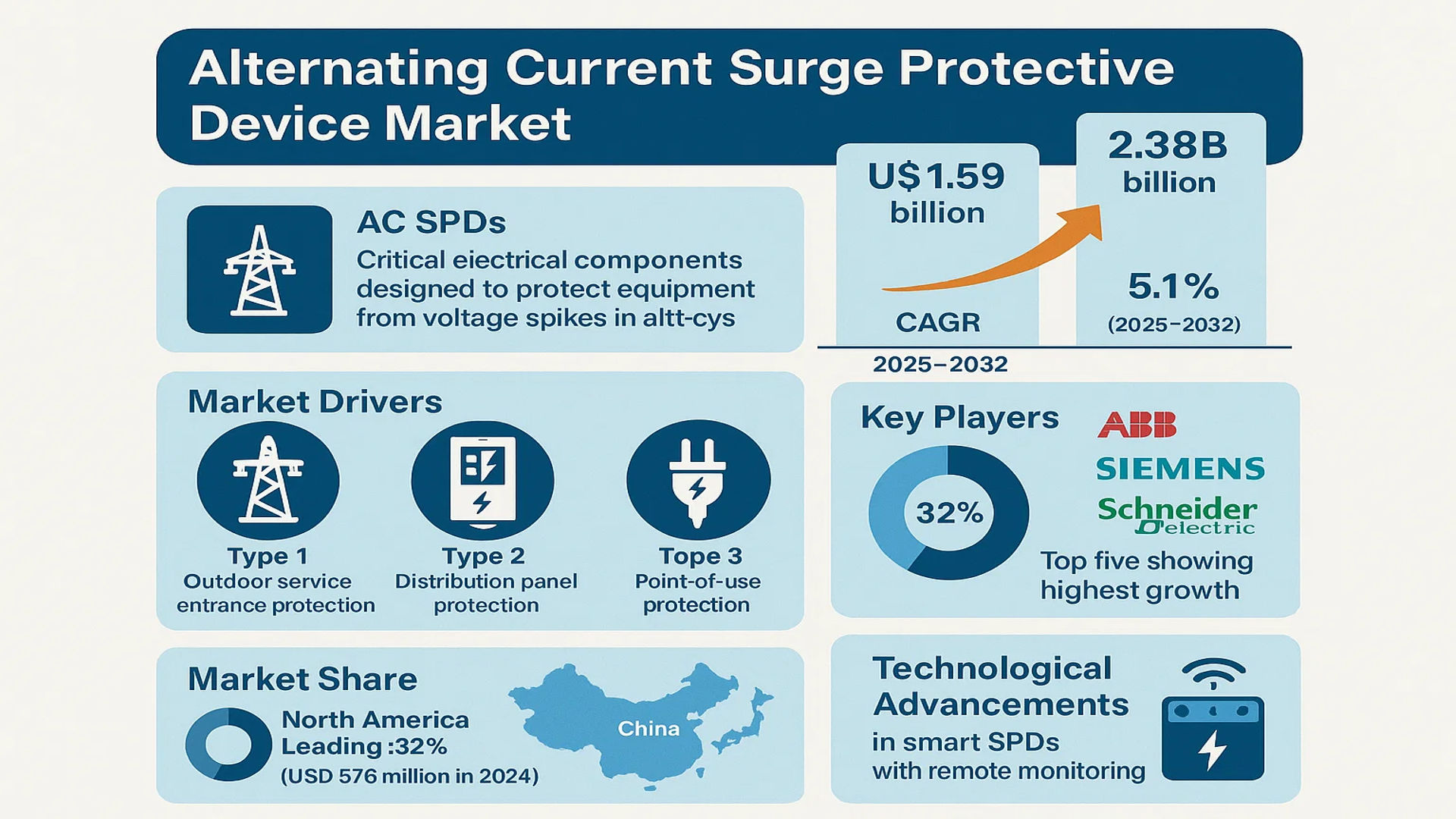

The global Alternating Current Surge Protective Device Market size was valued at US$ 1.59 billion in 2024 and is projected to reach US$ 2.38 billion by 2032, at a CAGR of 5.1% during the forecast period 2025-2032.

AC SPDs are critical electrical components designed to protect equipment from voltage spikes in alternating current systems. These devices limit transient overvoltages by diverting surge currents, safeguarding sensitive electronics across residential, commercial, and industrial applications. The market includes three key product types: Type 1 (for outdoor service entrance protection), Type 2 (distribution panel protection), and Type 3 (point-of-use protection).

Market growth is driven by increasing electrical infrastructure investments and stricter safety regulations worldwide. While North America currently leads with 32% market share (USD 576 million in 2024), Asia-Pacific shows the highest growth potential, particularly in China where urbanization is accelerating power infrastructure development. Major players like ABB, Siemens, and Schneider Electric are expanding their SPD portfolios, with the top five companies holding 45% of global revenue in 2024. Recent technological advancements in smart SPDs with remote monitoring capabilities are creating new opportunities in the industrial IoT segment.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Electrical Safety Solutions to Propel Market Growth

The global alternating current surge protective device (AC SPD) market is experiencing robust growth due to increasing awareness about electrical safety across industries. With power surges causing annual equipment damage losses estimated in billions, organizations are prioritizing SPD adoption as a cost-effective risk mitigation strategy. The growing integration of sensitive electronic components in industrial, commercial and residential applications further drives demand for reliable surge protection, as even minor voltage fluctuations can disrupt operations or cause permanent equipment damage.

Growth of Smart Infrastructure Projects Creates Sustained Demand

Smart city initiatives and infrastructure modernization programs worldwide are creating significant opportunities for AC SPD solutions. Governments are investing heavily in upgrading electrical grids and critical infrastructure to support digital transformation, with SPDs becoming mandatory in many new construction projects. The telecommunications sector alone accounts for a substantial share of SPD demand, as 5G network deployments require advanced protection for sensitive base station equipment against lightning strikes and power anomalies.

➤ For instance, regulatory mandates now require SPD installations in all electrical service entrance panels for new commercial buildings across multiple regions.

Furthermore, the rapid adoption of renewable energy systems has introduced new protection challenges, as solar arrays and wind turbines are particularly vulnerable to surge events. This has led to specialized SPD solutions gaining traction in the clean energy sector.

MARKET RESTRAINTS

High Initial Costs and Maintenance Requirements Limit Market Penetration

While AC SPDs offer long-term cost savings, their upfront installation expenses creates a barrier for widespread adoption, particularly in price-sensitive markets. Premium SPD solutions with advanced features can cost significantly more than basic models, making them less accessible to small businesses and residential users. Additionally, ongoing maintenance and replacement costs affect total ownership expenses, as SPD components degrade over time and require periodic inspection.

Other Restraints

Complex Installation Requirements

Proper SPD installation often requires electrical system modifications and certified professionals, adding to implementation costs. In retrofit applications, integrating SPDs with existing infrastructure can present technical challenges that deter end-users.

Lack of Awareness

Despite their importance, many organizations still underestimate electrical surge risks. This knowledge gap leads to inadequate protection strategies and slows market growth in developing regions where electrical safety standards are less stringent.

MARKET CHALLENGES

Technological Complexity Creates Product Development Hurdles

Designing SPDs that can handle increasingly complex electrical environments presents significant engineering challenges. Modern equipment with microprocessors and sensitive components requires SPD solutions with faster response times and greater precision. Manufacturers must continuously innovate to develop products that can protect against both low-voltage transients and catastrophic surges while meeting diverse industry specifications.

Other Challenges

Standardization Issues

The lack of uniform global standards for SPD specifications creates compatibility challenges, particularly for multinational corporations needing consistent protection across different regions. Varying certification requirements also complicate product development and market expansion strategies.

Supply Chain Vulnerabilities

The semiconductor shortages impacting multiple industries have affected SPD manufacturers, as many surge protection components rely on specialized electronic parts with limited alternative sourcing options.

MARKET OPPORTUNITIES

Emerging IoT and IIoT Applications Present New Growth Frontiers

The proliferation of IoT devices and industrial automation systems is creating unprecedented demand for advanced surge protection solutions. Smart factories and connected infrastructure require SPDs that can integrate with monitoring systems and provide predictive maintenance capabilities. This has led to the development of intelligent SPD solutions with remote diagnostics features, representing a significant market growth opportunity.

Growth in Edge Computing Facilities Drives Specialized Protection Needs

The rapid expansion of edge data centers to support cloud computing and content delivery networks requires specialized SPD solutions. These facilities process critical data closer to end-users but often lack the robust infrastructure of traditional data centers, making surge protection paramount. With edge computing deployments expected to double in the coming years, SPD manufacturers are developing compact, high-performance solutions tailored to these applications.

➤ Recent innovations include modular SPD systems that can be daisy-chained to protect multiple circuits while maintaining centralized monitoring capabilities.

Additionally, the electric vehicle charging infrastructure boom presents lucrative opportunities, as charging stations require robust protection against power quality issues that could damage expensive equipment or pose safety risks.

ALTERNATING CURRENT SURGE PROTECTIVE DEVICE MARKET TRENDS

Increasing Demand for Electrical Safety Solutions Drives Market Growth

The global Alternating Current Surge Protective Device (AC SPD) market is experiencing robust growth, projected to expand at a CAGR of 6.5% from 2024 to 2032, driven by increasing awareness of electrical safety and infrastructure development. AC SPDs serve as critical components in protecting sensitive electronic equipment from voltage spikes, particularly in industrial, commercial, and residential applications. With a current market valuation of $1.2 billion in 2024, analysts anticipate it will surpass $1.9 billion by 2032, fueled by rising investments in smart grids and renewable energy projects. The U.S. dominates this landscape with a market share of approximately 30%, while China is emerging as the fastest-growing region due to rapid urbanization and large-scale electrification initiatives.

Other Trends

Technological Advancements in SPD Design

The surge protective device market is witnessing innovations in modular and hybrid SPDs, which offer faster response times (<25 nanoseconds) and enhanced durability. Manufacturers are integrating IoT-enabled monitoring features, allowing real-time tracking of surge events and device health. Furthermore, the adoption of Type 1 SPDs, designed for high-energy surges such as lightning strikes, is growing significantly, particularly in regions prone to extreme weather conditions. These devices are projected to account for over 40% of total market revenue by 2027, reflecting higher demand in industrial and utility applications.

Growing Emphasis on Renewable Energy Integration

The global shift toward renewable energy sources, such as solar and wind power, is amplifying the need for reliable surge protection solutions. Renewable energy systems are highly susceptible to voltage fluctuations and transient surges, making SPDs indispensable for safeguarding inverters and distribution networks. The solar energy sector alone contributed to a 22% increase in SPD demand in 2023, a trend expected to strengthen as governments accelerate clean energy transitions. Additionally, strict regulatory standards in North America and Europe, including mandates for surge protection in photovoltaic installations, are compelling system integrators to prioritize SPD deployments.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Drive Innovation in AC Surge Protection

The global alternating current surge protective device (AC SPD) market features a mix of multinational conglomerates and specialized manufacturers, competing on technological innovation and product reliability. ABB and Siemens dominate the industrial segment, leveraging their expertise in power distribution systems and smart grid solutions. These companies collectively held over 25% market share in 2024, driven by large-scale infrastructure projects.

Eaton and Schneider Electric have strengthened their positions through strategic acquisitions, particularly in the commercial building protection segment. Their integrated electrical solutions combine SPDs with energy management systems, creating value-added offerings for smart buildings. Meanwhile, Littelfuse and Bourns lead in component-level protection with advanced metal oxide varistor (MOV) technologies.

The market sees increasing competition from regional specialists like Beny Electric in China and Phoenix Contact in Europe, who are gaining traction with cost-competitive solutions. These companies are expanding footprint through local partnerships and customized products for regional voltage standards.

Recent developments show a clear industry trend toward IoT-enabled surge protection, with players like Legrand and GE introducing connected SPDs that provide real-time monitoring. This technology shift is forcing traditional manufacturers to accelerate R&D investments, observed through a 15% year-over-year increase in patent filings related to surge protection between 2022-2024.

List of Key AC Surge Protective Device Manufacturers

- ABB (Switzerland)

- Siemens (Germany)

- Eaton (Ireland)

- Schneider Electric (France)

- Littelfuse (U.S.)

- Bourns (U.S.)

- Beny Electric (China)

- Phoenix Contact (Germany)

- Legrand (France)

- GE (U.S.)

- LSP International (China)

- Citel (France)

- Emerson Electric (U.S.)

- Leviton (U.S.)

- Tripp Lite (U.S.)

- Raycap (U.S.)

Segment Analysis:

By Type

Type 1 Surge Protective Devices Segment Leads Due to High-End Protection Capabilities

The market is segmented based on type into:

- Type 1 Surge Protective Devices

- Subtypes: Hardwired, Plug-in, and others

- Type 2 Surge Protective Devices

- Type 3 Surge Protective Devices

- Combined Type (Type 1+2+3)

- Others

By Application

Industrial Segment Dominates Due to Critical Power Protection Needs

The market is segmented based on application into:

- Residential

- Commercial

- Industrial

- Subtypes: Manufacturing, Energy & Power, Telecom, and others

- Transportation

- Others

By Voltage Range

Low Voltage Segment Holds Significant Market Share

The market is segmented based on voltage range into:

- Low Voltage (Up to 1kV)

- Medium Voltage (1kV-33kV)

- High Voltage (Above 33kV)

By Mounting Type

Panel Mount Segment Shows Strong Growth Potential

The market is segmented based on mounting type into:

- Panel Mount

- Din Rail Mount

- Plug-in

- Hardwired

Regional Analysis: Alternating Current Surge Protective Device Market

Asia-Pacific

The Asia-Pacific region dominates the AC Surge Protective Device (SPD) market, accounting for over 35% of global revenue share in 2024, driven by rapid industrialization and infrastructure development. China leads regional demand, supported by its massive power grid expansion and growing investments in smart city projects. India follows closely, with increasing adoption of Type 2 SPDs across commercial and industrial sectors to protect sensitive equipment. While cost sensitivity favors mid-range products, rising awareness about electrical safety standards and lightning protection is pushing the market toward advanced solutions. Japan and South Korea contribute significantly to technological advancements, particularly in high-performance SPDs for mission-critical applications.

North America

North America represents the second-largest AC SPD market, characterized by stringent electrical safety regulations such as UL 1449 standards and NEC requirements. The U.S. accounts for approximately 80% of regional demand, with significant deployment in data centers, healthcare facilities, and industrial plants. The Infrastructure Investment and Jobs Act has further stimulated market growth through power infrastructure upgrades. Canada shows steady adoption in the oil & gas and renewable energy sectors. While Type 1 SPDs dominate utility applications, the smart home revolution is driving residential SPD installations, particularly in states prone to severe weather conditions.

Europe

Europe’s mature AC SPD market is shaped by strict EU directives on electrical safety and the growing emphasis on renewable energy integration. Germany and France lead in industrial SPD adoption, while Nordic countries showcase high market penetration due to extreme weather conditions requiring robust surge protection. The region shows increasing preference for eco-friendly SPDs with lower carbon footprints. Eastern European nations present emerging opportunities as they upgrade aging power infrastructure. The market is transitioning toward smart SPDs with remote monitoring capabilities, aligned with the region’s Industry 4.0 initiatives.

South America

South America’s AC SPD market is developing steadily, with Brazil accounting for nearly half of regional demand. Growth is primarily driven by industrial applications in mining and energy sectors, along with increasing commercial construction. However, economic instability and inconsistent enforcement of electrical safety standards hinder market expansion. Argentina and Chile show promising growth in data center and telecom applications. While price sensitivity favors local manufacturers, international brands are gaining traction in premium segments through partnerships with utilities and OEMs.

Middle East & Africa

The MEA region represents an emerging market with growth concentrated in GCC countries and South Africa. Large-scale infrastructure projects and increasing power demand are key drivers, particularly for Type 1 and 2 SPDs. The UAE and Saudi Arabia lead adoption in commercial and industrial sectors, supported by stringent building codes. Africa shows uneven growth patterns, with South Africa maintaining the most developed market while other nations face challenges with power infrastructure development and affordability. The region presents long-term potential as renewable energy projects and smart city initiatives gain momentum.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Alternating Current Surge Protective Device (AC SPD) markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global AC SPD market is projected to grow at a significant CAGR during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (Type 1, Type 2, Type 3 SPDs), application (residential, commercial, industrial), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis of key markets like the U.S. and China.

- Competitive Landscape: Profiles of leading market participants including ABB, Eaton, Siemens, Schneider Electric, and GE, covering their product portfolios, market strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in surge protection, smart SPDs, and evolving industry standards like IEC 61643.

- Market Drivers & Restraints: Evaluation of factors such as increasing electrical infrastructure investments, growing awareness of power protection, along with challenges like price competition.

- Stakeholder Analysis: Strategic insights for manufacturers, distributors, system integrators, and investors regarding market opportunities and challenges.

The research employs both primary and secondary methods, including expert interviews and verified market data, to ensure accurate and reliable market intelligence.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Alternating Current Surge Protective Device Market?

-> Alternating Current Surge Protective Device Market size was valued at US$ 1.59 billion in 2024 and is projected to reach US$ 2.38 billion by 2032, at a CAGR of 5.1% during the forecast period 2025-2032.

Which key companies operate in Global AC SPD Market?

-> Key players include ABB, Eaton, Siemens, Schneider Electric, GE, Littelfuse, Leviton, and Phoenix Contact, among others.

What are the key growth drivers?

-> Key growth drivers include increasing electrical infrastructure investments, rising demand for power protection, and growing awareness of electrical safety.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is expected to show the highest growth rate during the forecast period.

What are the emerging trends?

-> Emerging trends include smart SPDs with remote monitoring, integration with IoT systems, and advanced materials for better protection.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...