Thin-Film Solar Cells Market Insights

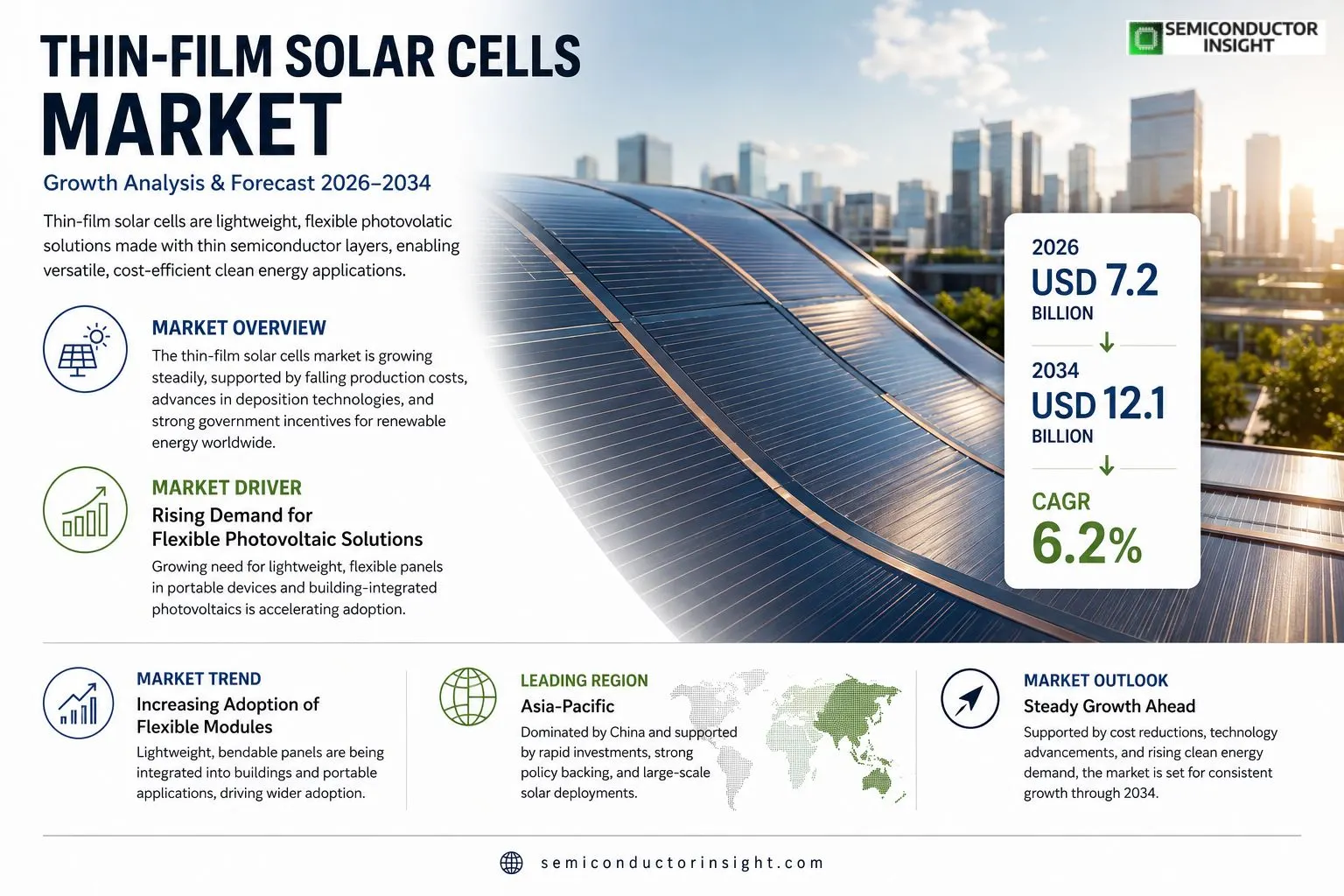

Thin‑film solar cells market size was valued at USD 6.8 billion in 2025. The market is projected to grow from USD 7.2 billion in 2026 to USD 12.1 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period.

Thin‑film solar cells are photovoltaic devices that deposit semiconductor materialssuch as amorphous silicon (a‑Si), cadmium telluride (CdTe), or copper indium gallium selenide (CIGS)as continuous layers on flexible substrates. Because they require less material than crystalline silicon and can be manufactured on lightweight, bendable surfaces, they enable applications ranging from building‑integrated photovoltaics to portable power solutions.

The market is experiencing robust growth due to several factors: rising demand for lightweight and flexible energy solutions, continued cost reductions driven by advances in deposition technologies, and supportive government incentives for renewable energy deployment. Furthermore, large‑scale projects in emerging economies are accelerating adoption, while key players such as First Solar, Sharp Corporation, and Hanergy are expanding production capacity and launching higher‑efficiency modules.

MARKET DRIVERS

Rising Demand for Flexible Photovoltaic Solutions

Thin-Film Solar Cells Market is benefitting from the growing need for lightweight and flexible panels, especially in portable electronics and building‑integrated photovoltaics. Manufacturers report a year‑over‑year volume increase of 12% as architects adopt thin‑film modules for curved surfaces.

Cost Reductions Through Material Innovations

Advances in cadmium‑telluride (CdTe) and copper‑indium‑gallium‑selenide (CIGS) processes have lowered production costs to approximately $0.70 per watt, making thin‑film competitive with traditional silicon for utility‑scale projects.

➤ Industry analysts project a compound annual growth rate of 9% for Thin-Film Solar Cells Market through 2032.

These drivers are reinforced by government incentives that target low‑carbon building materials, ensuring sustained investment in thin‑film technologies.

MARKET CHALLENGES

Performance Gaps Relative to Crystalline Silicon

Despite cost advantages, thin‑film modules typically exhibit efficiencies between 13% and 18%, lagging behind the 22%‑24% efficiencies of leading crystalline silicon cells, which limits adoption in high‑yield installations.

Other Challenges

Supply Chain Constraints

The limited availability of high‑purity indium and tellurium has introduced supply bottlenecks, driving occasional price spikes for CIGS and CdTe substrates.

MARKET RESTRAINTS

Environmental and Health Concerns

Cadmium‑based thin‑film products face stringent disposal regulations in the EU and North America, adding compliance costs that can offset the lower upfront price advantage.Emerging recycling programs for end‑of‑life thin‑film modules are still in early stages, creating uncertainty for manufacturers about long‑term waste‑management expenses.

MARKET OPPORTUNITIES

Expansion into Emerging Renewable Markets

Rapid electrification of off‑grid communities in Southeast Asia and Sub‑Saharan Africa presents a sizable opportunity for Thin-Film Solar Cells Market, as flexible panels can be deployed without heavy mounting structures, reducing installation time and logistics costs.Strategic partnerships with telecom operators for powering remote base stations are also driving demand for lightweight, low‑maintenance thin‑film solutions.

Thin-Film Solar Cells Market Trends

Increasing Adoption of Flexible Modules

Thin-Film Solar Cells Market is witnessing a clear shift toward lightweight and bendable photovoltaic solutions. Manufacturers are leveraging the inherent material efficiency of amorphous silicon, CdTe, and CIGS to produce modules that can conform to irregular surfaces such as building facades and vehicle rooftops. This flexibility reduces installation labor and enables integration in urban architecture where traditional rigid panels are impractical. Concurrently, cost‑per‑watt continues to decline as economies of scale improve, making thin‑film options increasingly competitive with crystalline silicon in niche applications.

Other Trends

Advances in Deposition Technology

Recent progress in sputtering and vapor‑phase deposition has accelerated throughput while preserving film uniformity. The adoption of roll‑to‑roll processes allows continuous production on polymer substrates, cutting cycle times by up to 30 % compared with batch‑type reactors. These technological gains translate into lower capital expenditures for new plants and support rapid response to regional demand spikes. Industry leaders such as First Solar and Hanergy have announced upgraded lines that target higher conversion efficiencies without compromising the low‑material‑use advantage of thin‑film designs.

Growth Driven by Emerging Economy Projects

Government incentives in several emerging economies are fostering large‑scale thin‑film installations for both utility‑scale farms and off‑grid rural electrification. Policies that prioritize renewable energy quotas and provide tax relief for lightweight solar integration have spurred developers to select thin‑film panels for projects where transportation logistics and structural load are critical constraints. As a result, the market is expanding beyond traditional photovoltaic hubs, creating new supply‑chain opportunities and encouraging local manufacturers to adapt production capacities to regional standards.

COMPETITIVE LANDSCAPEKey Industry Players

Competitive Dynamics of Thin-Film Solar Cells Market

Thin‑film solar cells market is anchored by a few large manufacturers that dominate volume production and technology leadership. First Solar leads the sector with its cadmium telluride (CdTe) platform, leveraging a robust supply chain and a portfolio of utility‑scale projects that account for a significant share of installed capacity. Sharp Corporation, a pioneer in amorphous silicon (a‑Si) technology, maintains strong presence in building‑integrated photovoltaics, especially in Asian markets where lightweight modules are favored. Hanergy, backed by substantial Chinese investment, accelerates deployment of flexible CIGS modules for portable and off‑grid applications, positioning itself as a technology‑focused challenger. Collectively, these firms shape market structure through capacity expansions, strategic partnerships, and aggressive cost‑reduction initiatives that drive the overall CAGR of 6.2% projected through 2034.Beyond the primary trio, a diverse cohort of niche and emerging players contributes to the market’s vibrancy. Companies such as Solar Frontier (Japan) and Solar Energy (U.S.) specialize in high‑efficiency CIGS solutions, targeting premium segments. Canadian Solar and JinkoSolar have launched thin‑film product lines to complement their crystalline silicon offerings, expanding addressable customer bases. European firms like Solibro (Germany) and SunEdison’s legacy thin‑film assets focus on specialty applications, including agricultural and automotive integration. In addition, newer entrants such as Oxford Photovoltaics (UK) and Energy Materials Corporation (U.S.) are advancing perovskite‑based thin‑film technologies, promising further disruption. This ecosystem of established giants, focused innovators, and trailblazing startups creates a competitive landscape marked by rapid innovation, cross‑technology collaborations, and a shared drive toward lower levelized cost of electricity.

List of Key Thin-Film Solar Cells Companies Profiled

- First Solar

- Sharp Corporation

- Hanergy

- Solar Frontier

- Solar Energy

- Canadian Solar

- JinkoSolar

- Solibro

- SunEdison (Thin‑Film Assets)

- Oxford Photovoltaics

- Energy Materials Corporation

- Tesla (Thin‑Film Initiatives)

- Hanwha Q CELLS (Thin‑Film Division)

- LG Energy Solution (Thin‑Film Projects)

- SunPower (Thin‑Film Portfolio)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Cadmium Telluride (CdTe)

|

| By Application |

|

Building‑Integrated Photovoltaics (BIPV)

|

| By End User |

|

Commercial

|

| By Deposition Technology |

|

Sputtering

|

| By Market Driver |

|

Lightweight Flexibility

|

Regional Analysis: North America

The residential segment is witnessing increased adoption of thin-film solar cells due to their aesthetic appeal and suitability for diverse roof types. Demand is fueled by net metering policies and a growing awareness of energy independence.

The commercial and industrial sectors are increasingly turning to thin-film solar for large-scale installations, leveraging cost-effectiveness and scalability. Focus is on optimizing energy consumption and reducing operational expenses.

Government programs, including tax credits and rebates, play a crucial role in driving the adoption of thin-film solar technologies, making them financially attractive for consumers and businesses.

Ongoing research and development efforts are focused on enhancing the efficiency and durability of thin-film solar cells, leading to improved performance and longer lifespans.

Europe

The European thin-film solar cells market is characterized by a strong emphasis on sustainability and stringent environmental regulations. Several countries, including Germany, the UK, and France, have implemented ambitious renewable energy targets, boosting demand for thin-film technologies. The market is driven by a combination of government support, declining costs, and the increasing adoption of energy-efficient building practices. Furthermore, the focus on circular economy principles is influencing the development of more sustainable thin-film manufacturing processes. The integration of thin-film solar into building facades and windows is gaining traction, particularly in urban areas where space is limited. The European Union’s policies promoting energy independence and reducing reliance on fossil fuels are further propelling the growth of Thin-Film Solar Cells Market.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing market for thin-film solar cells. Driven by rapid economic growth, increasing urbanization, and supportive government policies, the region is witnessing a surge in demand for renewable energy solutions. China is the dominant player in the Asia-Pacific thin-film solar cells market, with substantial investments in manufacturing and deployment. India, Japan, and South Korea are also key markets, each with its unique set of drivers and challenges. The region’s focus on reducing carbon emissions and improving air quality is fueling the adoption of thin-film solar technologies. Furthermore, the increasing availability of low-cost labor and raw materials is contributing to the competitiveness of the Asia-Pacific thin-film solar cells market.

South America

Thin-Film Solar Cells Market in South America is experiencing steady growth, driven by increasing energy demand and a growing awareness of renewable energy benefits. Brazil and Chile are the leading markets in the region, with favorable government policies and abundant solar resources. The expansion of solar power plants and the adoption of thin-film technologies for residential and commercial applications are key drivers of market growth. Furthermore, the region’s focus on energy access and rural electrification is creating opportunities for thin-film solar solutions.

Middle East & Africa

The Middle East & Africa thin-film solar cells market is poised for significant growth, driven by abundant solar resources and increasing investments in renewable energy projects. Countries like Saudi Arabia, the UAE, and South Africa are leading the way, with ambitious plans to diversify their energy mix and reduce their reliance on oil. The deployment of large-scale solar power plants and the adoption of thin-film technologies for water desalination and other applications are fueling market growth. Government initiatives promoting renewable energy and attracting foreign investment are further supporting the expansion of Thin-Film Solar Cells Market in the region.

Report Scope

This market research report provides a comprehensive analysis of the Thin-Film Solar Cells Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Thin-Film Solar Cells Market?

-> Thin-Film Solar Cells Market was valued at USD 6.8 billion in 2025 and is expected to reach USD 12.1 billion by 2034.

Which key companies operate in Thin-Film Solar Cells Market?

-> Key players include First Solar, Sharp Corporation, and Hanergy, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for lightweight and flexible energy solutions, continued cost reductions driven by advances in deposition technologies, and supportive government incentives for renewable energy deployment.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include integration of thin‑film photovoltaics into building‑integrated solutions, portable power applications, and ongoing improvements in material efficiencies such as a‑Si, CdTe, and CIGS technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...