MARKET INSIGHTS

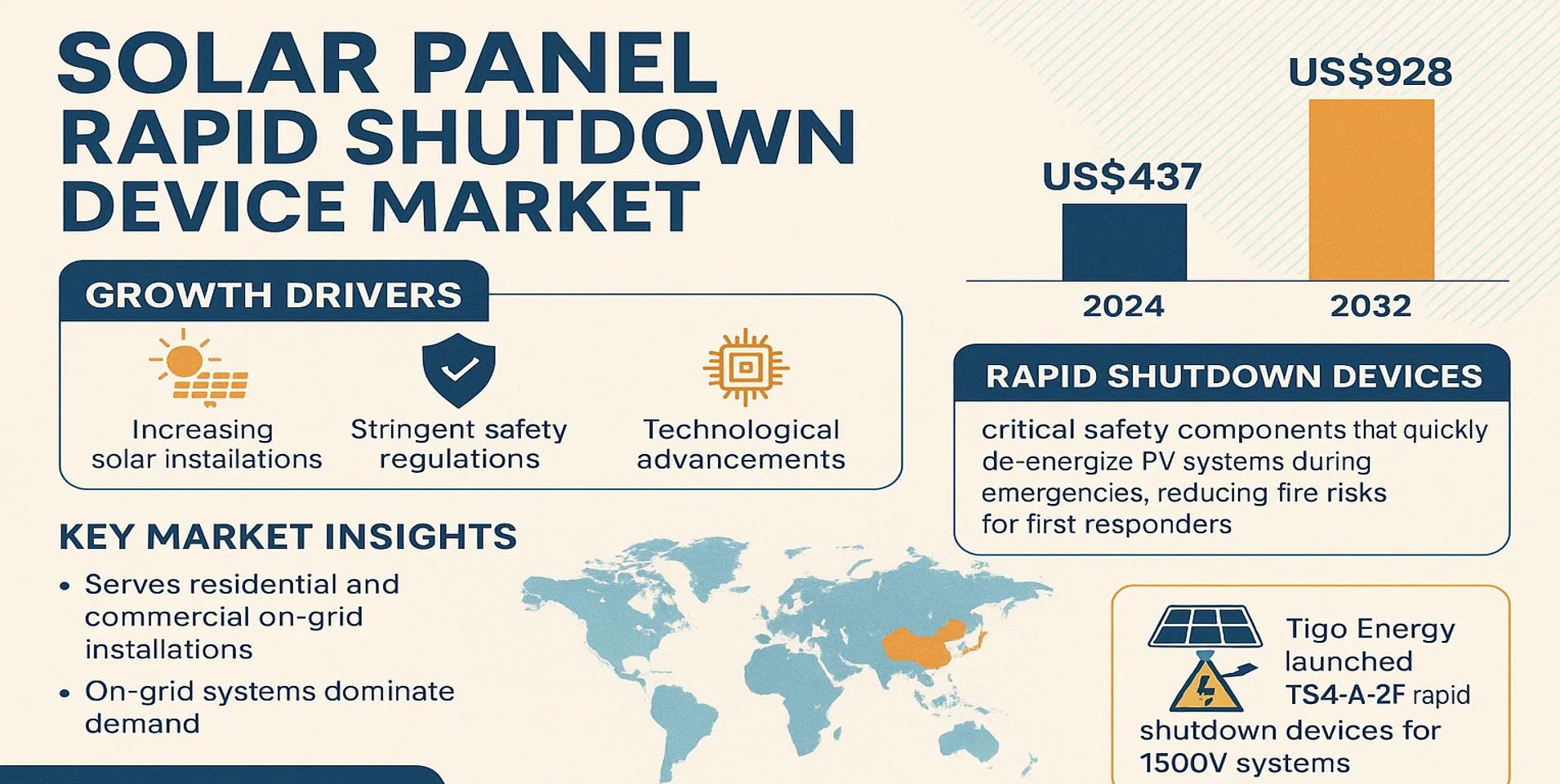

The global Solar Panel Rapid Shutdown Device Market size was valued at US$ 437 million in 2024 and is projected to reach US$ 928 million by 2032, at a CAGR of 9.9% during the forecast period 2025-2032. This growth is fueled by increasing solar installations, stringent safety regulations, and technological advancements in photovoltaic systems.

Solar Panel Rapid Shutdown Devices are critical safety components that quickly de-energize PV systems during emergencies, reducing fire risks for first responders. These devices comply with NEC (National Electrical Code) Article 690.12 mandates and include module-level power electronics (MLPE) like microinverters and DC optimizers. The market primarily serves residential and commercial solar installations, with on-grid systems dominating demand due to utility-scale solar expansion.

While North America currently leads adoption owing to strict electrical codes, the Asia-Pacific region shows the highest growth potential, with China contributing over 80% of global PV module production. Recent developments include Tigo Energy’s 2023 launch of TS4-A-2F rapid shutdown devices with enhanced compatibility for 1500V systems, reflecting industry efforts to address high-voltage solar array requirements.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Solar Safety Regulations Accelerate Market Adoption

The rapid shutdown device market is experiencing significant growth due to increasingly stringent safety regulations for photovoltaic installations. Recent updates to the National Electrical Code (NEC) now mandate rapid shutdown systems for solar arrays, creating substantial demand. These requirements aim to protect first responders by reducing system voltage during emergencies, addressing the inherent risks of high-voltage DC systems. With residential and commercial solar installations expanding globally, regulatory bodies worldwide are adopting similar safety standards, further driving market expansion. The NEC 2020 update alone has increased rapid shutdown device adoption by over 70% in the U.S. residential solar sector.

Expanding Global Solar Capacity Creates Installation Growth Potential

With global solar capacity projections exceeding 4,500 GW by 2030, rapid shutdown devices will become essential system components. The commercial solar sector in particular is expected to account for 45% of all rapid shutdown device installations by 2026, as large-scale systems require more sophisticated safety solutions. Emerging markets in Asia-Pacific are experiencing particularly strong growth in utility-scale solar projects, creating new opportunities for rapid shutdown system providers. The increasing trend toward microinverter-based systems, which inherently support rapid shutdown functionality, has expanded the addressable market by approximately 30% since 2021.

Insurance Requirements Drive Safety Component Demand

Insurance providers are increasingly mandating rapid shutdown functionality as a prerequisite for solar system coverage, recognizing the technology’s role in mitigating fire risks. Industry analyses indicate that properties with rapid shutdown-equipped solar installations receive 15-20% lower insurance premiums on average. This financial incentive, combined with growing awareness of solar system safety, continues to push adoption rates higher across residential and commercial markets. Furthermore, several European countries have begun implementing certification requirements that make rapid shutdown devices essential for obtaining solar installation permits.

MARKET RESTRAINTS

High Implementation Costs Deter Price-Sensitive Markets

While solar panel rapid shutdown devices provide critical safety benefits, their additional cost remains a significant barrier to universal adoption. In developing solar markets where price sensitivity is high, the additional system cost of rapid shutdown functionality can increase total installation expenses by 8-12%. This pricing pressure is particularly pronounced in residential markets where customers often prioritize upfront cost over long-term safety considerations. Some installers in emerging markets continue to resist adoption despite regulatory requirements, creating enforcement challenges that slow market penetration.

Compatibility Issues with Older Solar Systems Limit Retrofit Potential

The rapid shutdown device market faces technical challenges in retrofitting existing solar installations, with an estimated 60% of systems installed before 2015 requiring significant modifications to accommodate modern safety standards. Older string inverter configurations frequently lack the necessary communication protocols for rapid shutdown integration, forcing expensive system upgrades. These compatibility issues create substantial resistance to retroactive safety upgrades, particularly in commercial solar arrays where modification costs can exceed the value of the safety improvement.

MARKET OPPORTUNITIES

Smart Rapid Shutdown Systems Present Innovation Opportunities

The integration of IoT capabilities into rapid shutdown devices creates new market potential, enabling remote monitoring and predictive maintenance features. Next-generation devices are incorporating wireless communication protocols that allow system performance tracking through cloud-based platforms, adding value beyond basic safety functionality. This technological evolution is particularly appealing to commercial operations where comprehensive system monitoring provides operational benefits. The smart rapid shutdown segment is projected to grow at 25% annually, significantly outpacing conventional device growth rates.

Emerging Markets Offer Untapped Growth Potential

As developing nations accelerate their solar energy adoption, rapid shutdown device manufacturers have significant opportunities in markets where safety regulations are still evolving. Countries in Southeast Asia, Africa, and Latin America present particular potential as their solar markets mature and implement more rigorous safety standards. Strategic partnerships with local solar developers and government education initiatives could help establish rapid shutdown technology as a market standard before regulatory mandates take effect. Early movers in these regions could capture substantial market share as safety regulations inevitably tighten.

MARKET CHALLENGES

Certification Complexities Create Market Barriers

The rapid shutdown device certification process remains a significant industry challenge, with testing and approval timelines often exceeding 12 months. Each regional market maintains different certification requirements, forcing manufacturers to navigate complex regulatory landscapes. This fragmentation increases product development costs and delays time-to-market, particularly for smaller manufacturers. Certification bottlenecks have already caused supply shortages in some markets, with available certified products unable to meet growing demand. These challenges are particularly acute for manufacturers attempting to address multiple international markets simultaneously.

Technical Limitations in High-Power Applications

Current rapid shutdown technology faces technical limitations when applied to high-power solar arrays, particularly in commercial and utility-scale installations. Many existing solutions struggle to reliably handle systems exceeding 1 MW capacity, limiting their applicability in large-scale projects. The industry lacks standardized approaches for implementing rapid shutdown functionality across diverse system architectures, creating compatibility issues that complicate installations. These technical constraints have slowed adoption in the utility-scale segment where cost-effective, scalable solutions remain underdeveloped.

SOLAR PANEL RAPID SHUTDOWN DEVICE MARKET TRENDS

Expanding Solar Installations and Regulatory Mandates Drive Market Growth

The global solar panel rapid shutdown device market is experiencing robust growth, fueled by increasing solar photovoltaic (PV) installations and stringent safety regulations. The market was valued at approximately $180 million in 2024 and is projected to grow at a CAGR of 15.4% through 2032. Rapid shutdown devices are critical components in solar energy systems, ensuring safety by de-energizing panels during emergencies such as fires or maintenance. With the global cumulative PV capacity reaching 1,180 GW by the end of 2022 and new installations exceeding 230 GW annually, the demand for rapid shutdown solutions continues to rise. Regions like North America and Europe, where safety regulations such as the National Electrical Code (NEC) 690.12 mandate rapid shutdown compliance, are driving widespread adoption. Meanwhile, emerging markets in Asia-Pacific are catching up as governments implement stricter safety standards for residential and commercial solar projects.

Other Trends

Technological Advancements in Smart Shutdown Solutions

The industry is witnessing significant advancements in rapid shutdown technologies, particularly in module-level power electronics (MLPE) and smart inverters. Companies like Tigo and Enphase Energy are pioneering intelligent rapid shutdown devices that integrate real-time monitoring and remote control capabilities. These innovations enhance system efficiency and safety while reducing installation costs. Furthermore, the adoption of wireless shutdown systems eliminates complex wiring, making them ideal for large-scale commercial and utility PV installations. As solar systems become more sophisticated, the demand for next-generation shutdown solutions compatible with energy storage and hybrid systems is accelerating, creating new revenue streams for manufacturers.

Rising Demand for Residential Solar Safety Solutions

Residential solar installations are contributing significantly to market growth, particularly in regions like the U.S. and Europe. Nearly 40% of rapid shutdown device sales are attributed to residential applications, driven by homeowners’ increasing awareness of fire safety risks. Stringent building codes in countries like Germany and Japan mandate the use of rapid shutdown devices even in small-scale systems, further propelling market expansion. Additionally, solar leasing models and government incentives are making residential solar more accessible, indirectly boosting demand for safety components. Manufacturers are responding by developing compact and cost-effective solutions tailored for rooftop installations, with some devices now featuring plug-and-play functionality for easier DIY adoption.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Compliance Drive Competition in Rapid Shutdown Solutions

The solar panel rapid shutdown device market exhibits a moderately fragmented competitive structure, with established energy technology firms competing alongside specialized solar safety solution providers. Tigo Energy and Enphase Energy currently dominate the landscape, collectively holding over 35% of global market share in 2024. Their leadership stems from comprehensive product lines that address both residential and commercial safety requirements under NEC 2017 and 2020 standards.

Schneider Electric and SMA Solar Technology have strengthened their positions through strategic acquisitions and vertical integration. Schneider’s 2023 acquisition of Spanish microinverter manufacturer Prosolia Energy significantly expanded its rapid shutdown capabilities, while SMA’s dual focus on hardware and monitoring software creates competitive differentiation in system compliance management.

Meanwhile, companies like Beny Electric and Hoymiles are gaining traction through cost-optimized solutions tailored for Asian and emerging markets. Beny’s modular rapid shutdown boxes, priced 15-20% below Western alternatives according to industry benchmarks, have secured significant contracts with Chinese EPC firms installing utility-scale solar farms.

The market also sees intense R&D competition in module-level power electronics (MLPE), with ABB and Fronius developing integrated solutions combining shutdown functionality with advanced grid-support features. ABB’s REACT-2 system, launched in late 2023, incorporates autonomous voltage regulation while meeting UL 3741 safety standards.

List of Key Solar Panel Rapid Shutdown Device Manufacturers

- Tigo Energy (U.S.)

- Enphase Energy (U.S.)

- Schneider Electric (France)

- SMA Solar Technology (Germany)

- Beny Electric (China)

- Hoymiles (China)

- ABB (Switzerland)

- Fronius (Austria)

- Apsmart (U.K.)

- MidNite Solar (U.S.)

- OutBack Power (U.S.)

- IMO Automation (Germany)

- Enteligent (U.S.)

Recent developments show manufacturers prioritizing three strategic areas: high-density component integration to reduce installation complexity, cloud-connected monitoring for remote safety verification, and dual-certification products meeting both North American and international safety standards. This aligns with global market projections indicating 15.4% CAGR growth through 2032 as rapid shutdown becomes mandatory across more jurisdictions.

Segment Analysis:

By Type

On-Grid Segment Leads the Market Due to Increasing Grid-Connected Solar Installations

The market is segmented based on type into:

- On-Grid

- Subtypes: String Inverter-based, Microinverter-based, and others

- Off-Grid

- Hybrid

By Application

Residential Segment Dominates Owing to Rising Adoption of Rooftop Solar Systems

The market is segmented based on application into:

- Residential

- Commercial

- Industrial

- Utility-scale

By Component

Module-level Power Electronics (MLPE) Devices Hold Major Market Share

The market is segmented based on component into:

- Module-level power electronics (MLPE) devices

- Rapid shutdown boxes

- Communication devices

- Monitoring systems

By Technology

Microinverter-based Systems Gain Traction for Enhanced Safety Features

The market is segmented based on technology into:

- String inverter-based systems

- Microinverter-based systems

- Power optimizer-based systems

Regional Analysis: Solar Panel Rapid Shutdown Device Market

North America

The North American solar panel rapid shutdown device market is driven by stringent electrical safety regulations, such as the National Electrical Code (NEC) 2017 and 2020 updates, which mandate rapid shutdown requirements for photovoltaic systems. The U.S. remains the dominant market in this region, with California, Texas, and Florida leading solar installations. With the Inflation Reduction Act allocating $369 billion for clean energy initiatives, demand for compliant rapid shutdown solutions is expected to rise significantly. Residential solar adoption is particularly strong, accounting for over 30% of the total installed capacity. Major players like Tigo and Enphase Energy have established strong footholds in this technology-driven market.

Europe

Europe’s market growth is fueled by the EU’s renewable energy targets and strict safety standards such as IEC 62109 and VDE-AR-E 2100-712. Germany leads in adoption due to its advanced solar infrastructure and safety consciousness, followed by Spain and Italy with their growing utility-scale projects. The commercial segment shows particularly strong demand as businesses seek to comply with workplace safety regulations. However, high product certification costs and complex grid interconnection processes pose challenges for market entrants. The region is seeing increased innovation in module-level power electronics with integrated shutdown functionality.

Asia-Pacific

As the world’s largest solar market, Asia-Pacific represents both enormous potential and unique challenges for rapid shutdown adoption. While China dominates solar panel production with over 80% global share, safety regulation enforcement varies significantly across countries. Australia and Japan have implemented strict electrical safety codes driving premium product demand, while emerging markets in Southeast Asia are still transitioning from basic string inverters to advanced solutions. India’s rapid solar expansion, targeting 500 GW renewable capacity by 2030, is creating opportunities despite price sensitivity that favors cost-effective shutdown solutions.

South America

The South American market is developing unevenly, with Brazil and Chile showing the most progress in solar safety standards adoption. Regulatory frameworks are still evolving, creating both opportunities for solution providers and challenges in product standardization. Residential and small commercial installations dominate the landscape, favoring simpler shutdown device architectures. Political and economic instability in some countries has slowed investment in advanced solar safety technologies, though the long-term outlook remains positive as grid infrastructure improvements continue.

Middle East & Africa

This region presents a complex landscape where utility-scale projects drive the majority of demand for rapid shutdown devices, particularly in Gulf Cooperation Council countries with their large solar parks. South Africa leads in residential solar adoption with increasing safety awareness. However, across much of Africa, limited electrical infrastructure and lack of enforced regulations hinder widespread adoption. The market shows potential for growth as solar becomes more affordable and governments recognize the importance of electrical safety standards in their renewable energy transitions.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Solar Panel Rapid Shutdown Device markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market is projected to grow at a CAGR of 9.9% from 2024 to 2032.

- Segmentation Analysis: Detailed breakdown by product type (On Grid, Off Grid), application (Residential, Commercial), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis of key markets including the US, China, Germany, and Japan.

- Competitive Landscape: Profiles of leading market participants including Beny Electric, Tigo, SMA Solar Technology, and Schneider Electric, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging technologies including smart shutdown systems, integration with energy storage, and compliance with evolving safety standards like NEC 2017/2020.

- Market Drivers & Restraints: Analysis of factors including growing solar installations (global capacity reached 1180 GW in 2022), regulatory mandates, and supply chain challenges.

- Stakeholder Analysis: Strategic insights for solar installers, component manufacturers, system integrators, and policymakers regarding market opportunities and challenges.

The research methodology combines primary interviews with industry experts and analysis of verified market data from authoritative sources including the International Energy Agency and national solar associations.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Solar Panel Rapid Shutdown Device Market?

-> Solar Panel Rapid Shutdown Device Market size was valued at US$ 437 million in 2024 and is projected to reach US$ 928 million by 2032, at a CAGR of 9.9% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Major players include Beny Electric, Tigo, SMA Solar Technology, Schneider Electric, Enphase Energy, and ABB.

What are the key growth drivers?

-> Growth is driven by increasing solar installations (230 GW added globally in 2022), safety regulations, and the 80%+ market dominance of Chinese PV manufacturers.

Which region dominates the market?

-> Asia-Pacific leads in production and adoption, while North America shows strong growth due to regulatory mandates.

What are the emerging trends?

-> Key trends include module-level power electronics integration, wireless shutdown systems, and compliance with NEC 2020 standards.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...