MARKET INSIGHTS

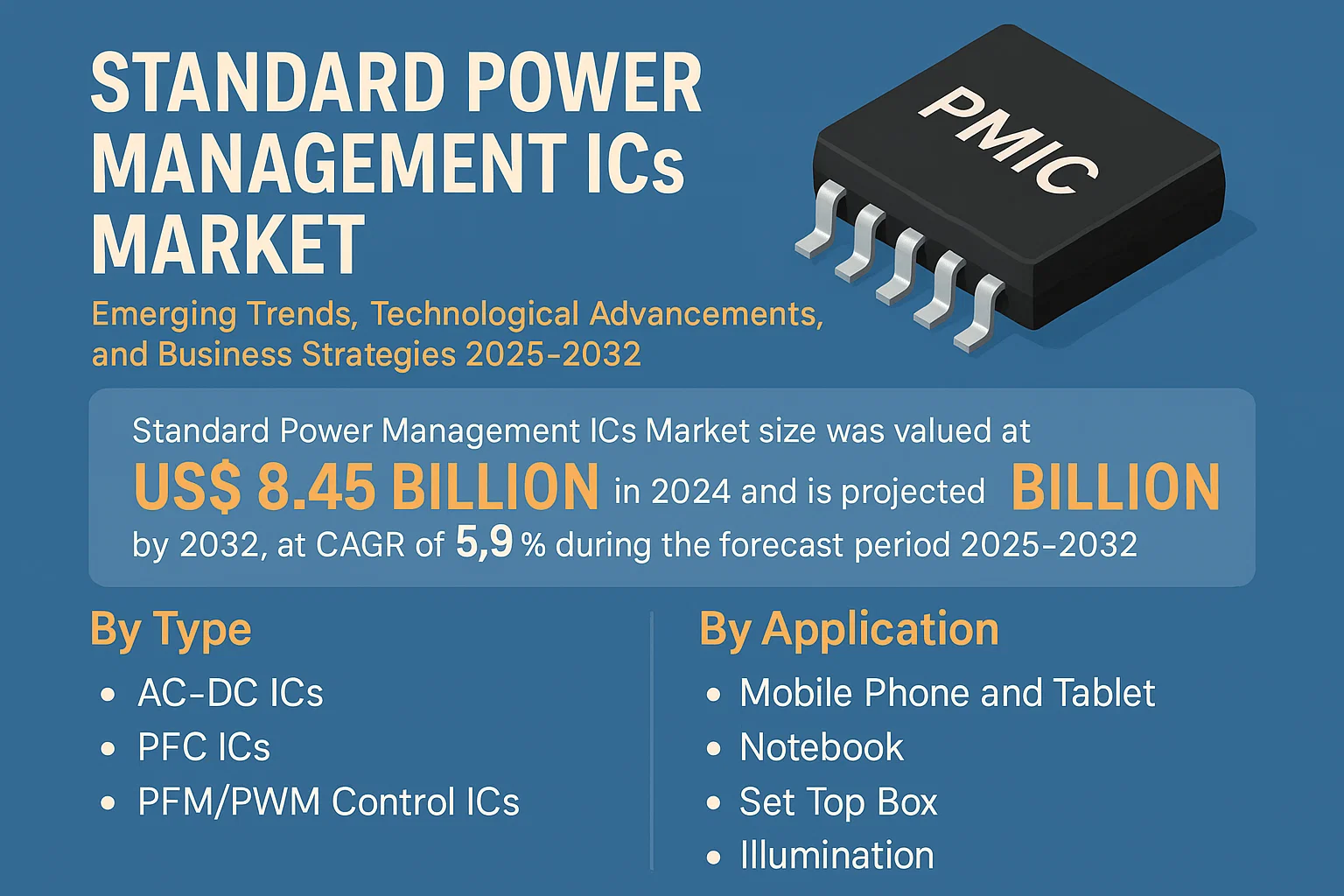

Global Standard Power Management ICs Market size was valued at US$ 8.45 billion in 2024 and is projected to reach US$ 12.67 billion by 2032, at a CAGR of 5.9% during the forecast period 2025-2032

Standard Power Management ICs are specialized semiconductor devices that regulate and distribute power in electronic systems. These chips play a critical role in converting and managing power efficiently across various applications, including AC-DC conversion, power factor correction (PFC), and pulse-width modulation (PWM) control. The key product segments include AC-DC ICs, PFC ICs, and PFM/PWM Control ICs, among others.

The market growth is driven by increasing demand for energy-efficient power solutions across consumer electronics, industrial applications, and automotive sectors. While the U.S. currently leads with a 28% market share, China’s rapid adoption of smart devices is fueling its growth trajectory. Notably, the AC-DC ICs segment is expected to dominate with 42% market share by 2032, supported by rising needs for fast-charging technologies. Key players like Texas Instruments and MPS collectively hold over 35% of the global market, with recent advancements focusing on miniaturization and thermal efficiency.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Consumer Electronics to Accelerate Market Expansion

The exponential growth in consumer electronics adoption is fueling demand for standard power management ICs globally. With over 6.8 billion smartphone users worldwide, the need for efficient power conversion solutions in charging adapters remains critical. Modern mobile devices require compact yet powerful PMICs that support fast charging protocols while minimizing energy loss. Leading manufacturers are responding with innovative solutions – Texas Instruments recently introduced a 98% efficiency AC-DC converter chip optimized for smartphone charger applications. This trend directly translates to increased PMIC integration across power supply designs.

Energy Efficiency Regulations to Stimulate Innovation

Stringent global energy efficiency standards are compelling power supply manufacturers to adopt advanced PMIC solutions. Regulatory frameworks like the EU’s Ecodesign Directive and the U.S. Department of Energy’s efficiency benchmarks have raised the performance bar for external power adapters by 15-20% over the past five years. Standard PMICs now incorporate sophisticated features including active burst mode operation and ultra-low standby power consumption below 10mW. This regulatory pressure has accelerated R&D investments, with leading players dedicating 8-12% of annual revenues to developing next-generation power conversion technologies.

5G Infrastructure Rollout to Create New Demand Channels

The global 5G network expansion presents significant opportunities for standard power management IC manufacturers. Each 5G small cell base station typically requires multiple PMICs for power conversion and distribution. With projections indicating over 7 million 5G base stations to be deployed by 2028, the demand for reliable AC-DC and DC-DC conversion chips is expected to grow substantially. Power Integrations recently unveiled a new line of PFC controllers specifically designed for 5G power supply applications, demonstrating how industry leaders are positioning themselves to capitalize on this infrastructure wave.

MARKET RESTRAINTS

Supply Chain Disruptions to Constrain Market Growth

The semiconductor industry continues to face significant supply chain challenges that impact PMIC production and delivery. While the global chip shortage has eased from its peak, lead times for certain power management ICs remain extended beyond 20 weeks for some product categories. Geopolitical tensions and export controls have further complicated procurement of raw materials like silicon wafers and specialized packaging components. These constraints are particularly acute for small-to-medium manufacturers lacking long-term supply agreements with foundry partners.

Price Competition from Regional Players to Squeeze Margins

The emergence of Chinese power IC manufacturers offering competitively priced alternatives is pressuring established suppliers’ profitability. Domestic players like Chipown and Silergy Corporation have gained notable market share in cost-sensitive segments through aggressive pricing strategies and government subsidies. This intensified competition has forced global leaders to reduce prices by 8-12% on mainstream PMIC products over the past two years, impacting overall industry revenue growth despite increasing unit volumes.

MARKET OPPORTUNITIES

GaN Technology Adoption to Unlock Next-Level Performance

The transition to gallium nitride (GaN) based power ICs represents a transformative opportunity for the industry. GaN solutions offer up to 65% improvement in power density compared to traditional silicon-based chips, enabling smaller and more efficient power adapters. Market penetration of GaN PMICs in fast chargers has already exceeded 25% for premium smartphones, with projections indicating this could surpass 50% by 2027. Several leading vendors including Navitas Semiconductor and Power Integrations have introduced GaN integrated circuits that combine multiple power management functions into single-chip solutions.

Industrial Automation Growth to Drive PMIC Demand

The accelerating adoption of industrial automation systems creates significant potential for specialized power management ICs. Modern factories require rugged PMICs that can operate in harsh environments while delivering precise voltage regulation for sensitive control systems. According to industry estimates, the average automated production line now incorporates 30-40 separate power management components. This demand has prompted companies like Texas Instruments to develop industrial-grade PMICs with extended temperature ranges (-40°C to +125°C) and enhanced electromagnetic interference protection.

MARKET CHALLENGES

Design Complexity to Increase Development Costs

The growing sophistication of power management ICs is significantly raising design and validation expenses. Modern PMICs now integrate multiple functional blocks including digital control loops, protection circuits, and communication interfaces. Developing such complex chips requires substantial engineering resources – approximately 18-24 months from concept to volume production for advanced designs. This extended development timeline and the need for specialized expertise in mixed-signal design create substantial barriers to entry for new market participants.

Global Economic Uncertainty to Impact Investment Decisions

Economic volatility and inflationary pressures are causing equipment manufacturers to reassess their PMIC procurement strategies. Many mid-market power supply companies have delayed upgrading to newer generation power management solutions due to budget constraints. This cautious approach is particularly evident in consumer electronics segments, where some brands extended product refresh cycles by 6-12 months. Such market conditions create unpredictable demand patterns that complicate production planning and inventory management for PMIC suppliers.

STANDARD POWER MANAGEMENT ICS MARKET TRENDS

Growth in Consumer Electronics to Drive Demand for Power Management ICs

The proliferation of smartphones, tablets, and portable devices continues to fuel the demand for efficient power management ICs. With global smartphone shipments exceeding 1.2 billion units annually, manufacturers are increasingly adopting advanced power management solutions that optimize battery life and thermal performance. The shift toward USB Power Delivery (PD) and fast charging technologies has further accelerated the need for sophisticated AC-DC converters and voltage regulators. Additionally, the growing adoption of OLED displays, which require precise power delivery, has created new opportunities for specialized PMICs in the consumer electronics segment.

Other Trends

Energy Efficiency Regulations

Stringent energy efficiency standards worldwide are compelling manufacturers to develop power management ICs with lower standby power consumption. Regulations like the European Union’s Ecodesign Directive, which mandates less than 0.5W standby power for external power supplies, have pushed innovation in low-power PFC (Power Factor Correction) ICs. The industry is responding with solutions that achieve conversion efficiencies above 94%, significantly reducing energy waste in both active and standby modes across applications from adapters to industrial power systems.

Integration of Advanced Technologies

The power management IC landscape is being transformed by the integration of wide bandgap semiconductors like GaN (Gallium Nitride) and SiC (Silicon Carbide). These materials enable higher switching frequencies, smaller form factors, and better thermal performance compared to traditional silicon-based solutions. GaN-based power ICs are particularly gaining traction in fast charging applications, with the market expected to grow at over 30% CAGR as they become cost-competitive. Meanwhile, the adoption of digital power management techniques allows for more intelligent control and monitoring of power delivery, creating new possibilities in adaptive voltage scaling and dynamic power optimization.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Leadership in Power Management IC Segment

The global standard power management IC market exhibits a dynamic competitive landscape characterized by the presence of established semiconductor giants alongside emerging regional players. Market intelligence reveals that the top five manufacturers collectively held approximately 42% revenue share in 2024, indicating moderate market concentration.

Texas Instruments maintains its position as the market leader, leveraging its extensive product portfolio covering AC-DC controllers, battery management ICs, and voltage regulators. The company’s technological edge stems from its Fab-Lite manufacturing strategy and consistent R&D investments exceeding 10% of annual revenues.

Meanwhile, MPS (Monolithic Power Systems) has demonstrated remarkable growth through its focus on high-efficiency power solutions for mobile and computing applications. The company’s proprietary ‘MP’ branded chips have gained significant traction in notebook and tablet segments, contributing to its 14% market share growth last fiscal year.

The competitive intensity is further amplified by Chinese manufacturers like Chipown and Sino Wealth Electronic who are capturing market share through cost-optimized solutions for consumer electronics. These domestic players benefit from China’s robust electronics manufacturing ecosystem and government support for semiconductor self-sufficiency.

Silergy Corporation and Power Integrations are responding to competitive pressures through technological differentiation. Silergy’s recent gallium nitride (GaN) based power ICs demonstrate 94% power conversion efficiency, while Power Integrations continues to dominate in compact USB PD controller solutions.

List of Key Standard Power Management IC Companies Profiled

- Texas Instruments (U.S.)

- Monolithic Power Systems (U.S.)

- Power Integrations (U.S.)

- Silergy Corporation (China)

- On-Bright Electronics Incorporated (China)

- Chipown (China)

- Sino Wealth Electronic (China)

- VeriSilicon (China)

- MR Semiconductor (China)

- Hangzhou Silan Microelectronics (China)

- Fine Made Microelectronics (Taiwan)

- SG Micro (China)

- Will Semiconductor (China)

Segment Analysis:

By Type

AC-DC ICs Segment Dominates the Market Due to Widespread Use in Power Supply Units

The market is segmented based on type into:

- AC-DC ICs

- Primary applications: Power adapters, chargers, LED drivers

- PFC ICs

- Primary applications: High-efficiency power supplies, industrial equipment

- PFM/PWM Control ICs

- Others

- Includes: Battery management ICs, voltage regulators

By Application

Mobile Phone and Tablet Segment Leads Due to Increasing Smart Device Penetration

The market is segmented based on application into:

- Mobile Phone and Tablet

- Notebook

- Set Top Box

- Illumination

- Other

- Includes: Industrial automation, automotive electronics

Regional Analysis: Standard Power Management ICs Market

North America

The North American Standard Power Management ICs market is driven by high adoption of advanced electronics across industries such as consumer electronics, automotive, and industrial automation. The U.S., accounting for a large share of global demand, benefits from strong R&D investments from leading players like Texas Instruments and Monolithic Power Systems. The region emphasizes energy-efficient power management solutions, particularly for fast-charging smartphone adapters and data center applications. Strict efficiency standards like ENERGY STAR and DOE regulations push manufacturers to innovate in AC-DC and PFC IC segments. However, supply chain disruptions and semiconductor shortages continue to pose challenges.

Europe

Europe’s market is shaped by rigorous energy efficiency policies, including the EU’s Ecodesign Directive and stringent power consumption standards. Germany, France, and the U.K. are key contributors, with demand driven by industrial automation, automotive electrification, and smart home adoption. Companies such as Power Integrations and Infineon lead in developing high-efficiency power conversion solutions for renewable energy systems and electric vehicle chargers. While the market remains technology-driven, high manufacturing costs and import dependency on Asian suppliers create pricing pressure.

Asia-Pacific

China dominates the Asia-Pacific market, fueled by its massive electronics manufacturing sector and growing domestic demand for smartphones, PCs, and IoT devices. The region is also the manufacturing hub for power ICs, with key players like Silergy Corporation and Will Semiconductor expanding production capacity. India and Southeast Asia are emerging markets, buoyed by government initiatives promoting domestic semiconductor manufacturing. The focus remains cost-competitive solutions, though demand for premium power management ICs in automotive and 5G infrastructure is rising. Intense local competition and pricing pressures slightly offset the growth potential.

South America

South America’s market is nascent but growing, primarily driven by Brazil and Argentina, where increasing smartphone penetration and renewable energy projects create demand for power ICs. However, economic instability and limited semiconductor ecosystem development constrain market expansion. Import reliance on North American and Asian suppliers leads to supply chain inefficiencies. Nonetheless, the gradual adoption of energy-efficient electronics in urban centers offers long-term opportunities for standardized power management solutions.

Middle East & Africa

The market here is in the early growth phase, with the UAE, Saudi Arabia, and South Africa emerging as key markets due to smart infrastructure projects and increasing consumer electronics demand. Power IC applications in solar energy systems and telecommunications are gaining traction. However, limited local production capabilities and reliance on imports slow market penetration. As digital transformation accelerates, demand for reliable power management ICs is expected to rise, particularly for data centers and industrial applications.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Standard Power Management ICs market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Standard Power Management ICs market was valued at USD million in 2024 and is projected to reach USD million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (AC-DC ICs, PFC ICs, PFM/PWM Control ICs, Others), application (Mobile Phone and Tablet, Notebook, Set Top Box, Illumination, Other), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading participants including Texas Instruments, MPS, Power Integrations, Silergy Corporation, and regional players like Chipown and Sino Wealth Electronic, covering their product portfolios and strategic developments.

- Technology Trends & Innovation: Assessment of evolving power conversion technologies, integration with smart devices, and energy efficiency improvements in semiconductor design.

- Market Drivers & Restraints: Evaluation of factors such as growing demand for consumer electronics, EV charging infrastructure, and challenges like supply chain constraints.

- Stakeholder Analysis: Strategic insights for chip manufacturers, OEMs, suppliers, and investors regarding market opportunities and competitive positioning.

The research employs primary and secondary methodologies including manufacturer surveys, industry expert interviews, and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Standard Power Management ICs Market?

->Standard Power Management ICs Market size was valued at US$ 8.45 billion in 2024 and is projected to reach US$ 12.67 billion by 2032, at a CAGR of 5.9% during the forecast period 2025-2032

Which key companies operate in this market?

-> Key players include Texas Instruments, MPS (Monolithic Power Systems), PI (Power Integrations), Silergy Corporation, Chipown, and Sino Wealth Electronic, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for consumer electronics, EV charging infrastructure development, and increasing power efficiency requirements.

Which region dominates the market?

-> Asia-Pacific is the largest market, driven by electronics manufacturing in China and South Korea, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include integration of GaN technology, development of ultra-low-power ICs, and smart power management solutions for IoT devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...