MARKET INSIGHTS

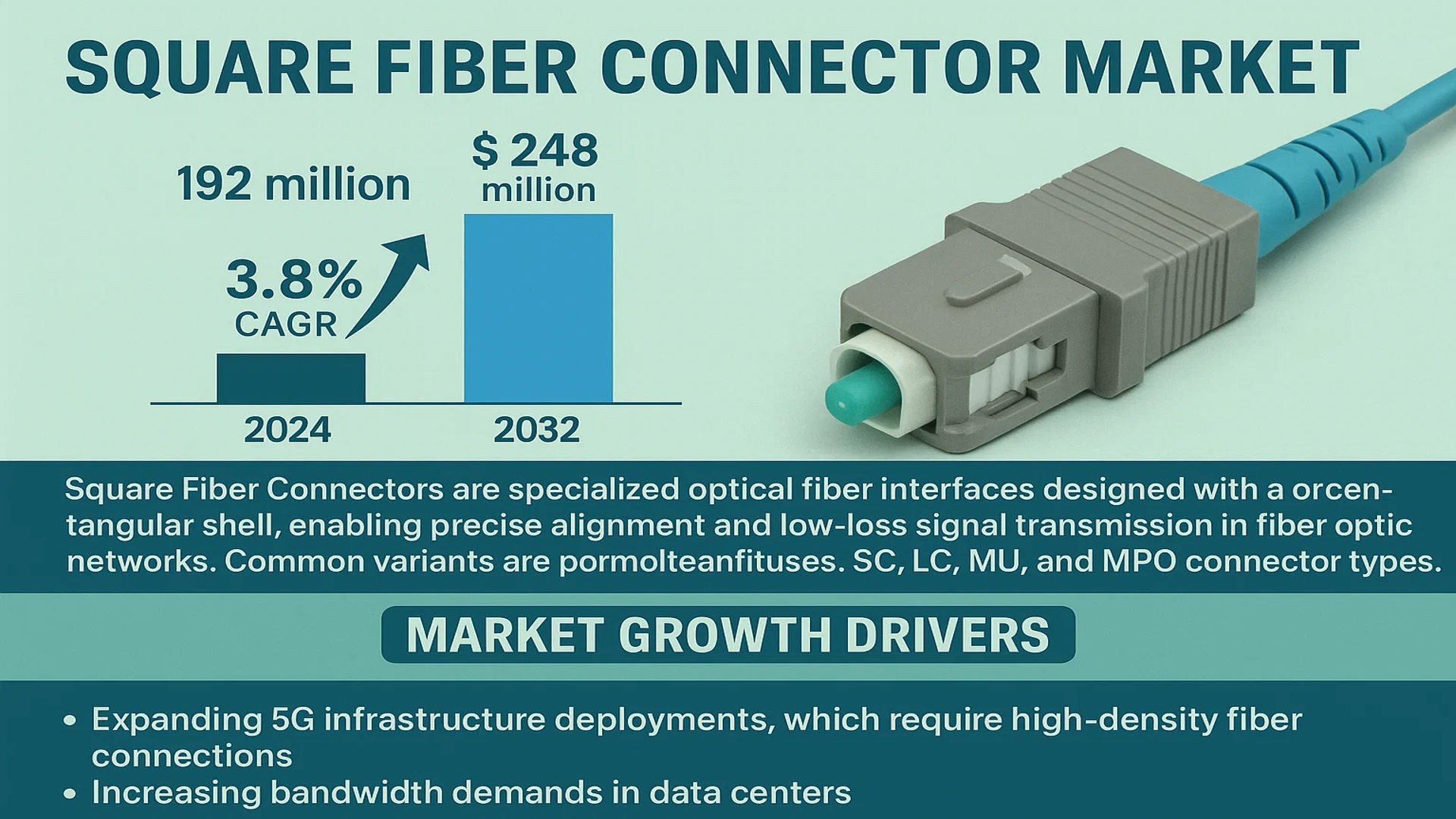

The global Square Fiber Connector Market was valued at 192 million in 2024 and is projected to reach US$ 248 million by 2032, at a CAGR of 3.8% during the forecast period.

Square Fiber Connectors are specialized optical fiber interfaces designed with a rectangular shell, enabling precise alignment and low-loss signal transmission in fiber optic networks. These connectors play a critical role in telecom, broadcast, military, and aerospace applications by ensuring reliable connections between optical fibers while minimizing insertion loss (typically below 0.3 dB) and reflection loss (under -55 dB). Common variants include SC, LC, MU, and MPO connector types, each optimized for specific performance requirements.

Market growth is being driven by expanding 5G infrastructure deployments, which require high-density fiber connections, and increasing bandwidth demands in data centers. While North America currently leads in adoption with 38% market share, Asia-Pacific is experiencing faster growth at 4.5% CAGR due to rapid digitalization. Key players like Amphenol and TE Connectivity are investing in advanced manufacturing techniques to meet evolving industry standards for higher port density and easier field termination.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth in Data Center Expansion Elevates Demand for Square Fiber Connectors

The global surge in hyperscale data center construction is significantly driving demand for square fiber connectors in high-density applications. With data traffic projected to grow at a compound annual rate exceeding 25% through 2030, infrastructure upgrades are mandatory to support bandwidth-intensive applications. These connectors offer space-efficient solutions in rack-mounted systems where real estate optimization is critical. Their rectangular design allows for tighter packing density compared to traditional circular connectors – a key advantage when modern data centers may contain over 100,000 fiber connections per facility.

Military Modernization Programs Accelerate Adoption in Defense Applications

Defense sector investments in secure fiber optic communication networks are creating substantial demand for ruggedized square fiber connectors. Modern warfare systems require lightweight, high-reliability interconnects that maintain signal integrity in harsh environments. The MPO variant sees particularly strong uptake in avionics systems, where its square form factor enables modular cable management in confined aircraft spaces. Global defense budgets allocated to communications infrastructure have shown consistent 5-7% annual growth, directly benefiting specialized connector manufacturers.

Furthermore, the connectors’ superior EMI shielding performance makes them indispensable for electronic warfare systems where signal leakage could prove catastrophic.

➤ The U.S. Department of Defense recently mandated MIL-STD-2042 compliance for all new fiber optic termination systems – a specification where square connectors frequently outperform traditional designs in shock/vibration testing.

Manufacturers are responding with innovative sealing technologies that maintain optical performance across extreme temperature ranges from -55°C to +125°C.

MARKET RESTRAINTS

Precision Manufacturing Requirements Elevate Production Costs

The square fiber connector market faces significant cost barriers due to stringent manufacturing tolerances. Achieving reliable multimode performance requires alignment precision within 5μm – a specification demanding expensive CNC machining and active alignment systems during assembly. These technical requirements result in per-unit costs 30-50% higher than standard circular connectors, creating adoption resistance in price-sensitive market segments

Additional Constraints

Installation Complexity

Field termination of square connectors requires specialized tooling and trained technicians, unlike simpler screw-type circular alternatives. The learning curve for proper polishing and inspection procedures adds considerable labor costs to deployment projects.

Durability Concerns

While designed for high mating cycles, square connectors demonstrate 15-20% lower insertion durability than military-spec circular designs in accelerated life testing. This performance gap limits their use in applications requiring frequent connection changes.

MARKET OPPORTUNITIES

5G Infrastructure Rollout Creates New Application Horizons

The ongoing global 5G deployment represents a transformative opportunity for square fiber connector suppliers. Small cell networks demand compact, high-density interconnects at both radio units and centralized offices. The SC square connector variant shows particular promise for fronthaul applications where its 2.5mm ferrule design enables space-efficient multiplexing. Early adopters report 40% space savings in outdoor cabinets when transitioning from traditional form factors.

Furthermore, the anticipated 400G Ethernet upgrade cycle in carrier networks will drive demand for high-channel-count MPO solutions. Square connectors’ parallel optics compatibility positions them as the preferred choice for next-generation backhaul links.

MARKET CHALLENGES

Industry Standardization Lag Creates Compatibility Issues

The square fiber connector market faces significant interoperability challenges due to competing proprietary designs. Unlike the mature circular connector ecosystem with well-established IEC and MIL standards, square variants suffer from fragmented specifications across manufacturers. This lack of uniformity leads to mating incompatibilities that can increase system integration costs by up to 25% when mixed-vendor deployments occur.

Emerging Technical Hurdles

Signal Degradation at Higher Frequencies

Testing reveals increasing insertion loss variance above 25GHz – a growing concern as networks transition to 56G PAM4 signaling. The square form factor presents unique challenges in maintaining consistent impedance across all channels.

Supply Chain Vulnerabilities

Specialized ceramics and precision alignment sleeves face periodic shortages, with lead times extending beyond 26 weeks during demand surges. These bottlenecks threaten to constrain market growth during critical infrastructure buildout phases.

SQUARE FIBER CONNECTOR MARKET TRENDS

5G Network Expansion Drives Demand for High-Performance Fiber Connectors

The global deployment of 5G networks is creating significant demand for high-performance fiber optic infrastructure, including square fiber connectors. These specialized connectors play a critical role in backhaul and fronthaul networks, where they ensure low-loss signal transmission between base stations and core networks. With over 1.3 billion 5G connections projected worldwide by 2024, telecom operators are increasingly adopting rectangular form factor connectors like SC and LC variants for their space efficiency in dense network environments. The compact design of square connectors proves particularly valuable in urban deployments where real estate for network equipment comes at a premium.

Other Trends

Military and Aerospace Sector Adoption

Military and aerospace applications are emerging as key growth drivers for ruggedized square fiber connector solutions. The superior vibration resistance and EMI shielding capabilities of military-grade rectangular connectors make them ideal for harsh environment deployments. Modern fighter jets now incorporate hundreds of fiber optic connections, with square connectors preferred for their reliable performance in high-G environments. Similarly, space agencies increasingly specify rectangular fiber interfaces for satellite communications systems where weight savings and reliability are paramount considerations.

Data Center Modernization Fuels MPO Connector Growth

The ongoing transition to 400G and 800G data center architectures is accelerating adoption of multi-fiber push-on (MPO) square connectors. These high-density solutions enable efficient management of growing bandwidth demands while minimizing rack space consumption. Industry assessments indicate MPO-based square connectors now account for over 25% of new hyperscale data center interconnects. The technology’s plug-and-play functionality significantly reduces deployment time compared to traditional splicing methods, a critical advantage for operators facing tight project timelines. Furthermore, the parallel optics capabilities of MPO connectors align perfectly with the requirements of AI/ML workloads that dominate modern data center traffic patterns.

Miniaturization Trend Reshapes Product Development

Connector manufacturers are responding to industry demands for smaller form factors without compromising performance. The development of ultra-compact square connectors with sub-1dB insertion loss represents a significant technical achievement, enabling high-density installations in space-constrained environments. Recent product introductions feature innovative latching mechanisms that maintain secure connections while reducing the overall connector footprint. This miniaturization wave particularly benefits medical imaging equipment and industrial automation systems where component size directly impacts product design flexibility.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Drive Innovation Through Product Diversification and Strategic Partnerships

The global square fiber connector market showcases a competitive yet fragmented landscape, with several key players dominating the industry due to their technological expertise and extensive distribution networks. Amphenol Corporation leads the market with a strong presence across telecom, military, and aerospace applications, leveraging its high-performance connector solutions to maintain a competitive edge. In 2024, the company accounted for nearly 18% of the global square fiber connector revenue, driven by its focus on low-loss and high-density connectivity solutions.

TE Connectivity and Corning Incorporated are other prominent contenders, collectively holding approximately 25% market share as of 2024. TE Connectivity has been expanding its MPO and LC connector portfolios to cater to 5G infrastructure demands, while Corning continues to innovate in ultra-low-loss fiber optic solutions for hyperscale data centers. Both companies are actively investing in R&D to develop next-gen square fiber connectors capable of handling 400G and 800G transmission speeds.

Meanwhile, specialized players like Yamaichi Electronics and Glenair are making significant strides in niche applications such as harsh-environment connectivity for defense and industrial sectors. Yamaichi’s latest solderless square fiber connectors have gained traction in military avionics, while Glenair’s ruggedized rectangular fiber optic solutions are becoming industry standards in oil & gas applications.

The competitive landscape is further shaped by regional leaders expanding globally. Fujikura Ltd. maintains strong positions in Asia-Pacific markets, particularly in Japan and China, through strategic collaborations with local telecom providers. Similarly, CommScope continues to strengthen its foothold in North America and Europe through acquisitions and continuous product line extensions in high-density connectivity solutions.

List of Key Square Fiber Connector Manufacturers

- Amphenol Corporation (U.S.)

- TE Connectivity (Switzerland)

- Corning Incorporated (U.S.)

- Infinite Electronics (U.S.)

- Yamaichi Electronics (Germany)

- Glenair (U.S.)

- Fujikura Ltd. (Japan)

- CommScope (U.S.)

- Cinch Connectivity Solutions (U.S.)

- Eaton Corporation (Ireland)

Segment Analysis:

By Type

SC Connectors Hold the Largest Market Share Due to Their Widespread Use in Telecommunication Networks

The market is segmented based on type into:

- SC Connectors

- LC Connectors

- MU Connectors

- MPO Connectors

By Application

Telecom Sector Leads Due to High Demand for High-Speed Data Transmission

The market is segmented based on application into:

- Telecom

- Broadcast

- Military

- Aerospace

- Subtypes: Avionics, Communication systems, and others

- Others

By End-User

Commercial Sector Dominates with Significant Adoption in Data Centers and Enterprise Networks

The market is segmented based on end-user into:

- Commercial

- Industrial

- Government

Regional Analysis: Square Fiber Connector Market

Asia-Pacific

The Asia-Pacific region dominates the global Square Fiber Connector market, driven by rapid telecom infrastructure expansion, government-backed digitalization initiatives, and growing demand for high-speed connectivity. China accounts for over 40% of regional demand, owing to massive 5G deployment projects and extensive fiber-to-the-home (FTTH) rollouts. India follows closely with increasing investments in smart city projects requiring high-density fiber connectivity. Japan and South Korea remain innovation hubs for advanced connector technologies, with manufacturers like Fujikura and Yamaichi Electronics leading R&D initiatives. While cost competition remains fierce across developing markets, there’s a noticeable shift toward higher-grade connectors as network reliability gains importance alongside bandwidth demands.

North America

North America represents the second-largest Square Fiber Connector market, characterized by stringent performance standards and early adoption of next-gen connectivity solutions. The U.S. leads with substantial data center buildouts – over 300 MW of capacity was added in 2023 alone – driving demand for high-density MPO-style square connectors. Major cloud providers’ hyperscale investments and federal broadband funding programs (including the $42.45 billion BEAD initiative) create sustained demand. Canadian markets emphasize ruggedized connectors for harsh environment applications in energy and defense sectors. The region sees strong competition between established players like Corning and TE Connectivity versus innovative startups specializing in compact form factors.

Europe

Europe’s Square Fiber Connector market benefits from harmonized telecom regulations and concentrated fiber deployment across EU member states. Germany and France account for nearly half of regional consumption, with particular strength in industrial and broadcast applications requiring robust connectivity. The EU’s Digital Decade targets (including universal gigabit connectivity by 2030) accelerate demand, though approval processes for new infrastructure sometimes delay deployments. Sustainability concerns drive innovations in connector materials and manufacturing processes, with companies like Neutrik leading in eco-design. Eastern European markets show growing potential as digital infrastructure gaps are addressed, though price sensitivity remains higher compared to Western Europe.

South America

South America presents a developing market for Square Fiber Connectors, with Brazil representing over 60% of regional demand. Growing mobile broadband penetration and submarine cable landing points drive connectivity needs, though economic volatility sometimes disrupts procurement cycles. Argentina and Chile show increasing adoption in data center applications, while Andean markets remain constrained by mountainous terrain challenges. Local manufacturing remains limited, with most connectors imported from North America or Asia, creating opportunities for regional distribution partnerships. Regulatory frameworks for fiber networks are gradually improving, particularly in Brazil’s Anatel-regulated market segments.

Middle East & Africa

The MEA Square Fiber Connector market shows divergent trends – Gulf Cooperation Council (GCC) countries demonstrate advanced adoption matching global standards, while Sub-Saharan Africa relies more on cost-effective solutions. The UAE and Saudi Arabia lead in smart city deployments requiring high-density fiber interconnects, with Dubai’s fiber penetration exceeding 95% as of 2023. Israel specializes in military-grade connector solutions. African growth concentrates on undersea cable connectivity points and mobile backhaul networks, though inconsistent power infrastructure sometimes limits fiber reliability. South Africa remains the most developed manufacturing hub, while other nations primarily depend on imports from global suppliers through distribution channels.

Report Scope

This market research report provides a comprehensive analysis of the global Square Fiber Connector market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Square Fiber Connector market was valued at USD 192 million in 2024 and is projected to reach USD 248 million by 2032, growing at a CAGR of 3.8%.

- Segmentation Analysis: Detailed breakdown by product type (SC, LC, MU, MPO) and application (Telecom, Broadcast, Military, Aerospace, Others) to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading market participants, including Infinite Electronics, Amphenol, Cinch Connectivity Solutions, Neutrik, Eaton, Yamaichi Electronics, Glenair, ITT Cannon, TE Connectivity, Corning, Fujikura, and CommScope, their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in fiber optic connectivity, including advancements in connector design and materials to minimize insertion loss and reflection loss.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing demand for high-speed data transmission, along with challenges like supply chain constraints and regulatory issues.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in fiber optic connectivity solutions.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Square Fiber Connector Market?

-> Square Fiber Connector Market was valued at 192 million in 2024 and is projected to reach US$ 248 million by 2032, at a CAGR of 3.8% during the forecast period.

Which key companies operate in Global Square Fiber Connector Market?

-> Key players include Infinite Electronics, Amphenol, Cinch Connectivity Solutions, Neutrik, Eaton, Yamaichi Electronics, Glenair, ITT Cannon, TE Connectivity, Corning, Fujikura, and CommScope, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high-speed data transmission, expansion of 5G networks, and growth in telecommunications infrastructure.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by technological advancements and infrastructure development, while North America remains a significant market.

What are the emerging trends?

-> Emerging trends include development of compact connector designs, improved durability for harsh environments, and integration with next-generation network technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...