SiC Power Electronics Market Insights

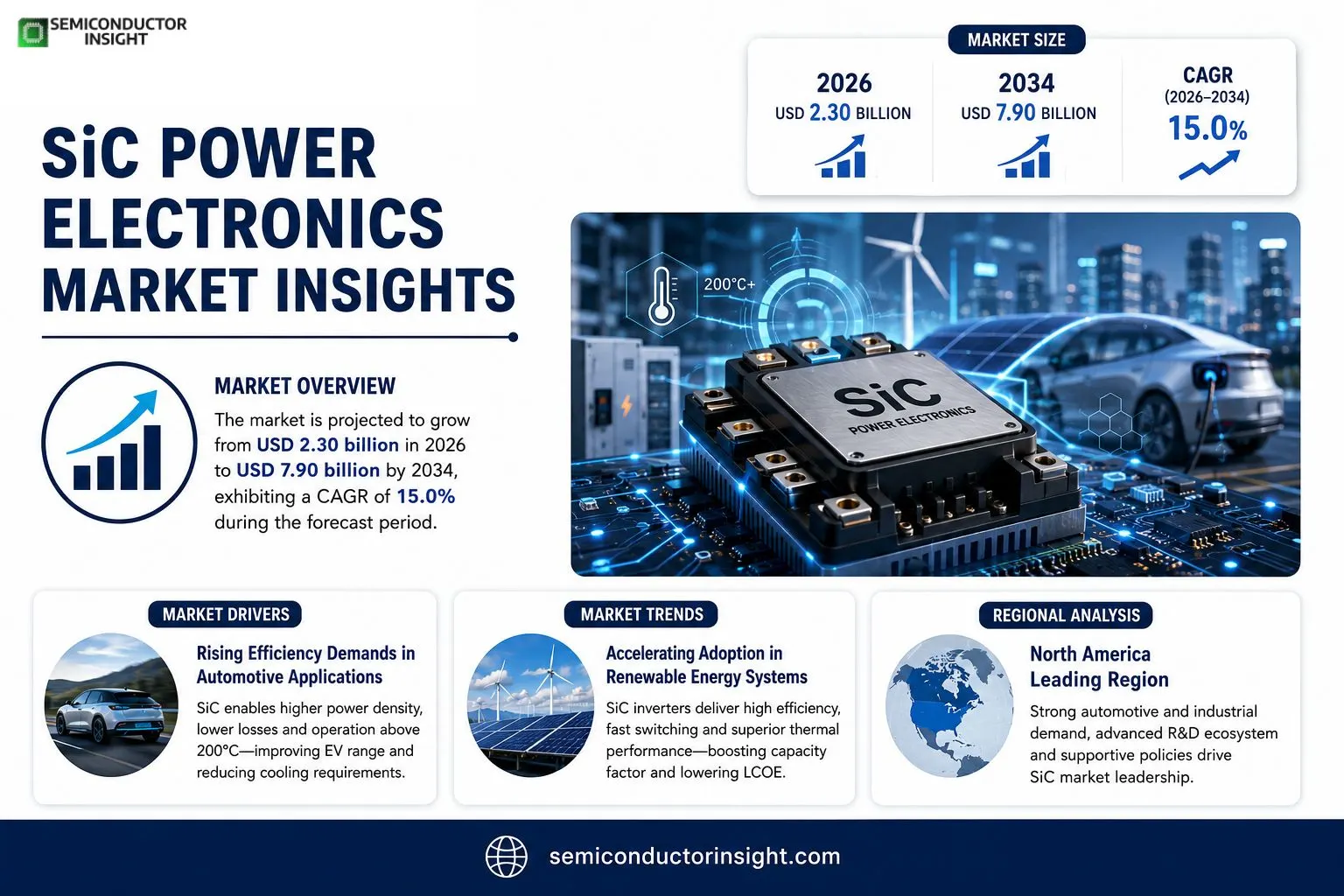

SiC Power Electronics market size was valued at USD 2.25 billion in 2025. The market is projected to grow from USD 2‑30 billion in 2026 to USD 7‑90 billion by 2034, exhibiting a CAGR of 15% during the forecast period.

Silicon carbide (SiC) power electronics comprise devices such as MOSFETs, Schottky diodes and modules that enable high‑efficiency conversion of electrical energy at elevated voltages and temperatures, making them essential for electric‑vehicle drivetrains, renewable‑energy inverters and industrial motor drives.The market is accelerating because automotive OEMs demand higher efficiency for longer range EVs, while renewable‑energy projects require robust converters that tolerate harsh environments.

Key playersincluding Infineon Technologies AG, Wolfspeed (a Cree company), STMicroelectronics, ROHM Semiconductor and ON Semiconductorhave expanded production capacity or announced joint ventures with major automakers such as Toyota and Volkswagento meet the surge in volume orders.

MARKET DRIVERS

Rising Efficiency Demands in Automotive Applications

push for electric vehicles has created a need for higher power density and lower losses. SiC Power Electronics Market components enable drivetrain converters to operate at temperatures above 200 °C, reducing cooling requirements and improving overall vehicle range. OEMs are rapidly qualifying SiC modules for on‑board chargers, making efficiency a decisive competitive edge.

Expansion of Renewable Energy Infrastructure

Grid‑scale solar and wind farms increasingly rely on high‑efficiency inverters to meet stringent regulatory standards. SiC devices provide fast switching speeds and reduced conduction losses, facilitating higher capacity factor and lower levelized cost of electricity. As policy incentives accelerate renewable deployments, demand for SiC‑based converters is projected to rise steadily.

➤ “Adoption of SiC technology is becoming a baseline requirement for next‑generation clean‑energy systems,” says a senior analyst at a leading research firm.

Combined, these efficiency‑driven trends are reshaping system architectures across automotive and power‑generation sectors, positioning SiC Power Electronics Market for robust growth over the next decade.

MARKET CHALLENGES

Thermal Management Complexity

Despite superior material properties, SiC devices generate high heat flux that demands advanced packaging and cooling solutions. Designers must balance thermal resistance with system size, often requiring costly ceramic substrates or liquid‑cooling modules, which can delay time‑to‑market for new products.

Other Challenges

Supply Chain Constraints

The limited number of certified SiC wafer manufacturers creates capacity bottlenecks, especially during peak demand periods. Lead times for high‑quality substrates can extend beyond six months, constraining OEM production schedules and raising inventory costs.

MARKET RESTRAINTS

High Initial Capital Expenditure

Deploying SiC technology often requires significant upfront investment in new design tools, testing equipment, and qualified personnel. For many mid‑size manufacturers, the return on investment horizon exceeds traditional silicon solutions, slowing broader market adoption.

MARKET OPPORTUNITIES

Emerging 5G and Data Center Power Supplies

The rollout of 5G networks and the exponential growth of data center workloads demand high‑efficiency, high‑power converters to manage heat and energy consumption. SiC Power Electronics Market offerings provide the performance needed for compact power modules in base stations and server farms, opening a sizable opportunity for manufacturers willing to tailor solutions for these high‑growth verticals.

SiC Power Electronics Market Trends

Increasing Adoption in Automotive Electrification

SiC Power Electronics Market is gaining momentum as automotive manufacturers intensify efforts to improve electric‑vehicle efficiency and range. SiC MOSFETs and Schottky diodes enable power converters that operate at higher voltages with markedly lower losses, directly supporting longer driving distances on a single charge. Recent capacity expansions by Infineon Technologies and Wolfspeed reflect a strategic response to the surge in volume orders from OEMs such as Toyota and Volkswagen. Joint ventures announced between semiconductor producers and major carmakers further underline the confidence in SiC‑based solutions as a cornerstone of next‑generation drivetrain architectures. This convergence of technology readiness and demand is reshaping supply chains across the automotive sector.

Other Trends

Renewable‑Energy Integration

Renewable‑energy projects are turning to SiC power electronics to meet the dual challenges of high efficiency and harsh operating environments. SiC modules provide superior thermal performance, which reduces the need for extensive cooling in offshore wind turbine inverters and utility‑scale solar converters. The resulting lower system losses translate into higher overall plant output, a critical factor for developers seeking to maximize return on investment. Recent procurement trends show a steady increase in orders for SiC‑based converters from independent power producers, driven by the imperative to meet tighter grid‑integration standards while maintaining reliability under extreme temperature variations.

Industrial Motor‑Drive Optimization

Industrial motor‑drive applications are embracing SiC technology to achieve faster switching, reduced conduction losses, and consequently lower energy consumption. High‑power motor‑drive manufacturers such as STMicroelectronics and ROHM are prioritizing SiC solutions for equipment that must meet stringent efficiency regulations across Europe and Asia. Early adopters report energy savings of up to 30 % compared with traditional silicon devices, contributing to lower operational costs and reduced carbon footprints. As manufacturers align product portfolios with sustainability targets, the adoption of SiC power electronics is expected to expand across a broader range of industrial automation and process‑control systems.

COMPETITIVE LANDSCAPEKey Industry Players

Competitive Landscape of SiC Power Electronics Market

SiC Power Electronics Market is dominated by a small group of vertically integrated manufacturers that have leveraged large‑scale fab capacity and strategic OEM partnerships to capture the bulk of automotive and renewable‑energy orders. Infineon Technologies AG leads the segment with a diversified portfolio of SiC MOSFETs and modules, supported by a multi‑billion‑dollar expansion programme in Europe and Asia. Wolfspeed, operating as a Cree subsidiary, commands a strong position in high‑voltage devices and has secured joint‑venture agreements with Toyota and Volkswagen to supply SiC components for next‑generation EV drivetrains. STMicroelectronics and ROHM Semiconductor complement the leadership tier by offering cost‑effective SiC solutions for industrial motor drives, while ON Semiconductor focuses on power modules for solar‑inverter applications. These four players together account for roughly 60 % of global SiC volume, shaping pricing dynamics and driving the industry’s rapid CAGR of about 15 %.Beyond the primary tier, a broader cohort of niche innovators contributes critical depth to the SiC ecosystem. Texas Instruments and Mitsubishi Electric provide specialized driver ICs that enable seamless integration of SiC devices into existing power architectures. NXP Semiconductors and GeneSiC target high‑frequency, high‑efficiency converters for aerospace and defense markets. Microchip Technology, Panasonic and CREE (operating under the Wolfspeed brand) supply customized solutions for consumer‑grade power supplies and lighting. Emerging players such as Silex Microsystems, Nexperia and Toshiba are accelerating product roadmaps and forming strategic alliances with regional automotive manufacturers, thereby expanding the competitive landscape and fostering technology diffusion across emerging geographies.

List of Key SiC Power Electronics Companies Profiled

- Infineon Technologies AG

- Wolfspeed (Cree)

- STMicroelectronics

- ROHM Semiconductor

- ON Semiconductor

- Texas Instruments

- Mitsubishi Electric

- NXP Semiconductors

- GeneSiC

- Microchip Technology

- Panasonic

- Silex Microsystems

- Nexperia

- Toshiba

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

SiC MOSFETs are the dominant sub‑segment because they combine high voltage tolerance with ultra‑fast switching, enabling compact converter designs.

|

| By Application |

|

Automotive EV Drivetrains lead this dimension as manufacturers pursue higher efficiency and range.

|

| By End User |

|

Automotive OEMs dominate the end‑user landscape, driving rapid adoption cycles.

|

| By Voltage Level |

|

High Voltage devices are the primary growth catalyst, especially for traction inverters and grid‑connected renewable converters.

|

| By Device Architecture |

|

Integrated SiC Power Modules capture the most attention due to their ability to combine multiple functions in a single footprint.

|

Regional Analysis: North America

North America

The automotive industry is the primary driver for SiC Power Electronics in North America. Increased adoption in EVs for inverters, on-board chargers, and power management systems is significantly boosting demand. The pursuit of longer driving ranges and faster charging times necessitates the use of highly efficient SiC devices.

The industrial sector is witnessing a growing demand for SiC Power Electronics in power supplies, motor drives, and industrial heating equipment. The benefits of increased efficiency, reduced size, and improved reliability are driving adoption across various industrial applications.

Consumer electronics, including laptop chargers, TV power supplies, and other devices, are increasingly incorporating SiC Power Electronics to enhance energy efficiency and reduce device size. This trend is driven by the demand for smaller, lighter, and more power-efficient electronic devices.

Government initiatives focused on renewable energy and energy efficiency are supporting the adoption of SiC Power Electronics in grid infrastructure and energy storage systems. Tax incentives and regulatory policies are further encouraging investment in this technology.

Europe

Europe is another key market for SiC Power Electronics, characterized by a strong focus on energy efficiency and sustainability. The region’s stringent environmental regulations are driving demand for more efficient power solutions across various sectors. The automotive industry in Europe is also a significant driver, with increasing adoption of EVs and hybrid vehicles. Furthermore, the growing deployment of renewable energy sources such as solar and wind power is creating opportunities for SiC Power Electronics in grid stabilization and energy storage. The European Union’s emphasis on the Green Deal is expected to further accelerate the adoption of SiC technology in the coming years. The industrial sector in Europe is also adopting SiC for improved efficiency in motor drives and power supplies.

Asia-Pacific

Asia-Pacific presents the fastest-growing market for SiC Power Electronics, driven by rapid industrialization and increasing automotive production, particularly in China and India. The region’s burgeoning electric vehicle market is a major growth driver, with significant investments in EV manufacturing and infrastructure. The increasing adoption of SiC in industrial automation and power management systems is also contributing to market expansion. Government support for advanced manufacturing and renewable energy is further fueling demand. The cost competitiveness of SiC devices is also making them increasingly attractive for various applications in this region. The expansion of the consumer electronics market in Asia-Pacific also contributes to the growth of SiC Power Electronics Market.

South America

South America is an emerging market for SiC Power Electronics, with growing demand in the automotive, industrial, and renewable energy sectors. Increasing investments in electric vehicle charging infrastructure and the deployment of solar and wind power plants are driving adoption. The region’s focus on energy efficiency and sustainability, coupled with supportive government policies, is expected to further accelerate market growth. The industrial sector is also witnessing increased adoption of SiC in motor drives and power supplies. However, the market in South America is relatively smaller compared to North America and Asia-Pacific.

Middle East & Africa

The Middle East & Africa region represents a nascent market for SiC Power Electronics, with significant potential for growth. Increasing investments in renewable energy projects, particularly solar power, are creating opportunities for SiC in grid stabilization and energy storage. The automotive industry in the region is also growing, with increasing adoption of electric vehicles. Government initiatives promoting energy efficiency and diversification of energy sources are expected to drive market expansion. The industrial sector in the region is also witnessing increased adoption of SiC in power supplies and motor drives. While currently a smaller market, the region offers promising long-term growth prospects for SiC Power Electronics.

Report Scope

This market research report provides a comprehensive analysis of the SiC Power Electronics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of SiC Power Electronics Market?

-> SiC Power Electronics Market was valued at USD 2.25 billion in 2025 and is expected to reach USD 7‑90 billion by 2034, exhibiting a CAGR of 15% during the forecast period.

Which key companies operate in SiC Power Electronics Market?

-> Key players include Infineon Technologies AG, Wolfspeed (Cree), STMicroelectronics, ROHM Semiconductor, and ON Semiconductor.

What are the key growth drivers?

-> Key growth drivers include automotive OEM demand for higher efficiency and longer‑range EVs, and renewable‑energy projects requiring robust high‑temperature converters.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, driven by strong automotive and renewable‑energy investments, while Europe remains a significant market.

What are the emerging trends?

-> Emerging trends include integration of SiC devices with AI/IoT for smart power management, advances in wafer fabrication, and development of high‑voltage modules for industrial applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...