Semiconductor Packaging Materials Market Analysis:

The global Semiconductor Packaging Materials Market was valued at 31260 million in 2024 and is projected to reach US$ 76960 million by 2031, at a CAGR of 14.1% during the forecast period.

Semiconductor Packaging Materials Market Overview

Semiconductor packaging serves four primary functions:

- Protection: Safeguards chips from environmental damage.

- Support: Physically supports the semiconductor die.

- Connection: Links the chip to the circuit board via electrical pathways.

- Reliability: Ensures long-term performance and functionality.

Packaging is critical for enabling semiconductors to operate effectively across a wide range of devices and environmental conditions.

Semiconductor Industry Background

A semiconductor is a material that selectively conducts electricity. By adjusting its properties (e.g., sensitivity to heat or light), manufacturers can customize its performance for a variety of applications.

Key Highlights:

- Leading Chip Makers:

- Intel: $48.7 billion in revenue (2023)

- Samsung Electronics: $39.9 billion in revenue (2023)

- Global Semiconductor Sales:

- 2023: Experienced a 9.4% decline

- 2024 (forecast): Projected to reach $611.23 billion, with 16% year-on-year growth

- Applications:Semiconductors are foundational to smartphones, PCs, tablets, AI systems, IoT devices, and machine learning applications.

Market Growth Drivers

- Boom in Consumer Electronics: Rising demand for smart and connected devices.

- AI, IoT, and ML Integration: Higher need for high-speed processing and data handling.

- Data Center Expansion: Accelerated need for advanced memory chips.

- Post-2023 Market Recovery: Strong rebound expected in 2024 and beyond.

Key Players in Semiconductor Packaging Materials Market

- Kyocera

- Shinko

- Ibiden

The top three companies collectively hold over 22% of the global market share, highlighting a moderately concentrated market structure.

The Semiconductor Packaging Materials Market is set for robust growth, supported by surging semiconductor demand across consumer electronics, AI, and cloud infrastructure. With innovation at its core, and top players like Kyocera and Shinko leading the charge, this market is crucial to the evolution of next-gen electronics.

We have surveyed the Semiconductor Packaging Materials companies, and industry experts on this industry, involving the revenue, demand, product type, recent developments and plans, industry trends, drivers, challenges, obstacles, and potential risks

This report aims to provide a comprehensive presentation of the global market for Semiconductor Packaging Materials, with both quantitative and qualitative analysis, to help readers develop business/growth strategies, assess the market competitive situation, analyze their position in the current marketplace, and make informed business decisions regarding Semiconductor Packaging Materials. This report contains market size and forecasts of Semiconductor Packaging Materials in global, including the following market information:

- Global Semiconductor Packaging Materials market revenue, 2020-2025, 2026-2031, ($ millions)

- Global top five Semiconductor Packaging Materials companies in 2024 (%)

Audio Digital Signal Processor Key Market Trends :

Rising Demand for AI and IoT Applications

The growing adoption of AI, IoT, and ML technologies is fueling demand for advanced semiconductor packaging materials to support high-performance chips.Shift Toward Advanced Packaging Technologies

The market is witnessing a transition from traditional packaging to advanced options like fan-out wafer-level packaging and 3D IC packaging to enhance performance and miniaturization.Surge in Consumer Electronics Production

The increasing global consumption of smartphones, tablets, and smart devices is accelerating demand for reliable and efficient semiconductor packaging materials.Increased Investment in Data Centers

Rising demand for high-speed memory chips for data center applications is driving innovation and growth in packaging materials.Environmental Sustainability Focus

Key players are investing in eco-friendly and lead-free packaging materials to align with global sustainability goals and regulatory compliance.

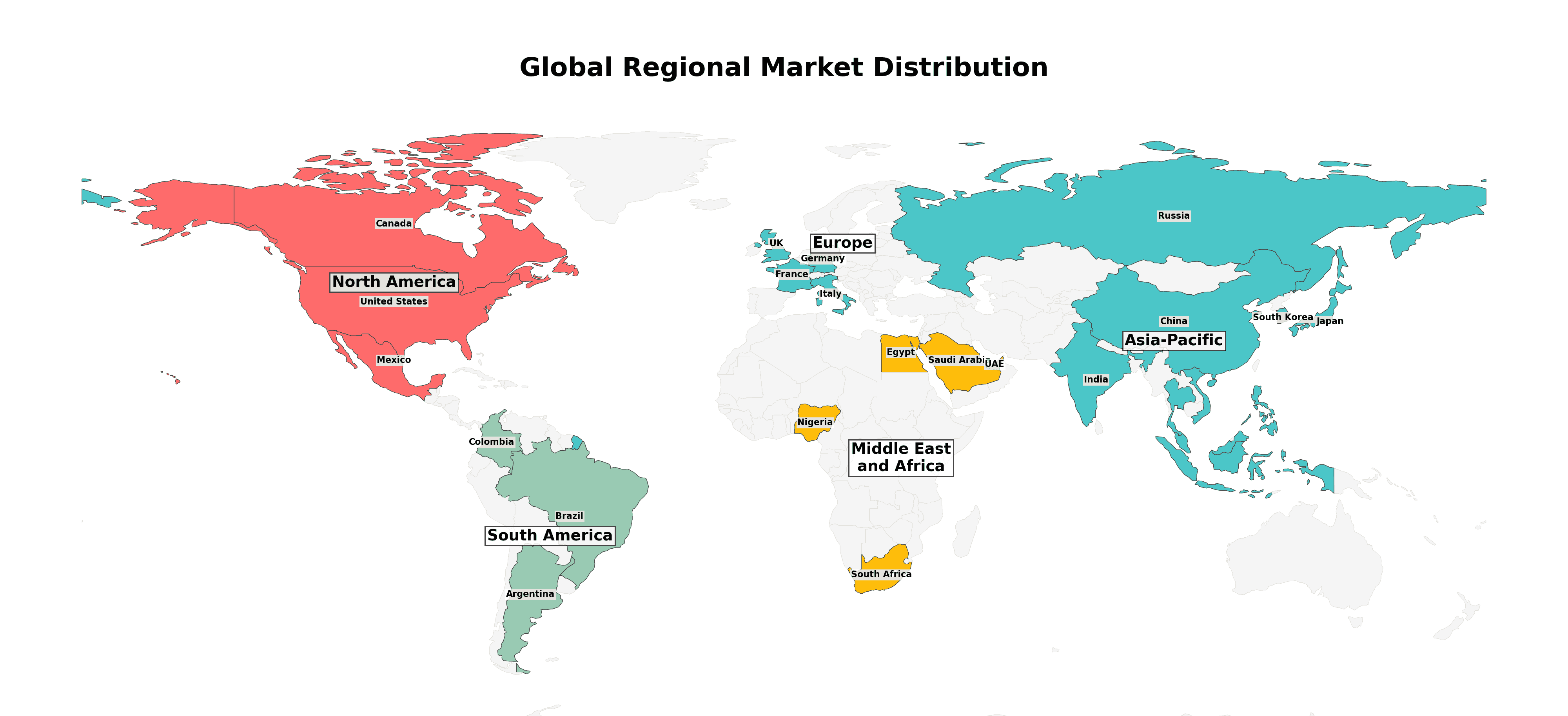

Audio Digital Signal Processor Market Regional Analysis :

North America:

Strong demand driven by EVs, 5G infrastructure, and renewable energy, with the U.S. leading the market.

Europe:

Growth fueled by automotive electrification, renewable energy, and strong regulatory support, with Germany as a key player.

Asia-Pacific:

Dominates the market due to large-scale manufacturing in China and Japan, with growing demand from EVs, 5G, and semiconductors.

South America:

Emerging market, driven by renewable energy and EV adoption, with Brazil leading growth.

Middle East & Africa:

Gradual growth, mainly due to investments in renewable energy and EV infrastructure, with Saudi Arabia and UAE as key contributors.

Total Market by Segment:

Global Semiconductor Packaging Materials market, by Type, 2020-2025, 2026-2031 ($ millions)

Global Semiconductor Packaging Materials market segment percentages, by Type, 2024 (%)

- Packaging Substrate

- Lead Frame

- Bonding Wire

- Encapsulating Resin

- Ceramic Packaging Material

- Chip Bonding Material

- Others

Global Semiconductor Packaging Materials market, by Application, 2020-2025, 2026-2031 ($ millions)

Global Semiconductor Packaging Materials market segment percentages, by Application, 2024 (%)

- Consume Electrons

- Automobiles

- Communications

- Medical

- Others

Competitor Analysis

The report also provides analysis of leading market participants including:

- Key companies Semiconductor Packaging Materials revenues in global market, 2020-2025 (estimated), ($ millions)

- Key companies Semiconductor Packaging Materials revenues share in global market, 2024 (%)

Further, the report presents profiles of competitors in the market, key players include:

- Kyocera

- Shinko

- Ibiden

- LG Innotek

- Unimicron Technology

- ZhenDing Tech

- Semco

- KINSUS INTERCONNECT TECHNOLOGY

- Nan Ya PCB

- Nippon Micrometal Corporation

- Simmtech

- Mitsui High-tec, Inc.

- HAESUNG

- Shin-Etsu

- Heraeus

- AAMI

- Henkel

- Shennan Circuits

- Kangqiang Electronics

- LG Chem

- NGK/NTK

- MK Electron

- Toppan Printing Co., Ltd.

- Tanaka

- MARUWA

- Momentive

- SCHOTT

- Element Solutions

- Hitachi Chemical

- Fastprint

- Hongchang Electronic

- Sumitomo

Drivers

Boom in Consumer Electronics and Smart Devices

The global surge in electronics consumption, especially smartphones, tablets, and smart wearables, is boosting demand for semiconductor packaging materials.Growth in Semiconductor Industry Revenue

With semiconductor revenues reaching $611.23 billion in 2024 and expected to grow, packaging materials are seeing parallel demand.Technological Advancements in Chip Design

Innovations in chip architecture and design are creating the need for advanced packaging materials to support next-gen electronic functions.

Restraints

High Cost of Advanced Packaging Solutions

Sophisticated packaging materials and technologies often come at a premium cost, limiting adoption in cost-sensitive applications.Complex Manufacturing Processes

Packaging materials require precision engineering and complex fabrication, posing a challenge for smaller manufacturers.Environmental and Regulatory Compliance

Meeting stringent environmental standards and safety regulations may slow down the development and commercialization of certain packaging materials.

Opportunities

Rising AI and Data Center Applications

The increasing need for high-speed, efficient memory chips in AI and data centers opens up vast opportunities for material providers.Emerging Markets and 5G Rollouts

Growth in emerging economies and the global push toward 5G infrastructure are driving demand for semiconductors and related packaging materials.Customization and Specialty Packaging Needs

Demand for tailored solutions in automotive, medical, and industrial applications provides opportunities for niche material innovation.

Market Challenges

Supply Chain Disruptions

Global supply chain issues and raw material shortages can delay production and disrupt the semiconductor packaging ecosystem.Intense Market Competition

Leading players like Kyocera, Shinko, and Ibiden dominate the market, creating high competition and entry barriers for new players.Technological Obsolescence

Rapid changes in chip technology require continuous upgrades in packaging materials, which can be resource-intensive for manufacturers.

FAQs

Q: What are the key driving factors and opportunities in the Semiconductor Packaging Materials market?

A: Key drivers include the rising demand for consumer electronics, AI, IoT, and advanced chip designs. Opportunities lie in AI data centers, 5G adoption, and eco-friendly packaging innovations.

Q: Which region is projected to have the largest market share?

A: Asia-Pacific is expected to dominate the market due to its strong semiconductor manufacturing base and increasing demand from consumer electronics and automotive sectors.

Q: Who are the top players in the global Semiconductor Packaging Materials market?

A: Major players include Kyocera, Shinko, and Ibiden, with the top three companies collectively holding over 22% market share globally.

Q: What are the latest technological advancements in the industry?

A: Advancements include 3D IC packaging, fan-out wafer-level packaging, and the development of eco-friendly, lead-free packaging materials.

Q: What is the current size of the global Semiconductor Packaging Materials market?

A: The market was valued at USD 31,260 million in 2024 and is projected to reach USD 76,960 million by 2031, growing at a CAGR of 14.1%.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...