MARKET INSIGHTS

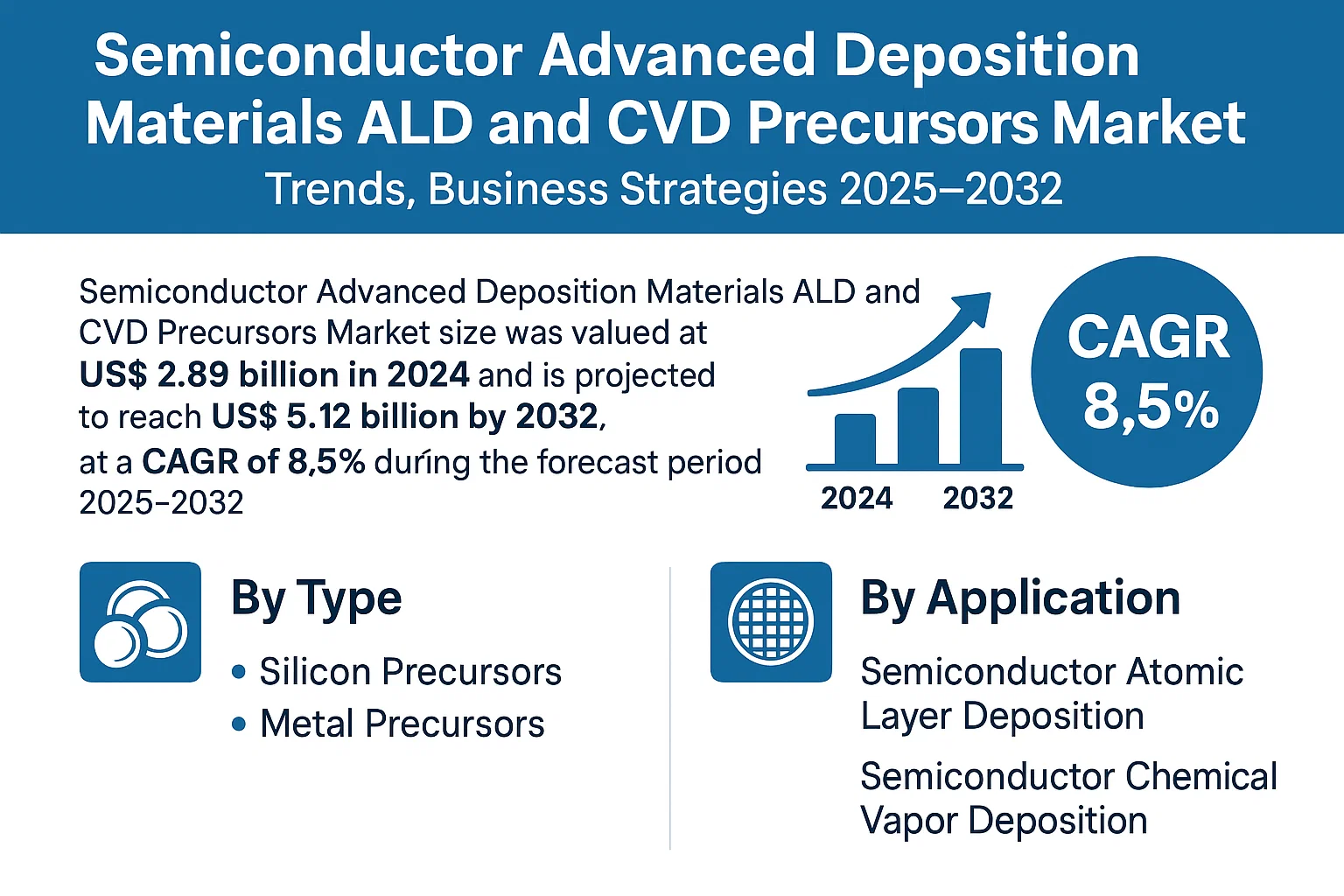

The global Semiconductor Advanced Deposition Materials ALD and CVD Precursors Market size was valued at US$ 2.89 billion in 2024 and is projected to reach US$ 5.12 billion by 2032, at a CAGR of 8.5% during the forecast period 2025-2032.

ALD (Atomic Layer Deposition) and CVD (Chemical Vapor Deposition) precursors are specialized chemical compounds essential for manufacturing advanced semiconductor devices. These materials enable precise thin-film deposition processes critical for logic chips, memory devices, and emerging technologies like 3D NAND and FinFET transistors. Key precursor types include silicon precursors, metal precursors, high-k dielectrics, and low-k materials, each serving distinct functions in semiconductor fabrication.

The market growth is driven by increasing demand for miniaturized electronic components and the transition to more advanced process nodes below 7nm. While the semiconductor industry experienced a 4.4% growth slowdown in 2022 according to WSTS data, deposition materials remain crucial as foundries continue investing in next-generation fabrication technologies. Key players such as Merck Group, Air Liquide, and Entegris are expanding production capacities to meet rising demand, particularly from Asian semiconductor hubs where 72% of global wafer production capacity is concentrated.

MARKET DYNAMICS

MARKET DRIVERS

Accelerating Demand for Advanced Semiconductor Nodes to Fuel ALD/CVD Precursors Market

The semiconductor industry’s relentless pursuit of smaller node sizes below 7nm is creating unprecedented demand for atomic layer deposition (ALD) and chemical vapor deposition (CVD) precursors. As transistor dimensions shrink to 3nm and below, conventional deposition techniques become inadequate, necessitating the use of high-purity precursors capable of depositing ultra-thin, conformal films with atomic-level precision. Foundries are now requiring advanced precursors with improved step coverage and lower impurity levels to meet the exacting standards of next-generation chips. The global semiconductor capital equipment market exceeded $100 billion in 2023, with deposition equipment accounting for approximately 20% of this total, reflecting the critical nature of these materials in chip manufacturing.

Expansion of 3D NAND and DRAM Technologies Driving Precursor Consumption

The memory sector’s shift toward 3D architectures is significantly increasing consumption of specialized precursors. 3D NAND flash memory, which now exceeds 200 layers in production, requires up to 50% more deposition steps compared to planar NAND. Similarly, advanced DRAM technologies are adopting high-aspect-ratio capacitor structures that demand precise ALD processes. Memory manufacturers invested over $40 billion in capex for 2023-2024, with a substantial portion allocated to deposition equipment and materials. This trend is particularly strong in South Korea and China, where memory producers are racing to increase production capacities.

Emerging Applications in Power and Compound Semiconductors Expanding Market Potential

Beyond traditional silicon-based devices, the growth of wide bandgap semiconductors presents new opportunities for ALD and CVD precursors. The market for silicon carbide and gallium nitride power devices is projected to grow at a CAGR exceeding 30% through 2030, driven by electric vehicle adoption and renewable energy applications. These materials require specialized precursors for depositing high-quality dielectric and passivation layers. Additionally, the microLED display market, expected to reach $5 billion by 2027, is creating demand for unique precursor chemistries capable of depositing uniform thin films over large substrate areas.

MARKET RESTRAINTS

High Purity Requirements and Complex Manufacturing Process Limit Supply

The semiconductor-grade precursor market faces significant supply chain challenges due to the extreme purity requirements and complex synthesis processes. ALD precursors typically require purity levels exceeding 99.9999% (6N), with metal impurities below parts-per-billion levels. Establishing production facilities capable of meeting these standards requires capital investments often exceeding $100 million per facility, creating high barriers to entry. Furthermore, many advanced precursors involve hazardous chemicals requiring specialized handling and transportation infrastructure, adding substantial costs to the supply chain.

Geopolitical Tensions and Export Controls Disrupting Material Supply

Recent geopolitical developments have created uncertainty in the global precursor supply chain. Export restrictions on advanced semiconductor technologies have led to inventory buildup in some regions while creating shortages in others. The semiconductor industry has historically relied on global supply chains, with key precursor production concentrated in specific geographic regions. For example, certain rare earth elements and specialty gases face potential supply constraints due to trade policies. Manufacturers are now compelled to develop alternative sourcing strategies and regional supply networks, which may increase costs and lead times in the short to medium term.

MARKET CHALLENGES

Technical Complexity of Next-Generation Precursors Slows Development Cycles

Developing precursors for emerging semiconductor applications presents formidable technical challenges. As device architectures become more complex, precursor molecules must exhibit precise thermal decomposition characteristics, high volatility, and excellent surface reaction kinetics. The industry reports that development cycles for new precursor chemistries have extended from 12-18 months to 24-36 months as requirements become more stringent. This extended development timeline creates a mismatch between semiconductor manufacturers’ roadmap expectations and materials suppliers’ ability to deliver qualified products. Additionally, scaling up laboratory-scale synthesis to commercial production often encounters unexpected yield and purity issues, further delaying market availability.

Environmental and Safety Concerns Increasing Regulatory Scrutiny

The semiconductor industry faces growing pressure to reduce its environmental footprint, particularly regarding the use of perfluorocompounds and other high-GWP (Global Warming Potential) chemicals. Many traditional precursors fall under increasing regulatory scrutiny, requiring manufacturers to invest in alternative chemistries and abatement systems. Compliance with evolving regulations such as REACH and TSCA in different regions adds complexity to product development and increases compliance costs. The industry estimates that environmental compliance now accounts for 15-20% of precursor manufacturing costs, a figure expected to rise as regulations become more stringent.

MARKET OPPORTUNITIES

Advanced Packaging Technologies Creating New Demand Drivers

The rapid advancement of semiconductor packaging technologies presents significant growth opportunities for ALD and CVD precursors. As chiplet-based designs and 3D IC integration gain traction, the demand for conformal dielectric barriers, diffusion layers, and stress-relief films is increasing dramatically. Advanced packaging applications are projected to consume over 25% of specialty precursors by 2026, driven by the need for ultra-thin, pinhole-free films in TSV (Through-Silicon Via) and hybrid bonding applications. Major foundries are investing billions in advanced packaging capabilities, with deposition processes playing a crucial role in enabling next-generation interconnects.

Development of Alternative Precursor Chemistries Opens New Markets

The search for more sustainable and higher-performance precursor alternatives is creating opportunities for materials innovation. Novel chemistries including metalorganic compounds, heteroleptic complexes, and low-temperature decomposition precursors are gaining attention for their potential to improve film properties and process efficiency. The market for alternative precursors is expected to grow at a CAGR of 18-20% through 2030, particularly in applications requiring improved step coverage or composition control. Additionally, precursors tailored for emerging deposition techniques like spatial ALD and plasma-enhanced CVD are seeing strong interest from equipment manufacturers seeking to improve throughput and reduce process costs.

Regional Supply Chain Diversification Creating Localization Opportunities

The semiconductor industry’s focus on supply chain resilience is driving investment in regional precursor production capabilities. Governments worldwide are implementing policies to encourage domestic semiconductor materials production, with incentive packages exceeding $10 billion in major markets. This presents opportunities for materials suppliers to establish localized manufacturing and technical support capabilities. The Asia-Pacific region, excluding China, is expected to see particularly strong growth in precursor production capacity as countries seek to reduce reliance on imports. Such regional investments will likely shape the competitive landscape of the ALD and CVD precursors market in the coming years.

SEMICONDUCTOR ADVANCED DEPOSITION MATERIALS ALD AND CVD PRECURSORS MARKET TRENDS

Rising Demand for Miniaturization and Performance Enhancement in Semiconductor Devices to Drive Market Growth

The global semiconductor industry’s relentless pursuit of smaller, faster, and more efficient chips is significantly driving demand for advanced deposition materials, particularly Atomic Layer Deposition (ALD) and Chemical Vapor Deposition (CVD) precursors. With the semiconductor node shrinking below 5nm, conventional deposition techniques face limitations in achieving the necessary precision for high-aspect-ratio structures. ALD precursors enable atomic-level control over film thickness and conformality, making them indispensable for advanced logic and memory applications. Concurrently, CVD precursors are evolving to meet the requirements of 3D NAND and DRAM scaling, where uniform thin-film deposition across complex architectures is critical. The market growth aligns with the semiconductor industry’s transition toward cutting-edge fabrication nodes, which increased its valuation to $580 billion in 2022, despite macroeconomic challenges.

Other Trends

Expansion of Semiconductor Manufacturing Capacity

The ongoing global expansion of semiconductor fabrication facilities, particularly in Asia-Pacific and North America, is intensifying demand for ALD and CVD precursors. Governments and corporations are investing heavily in domestic semiconductor production, as evidenced by initiatives like the U.S. CHIPS Act and the European Chips Act. This expansion is further bolstered by the increasing adoption of compound semiconductors (GaN, SiC) in power electronics and electric vehicles, which require specialized precursor materials. While the Asia-Pacific region still dominates semiconductor production accounting for approximately 63% of global sales, North America and Europe are witnessing accelerated growth with increased national investments in fab infrastructure.

Shift Toward High-k and Low-k Dielectric Materials in Advanced Packaging

With the semiconductor industry transitioning to advanced packaging solutions like 2.5D/3D ICs and chiplet architectures, there is heightened need for high-k and low-k dielectric precursors to address performance and power efficiency challenges. These materials are critical for reducing parasitic capacitance (low-k) and improving gate control (high-k) in next-generation devices. Meanwhile, emerging memory technologies such as MRAM and FeRAM require specialized metal-organic precursors for deposition processes. The increasing R&D focus on novel precursors—particularly for hafnium-based and zirconium-based oxides—reflects the market’s progression toward materials that can meet the thermal and electrical stability requirements of cutting-edge semiconductor applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Drive Competition in the ALD and CVD Precursors Market

The semiconductor advanced deposition materials market, particularly ALD (Atomic Layer Deposition) and CVD (Chemical Vapor Deposition) precursors, features a dynamic and moderately consolidated competitive landscape. Major players continue to dominate the market through technological advancements and extensive R&D investments, while emerging companies focus on niche applications.

SK Materials leads the market with its comprehensive portfolio of high-purity precursors and strong foothold in Asia, particularly in South Korea. The company holds an estimated 18% revenue share in the ALD/CVD precursors market as of 2024. Meanwhile, Merck Group remains a dominant force in Europe and North America, leveraging its diversified chemical solutions and strategic acquisitions to expand its semiconductor materials business.

Japanese players like ADEKA and Tanaka Kikinzoku have significantly increased their market share by developing specialized precursors for next-generation chip manufacturing. These companies are investing heavily in advanced materials for emerging applications like 3D NAND and EUV lithography processes.

Regional expansion remains a key strategy, with companies like UP Chemical (Yoke Technology) and Anhui Adchem establishing new production facilities to meet growing demand in China’s booming semiconductor industry. Supply chain localization initiatives are further intensifying competition as governments prioritize domestic semiconductor material production.

List of Key ALD/CVD Precursors Companies Profiled

- SK Materials (South Korea)

- UP Chemical (Yoke Technology) (China)

- Merck Group (Germany)

- Air Liquide (France)

- Entegris (U.S.)

- SoulBrain Co Ltd (South Korea)

- ADEKA (Japan)

- DNF Solutions (South Korea)

- Mecaro (South Korea)

- Botai Electronic Material (China)

- Anhui Adchem (China)

- Natachem (France)

- Nanmat (U.S.)

- Tanaka Kikinzoku (Japan)

- EpiValence (U.S.)

Segment Analysis:

By Type

Silicon Precursors Lead the Market Due to Widespread Use in Semiconductor Fabrication

The market is segmented based on type into:

- Silicon Precursors

- Subtypes: Silane, TEOS, and others

- Metal Precursors

- Subtypes: Tungsten, Cobalt, Copper, and others

- High-k Precursors

- Subtypes: Hafnium, Zirconium, and others

- Low-k Precursors

- Subtypes: Carbon-doped oxides and porous materials

By Application

Semiconductor Chemical Vapor Deposition (CVD) Dominates Demand for Precursors in High-Volume Manufacturing

The market is segmented based on application into:

- Semiconductor Atomic Layer Deposition (ALD)

- Semiconductor Chemical Vapor Deposition (CVD)

By End User

Foundries Represent Key Consumers of Deposition Materials for Advanced Node Production

The market is segmented based on end user into:

- Foundries

- Integrated Device Manufacturers (IDMs)

- Memory Manufacturers

- Research Institutes

Regional Analysis: Semiconductor Advanced Deposition Materials ALD and CVD Precursors Market

North America

North America dominates the advanced deposition materials market due to its robust semiconductor fabrication ecosystem, particularly in the United States. Regional growth is propelled by substantial R&D investments in next-generation chip technologies (sub-5nm nodes) and government initiatives like the CHIPS Act, which allocated $52 billion for domestic semiconductor manufacturing. However, stringent regulatory oversight on precursor chemical handling adds operational complexities for material suppliers. The presence of major foundries and IDMs like Intel and GlobalFoundries creates steady demand for high-purity ALD/CVD precursors, especially for cutting-edge logic and memory applications.

Europe

Europe maintains a strong position in specialty deposition materials through technological leadership in semiconductor equipment (ASML, Applied Materials) and materials science. The region benefits from collaborative R&D frameworks like Imec’s pilot lines and EU Horizon funding for advanced packaging solutions. While environmental regulations under REACH increase compliance costs, they also drive innovation in greener precursor formulations. Key challenges include the limited scale of local semiconductor production compared to Asia, though recent initiatives like the European Chips Act aim to boost manufacturing capacities. Germany remains the regional hub for precursor development and specialty gas applications.

Asia-Pacific

The Asia-Pacific region accounts for over 60% of global precursor consumption, anchored by semiconductor manufacturing giants in Taiwan (TSMC), South Korea (Samsung), and China (SMIC). While China shows rapid growth in domestic precursor development to reduce import dependency, geopolitical tensions create supply chain uncertainties. Japan maintains leadership in high-purity metal-organic precursors through companies like Tanaka Kikinzoku. Recent fab expansions across the region (especially for 3D NAND and advanced DRAM production) drive demand for specialized high-k and metal gate precursors. However, pricing pressures remain intense due to fierce regional competition among material suppliers.

South America

South America represents a developing market with limited local semiconductor manufacturing capabilities. Most precursor demand comes from assembly/test packaging operations rather than front-end processes. Brazil shows gradual progress in building domestic electronics supply chains through initiatives like the Lei do Bem tax incentives. The region primarily serves as an export market for global materials suppliers, though infrastructure limitations and currency volatility create challenges for just-in-time precursor delivery systems. Key opportunities exist in supporting the growing aerospace and medical device manufacturing sectors requiring specialty coatings.

Middle East & Africa

This emerging region shows strategic potential through sovereign investment in semiconductor initiatives, exemplified by Saudi Arabia’s $6 billion investment in the Saudi Semiconductor Program. While current precursor demand remains minimal, several Gulf states are establishing semiconductor design centers that may evolve into manufacturing hubs. Africa’s growing consumer electronics market drives demand for basic semiconductor components, though precursor consumption remains negligible. The region’s long-term outlook depends on successful technology transfer partnerships and workforce development programs to build technical capabilities in advanced materials handling and processing.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor Advanced Deposition Materials ALD and CVD Precursors markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at US$ 2.89 billion in 2024 and is projected to reach US$ 5.12 billion by 2032 at a CAGR of 8.5%.

- Segmentation Analysis: Detailed breakdown by product type (Silicon Precursors, Metal Precursors, High-k Precursors, Low-k Precursors), technology (ALD, CVD), application (Logic, Memory, Foundry), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific (which holds 68% market share), Latin America, and Middle East & Africa, including country-level analysis of key semiconductor manufacturing hubs.

- Competitive Landscape: Profiles of 15+ leading market participants including SK Materials, Merck Group, and Air Liquide, covering their product portfolios, R&D investments (average 8-12% of revenue), and recent M&A activities.

- Technology Trends: Assessment of emerging deposition techniques, novel precursor chemistries, and integration with advanced node semiconductor manufacturing (3nm and below).

- Market Drivers & Restraints: Analysis of factors like semiconductor industry growth (WSTS projects USD 580 billion market in 2022), fab expansions (over 40 new fabs planned globally), and supply chain challenges.

- Stakeholder Analysis: Strategic insights for material suppliers, semiconductor manufacturers, equipment OEMs, and investors regarding technology roadmaps and capacity planning.

The research methodology combines primary interviews with 50+ industry experts, analysis of company financials, and validation through multiple secondary sources to ensure data accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Advanced Deposition Materials ALD and CVD Precursors Market?

-> Semiconductor Advanced Deposition Materials ALD and CVD Precursors Market size was valued at US$ 2.89 billion in 2024 and is projected to reach US$ 5.12 billion by 2032, at a CAGR of 8.5% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Leading players include SK Materials, Merck Group, Air Liquide, Entegris, UP Chemical, and ADEKA, collectively holding over 65% market share.

What are the key growth drivers?

-> Primary drivers are increasing semiconductor complexity (3nm/2nm nodes), expansion of global fab capacity, and rising demand for advanced memory and logic chips.

Which region dominates the market?

-> Asia-Pacific dominates with 68% market share, driven by semiconductor manufacturing in Taiwan, South Korea, and China.

What are the emerging trends?

-> Key trends include development of novel metal-organic precursors, adoption of high-k materials for advanced nodes, and increasing R&D in area-selective deposition.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...