MARKET INSIGHTS

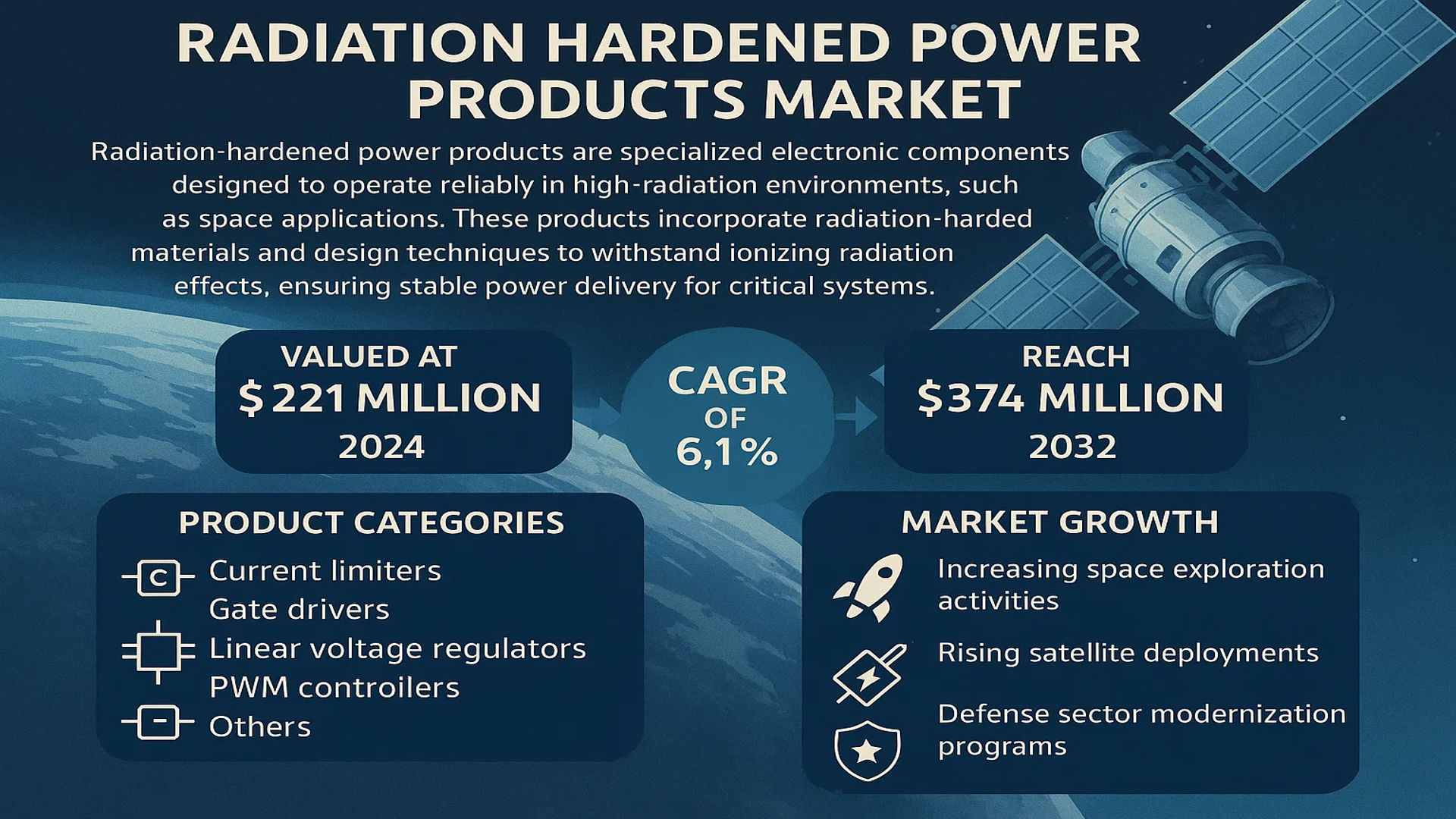

The global Radiation Hardened Power Products Market was valued at 221 million in 2024 and is projected to reach US$ 374 million by 2032, at a CAGR of 6.1% during the forecast period.

Radiation hardened power products are specialized electronic components designed to operate reliably in high-radiation environments, such as space applications. These products incorporate radiation-hardened materials and design techniques to withstand ionizing radiation effects, ensuring stable power delivery for critical systems. The product categories include radiation hardened current limiters, gate drivers, linear voltage regulators, PWM controllers, and others.

The market is growing due to increasing space exploration activities, rising satellite deployments, and defense sector modernization programs. While government investments in space technology drive demand, commercial space initiatives from companies like SpaceX and Blue Origin further contribute to market expansion. Key players such as BAE Systems, Renesas, and Infineon are focusing on product innovations to meet stringent radiation tolerance requirements for aerospace applications.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Space Exploration Activities to Drive Market Demand

The global space industry is witnessing unprecedented growth, with government space agencies and private companies launching more satellites and deep space missions than ever before. This surge in space exploration directly fuels the demand for radiation hardened power products that ensure uninterrupted operations in extreme environments. Recent data indicates over 5,000 active satellites currently orbit the Earth, with projections suggesting this number could exceed 20,000 by 2030. These numbers highlight the critical need for reliable power solutions that can withstand radiation exposure in space applications.

Military Modernization Programs Boosting Adoption Rates

Defense agencies worldwide are investing heavily in modernizing their electronic warfare and communication systems, particularly those requiring operation in nuclear or high-radiation environments. Radiation hardened power components have become essential for missile guidance systems, secure communications, and surveillance platforms. Military budgets across major economies continue to allocate significant portions to electronic warfare capabilities, with radiation hardened solutions forming a critical part of these strategic upgrades.

Moreover, the increasing deployment of automation in defense systems requires power solutions that maintain performance even in radiation-intensive scenarios. This trend is particularly evident in unmanned systems and electronic countermeasure devices where power reliability directly impacts mission success rates.

MARKET CHALLENGES

High Development Costs Creating Barriers for Market Entry

The specialized nature of radiation hardened power products demands extensive testing and certification processes, leading to significantly higher development costs compared to conventional power components. These products typically require additional shielding materials, rigorous qualification testing under radiation exposure, and specialized manufacturing techniques. The cost premium for radiation hardened versions can range from 3-5 times that of standard components, creating financial barriers for some end-users.

Other Challenges

Lengthy Certification Processes

The stringent qualification requirements for space and military applications often result in prolonged certification timelines, sometimes extending beyond 24 months for certain components. These delays can impact product development cycles and time-to-market for manufacturers.

Limited Production Volumes

Unlike commercial power products manufactured in high volumes, radiation hardened components typically have lower production quantities due to their niche applications. This limits economies of scale and keeps costs elevated.

MARKET RESTRAINTS

Technological Complexity Constraining Innovation Pace

Developing radiation hardened power products requires balancing performance, size and cost while meeting demanding reliability standards. The need to harden components against various radiation effects – including total ionizing dose, single event effects, and displacement damage – adds multiple layers of complexity to the design process. This technical challenge slows the pace of innovation compared to commercial power electronics, where new technologies emerge more rapidly.

Additionally, the limited number of qualified foundries capable of producing radiation hardened semiconductor components creates bottlenecks in the supply chain. Many standard manufacturing processes must be modified to meet radiation hardening requirements, further complicating production.

MARKET OPPORTUNITIES

Advancements in Commercial Space Sector Opening New Revenue Streams

The rapid expansion of commercial space ventures presents significant growth opportunities for radiation hardened power products. Companies are developing small satellites and constellation networks that require cost-effective yet reliable power solutions. This has led to innovative approaches in radiation hardening techniques that maintain reliability while reducing costs, creating new market segments between traditional aerospace-grade and commercial-grade components.

Furthermore, emerging technologies like nuclear power systems for space applications and new semiconductor materials specifically designed for radiation environments are creating additional avenues for market expansion. These technological developments allow manufacturers to address previously untapped applications in both government and commercial sectors.

RADIATION HARDENED POWER PRODUCTS MARKET TRENDS

Increasing Demand for Space Exploration Drives Market Growth

The global Radiation Hardened Power Products market is witnessing accelerated growth, primarily fueled by the increasing investment in space exploration programs. With NASA’s Artemis mission reviving lunar exploration and commercial space ventures like SpaceX pushing the boundaries of deep space missions, the demand for robust power solutions that can withstand high-radiation environments has risen significantly. The market, valued at $221 million in 2024, is projected to grow at a CAGR of 6.1%, reaching $374 million by 2032. Space agencies and private aerospace companies are prioritizing radiation-hardened electronics to ensure reliable satellite, rover, and spacecraft operations, further enhancing market expansion.

Other Trends

Advancements in Semiconductor Technology

Innovations in semiconductor manufacturing have led to the development of radiation-hardened power products with enhanced efficiency and reliability. Technologies such as silicon carbide (SiC) and gallium nitride (GaN) are being increasingly integrated into these components, offering superior thermal stability and radiation resistance. Manufacturers like Infineon and Renesas are investing in R&D to produce next-generation power devices that reduce power losses and improve mission-critical performance. Despite the rise of commercial-off-the-shelf (COTS) components in some applications, radiation-hardened variants remain irreplaceable for aerospace and defense applications due to their guaranteed performance under extreme conditions.

Military Modernization and Defense Applications

Military forces globally are modernizing their electronic warfare and communication systems, directly contributing to the demand for radiation-hardened power products. These components are critical for tactical systems deployed in harsh environments, including nuclear facilities and high-altitude defense platforms. Furthermore, the integration of AI-driven power management systems in defense electronics necessitates radiation-tolerant components to ensure uninterrupted functionality. While commercial sectors such as industrial IoT and automotive also benefit from radiation-hardened technology, defense applications dominate due to stringent reliability requirements and increased defense budgets in regions like North America and Europe.

COMPETITIVE LANDSCAPE

Key Industry Players

Radiation-Hardened Power Market Sees Strategic Moves as Space and Defense Demand Rises

The global radiation-hardened power products market is characterized by intense competition among established semiconductor companies and specialized aerospace/defense manufacturers. While the market remains semi-consolidated, recent years have seen increased crossover between commercial semiconductor firms and traditional radiation-hardened component suppliers. Renesas Electronics Corporation and Infineon Technologies have emerged as technology leaders, leveraging their commercial power semiconductor expertise to develop radiation-tolerant solutions for space applications.

Meanwhile, defense contractors like BAE Systems continue dominating mission-critical military applications through proprietary radiation-hardening techniques developed over decades. The company’s vertically integrated manufacturing approach gives it unique advantages in custom radiation-hardened power solutions for satellite and spacecraft applications. Their recent partnership with NASA for lunar missions underscores this technological leadership.

New entrants such as EPC Space are disrupting traditional radiation-hardening approaches with innovative gallium nitride (GaN) based solutions. These next-generation power devices demonstrate superior radiation tolerance compared to conventional silicon-based components – a key reason why the company secured $15 million in Series B funding in early 2024 specifically for space power product development.

The market also sees strong competition from niche players: VPT Inc. specializes in radiation-hardened DC-DC converters used in satellites, while TTM Technologies focuses on radiation-tolerant power distribution systems. Both companies have expanded production capacity in 2024 to meet growing demand from commercial space operators.

Interestingly, European firm STMicroelectronics has made significant inroads by adapting its automotive-grade power management ICs for radiation environments, demonstrating how cross-industry technology transfer is reshaping competitive dynamics. Their radiation-hardened voltage regulators now power several Earth observation satellites, proving commercial semiconductor processes can be successfully adapted for space applications.

List of Key Radiation-Hardened Power Product Manufacturers

- Renesas Electronics Corporation (Japan)

- BAE Systems (UK)

- Infineon Technologies AG (Germany)

- Power Device Corporation (PDC) (USA)

- VPT, Inc (USA)

- Frontgrade Technologies (USA)

- TTM Technologies, Inc. (USA)

- EPC Space (USA)

- Micross Components (USA)

- STMicroelectronics (Switzerland)

- Texas Instruments (USA)

Segment Analysis:

By Type

Radiation Hardened Current Limiters Segment Shows Strong Demand Due to Rising Space Applications

The market is segmented based on type into:

- Radiation Hardened Current Limiters

- Radiation Hardened Gate Drivers

- Radiation Hardened Linear Voltage Regulators

- Radiation Hardened PWM Controllers

- Others

By Application

Satellite Applications Lead Market Share with Increased Space Exploration Initiatives

The market is segmented based on application into:

- Satellite

- Space Station

- Deep Space Exploration

- Others

Regional Analysis: Radiation Hardened Power Products Market

North America

North America leads the global radiation-hardened power products market, driven by extensive space exploration initiatives and advanced military applications. The U.S. dominates the region, accounting for over 60% of the market share due to heavy investment in defense and aerospace sectors. NASA’s Artemis program, along with growing private sector involvement from companies like SpaceX and Blue Origin, fuels demand for reliable rad-hard power solutions. Stringent quality standards and high R&D expenditure further reinforce North America’s position as the largest revenue contributor. The region is also home to key players like BAE Systems, VPT Inc., and Power Device Corporation (PDC), strengthening its technological leadership.

Europe

Europe’s market growth centers on nuclear energy applications and satellite communications, with agencies like ESA driving innovation. The region prioritizes radiation-hardened power products for both civilian and defense applications, particularly in countries with nuclear power infrastructure. Regulatory frameworks such as the European Space Components Coordination (ESCC) ensure standardized reliability for harsh environments. Though market growth faces competition from North American suppliers, European firms like STMicroelectronics and Infineon are gaining traction with localized semiconductor solutions. However, budget constraints in some EU nations slow adoption rates compared to North America.

Asia-Pacific

Asia-Pacific is the fastest-growing market, projected to surpass Europe by 2027, with China and Japan leading production and adoption. China’s aggressive space program and military modernization efforts account for nearly 40% of regional demand. India’s ISRO and Japan’s JAXA also contribute significantly, leveraging cost-effective rad-hard power solutions for satellites. While local manufacturers like Renesas Electronics compete globally, price sensitivity in emerging economies encourages hybrid solutions combining radiation tolerance with affordability. The lack of standardized testing facilities in some countries remains a market restraint.

Middle East & Africa

This emerging market shows potential through growing interest in satellite communications and nuclear energy. The UAE’s space agency and Saudi Arabia’s Vision 2030 investments are creating demand for radiation-hardened components, though reliance on imports persists. Limited local manufacturing capabilities and insufficient R&D funding hinder rapid growth, but partnerships with global players are gradually improving accessibility. Israel stands out as a regional hub for military-grade rad-hard electronics due to its advanced defense sector.

South America

South America’s market remains niche, primarily serving academic and limited commercial satellite projects. Brazil’s space agency (AEB) and Argentina’s CONAE drive most regional demand, though economic instability restricts large-scale investments. Local supply chains are underdeveloped, forcing dependence on North American and European suppliers. Despite these challenges, collaborations with global space organizations signal long-term growth opportunities in research-focused applications.

Report Scope

This market research report provides a comprehensive analysis of the Global Radiation Hardened Power Products Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 221 million in 2024 and is projected to reach USD 374 million by 2032, growing at a CAGR of 6.1%.

- Segmentation Analysis: Detailed breakdown by product type (Radiation Hardened Current Limiters, Gate Drivers, Linear Voltage Regulators, PWM Controllers) and application (Satellite, Space Station, Deep Space Exploration) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with the U.S. and China being key growth markets.

- Competitive Landscape: Profiles of leading market participants including Renesas, BAE Systems, Infineon, Power Device Corporation (PDC), Frontgrade, VPT, Inc, and others, with their market share and strategic developments.

- Technology Trends & Innovation: Assessment of emerging radiation-hardening technologies, material innovations, and design improvements for space-grade electronics.

- Market Drivers & Restraints: Evaluation of factors such as increasing space exploration missions, satellite deployments, and defense applications, along with challenges like high development costs and stringent certification requirements.

- Stakeholder Analysis: Insights for component manufacturers, space agencies, defense contractors, and investors regarding market opportunities and strategic positioning.

The report employs primary and secondary research methods, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Radiation Hardened Power Products Market?

-> Radiation Hardened Power Products Market was valued at 221 million in 2024 and is projected to reach US$ 374 million by 2032, at a CAGR of 6.1% during the forecast period.

Which key companies operate in this market?

-> Key players include Renesas, BAE Systems, Infineon, Power Device Corporation (PDC), Frontgrade, VPT, Inc, TTM Technologies, EPC Space, Micross, and STMicroelectronics.

What are the key growth drivers?

-> Key growth drivers include increasing space exploration activities, growing satellite deployments, and rising defense applications requiring radiation-hardened electronics.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is expected to show the fastest growth due to expanding space programs in China and India.

What are the emerging trends?

-> Emerging trends include development of more compact and efficient radiation-hardened power solutions, integration of advanced materials, and increasing adoption of commercial-off-the-shelf (COTS) components for space applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...