Quantum Optoelectronics Market Insights

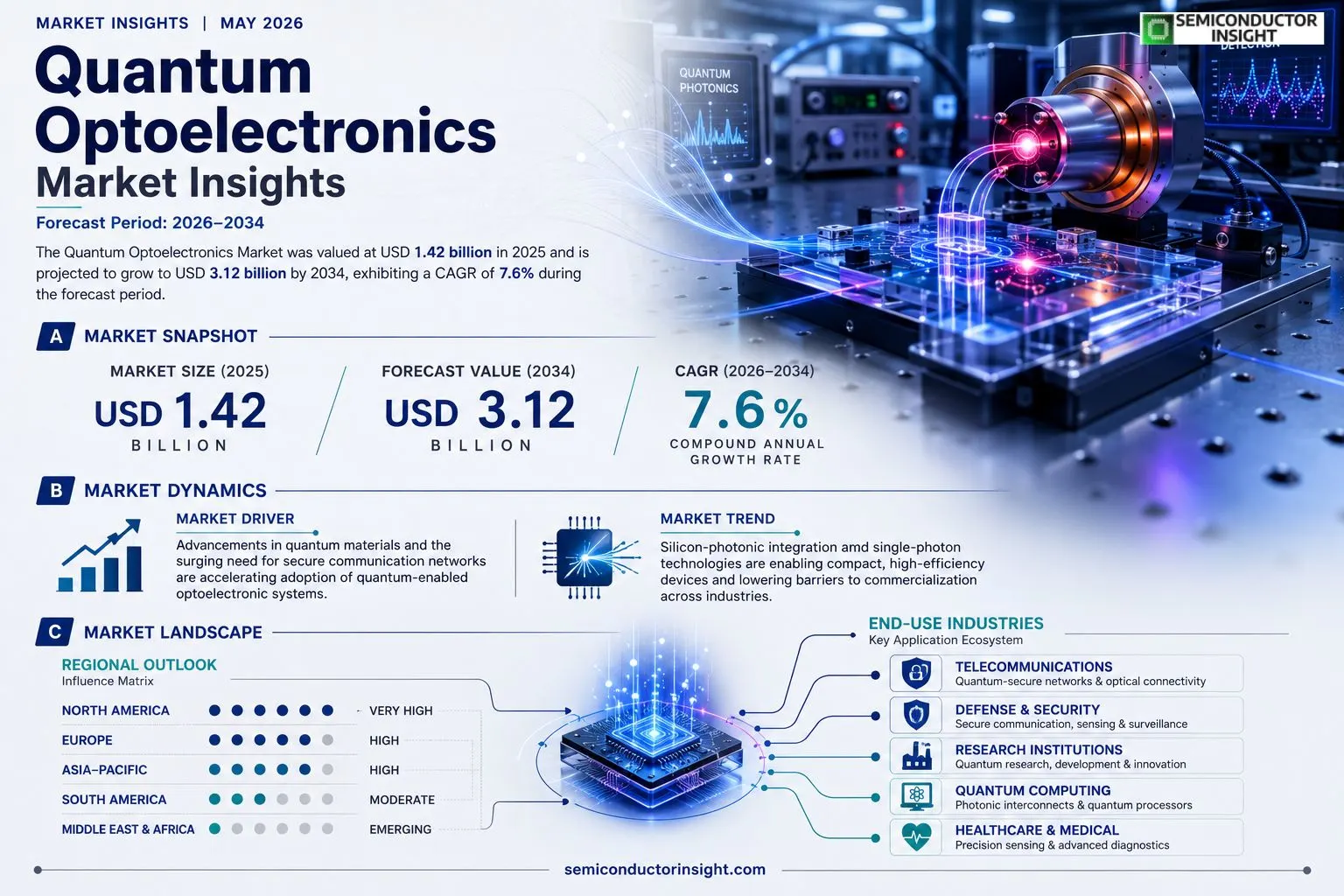

Quantum optoelectronics market size was valued at USD 1.42 billion in 2025. The market is projected to grow from USD 1.45 billion in 2025 to USD 3.12 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period.

Quantum optoelectronics encompasses devices that manipulate light at the Quantum level for applications such as Quantum communication, sensing, and computing. Core technologies include single‑photon sources, superconducting nanowire detectors, entangled‑photon emitters, and integrated photonic circuits that enable coherent control of Quantum states.

The market is experiencing rapid growth because substantial capital is flowing into Quantum research hubs and because demand for secure communication links is rising worldwide. Furthermore, breakthroughs in silicon‑photonic integration are lowering cost barriers, while collaborations,such as the March 2024 partnership between Intel and Hamamatsu on hybrid photon‑detector modules,are accelerating commercialization. Key players such as IBM Quantum, Thorlabs, and NTT Research continue to expand their portfolios, reinforcing the upward trajectory.

MARKET DRIVERS

Advancements in Quantum Materials

The rapid progress in low‑dimensional Quantum materials, such as Quantum wells and Quantum dots, is fueling Quantum Optoelectronics Market. Researchers are achieving higher photon‑electron coupling efficiencies, which enable more compact and energy‑efficient devices across telecommunications and sensing.

Growth of Quantum Communication Networks

Governments and private enterprises are investing heavily in Quantum‑secure communication infrastructure. This creates a direct demand for Quantum‑enabled optoelectronic components, including single‑photon emitters and ultra‑low‑noise detectors, accelerating market adoption.

➤ “The convergence of Quantum computing research and photonic integration is poised to redefine data transmission speeds.”

In addition, the rise of integrated photonic platforms that support on‑chip Quantum light sources is reducing system‑level complexity, making Quantum optoelectronic solutions more accessible to a broader range of industries.

MARKET CHALLENGES

Manufacturing Scalability

Scaling laboratory‑grade Quantum optoelectronic devices to volume production remains a significant hurdle. Precise control over material uniformity and defect density is required, and current semiconductor fabs are only beginning to adapt.

Other Challenges

Standardization Gaps

The lack of universally accepted performance standards for Quantum photonic components hampers interoperability and slows market confidence.

MARKET RESTRAINTS

High Production Costs

Fabrication of Quantum‑grade optoelectronic devices often requires specialized equipment and ultra‑clean environments, leading to cost structures that exceed those of conventional photonic components. These elevated expenses limit early‑stage adoption, especially in price‑sensitive sectors.

MARKET OPPORTUNITIES

Emerging Quantum Sensing Applications

Quantum optoelectronic sensors, leveraging phenomena such as squeezed light and entanglement, are opening new avenues in precision imaging, biomedical diagnostics, and environmental monitoring. These applications promise sizable revenue streams for early innovators.

Strategic Partnerships and Ecosystem Development

Collaboration between semiconductor manufacturers, research institutions, and system integrators is accelerating the development of turnkey Quantum optoelectronic solutions. Such partnerships reduce time‑to‑market and create a robust ecosystem that can sustain long‑term growth of Quantum Optoelectronics Market.

Quantum Optoelectronics Market Trends

Rapid Expansion of Silicon‑Photonic Integration

Quantum Optoelectronics Market is witnessing a swift shift toward silicon‑photonic platforms that merge traditional semiconductor processing with Quantum‑grade optical functionality. By leveraging mature CMOS lines, manufacturers can embed waveguides, modulators, and detectors on a single chip, cutting assembly steps and reducing unit cost. This integration directly supports Quantum communication links and on‑chip sensing arrays, allowing enterprises to deploy secure channels without extensive bulk‑optics installations. Design houses are standardizing a common waveguide geometry that simplifies inter‑vendor compatibility, and foundries are offering dedicated process design kits for Quantum‑photonics, accelerating time‑to‑volume production. In parallel, reliability data from early field trials show photon loss below 2 dB per centimeter, a threshold that enables practical Quantum repeaters. The trend is reinforced by multiple pilot production runs that demonstrate reliable photon‑pair generation and low‑loss routing across centimeter‑scale circuits, positioning silicon‑photonics as the backbone for next‑generation Quantum networks.

Other Trends

Funding and Collaborative Ecosystem

Public and private capital continues to flow into research hubs that specialize in Quantum photonics, creating a dense network of joint development agreements. Government programmes in North America, Europe, and Asia have earmarked billions of dollars for secure‑communication infrastructure, while venture‑capital funds target early‑stage photon‑engine companies. Notable collaborations such as the 2024 Intel‑Hamamatsu partnership on hybrid photon‑detector modules exemplify how hardware manufacturers and component specialists align product roadmaps. Likewise, IBM Quantum and NTT Research have expanded joint‑lab programs that accelerate prototype validation for entangled‑photon emitters. These alliances shorten time‑to‑market and broaden the supply chain, reinforcing confidence among mid‑size suppliers entering Quantum Optoelectronics Market. The growing ecosystem also supports talent pipelines, with university spin‑outs feeding patented designs into commercial portfolios, further stabilizing market momentum.

Advances in Single‑Photon Sources

Recent progress in deterministic single‑photon emitters, particularly those based on Quantum‑dot technology, is reshaping system design. Improved extraction efficiency and spectral purity enable direct integration with on‑chip detectors, eliminating bulky external sources. Commercial vendors now offer turnkey modules that deliver sub‑nanosecond timing jitter, meeting the stringent requirements of Quantum key distribution and high‑resolution sensing. In addition, emerging control electronics that operate at cryogenic temperatures are simplifying the overall device stack, reducing the need for separate cooling infrastructure. This evolution reduces the engineering overhead for end‑users and encourages adoption across sectors such as finance, defense, and telecommunications. Analysts anticipate that as reliability benchmarks converge with classical photonic standards, Quantum Optoelectronics Market will transition from niche research projects to broadly deployed secure‑communication links and sensor networks.

COMPETITIVE LANDSCAPEKey Industry Players

Quantum Optoelectronics Market Competitive Overview

Quantum Optoelectronics Market is anchored by a handful of large, vertically integrated firms that dominate both research funding and product roll‑out. IBM Quantum leverages its extensive cloud‑based Quantum computing platform to commercialize superconducting nanowire single‑photon detectors, while Intel’s partnership with Hamamatsu Photonics accelerates hybrid photon‑detector modules that combine silicon photonics with high‑efficiency avalanche photodiodes. These collaborations underpin a market structure where a few heavyweight innovators set performance benchmarks and shape supply‑chain standards for integrated photonic circuits, entangled‑photon sources, and secure Quantum communication modules. The projected CAGR of 7.6 % reflects the scale‑up of these core technologies as capital flows from governmental Quantum initiatives into commercial deployments.Beyond the leaders, a vibrant ecosystem of niche specialists enriches the competitive landscape. Thorlabs supplies precision opto‑mechanical components and custom single‑photon sources, while NTT Research advances entangled‑photon emitters for metropolitan‑scale Quantum networks. Emerging firms such as Qubitekk and Xanadu focus on scalable photonic Quantum processors, and PsiQuantum pursues error‑corrected silicon‑photonics chips. Japanese and Korean manufacturers like Murata and Samsung Electro‑Mechanics contribute high‑frequency modulators and low‑noise superconducting detectors. European players including AXT and Quintessence Labs drive standards‑driven integration for Quantum‑safe communication, ensuring that market growth is balanced across large‑scale integrators and specialized component innovators.

List of Key Quantum Optoelectronics Companies Profiled

- IBM Quantum

- Intel

- Hamamatsu Photonics

- Thorlabs

- NTT Research

- Qubitekk

- Xanadu

- PsiQuantum

- Murata Manufacturing

- Samsung Electro‑Mechanics

- AXT

- Quintessence Labs

- Photonics Research Institute

- CleverTap

- Quantum Devices GmbH

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Single‑Photon Sources are emerging as the cornerstone of Quantum optoelectronics because they enable deterministic generation of Quantum bits of light. Their flexibility across platforms fuels rapid adoption.

|

| By Application |

|

Quantum Communication drives the market as enterprises and governments prioritize tamper‑proof data exchange. The unique ability of Quantum channels to detect eavesdropping creates a compelling value proposition.

|

| By End User |

|

Telecommunications represents the largest end‑user cohort, motivated by the need for Quantum‑grade encryption across backbone networks.

|

| By Technology |

|

Silicon‑Photonic Integration is gaining prominence because it leverages the mature silicon manufacturing ecosystem to host Quantum components.

|

| By Market Drivers |

|

Capital Investment fuels ecosystem growth, with research consortia and venture capital backing accelerating technology readiness.

|

Regional Analysis: North America

United States

The defense and aerospace sectors are major drivers for Quantum Optoelectronics in the US. Quantum sensors are increasingly being explored for navigation, surveillance, and threat detection. Furthermore, Quantum communication technologies are gaining traction for secure data transmission in sensitive environments. The focus on enhanced cybersecurity within these sectors is boosting the demand for Quantum cryptography solutions.

The telecommunications industry in the US is actively exploring Quantum key distribution (QKD) for enhanced data security in long-haul networks. Quantum repeaters, while still in development, hold the potential to revolutionize the scalability of Quantum networks. Furthermore, Quantum-enhanced optical amplifiers are being investigated to improve the performance of existing fiber optic infrastructure and support future high-bandwidth communication needs.

Significant investments are being directed towards Quantum computing research and development in the US. Major universities and research institutions are leading the way in developing Quantum algorithms and hardware. The government’s Quantum Initiative is providing substantial funding for these efforts. This focus on Quantum computing is creating a strong ecosystem for Quantum Optoelectronics, as it relies heavily on advanced photonics and laser technologies.

Quantum optoelectronics plays a vital role in advanced scientific instrumentation and sensing technologies. Quantum sensors are being developed for applications in medical imaging, environmental monitoring, and materials science. The ability of Quantum sensors to detect extremely weak signals offers enhanced precision and sensitivity compared to classical sensors. This is creating new opportunities for Quantum Optoelectronics in diverse scientific fields.

Europe

Europe is experiencing a growing interest in Quantum Optoelectronics, fueled by government initiatives like the Quantum Flagship. Countries such as Germany, France, and the UK are investing heavily in research and development. The region’s strengths lie in fundamental research, laser technology, and photonics manufacturing. Europe is particularly focused on developing Quantum communication infrastructure and exploring applications in industrial sensing and metrology. While the market is fragmented, collaborations between academic institutions and industry players are accelerating innovation. The emphasis on sustainable technologies also aligns with the potential of Quantum optoelectronics for energy-efficient applications.

Asia-Pacific

Asia-Pacific, particularly China and Japan, presents a significant growth opportunity for Quantum Optoelectronics Market. China’s government is actively promoting the development of Quantum technologies through substantial investments and strategic planning. Japan possesses strong technological capabilities in photonics and optoelectronics, and is focusing on applications in telecommunications and industrial automation. The region’s large manufacturing base provides a favorable environment for scaling up production of Quantum Optoelectronics components and systems. Competition is intense, with both domestic and international players vying for market share. The focus on high-tech manufacturing and advanced infrastructure is driving demand for Quantum-enhanced solutions.

South America

South America represents a nascent market for Quantum Optoelectronics, with opportunities emerging in areas such as scientific research and telecommunications infrastructure. Brazil and Argentina are the largest economies in the region and are showing increasing interest in advanced technologies. However, the market is currently limited by a lack of strong domestic manufacturing capabilities and a relatively underdeveloped research ecosystem. Government initiatives and international collaborations are crucial for fostering growth in this region. The potential applications include Quantum sensing for environmental monitoring and secure data transmission for financial institutions.

Middle East & Africa

The Middle East and Africa represent a long-term growth potential for Quantum Optoelectronics Market. Countries in this region are increasingly investing in technological advancements to diversify their economies. The focus on smart cities, defense modernization, and energy efficiency is creating opportunities for Quantum Optoelectronics applications. The region’s strategic location and growing infrastructure projects are also contributing to market growth. However, challenges such as limited research capabilities and regulatory hurdles need to be addressed for sustainable development.

Report Scope

This market research report provides a comprehensive analysis of the Quantum Optoelectronics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Quantum Optoelectronics Market?

-> Quantum Optoelectronics Market was valued at USD 1.42 billion in 2025 and is expected to reach USD 3.12 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period.

Which key companies operate in Quantum Optoelectronics Market?

-> Key players include IBM Quantum, Thorlabs, NTT Research, Intel, and Hamamatsu, among others.

What are the key growth drivers?

-> Key growth drivers include significant capital inflow into Quantum research hubs, rising demand for secure communication links, breakthroughs in silicon‑photonic integration, and strategic collaborations such as the Intel‑Hamamatsu partnership.

Which region dominates the market?

-> The provided reference does not specify a dominant region for Quantum Optoelectronics Market.

What are the emerging trends?

-> Emerging trends include single‑photon sources, superconducting nanowire detectors, entangled‑photon emitters, integrated photonic circuits, and silicon‑photonic integration.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...