Power Management IC Market Insights

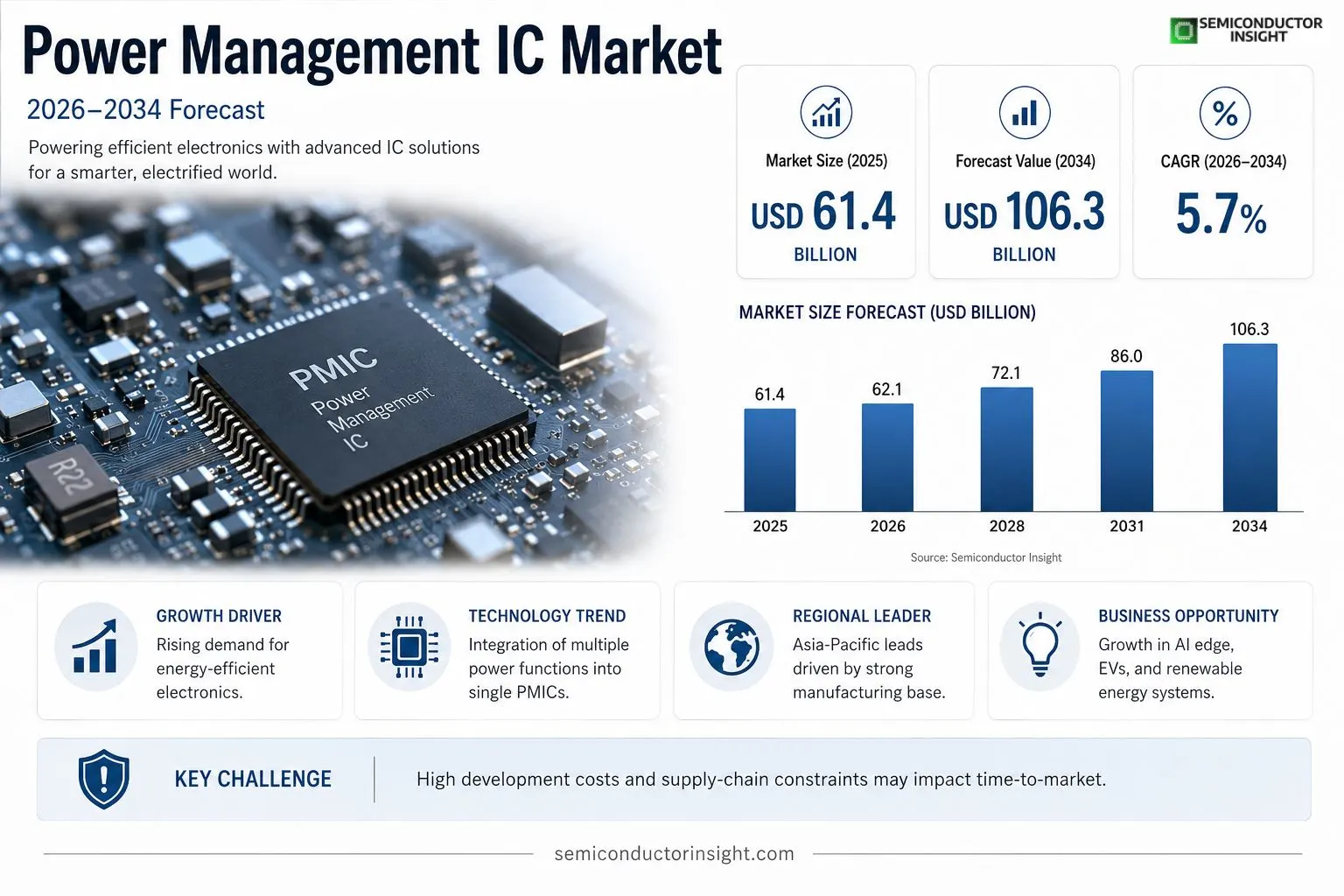

Global Power Management IC market size was valued at USD 61.4 billion in 2025. The market is projected to grow from USD 62.1 billion in 2026 to USD 106.3 billion by 2034, exhibiting a CAGR of 5.7% during the forecast period.

Power Management Integrated Circuits are semiconductor devices that regulate voltage, control power distribution, and improve energy efficiency across electronic systems ranging from smartphones to electric vehicles.These ICs include voltage regulators, battery‑management solutions, DC‑DC converters, and load‑switches, enabling precise power sequencing and protection.Because modern electronics demand higher performance while minimizing energy consumption, manufacturers continuously innovate on silicon‑on‑insulator technologies and digital control architectures.Furthermore, the rise of IoT devices and autonomous vehicles drives demand for highly integrated PMICs that combine multiple functions into compact footprints.

MARKET DRIVERS

Rising Demand for Energy‑Efficient Electronics

The rapid adoption of energy‑saving technologies in consumer devices is pushing manufacturers to integrate advanced power management solutions. This trend fuels Power Management IC Market as designers seek higher efficiency to extend battery life.

Growth of Electric Vehicles and Renewable Energy

Electric vehicle (EV) penetration and the expansion of solar‑plus‑storage systems require robust regulation of high‑power currents, creating a sizable demand for specialized power ICs. The market benefits from the convergence of automotive electrification and grid‑level renewable integration.

➤ “Power management is the backbone of every modern electronic system, and its importance will only increase as devices become smarter.”

In addition, the proliferation of IoT endpoints and 5G infrastructure drives the need for compact, low‑dropout regulators and DC‑DC converters, further accelerating market growth.

MARKET CHALLENGES

Complexity of Design and Integration

Design engineers face increasing complexity when integrating multiple power domains, requiring advanced simulation tools and stringent validation processes. This can extend development cycles and raise costs.

Other Challenges

Supply‑Chain Constraints

Global semiconductor shortages and geopolitical tensions have intermittently limited component availability, affecting timely product launches and inventory planning.

MARKET RESTRAINTS

High Development Costs

Developing high‑performance power management ICs involves substantial R&D investment, particularly for advanced semiconductor nodes. Smaller OEMs may lack the capital to compete, limiting market participation.Regulatory compliance, such as stringent energy‑efficiency standards, adds further testing expenses, which can deter entry of new vendors.Additionally, the need for extensive reliability testing across temperature and voltage extremes increases time‑to‑market for innovative products.

MARKET OPPORTUNITIES

Emerging Applications in AI Edge Devices

Artificial intelligence at the edge demands ultra‑low power consumption combined with burst performance, opening opportunities for novel power‑management architectures tailored to AI accelerators.Furthermore, the rollout of 6G networks will require dense, high‑efficiency power solutions for massive MIMO and back‑haul equipment, presenting a sizable growth avenue for Power Management IC Market.Finally, advancements in silicon‑carbide (SiC) and gallium‑nitride (GaN) technologies enable power ICs that can operate at higher voltages and frequencies, unlocking new markets in aerospace and industrial automation.

Power Management IC Market Trends

Integration and Functional Consolidation

Power Management IC Market is increasingly driven by the need to pack multiple power functions into a single silicon footprint. Designers of smartphones, wearables, and electric vehicles are favoring highly integrated PMICs that combine voltage regulation, battery‑management, and load‑switching capabilities. This approach reduces board space, lowers bill‑of‑materials, and simplifies thermal management. Silicon‑on‑insulator technologies and digital control loops are becoming standard, enabling precise sequencing and real‑time adaptation to workload changes. As a result, product families are expanding to support a broader range of input voltages while maintaining tight efficiency targets, a trend that is reshaping supplier portfolios across the ecosystem.

Other Trends

Energy Efficiency in Mobile Devices

Mobile platforms continue to demand sub‑20‑milliwatt standby power, prompting Power Management IC Market to innovate with ultra‑low‑quiescent‑current regulators and adaptive power‑gating schemes. Advanced architectures monitor usage patterns and dynamically scale voltage rails, delivering noticeable extensions in battery life without compromising performance. The industry’s focus on high‑density, multi‑output converters also supports fast‑charging standards while mitigating heat generation, a critical factor for slim‑form‑factor designs.

Advanced Control Architectures for Automotive

In the automotive sector, safety‑critical applications and the rise of autonomous driving are steering Power Management IC Market toward robust digital controllers with built‑in fault detection and redundancy features. These devices manage high‑voltage traction batteries and low‑voltage infotainment systems simultaneously, ensuring seamless power transition during start‑stop events. Moreover, the shift to electrified powertrains requires converters that can operate across wide temperature ranges while maintaining efficiency above 95 %. Suppliers are responding with modular solutions that integrate diagnostics, communication interfaces, and over‑current protection, aligning with the automotive industry’s stringent reliability standards.

COMPETITIVE LANDSCAPEKey Industry Players

Power Management IC Market – Competitive Overview

Power Management IC (PMIC) Market is anchored by a handful of multinational semiconductor firms that control the majority of high‑volume product categories. Texas Instruments (TI) emerges as the clear market leader, leveraging its extensive analog design expertise and a portfolio that spans linear regulators, buck‑boost converters, and integrated battery‑management solutions for smartphones, data‑center servers, and electric‑vehicle platforms. TI’s ability to deliver silicon‑on‑insulator (SOI) technologies, combined with a deep global sales network, translates into a commanding share of the projected USD 106.3 billion market by 2034. The market structure reflects a classic oligopoly: a few large players dominate core segments while maintaining strategic partnerships with original equipment manufacturers (OEMs), whereas a second tier of specialized firms focuses on niche functions such as ultra‑low‑power IoT nodes or high‑voltage automotive modules.Beyond the tier‑one leaders, several technology‑focused companies contribute critical depth to the competitive landscape. Analog Devices and Maxim Integrated (now part of ADI) differentiate themselves through precision analog front‑ends and high‑performance DC‑DC converters targeting industrial and automotive safety systems. Infineon Technologies and NXP Semiconductors concentrate on automotive power‑train and onboard charging solutions, capitalising on the rapid electrification of vehicles. STMicroelectronics, Renesas Electronics, and ON Semiconductor supply mixed‑signal PMICs for consumer wearables and smart‑home devices, often bundling digital control ASICs to meet stringent energy‑efficiency standards. Smaller but highly innovative players such as ROHM Semiconductor, Silicon Labs, Microchip Technology, TDK, and Cypress Semiconductor (now under Infineon) address ultra‑compact IoT modules, wearable health sensors, and 5G infrastructure, where integration density and low quiescent current are decisive. Collectively, these firms intensify R&D competition, accelerate time‑to‑market for next‑generation power architectures, and reinforce a fragmented yet highly collaborative ecosystem.

List of Key Power Management IC Companies Profiled

- Texas Instruments

- Analog Devices

- Infineon Technologies

- STMicroelectronics

- NXP Semiconductors

- Renesas Electronics

- Maxim Integrated

- ON Semiconductor

- Microchip Technology

- ROHM Semiconductor

- Silicon Labs

- TDK

- Cypress Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Switching Regulators dominate due to their superior efficiency and flexibility.

|

| By Application |

|

Automotive is a leading application segment as vehicles require robust power sequencing and high‑efficiency conversion for electric powertrains.

|

| By End User |

|

Device Manufacturers prioritize highly integrated PMICs to meet aggressive miniaturization goals.

|

| By Technology |

|

Digital Power Management is reshaping the market by offering fine‑grained control and programmability.

|

| By Integration Level |

|

Multi‑Function PMICs are gaining traction as they consolidate voltage regulation, sequencing, and monitoring into a single device.

|

Regional Analysis: Asia-Pacific

Asia-Pacific

The industrial sector in Asia-Pacific is a major consumer of power management ICs, utilizing them in a wide range of applications from automation and control systems to power supplies and motor drives. The ongoing expansion of manufacturing facilities and infrastructure projects across the region is driving demand for robust and efficient power solutions.

The vibrant consumer electronics market in Asia-Pacific, driven by a large population and increasing disposable incomes, represents a significant segment for power management ICs. Smartphones, laptops, tablets, and other portable devices rely heavily on these components for battery management, power conversion, and efficient operation.

The automotive industry in Asia-Pacific is undergoing a transformative shift towards electric vehicles and advanced driver-assistance systems (ADAS). This transition is creating a surge in demand for power management ICs that can handle the complex power requirements of EVs and support innovative automotive technologies.

The growing emphasis on renewable energy sources like solar and wind power in Asia-Pacific is driving the need for efficient power management ICs for energy storage, grid integration, and power conversion in renewable energy systems.

North America

North America exhibits a mature power management IC market with a focus on high-performance and energy-efficient solutions for data centers, industrial automation, and automotive applications. While growth rates may be moderate compared to other regions, the market benefits from a strong technological infrastructure and a demand for advanced power solutions.

Europe

Europe’s power management IC market is characterized by stringent energy efficiency regulations and a strong emphasis on sustainability. The automotive and industrial sectors are key drivers of demand, with a growing focus on power solutions for electric vehicles and smart manufacturing.

South America

South America presents a developing power management IC market with growth potential driven by expanding industrialization, infrastructure development, and increasing adoption of consumer electronics. The automotive sector is also emerging as a significant market segment.

Middle East & Africa

The Middle East & Africa region is witnessing increasing demand for power management ICs due to infrastructure development projects, growing industrial activity, and rising demand for consumer electronics. The energy sector is also a key driver, with applications in renewable energy and power distribution.

Report Scope

This market research report provides a comprehensive analysis of the Power Management IC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

-

Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Power Management IC Market?

-> Power Management IC Market was valued at USD 61.4 billion in 2025 and is expected to reach USD 106.3 billion by 2034, reflecting a CAGR of 5.7% over the forecast period.

Which key companies operate in Power Management IC Market?

-> Key players include Texas Instruments, Analog Devices, Infineon Technologies, STMicroelectronics, and NXP Semiconductors.

What are the key growth drivers?

-> Key growth drivers include the expanding demand for energy‑efficient electronics, proliferation of IoT devices, growth of electric and autonomous vehicles, and the need for higher‑performance power management in smartphones and data centers.

Which region dominates the market?

-> Asia‑Pacific is emerging as a fast‑growing region due to strong semiconductor manufacturing bases, while North America and Europe also hold significant market shares.

What are the emerging trends?

-> Emerging trends include integration of multiple power functions into single PMICs, adoption of silicon‑on‑insulator technologies, and the development of digital control architectures to support IoT and autonomous vehicle applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...