Photonics Chip Market Insights

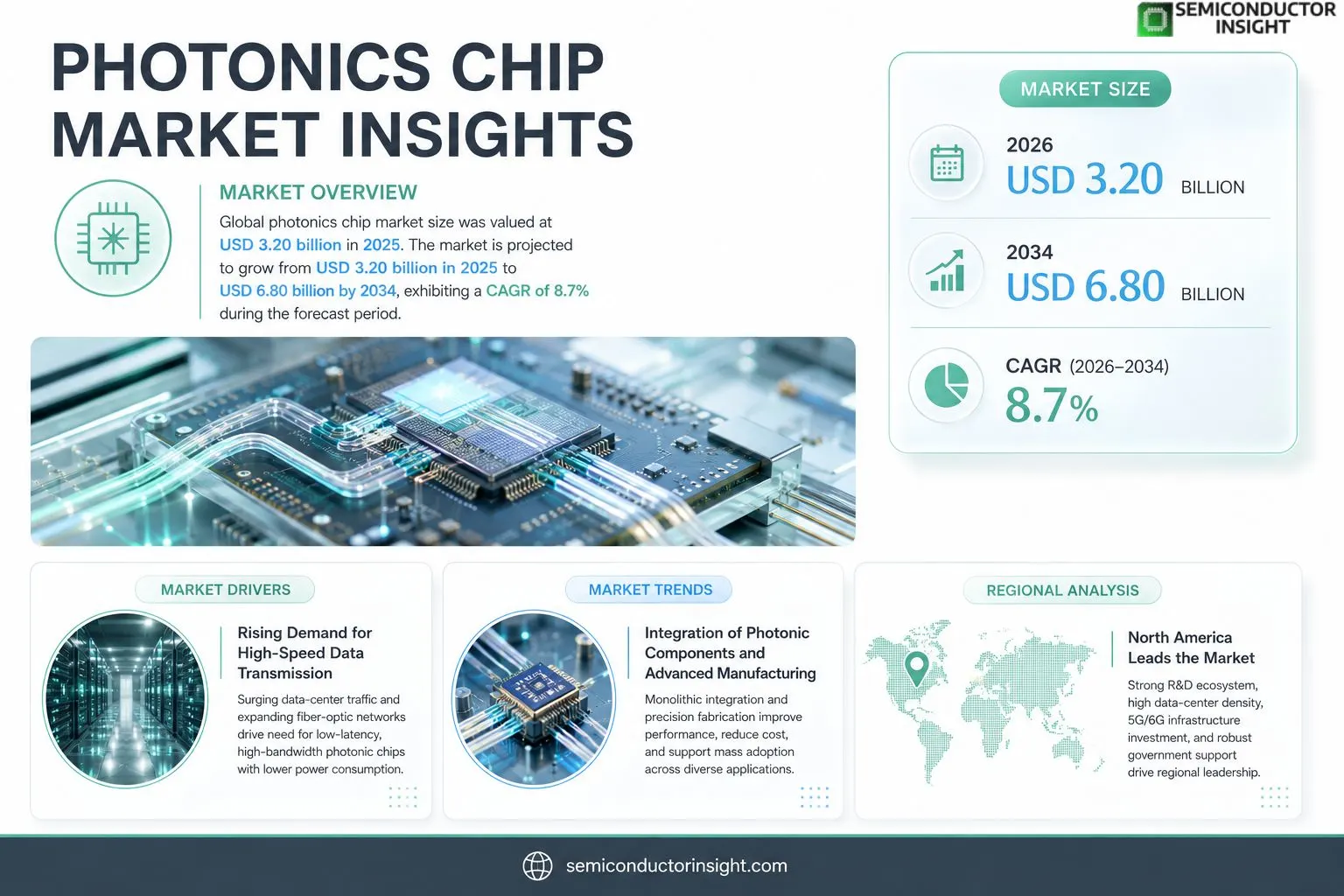

Photonics chip market size was valued at USD 3.20 billion in 2025. The market is projected to grow from USD 3.20 billion in 2025 to USD 6.80 billion by 2034, exhibiting a CAGR of 8.7% during the forecast period.

Photonics chips are miniature integrated optical circuits that manipulate light for data transmission, sensing, and signal processing. They combine waveguides, modulators, detectors and lasers on a single substrate, enabling high‑speed communication while reducing power consumption compared with traditional electronic components.The market is accelerating because telecom operators are expanding fiber‑optic networks, data‑center demand for low‑latency interconnects is rising, and automotive lidar systems are scaling up for autonomous vehicles. Furthermore, government funding for quantum‑photonic research and the rollout of 5G/6G infrastructure are driving adoption. Key players such as Intel Corporation, Lumentum Holdings Inc., Acacia Communications (now part of Cisco), and IBM are investing heavily in advanced manufacturing processes and strategic partnerships to capture growth opportunities.

MARKET DRIVERS

Increasing Demand for High‑Speed Data Transmission

Photonics Chip Market is propelled by exponential growth in data‑center traffic, where carriers require bandwidths beyond 400 Gb/s. Optical interconnects based on photonic chips deliver lower latency and power consumption compared with electrical alternatives, making them essential for next‑generation cloud services.

Advancements in Integrated Photonic Technologies

Recent silicon‑photonic process nodes enable monolithic integration of lasers, modulators, and detectors on a single chip, reducing assembly cost by up to 30 %. These technology gains expand the addressable market beyond telecom to automotive lidar and quantum computing applications.

➤ “Integrated photonics is set to capture 60 % of new optical component spend by 2030,” analysts predict.

Combined, these drivers create a robust pipeline of design wins, positioning Photonics Chip Market for double‑digit CAGR through 2028.

MARKET CHALLENGES

High Capital Expenditure for Foundry Qualification

Manufacturers must invest heavily in specialized cleanrooms and process‑control equipment to meet the stringent tolerance levels of photonic devices. The upfront cost, often exceeding $200 M for a qualified line, deters new entrants and slows scale‑up.

Other Challenges

Supply Chain Fragmentation

Limited wafer suppliers and the reliance on a few laser‑source vendors create bottlenecks that can extend lead times beyond six months, affecting rollout schedules for large‑scale customers.

MARKET RESTRAINTS

Regulatory and Standardization Gaps

Absence of unified performance standards for photonic interconnects hinders cross‑vendor compatibility, forcing system integrators to adopt bespoke validation processes that increase engineering effort and cost.

MARKET OPPORTUNITIES

Emerging Applications in Edge Computing and 6G

Edge devices require ultra‑low‑power optical links to support real‑time AI inference, while the upcoming 6G wireless ecosystem will rely on photonic beam‑forming chips. These nascent segments represent a multi‑billion‑dollar upside for Photonics Chip Market as manufacturers adapt designs for mass production.

Photonics Chip Market Trends

Rapid Expansion Driven by Data‑Center Demand

Photonics Chip Market is experiencing accelerated adoption as telecom operators expand fiber‑optic backbones and data‑center operators seek low‑latency, high‑bandwidth interconnects. Simultaneously, automotive manufacturers scale lidar modules for autonomous driving, creating a broader consumer base for integrated optical solutions. Government initiatives supporting quantum‑photonic research and the ongoing rollout of 5G and emerging 6G infrastructure further reinforce demand for compact, power‑efficient photonic chips. These converging forces collectively push the market toward faster deployment cycles and higher volume production.

Other Trends

Integration of Photonic Components

Design teams are consolidating waveguides, modulators, detectors and on‑chip lasers onto a single substrate to reduce footprint and power consumption. This integration enables seamless signal processing and data transmission while simplifying packaging requirements. Advanced silicon‑photonic platforms and heterogeneous integration techniques are becoming standard practice, allowing manufacturers to tailor performance characteristics for specific applications such as high‑frequency trading, cloud computing and vehicular sensing.

Strategic Partnerships and Advanced Manufacturing

Key industry players are forming alliances to share wafer‑fab capacity, co‑develop next‑generation process nodes, and accelerate time‑to‑market. Investments in high‑precision lithography and wafer‑scale testing are reducing defect rates and improving yield, which supports the shift from low‑volume prototypes to mass‑produced modules. Collaborative R&D programs with academic institutions also stimulate innovation in quantum‑compatible photonic architectures, positioning the market for long‑term growth beyond traditional telecommunications.

COMPETITIVE LANDSCAPEKey Industry Players

Emerging Dynamics in the Photonics Chip Sector

Photonics Chip Market is anchored by a few multinational leaders that dominate both technology development and high‑volume manufacturing. Intel Corporation leverages its silicon‑photonic foundry to ship integrated transceivers for data‑center interconnects, while Lumentum Holdings Inc. supplies high‑performance lasers and modulators for telecom and aerospace applications. Acacia Communications, now part of Cisco, combines advanced coherent optics with Cisco’s networking portfolio, creating a powerful end‑to‑end solution for long‑haul transport. IBM’s research labs continue to push quantum‑photonic integration, positioning the company as a long‑term innovator. These incumbents benefit from deep capital investment, extensive IP portfolios, and strategic alliances with cloud providers and telecom operators, reinforcing a market structure where scale and R&D intensity dictate competitive advantage.Beyond the dominant tier, a vibrant ecosystem of specialist firms fuels niche growth and diversification. NeoPhotonics and Finisar (now part of II‑VI Incorporated) focus on high‑bandwidth transceiver modules for hyperscale data centers. Infinera supplies carrier‑grade coherent optical engines, while Rockley Photonics targets on‑chip sensing and 5G RF‑photonic front‑ends. Regional challengers such as Nokia, Huawei, Samsung, and Globalfoundries are expanding their photonic integration capabilities to capture emerging automotive lidar and quantum‑communication markets. Smaller innovators like Ayar Labs, Aurrion, and Lightwave Logic contribute breakthrough materials and packaging technologies, creating a layered competitive landscape where collaboration and acquisition are common pathways to scale.

List of Key Photonics Chip Companies Profiled

- Intel Corporation

- Lumentum Holdings Inc.

- Acacia Communications (Cisco)

- IBM Research

- NeoPhotonics

- Infinera Corporation

- Finisar (II‑VI Incorporated)

- Rockley Photonics

- Nokia

- Huawei Technologies Co., Ltd.

- Samsung Electronics

- Globalfoundries

- II‑VI Incorporated

- Ayus Photonics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon Photonics – dominates design conversations because it leverages mature CMOS processes, delivering cost‑effective, high‑density integration. – Enables ultra‑low‑latency data‑center interconnects and seamless co‑packaging with electronic drivers. – Attracts telecom operators seeking scalable solutions for expanding fiber‑optic backbones. – Supported by strong ecosystem of foundries and design automation tools, fostering rapid innovation cycles. |

| By Application |

|

Data‑Center Interconnect – the most compelling application because it demands the highest bandwidth density and energy efficiency. – Photonics chips replace electrical transceivers, cutting power consumption while sustaining terabit‑per‑second links. – Drives adoption of coherent modulation formats, improving reach and reliability across metro and long‑haul networks. – Aligns with cloud providers’ strategic focus on latency reduction, making it a priority investment area for leading chip manufacturers. |

| By End User |

|

Cloud & Hyperscale Data Centers – represent the most dynamic end‑user segment, seeking continuous performance improvements. – Prioritize chips that enable dense optical packaging and seamless integration with existing server architectures. – Value the reduced thermal footprint of photonics solutions, supporting sustainable data‑center operations. – Engage in strategic partnerships with chip vendors to co‑develop custom optical engines tuned to workload-specific traffic patterns. |

| By Market Trend |

|

Integration with AI Accelerators – increasingly viewed as a strategic lever to meet the throughput demands of generative AI workloads. – Photonics chips provide optical interconnects that bypass electronic bottlenecks, enabling terabit‑scale data shuffling between AI clusters. – Encourages co‑development of chiplet‑based architectures where photonic and electronic modules are stitched together. – Positions vendors at the forefront of next‑generation computing platforms, aligning with broader industry roadmaps. |

| By Value Chain |

|

Design & IP Licensing – emerging as a critical differentiator for market participants. – Enables rapid time‑to‑market by leveraging proven building blocks, reducing risk for new entrants. – Fuels collaboration between semiconductor foundries and optical specialists, accelerating the creation of standardized photonic libraries. – Encourages ecosystem growth, where software‑defined photonics can be tailored to diverse application needs. |

Regional Analysis: North America

North America

The telecommunications sector represents a major application area for Photonics Chips in North America. The demand for high-speed data transmission in 5G networks and fiber optic infrastructure is driving significant growth. Advancements in optical amplifiers and laser diodes are crucial for enhancing the performance and efficiency of these networks.

The burgeoning data center industry in North America is a key consumer of Photonics Chips. The need for faster and more energy-efficient data transmission within data centers is fueling innovation in optical interconnects and photonic integrated circuits. This market segment is seeing increased adoption of silicon photonics to address bandwidth demands.

The automotive industry is increasingly incorporating Photonics Chips for applications such as LiDAR systems for autonomous driving, advanced driver-assistance systems (ADAS), and in-vehicle communication networks. This represents a growing, albeit nascent, segment of the North American market.

Industrial applications utilizing Photonics Chips include optical sensors for process control, laser-based measurement systems, and advanced manufacturing processes. In the medical sector, Photonics Chips are employed in diagnostic imaging, laser surgery, and optical coherence tomography for advanced medical diagnostics.

Europe

The European Photonics Chip Market is a significant contributor to the global landscape. Several countries, including Germany, France, and the UK, possess strong technological bases and are actively investing in photonic research and development. The push for sustainable technologies and energy efficiency is a key driver, with Photonics Chips playing a vital role in optimizing energy consumption across various sectors. The automotive industry in Europe is also a substantial market, with increasing adoption of LiDAR and advanced driver-assistance systems which rely on sophisticated photonic components. European regulations regarding data privacy and security are influencing the design and deployment of photonic interconnects used in data centers. The region is focused on developing advanced silicon photonics and integrated photonic solutions to meet the growing demands of diverse applications. Collaboration initiatives between European research institutions and industry stakeholders are crucial for fostering innovation and competitiveness within Photonics Chip Market.

Asia-Pacific

Asia-Pacific represents the fastest-growing region in Photonics Chip Market. Countries like China, Japan, South Korea, and Taiwan are leading the way in manufacturing and innovation. China’s significant investments in 5G infrastructure and high-speed data networks are driving substantial demand for Photonics Chips. South Korea and Taiwan are key hubs for semiconductor manufacturing and are heavily involved in the development of advanced photonic technologies. The automotive sector in Asia-Pacific is also seeing rapid adoption of LiDAR and other photonic applications. Government initiatives to promote domestic manufacturing and reduce reliance on imports are influencing the regional market dynamics. The Asia-Pacific region is witnessing significant growth in the integrated photonic solutions space, driven by the increasing demand for compact and energy-efficient photonic devices. The market is characterized by high competition and rapid technological advancements.

South America

Photonics Chip Market in South America is currently in an early stage of development but is poised for growth. Countries like Brazil and Chile are showing potential as emerging markets. The expansion of telecommunications infrastructure, particularly fiber optic networks, is driving initial demand for Photonics Chips. The mining industry in South America is also a potential market, with applications in remote sensing and process control. Government investments in technology and infrastructure development are expected to fuel further growth in the region. Challenges include limited domestic manufacturing capabilities and reliance on imports. However, the increasing adoption of cloud computing and the growing demand for high-speed data transmission are creating opportunities for Photonics Chip suppliers.

Middle East & Africa

Photonics Chip Market in the Middle East & Africa is a relatively small but growing market. Investments in infrastructure development, particularly in the telecommunications and energy sectors, are driving demand. The region’s focus on smart city initiatives and the expansion of high-speed internet access are also contributing to market growth. The oil and gas industry in the Middle East is a potential consumer of Photonics Chips for remote sensing and pipeline monitoring. The increasing adoption of renewable energy technologies is also creating opportunities for Photonics Chips in solar power and smart grids. Challenges include limited technological infrastructure and a relatively small domestic market. However, increasing government initiatives to promote technological advancement are expected to spur further growth in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the Photonics Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Photonics Chip Market?

-> Photonics Chip Market was valued at USD 3.20 billion in 2025 and is expected to reach USD 6.80 billion by 2034, representing a CAGR of 8.7% over the forecast period.

Which key companies operate in Photonics Chip Market?

-> Key players include Intel Corporation, Lumentum Holdings Inc., Acacia Communications (now part of Cisco), and IBM, among others.

What are the key growth drivers?

-> Key growth drivers include expansion of fiber‑optic networks by telecom operators, rising data‑center demand for low‑latency interconnects, scaling of automotive lidar systems for autonomous vehicles, government funding for quantum‑photonic research, and the rollout of 5G/6G infrastructure.

Which region dominates the market?

-> The reference does not specify a single dominant region.

What are the emerging trends?

-> Emerging trends include integration of photonic chips with quantum computing platforms, advanced AI‑driven design automation, and the development of ultra‑low‑power fabrication processes for next‑generation data‑center and automotive applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...