Optical DSP chip for coherent metro transponder Market Insights

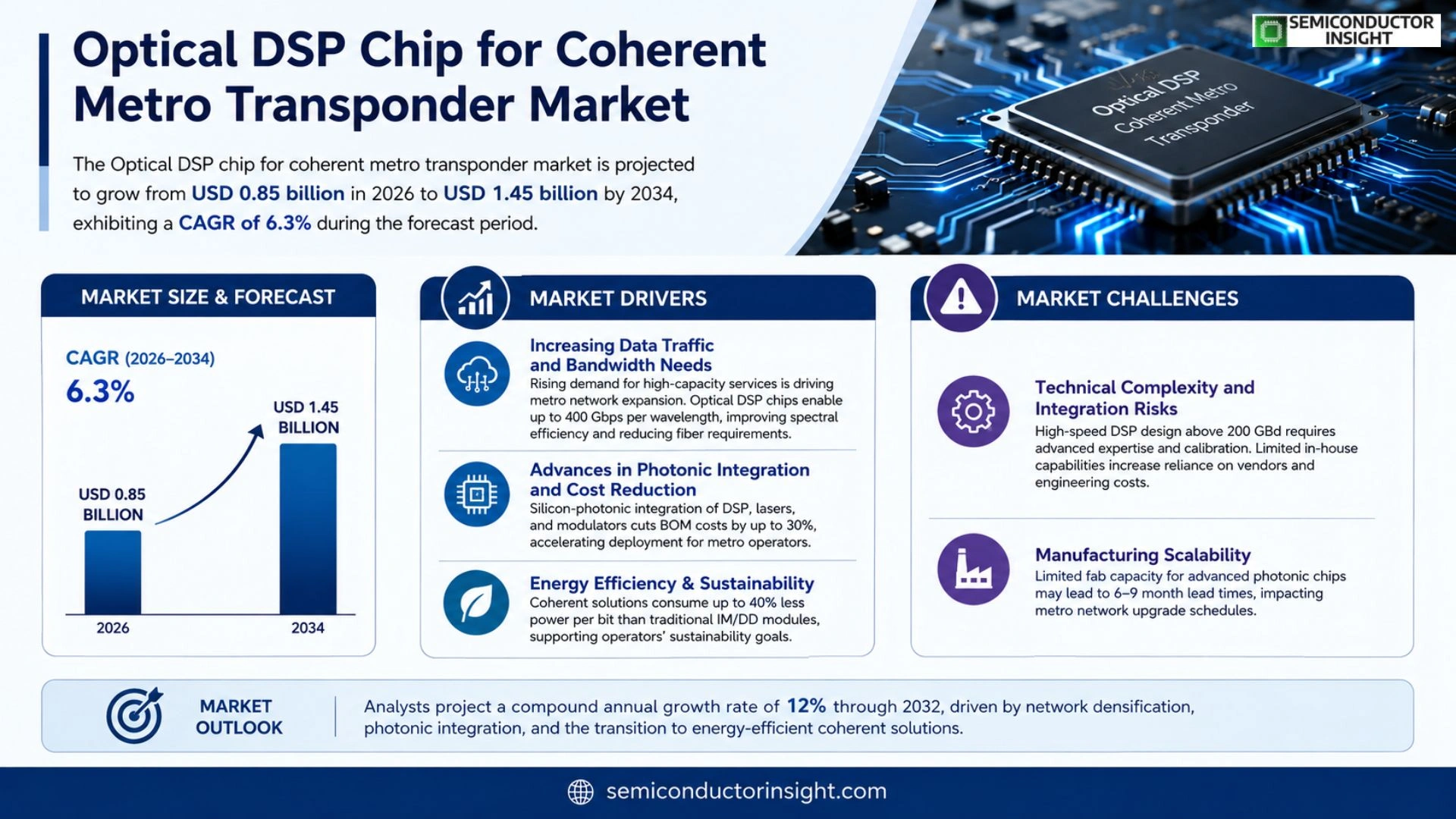

Global Optical DSP chip for coherent metro transponder market is projected to grow from USD 0.85 billion in 2025 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Optical DSP chips enable high‑speed digital signal processing on photonic platforms, allowing coherent detection and advanced modulation formats in metro‑area network transponders. These chips integrate functions such as carrier recovery, equalization, and forward error correction within a compact silicon‑photonic or indium phosphide substrate.

The market is gaining momentum because telecom operators are expanding capacity in dense urban cores, while cost‑effective silicon photonics drives adoption. Furthermore, standards evolution toward higher spectral efficiency and government incentives for fiber‑to‑the‑home deployments are accelerating demand.

MARKET DRIVERS

Increasing Data Traffic and Bandwidth Needs

The rapid expansion of metro networks to support high‑capacity video streaming, cloud services, and edge computing is driving demand for more efficient transponder solutions. Operators are seeking higher spectral efficiency, and Optical DSP chip for coherent metro transponder Market offers the ability to multiplex up to 400 Gbps per wavelength, reducing the number of fibers required.

Advances in Photonic Integration and Cost Reduction

Recent breakthroughs in silicon‑photonic platforms enable integration of DSP functions with lasers and modulators on a single die, lowering bill‑of‑materials by up to 30 %. This integration accelerates deployment cycles and makes coherent transponders financially viable for mid‑size metro operators.

➤ Analysts project a compound annual growth rate of 12 % for Optical DSP chip for coherent metro transponder Market through 2032, propelled by network densification and cost‑effective photonic chips.

Regulatory pushes for energy‑efficient infrastructure also favor coherent solutions, as they consume up to 40 % less power per bit compared with traditional IM/DD modules, aligning with sustainability targets across the telecom sector.

MARKET CHALLENGES

Technical Complexity and Integration Risks

Designing DSP algorithms that operate reliably at line rates above 200 GBd requires sophisticated calibration and signal processing expertise. Operators often lack in‑house capabilities, leading to reliance on qualified vendors, which can slow adoption and increase upfront engineering costs.

Other Challenges

Manufacturing Scalability

Current fab capacity for high‑volume photonic chips is limited to a few specialized fabs. Scaling production to meet projected demand may cause lead‑time extensions of 6–9 months, impacting rollout schedules for metro upgrades.

MARKET RESTRAINTS

High Capital Expenditure (CAPEX) Requirements

Deploying coherent transponders equipped with Optical DSP chips often entails a 10‑15 % premium over conventional solutions due to specialized optics and cooling. For many metro operators with tight budget cycles, justifying this CAPEX without clear short‑term ROI can restrain market expansion.

MARKET OPPORTUNITIES

5G Backhaul and Edge Computing Growth

The rollout of 5G services is creating a surge in backhaul traffic that demands low‑latency, high‑throughput links. Optical DSP chips enable coherent metro transponders to support flexible grid wavelengths and adaptive modulation, positioning them as a key enabler for future‑proof 5G and edge computing infrastructures.

Optical DSP chip for coherent metro transponder Market Trends

Increasing Adoption Driven by Urban Capacity Expansion

Telecom operators are accelerating upgrades in dense urban cores to meet the surge in data traffic generated by cloud services and 5G back‑haul. This network densification directly fuels demand for optical DSP chips that can support coherent detection and advanced modulation formats in metro‑area transponder equipment. The shift from legacy O‑band solutions to integrated silicon‑photonic DSPs is evident across major metropolitan hubs, where capacity constraints are most acute.

Cost‑effective silicon photonics has become a decisive factor, offering high‑volume manufacturing while maintaining the precision required for carrier recovery, equalization, and forward error correction. By consolidating these functions on a single silicon or indium‑phosphide substrate, vendors reduce both bill‑of‑materials and power draw, enabling operators to deploy more transponders per fiber strand without compromising performance.

Regulatory incentives and government‑backed fiber‑to‑the‑home programs further reinforce market momentum. Policies that subsidize fiber rollout in urban districts lower the total cost of ownership for service providers, prompting a quicker transition to coherent metro transponders equipped with modern DSP chips.

Other Trends

Silicon‑Photonic Integration

The industry is witnessing a convergence of photonic integration and digital signal processing. Silicon‑photonic DSP chips now routinely incorporate multi‑channel arrays, allowing simultaneous handling of several wavelength‑division multiplexed (WDM) channels. This integration simplifies the transponder architecture, reduces the need for discrete components, and shortens time‑to‑market for new service offerings.

Manufacturers are also embracing heterogeneous integration, embedding indium‑phosphide gain sections with silicon waveguides to achieve higher optical power levels without sacrificing the compact footprint of silicon platforms. The result is a more robust solution that meets the reliability standards demanded by metro operators.

Standard Evolution and Spectral Efficiency

Emerging standards that prioritize higher spectral efficiency are compelling vendors to embed more sophisticated DSP algorithms. Support for modulation schemes such as 64‑QAM and beyond requires precise phase noise mitigation and error correction, functions that modern optical DSP chips are engineered to perform in real time. This alignment with next‑generation standards ensures that transponders remain future‑proof as network requirements evolve.

In parallel, the push for lower latency in metro networks is driving optimization of DSP pipelines. Engineers are refining algorithmic latency and leveraging parallel processing units within the chip to meet the sub‑microsecond latency targets set by service providers for latency‑sensitive applications like high‑frequency trading and real‑time video streaming.

COMPETITIVE LANDSCAPE

Key Industry Players

Optical DSP Chip for Coherent Metro Transponder Market Overview

The competitive arena is concentrated around a handful of integrated silicon‑photonic and indium‑phosphide specialists that command the bulk of revenue. Intel Corporation leads with its extensive silicon‑photonic foundry, leveraging deep ties to data‑center and telecom ecosystems. Marvell Technology, after acquiring Inphi, supplies high‑bandwidth DSP cores that are increasingly paired with silicon photonics. Lumentum Holdings and II‑VI Incorporated (including the former Finisar portfolio) anchor the supply chain for carrier‑recovery and forward error correction blocks, creating a tiered structure where a few Tier‑1 vendors dominate chipset design while a broader set of silicon foundries provide volume fabrication. This hierarchy sustains a market where differentiation rests on integration depth, power efficiency, and the ability to support emerging modulation formats required for metro‑area coherent transponders.

Niche but strategically important players add depth and specialization. NeoPhotonics focuses on indium‑phosphide electro‑optic integration, delivering high‑performance coherent receivers that complement DSP chips from larger vendors. Cisco Systems, through its Acacia Communications acquisition, offers DSP modules tailored for carrier‑grade networking gear. Ciena Corporation, Nokia and Huawei provide end‑to‑end transponder solutions that embed third‑party DSP IP, influencing specifications and driving adoption in carrier roll‑outs. Broadcom Inc. supplies ancillary high‑speed serializers/deserializers that interface with DSP cores, while emerging fabless firms such as Lightwire and Acacia‑derived startups explore AI‑optimized DSP algorithms for next‑generation spectral efficiency. Collectively, these companies shape a competitive landscape that balances scale‑driven cost advantages with application‑specific innovation.

List of Key Optical DSP Chip Companies Profiled

- Intel Corporation

- Marvell Technology Group

- Lumentum Holdings

- II‑VI Incorporated

- NeoPhotonics Corp.

- Cisco Systems (Acacia Communications)

- Ciena Corporation

- Nokia

- Huawei Technologies Co., Ltd.

- Broadcom Inc.

- Lightwire

- Acacia Communications (now part of Cisco)

- Inphi Corporation (merged with Marvell)

- Finisar (now part of II‑VI)

- VPI Photonics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon‑photonic DSP chips are emerging as the dominant type because they combine mature CMOS manufacturing with high‑density integration.

|

| By Application |

|

Metro‑Ethernet transponders drive the bulk of demand because they address capacity bottlenecks in dense urban cores.

|

| By End User |

|

Telecom operators are the primary end users, seeking to expand bandwidth while managing CAPEX.

|

| By Technology |

|

Monolithic silicon‑photonic integration is gaining traction as it consolidates photonic and electronic functions onto a single die.

|

| By Market Driver |

|

Capacity expansion in dense metros underpins the market narrative.

|

Regional Analysis: North America

The competitive landscape in North America is characterized by the presence of major optical networking equipment vendors and semiconductor manufacturers. Innovation in Optical DSP technology is focused on enhancing performance metrics such as modulation formats, digital signal processing algorithms, and low-latency processing. Government initiatives supporting broadband infrastructure development further contribute to the growth of the Optical DSP chip market.

Ongoing investments in fiber optic infrastructure across North America are a primary driver for Optical DSP chip demand. Network operators are continuously upgrading their networks to support increasing data traffic and emerging applications.

The deployment of 5G networks necessitates high-capacity, long-reach networks, creating a strong demand for coherent metro transponders equipped with advanced Optical DSP chips.

The rapid growth of data centers in North America is driving the need for high-speed interconnects, which rely on coherent optical technologies and sophisticated Optical DSP chips.

Increasing emphasis on energy efficiency in telecommunications networks is pushing the development and adoption of Optical DSP chips that minimize power consumption while maximizing performance.

Europe

Europe exhibits a steady growth trajectory in Optical DSP chip for coherent metro transponder Market. The region’s well-developed telecommunications infrastructure and stringent data privacy regulations influence the adoption of advanced optical networking solutions. Key drivers include the expansion of high-speed internet access, the growth of data-intensive industries, and the increasing demand for secure network communication. The European Union’s initiatives promoting digital connectivity further contribute to market growth. The market in Europe is also witnessing increasing adoption of open optical networking architectures.

The European market is characterized by a mix of established telecom operators and emerging players. Research and development efforts are focused on developing energy-efficient and cost-effective Optical DSP chips that meet the evolving needs of the European telecommunications landscape.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing market for Optical DSP chips in the coherent metro transponder segment. The region’s rapid economic development, increasing internet penetration, and large-scale investments in digital infrastructure are key growth drivers. The deployment of 5G networks, particularly in countries like China and India, is fueling significant demand for advanced optical networking solutions. The burgeoning data center industry in Asia-Pacific also contributes to market expansion. The focus on cloud computing and the Internet of Things (IoT) further accelerates the need for high-capacity, long-reach optical transmission.

The Asia-Pacific market is highly competitive, with both domestic and international players vying for market share. Innovation in Optical DSP technology is geared towards meeting the specific requirements of the region’s diverse telecommunications infrastructure and network deployment scenarios.

South America

South America represents a developing market for Optical DSP chips in the coherent metro transponder segment. The region is witnessing increasing investments in telecommunications infrastructure to improve broadband connectivity and support economic growth. The expansion of data centers and the growing demand for high-speed internet access are driving market growth. Government initiatives promoting digital inclusion and infrastructure development are also contributing to market expansion. The adoption of advanced optical networking technologies is expected to increase in the coming years.

The South American market presents opportunities for growth, but challenges include infrastructure limitations and economic uncertainties. Market players are focusing on providing cost-effective and scalable optical networking solutions to meet the evolving needs of the region.

Middle East & Africa

The Middle East & Africa region presents a promising growth opportunity for Optical DSP chips in the coherent metro transponder market. The region is experiencing rapid economic development and increasing investments in telecommunications infrastructure. Government initiatives focused on digital transformation and the expansion of broadband networks are driving market growth. The deployment of 5G networks and the growth of data-intensive industries are further boosting demand for advanced optical networking solutions. The region’s increasing focus on cloud computing and IoT applications also contributes to market expansion.

The Middle East & Africa market is characterized by diverse regulatory landscapes and infrastructure challenges. Market players are focusing on providing tailored optical networking solutions to meet the specific requirements of the region.

Report Scope

This market research report provides a comprehensive analysis of the Optical DSP chip for coherent metro transponder Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Optical DSP chip for coherent metro transponder Market?

-> Optical DSP chip for coherent metro transponder Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.45 billion by 2034.

Which key companies operate in Optical DSP chip for coherent metro transponder Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...