MARKET INSIGHTS

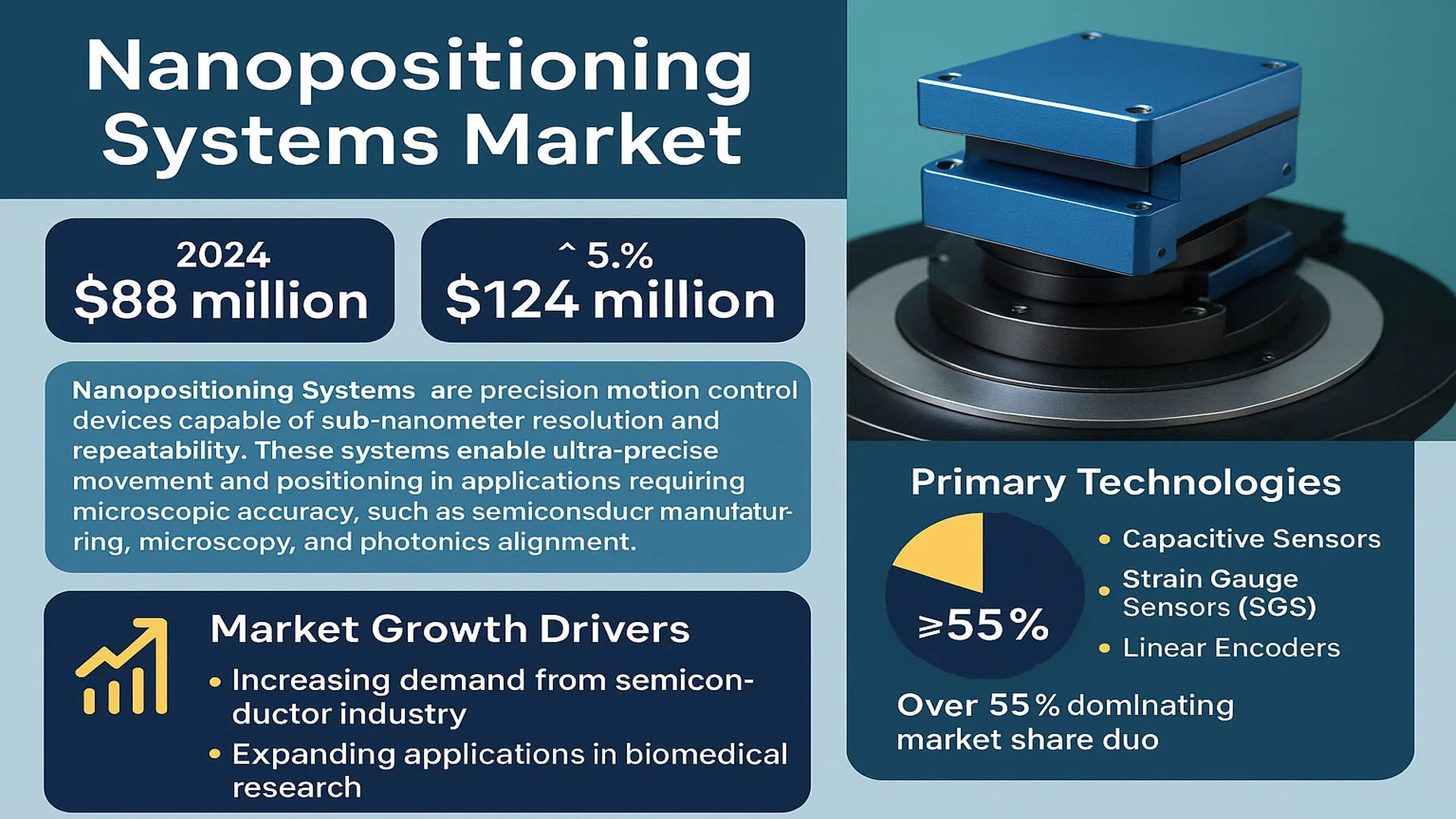

The global Nanopositioning Systems Market was valued at 88 million in 2024 and is projected to reach US$ 124 million by 2032, at a CAGR of 5.1% during the forecast period.

Nanopositioning Systems are precision motion control devices capable of sub-nanometer resolution and repeatability. These systems enable ultra-precise movement and positioning in applications requiring microscopic accuracy, such as semiconductor manufacturing, microscopy, and photonics alignment. The primary technologies include capacitive sensors, strain gauge sensors (SGS), and linear encoders, with capacitive sensors dominating over 55% of the market share due to their high resolution and stability.

Market growth is driven by increasing demand from the semiconductor industry and expanding applications in biomedical research. However, high costs and technical complexity pose challenges. Key players like Physik Instrumente (PI) GmbH and Aerotech are investing in modular designs to improve accessibility. The Asia-Pacific region leads with 42% market share, fueled by semiconductor manufacturing growth in China and South Korea.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand in Semiconductor Manufacturing Accelerates Market Expansion

The nanopositioning systems market is witnessing robust growth due to increasing adoption in semiconductor fabrication processes. As chip manufacturers push towards smaller node sizes below 5nm, the requirement for nanometer-level precision in lithography equipment has intensified. Advanced photolithography systems now incorporate multiple nanopositioning stages to achieve alignment accuracies under 1nm. The semiconductor industry’s projected expansion at nearly 7% annually creates direct demand for high-precision motion systems. Leading manufacturers are developing specialized piezoelectric stages with closed-loop control to meet these exacting requirements.

Advancements in Biomedical Imaging Spur New Applications

Medical research institutions are increasingly adopting nanopositioners for super-resolution microscopy techniques like STED and PALM/STORM. These imaging methods require precise sample positioning to achieve resolutions beyond the diffraction limit, driving demand for compact nanopositioning systems with sub-nanometer stability. The global microscopy market’s expansion, projected to exceed 15 billion annually, indicates sustained growth potential for precision motion components. Researchers developing novel diagnostic techniques particularly value systems combining large travel ranges with atomic-scale positioning accuracy.

Automation in Manufacturing Boosts Industrial Adoption

Industrial quality control systems increasingly incorporate nanopositioning technology for ultra-precise measurement and inspection applications. Automated optical inspection (AOI) systems in electronics manufacturing now routinely achieve micron-level alignment using compact linear nanopositioning stages. This transition towards automated precision manufacturing aligns with broader Industry 4.0 initiatives, creating opportunities for motion system providers. Capacitive sensor-based nanopositioners have gained particular traction in industrial environments due to their non-contact operation and immunity to environmental interference.

MARKET RESTRAINTS

High System Costs Limit Widespread Adoption

While nanopositioning technology offers unparalleled precision, the significant capital investment required presents a barrier for many potential users. Complete systems incorporating high-performance piezoelectric actuators, capacitive sensors, and sophisticated control electronics often exceed budget constraints for academic and smaller industrial users. The need for specialized mounting frames, vibration isolation platforms, and calibration services further increases total cost of ownership. This pricing pressure is particularly acute in price-sensitive emerging markets where adoption remains limited despite growing technical requirements.

Other Restraints

Thermal Sensitivity Challenges

Nanopositioning systems frequently operate at the limits of mechanical and electronic stability, making them susceptible to thermal drift effects. Even minor temperature fluctuations can introduce measurement errors exceeding positioning tolerances, requiring robust environmental controls. This sensitivity complicates deployment in industrial settings where temperature variations are common, limiting application scope despite the technology’s precision advantages.

Integration Complexity

Incorporating nanopositioning systems into existing equipment often requires customized mounting solutions and control integration. The specialized knowledge needed for optimal implementation creates dependency on vendor support, adding to operational costs. Users frequently encounter challenges matching mechanical interfaces, control protocols, and software compatibility between components from different manufacturers.

MARKET CHALLENGES

Precision-Reliability Tradeoff Presents Engineering Dilemma

Manufacturers face persistent challenges balancing sub-nanometer precision with long-term mechanical reliability. Piezoelectric actuators, while offering exceptional resolution, exhibit hysteresis and creep effects that degrade positioning accuracy over time. Though advanced control algorithms mitigate these effects, they complicate system design and require specialized maintenance. The need for regular recalibration and potential component wear create operational challenges for users requiring sustained high precision.

Industry-Wide Component Shortages Disrupt Supply Chains

The specialized nature of nanopositioning components makes manufacturers vulnerable to supply chain disruptions. Critical materials like high-performance piezoceramics and precision ground flexures often face limited supplier availability. These constraints became particularly acute during recent global supply chain disruptions, with lead times for certain components extending beyond twelve months. Manufacturers must balance inventory costs with the need for reliable component availability.

Emerging Challenges

Competition from Alternative Technologies

Emerging technologies like MEMS-based positioning systems and novel actuator designs threaten to disrupt traditional nanopositioning markets. While currently lacking the performance of conventional systems, these alternatives offer advantages in cost, size, and power consumption that appeal to certain applications. Traditional manufacturers must continuously innovate to maintain technological leadership.

MARKET OPPORTUNITIES

Emerging Quantum Technologies Open New Application Frontiers

The rapid development of quantum computing and sensing applications creates significant opportunities for nanopositioning system providers. Quantum research laboratories require extreme precision in component alignment, often at cryogenic temperatures. Specialized cryo-compatible nanopositioners capable of operating below 4K represent a growing niche market. Investment in quantum technologies exceeding several billion dollars annually suggests strong future demand for customized precision motion solutions.

Expansion in Additive Manufacturing Enables Custom Solutions

Advances in metal additive manufacturing allow nanopositioning system producers to create optimized component geometries previously impossible to machine conventionally. This capability enables faster prototyping of custom positioning stages with improved stiffness and reduced moving mass. Manufacturers leveraging these techniques gain competitive advantages in delivering application-specific solutions with enhanced performance characteristics.

Modular System Architectures Address Diverse Needs

The development of modular nanopositioning platforms allows manufacturers to serve broader market segments efficiently. Configurable systems combining standardized motion modules with application-specific components reduce both development time and cost for customized solutions. This approach particularly benefits research institutions and small-scale manufacturers requiring tailored solutions without prohibitive development expenses.

NANOPOSITIONING SYSTEMS MARKET TRENDS

Growing Demand for High-Precision Manufacturing Drives Market Expansion

The global nanopositioning systems market is experiencing robust growth, driven by the increasing demand for ultra-precise motion control in industries such as semiconductor manufacturing, biomedical research, and optics. These systems enable nanometer-level accuracy, which is critical for applications like wafer inspection, laser processing, and atomic force microscopy. Asia-Pacific currently dominates the market with a 42% share, largely due to rapid industrialization and significant investments in semiconductor fabrication plants. The adoption of capacitive sensors, which account for 55% of the market, is particularly strong due to their high resolution and stability in feedback control applications.

Other Trends

Integration with Automation Technologies

The growing automation across industries has created substantial demand for nanopositioning systems that can be seamlessly integrated into robotic workflows. Modern systems increasingly incorporate smart features such as IoT connectivity and AI-based predictive maintenance, enhancing their usability in smart factories. Industrial applications represent 60% of market demand, with expanding use cases in micro-assembly and ultra-precision machining where sub-micron tolerances are required.

Advancements in Piezoelectric Actuation Technology

Recent innovations in piezoelectric materials and control algorithms have significantly improved the performance of nanopositioners, expanding their application scope. Modern systems achieve positioning resolutions below 1 nanometer with response times measured in microseconds – a critical requirement for next-generation photolithography equipment. Leading manufacturers are incorporating advanced vibration damping techniques and thermal compensation mechanisms to maintain stability in high-performance environments. The market is witnessing increased demand for multi-axis configurations that can perform complex 3D alignment tasks essential for photonics packaging and MEMS manufacturing.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders and Innovators Drive Advancement in Precision Positioning Technologies

The global nanopositioning systems market features a competitive landscape where established technology leaders and specialized innovators coexist. The market is characterized by continuous technological advancements and strategic collaborations to meet the increasing demand for ultra-precise positioning solutions across multiple industries.

Physik Instrumente (PI) GmbH emerges as the undisputed market leader, commanding significant global dominance through its comprehensive portfolio of high-performance nanopositioning stages and controllers. As a German precision engineering specialist, PI GmbH has maintained technological leadership through substantial R&D investments averaging 15-20% of annual revenues, resulting in patented piezoelectric and servo motor-driven solutions.

The competitive landscape sees strong participation from Attocube Systems AG and Prior Scientific Instruments (Queensgate), who have carved distinct market positions through specialization in cryogenic and microscopy applications respectively. These players demonstrate expertise in niche applications, enabling them to compete effectively against larger corporations through targeted innovation.

Strategic Developments and Regional Focus

Market leaders are currently pursuing three strategic priorities: geographic expansion into high-growth Asian markets, development of integrated smart positioning systems with IoT capabilities, and strategic acquisitions to broaden application expertise. Notably, Aerotech Inc. recently enhanced its 3D nanopositioning offerings through the acquisition of a specialist motion control firm, while SmarAct GmbH expanded its Asian distribution network.

Chinese manufacturers including Liaoning Yansheng Technology and CoreMorrow are gaining traction by offering cost-competitive alternatives for industrial automation applications, though they currently lag in high-end research and semiconductor market segments dominated by European and American suppliers.

The competitive environment remains dynamic, with increasing vertical integration observed among major players. Companies like Piezosystem Jena now offer complete positioning solutions encompassing mechanics, electronics, and software, creating higher barriers to entry for smaller competitors.

List of Key Nanopositioning System Companies

- Physik Instrumente (PI) GmbH (Germany)

- Attocube Systems AG (Germany)

- Prior Scientific Instruments (UK)

- Piezosystem Jena GmbH (Germany)

- Aerotech Inc. (U.S.)

- SmarAct GmbH (Germany)

- CoreMorrow (China)

- Mad City Labs (U.S.)

- Nanomotion Ltd. (Israel)

- Liaoning Yansheng Technology (China)

- nPoint Inc. (U.S.)

- OME Technology (UK)

Segment Analysis:

By Type

Capacitive Sensors Dominate the Market Owing to High Precision and Stability in Positioning Applications

The market is segmented based on type into:

- Capacitive Sensors

- Subtypes: Single-channel, multi-channel, and others

- Strain Gauge Sensors (SGS)

- Linear Encoders

- Others

By Application

Industrial Use Leads the Market Due to High Adoption in Manufacturing and Automation Processes

The market is segmented based on application into:

- Industrial Use

- Subtypes: Semiconductor manufacturing, precision engineering, and others

- Research Use

- Subtypes: Microscopy, nanotechnology research, and others

By End-User Industry

Semiconductor Industry Drives Demand for High-Precision Nanopositioning Solutions

The market is segmented based on end-user industry into:

- Semiconductor

- Automotive

- Healthcare

- Subtypes: Medical imaging, robotic surgery, and others

- Aerospace & Defense

- Academic & Research Institutions

Regional Analysis: Nanopositioning Systems Market

Asia-Pacific

As the dominant market for nanopositioning systems with a 42% global share, the Asia-Pacific region is fueled by substantial investments in semiconductor manufacturing, nanotechnology research, and industrial automation. China leads regional demand due to its aggressive academic and industrial R&D spending, accounting for over 60% of the region’s market. Japan follows with cutting-edge applications in microscopy and photonics, while India shows growing adoption in biomedical instrumentation. The region benefits from strong government backing for nanoelectronics initiatives and expanding electronics manufacturing ecosystems, though competition from local players like CoreMorrow creates pricing pressures for international suppliers.

North America

Holding 26% of global revenue, North America’s market is characterized by high-value applications in aerospace, defense, and advanced microscopy. The U.S. accounts for 85% of regional demand, driven by National Nanotechnology Initiative funding and precision manufacturing requirements in sectors like semiconductor lithography. Major players including Aerotech and Mad City Labs benefit from collaboration with research institutions, though supply chain vulnerabilities for piezoelectric materials present ongoing challenges. The region leads in commercializing novel applications, particularly in quantum computing alignment systems and adaptive optics.

Europe

Representing 22% of the global market, Europe excels in high-precision nanopositioning solutions for scientific instrumentation and photonics. Germany dominates with specialized manufacturers like PI GmbH and SmarAct leveraging the region’s strong mechanical engineering tradition. EU Horizon 2020 funding continues to support nanotechnology developments, particularly in biomedical applications. However, slower industrial adoption compared to research usage creates imbalances, with academic institutions accounting for 45% of regional demand. The market sees increasing competition from Asian suppliers in industrial segments requiring cost-effective solutions.

South America

Showing nascent but steady growth, the region benefits from expanding university nanotechnology programs in Brazil and Argentina. Industrial adoption remains limited to select automotive and precision engineering applications, composing just 6% of regional consumption. Infrastructure limitations for advanced research and reliance on imported systems constrain market expansion. However, Brazil’s emerging optics and photonics industry presents opportunities, particularly in microscopy applications for agricultural and mining research where precision requirements are less stringent than in semiconductor manufacturing.

Middle East & AfricaAfrica

The market remains in early development stages, with Israel and Saudi Arabia showing the most activity through research partnerships with European and American institutions. Nanotechnology-focused initiatives like Saudi Arabia’s National Nanotechnology Program drive specialized demand, though overall regional penetration is below 4% of global sales. Limited local manufacturing capability creates dependence on imports, while high system costs relative to research budgets slow adoption. Long-term potential exists in oil/gas sensing applications and biomedical research as funding for technical universities increases across the GCC region.

Report Scope

This market research report provides a comprehensive analysis of the global Nanopositioning Systems market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Nanopositioning Systems market was valued at USD 88 million in 2024 and is projected to reach USD 124 million by 2032, growing at a CAGR of 5.1%.

- Segmentation Analysis: Detailed breakdown by product type (Capacitive Sensors, Strain Gauges Sensors, Linear Encoders) and application (Industrial Use, Research Use). Capacitive Sensors dominate with a 55% market share, while Industrial Use accounts for 60% of applications.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific leads with 42% market share, followed by North America (26%) and Europe (22%).

- Competitive Landscape: Profiles of leading market participants including Physik Instrumente (PI) GmbH, Attocube, Prior Scientific, and Piezosystem Jena GmbH. The top 5 players hold 44% market share.

- Technology Trends & Innovation: Assessment of emerging precision positioning technologies, integration with microscopy systems, and advancements in piezoelectric actuators.

- Market Drivers & Restraints: Evaluation of factors including increasing semiconductor manufacturing, nanotechnology research funding, alongside challenges like high system costs.

- Stakeholder Analysis: Insights for equipment manufacturers, research institutions, component suppliers, and investors regarding market opportunities and strategic positioning.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and analysis of company financial reports to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Nanopositioning Systems Market?

-> Nanopositioning Systems Market was valued at 88 million in 2024 and is projected to reach US$ 124 million by 2032, at a CAGR of 5.1% during the forecast period.

Which key companies operate in Global Nanopositioning Systems Market?

-> Key players include Physik Instrumente (PI) GmbH, Attocube, Prior Scientific (Queensgate), Piezosystem Jena GmbH, and Aerotech, among others.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor manufacturing, nanotechnology research funding, and demand for precision positioning in microscopy applications.

Which region dominates the market?

-> Asia-Pacific is the largest market with 42% share, driven by semiconductor manufacturing growth in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include integration with AI for adaptive positioning, multi-axis positioning systems, and miniaturization of nanopositioning components.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...