MARKET INSIGHTS

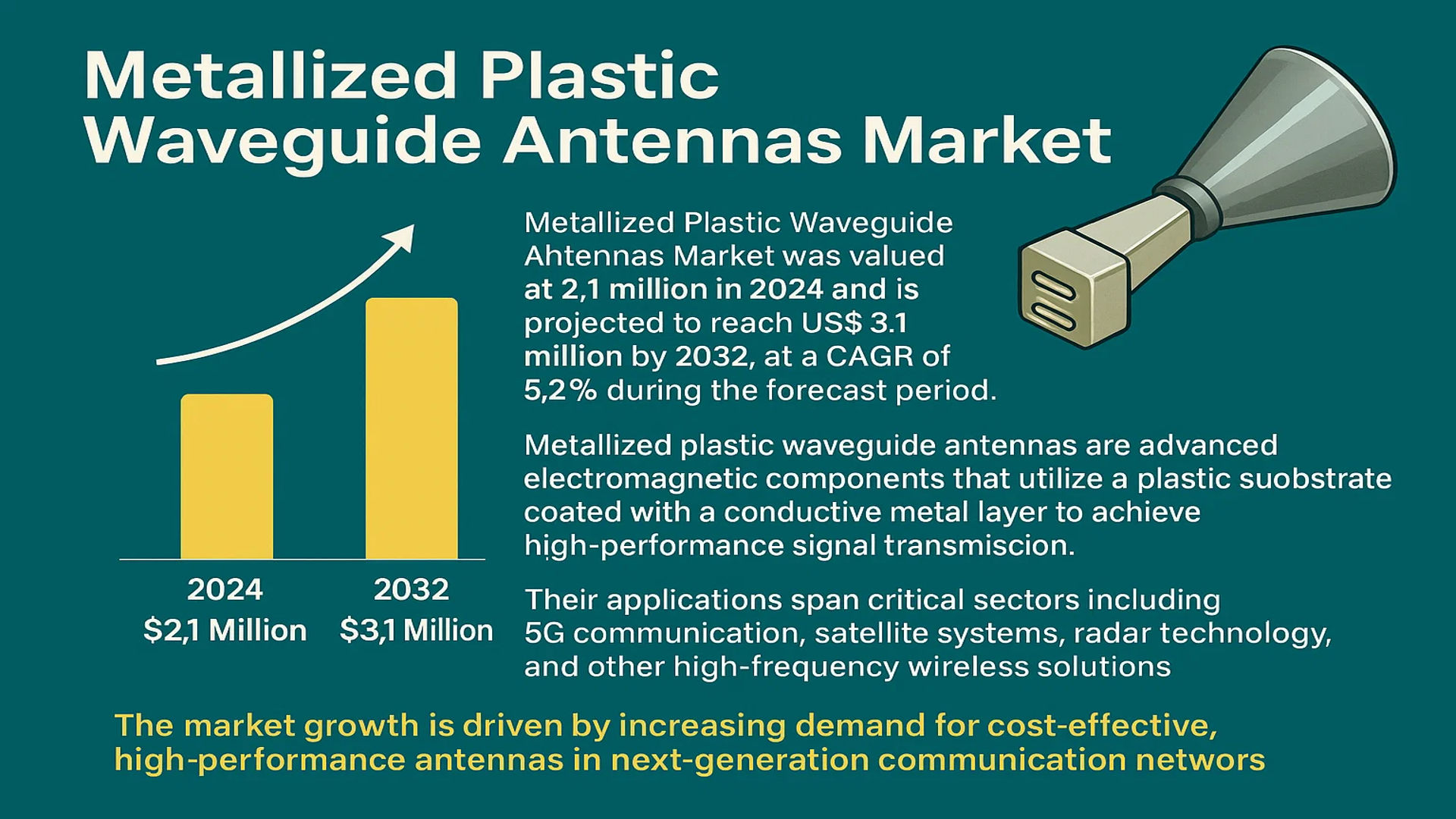

The global Metallized Plastic Waveguide Antennas Market was valued at 2.1 million in 2024 and is projected to reach US$ 3.1 million by 2032, at a CAGR of 5.2% during the forecast period.

Metallized plastic waveguide antennas are advanced electromagnetic components that utilize a plastic substrate coated with a conductive metal layer to achieve high-performance signal transmission. These antennas combine the lightweight and corrosion-resistant properties of polymers with the radiofrequency efficiency of metallization techniques such as Physical Vapor Deposition (PVD) and Chemical Plating. Their applications span critical sectors including 5G communication, satellite systems, radar technology, and other high-frequency wireless solutions.

The market growth is driven by increasing demand for cost-effective, high-performance antennas in next-generation communication networks. The U.S. holds a dominant share, while China is emerging as a key growth region. Leading manufacturers such as Huber+Suhner and Boxun Tech are investing in material innovations to enhance antenna efficiency, particularly for 5G infrastructure deployment. However, competition from traditional metal waveguide solutions poses a challenge, though the advantages of weight reduction and manufacturing scalability continue to bolster adoption.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for 5G Infrastructure Deployment Accelerates Market Growth

The global expansion of 5G networks is creating unprecedented demand for high-performance waveguide antennas. Metallized plastic waveguides offer significant advantages over traditional metal alternatives, including 40-60% weight reduction and 30-50% cost savings in manufacturing. These benefits are particularly crucial for 5G mmWave applications where thousands of small cells require lightweight, durable antenna solutions. With 5G subscriptions projected to exceed 3 billion globally by 2026, telecom operators are increasingly adopting metallized plastic waveguide antennas to meet the stringent performance and deployment requirements of next-generation networks.

Aerospace and Defense Modernization Programs Fuel Adoption

Modern military platforms demand lightweight radar and communication systems without compromising performance. Metallized plastic waveguide antennas are being increasingly specified for airborne and naval applications where their corrosion resistance and reduced weight-to-performance ratio provide strategic advantages. Recent defense budget increases, particularly in North America and Asia-Pacific regions, are accelerating the replacement of legacy systems with advanced radar architectures that incorporate these antennas. The growing adoption of phased array systems in modern fighter jets and naval vessels is particularly driving demand for conformal plastic waveguide solutions.

Automation in Manufacturing Processes Enhances Market Competitiveness

Advancements in physical vapor deposition (PVD) technologies have significantly improved the production efficiency of metallized plastic waveguides. Modern automated deposition systems can now achieve consistent coating thicknesses below 5 microns with defect rates under 0.5%, making plastic waveguides competitive with machined metal counterparts. These manufacturing improvements have reduced unit production costs by approximately 25% over the past three years while maintaining the required electrical performance characteristics. The resulting cost-performance benefits are expanding application opportunities across commercial satellite communications and industrial radar systems.

MARKET RESTRAINTS

Thermal Management Challenges Limit High-Power Applications

While metallized plastic waveguides offer numerous advantages, their adoption in high-power applications remains constrained by thermal limitations. Plastic substrates typically have thermal conductivity values below 0.5 W/mK compared to over 200 W/mK for aluminum waveguides. This makes them unsuitable for systems requiring continuous power handling above 500W without significant derating. The industry is actively developing advanced polymer composites and cooling solutions, but current technical constraints continue to restrict market penetration in certain radar and satellite uplink applications where metal waveguides remain dominant.

Standardization Gaps Create Integration Challenges

The lack of uniform industry standards for metallized plastic waveguide interfaces presents a significant adoption barrier. Many legacy systems were designed for conventional flange-mounted metal waveguides, requiring costly adapters or redesigns when implementing plastic alternatives. This compatibility issue is particularly acute in defense and aerospace sectors where system certification processes can add 12-18 months to transition timelines. While industry consortia are working to establish common interface specifications, the current fragmentation increases total cost of ownership and slows market adoption rates.

MARKET OPPORTUNITIES

Emerging Satellite Constellations Present High-Growth Potential

The rapid deployment of low Earth orbit (LEO) satellite networks creates substantial opportunities for lightweight antenna solutions. Metallized plastic waveguides are ideally suited for space applications where mass reduction directly translates to lower launch costs. With over 15,000 LEO satellites expected to be operational by 2028, antenna manufacturers are developing specialized plastic waveguide designs that can withstand the space environment while meeting stringent RF performance requirements. This emerging application segment could account for over 20% of the total market revenue by the end of the forecast period.

Advancements in Automotive Radar Open New Application Segments

The automotive industry’s transition to higher frequency radar systems (77-81 GHz) for autonomous driving features is creating demand for cost-effective waveguide solutions. Metallized plastic antennas enable the production of compact, integrated radar modules that meet automotive environmental requirements while achieving attractive price points for mass market vehicles. Several Tier 1 suppliers are currently qualifying plastic waveguide solutions that could reduce ADAS sensor costs by 15-25% compared to current technologies. This application sector is projected to grow at a CAGR exceeding 30% through 2032.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impact Material Availability

The specialty polymers used in high-frequency waveguide applications face periodic supply constraints due to limited global production capacity. Recent disruptions have caused lead times for certain engineered thermoplastics to extend beyond 6 months, creating production bottlenecks. Furthermore, the metallization process relies on scarce precious metals whose price volatility can erode cost advantages. Manufacturers are investing in alternative material formulations and localized supply chains, but these transitions require extensive requalification periods that temporarily constrain market responsiveness.

Technical Workforce Shortage Constrains Innovation Pace

The specialized nature of RF plastics engineering has created a talent gap that hinders product development cycles. Industry surveys indicate that over 60% of manufacturers report difficulties finding engineers with expertise in both polymer science and microwave engineering. This skills shortage is particularly acute for advanced simulation and testing roles required to develop next-generation designs. While academic partnerships are being established to address this challenge, the current talent deficit adds 6-9 months to typical development timelines for new waveguide products.

METALLIZED PLASTIC WAVEGUIDE ANTENNAS MARKET TRENDS

5G Deployment Accelerates Demand for Lightweight Antenna Solutions

The rapid global expansion of 5G networks is significantly boosting the adoption of metallized plastic waveguide antennas, valued for their high-frequency performance and cost efficiency. Traditional metal antennas struggle with weight and corrosion issues in outdoor deployments, whereas plastic alternatives with metallized coatings offer superior durability at reduced manufacturing costs. For mmWave applications in 5G, these antennas provide crucial advantages in signal integrity, with efficiency rates exceeding 90% in field tests. Furthermore, their modular design facilitates easier integration into compact base stations and small cells—key infrastructure for dense urban 5G coverage. The global market for these antennas in telecom applications is projected to grow at a CAGR of 6.8% through 2030.

Other Trends

Satellite Communication Modernization

Low-earth-orbit (LEO) satellite constellations are driving innovation in antenna design, where metallized plastics balance weight savings against radiation resistance—a critical factor for space applications. Recent advancements in physical vapor deposition (PVD) techniques have enabled thinner, more uniform metal coatings that maintain conductivity while withstanding thermal cycling in orbit. Companies like SpaceX and OneWeb are increasingly incorporating these antennas into next-generation satellite designs, with the segment expected to account for 22% of total market revenue by 2026. Concurrently, advancements in polymer composites have improved thermal stability, allowing operation across -40°C to +125°C ranges without performance degradation.

Defense Sector Prioritizes Stealth and Durability

Military applications are embracing metallized plastic antennas for their radar cross-section reduction capabilities and resilience in harsh environments. Unlike traditional metal arrays, these solutions enable tighter integration with composite radomes while maintaining RF transparency. Recent DoD contracts highlight a shift toward chemical plating processes for defense-grade antennas, as they provide better adhesion in extreme humidity and salt fog conditions. The U.S. and China dominate this segment, collectively representing 68% of defense-related antenna procurement in 2024. Emerging electronic warfare systems further leverage these antennas’ broadband characteristics, with some models now covering 2-40 GHz ranges in single-unit configurations.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership

The global metallized plastic waveguide antennas market features a competitive yet fragmented landscape, with established players and emerging companies vying for market share. Huber+Suhner, a Swiss-based multinational, dominates the sector due to its extensive expertise in radio frequency technology and strong global distribution network. The company has consistently invested in R&D to enhance antenna performance for 5G and satellite applications, reinforcing its market position.

Boxun Tech, a Chinese manufacturer, has rapidly gained traction by offering cost-effective solutions tailored for the Asia-Pacific region’s growing telecommunications infrastructure. Their competitive pricing strategy and localized production capabilities have enabled them to capture significant market share, particularly in emerging economies.

Meanwhile, North American and European manufacturers are focusing on high-precision antennas for defense and radar applications, where performance reliability outweighs cost considerations. This specialization allows them to maintain premium pricing and long-term contracts with government and aerospace clients.

Recent market developments show increasing vertical integration among key players. Several manufacturers have begun acquiring material suppliers to secure their polymer and metallization supply chains, mitigating raw material volatility risks. Furthermore, partnerships between antenna producers and 5G equipment vendors are becoming more common as the industry prepares for large-scale network deployments.

List of Key Metallized Plastic Waveguide Antenna Manufacturers

- Huber+Suhner (Switzerland)

- Boxun Tech (China)

- Radiometer Physics GmbH (Germany)

- Eravant (U.S.)

- Microwave Engineering Corporation (U.S.)

- SAGE Millimeter, Inc. (U.S.)

- QuinStar Technology, Inc. (U.S.)

- Mician GmbH (Germany)

- Farran Technology (Ireland)

Segment Analysis:

By Type

Physical Vapor Deposition Dominates the Market Due to High Precision and Durability

The market is segmented based on manufacturing process into:

- Physical Vapor Deposition (PVD)

- Chemical Plating

By Application

5G Communication Segment Leads Due to Expanding Global Network Infrastructure

The market is segmented based on application into:

- 5G Communication

- Satellite

- Radar

- Other Applications

By Frequency Range

Millimeter Wave Segment Gains Traction for High-Speed Data Transmission

The market is segmented based on frequency capabilities into:

- Sub-6 GHz

- Millimeter Wave (mmWave)

Regional Analysis: Metallized Plastic Waveguide Antennas Market

Asia-Pacific

The Asia-Pacific region dominates the global metallized plastic waveguide antennas market, driven by rapid 5G infrastructure deployment and satellite communication advancements. China leads with aggressive telecom expansion plans, allocating over $58 billion annually for 5G development, creating substantial demand for lightweight, corrosion-resistant antennas. India follows with increasing private sector participation in telecom and space sectors. Japan’s mature technology sector continues to innovate in precision waveguide designs, particularly for radar applications. The region benefits from cost-competitive manufacturing and strong supply chain integration, though intellectual property protection remains a concern in some emerging markets.

North America

North America represents the second-largest market, characterized by high-value applications in defense and aerospace sectors. The U.S. Department of Defense increasingly adopts metallized plastic antennas for their weight-saving advantages in unmanned systems – a market projected to exceed $14 billion by 2026. Commercial applications are growing through partnerships between telecom giants and antenna manufacturers to develop mmWave solutions for 5G networks. Strict quality standards and technical certifications create barriers for new entrants while ensuring premium product positioning for established players like Huber+Suhner.

Europe

European adoption focuses on sustainability and precision engineering, with German and French manufacturers leading in chemical plating processes that reduce environmental impact. The EU’s Horizon Europe program funds research into advanced dielectric materials for next-generation antennas. Automotive radar applications are expanding with increasing ADAS penetration rates exceeding 80% in new premium vehicles. However, the market faces challenges from component shortages and energy price volatility affecting polymer feedstock costs, prompting manufacturers to explore recycled material options without compromising RF performance.

Middle East & Africa

This emerging market shows growing potential in satellite communication as Gulf countries invest heavily in space programs. The UAE’s Hope Mars Mission and Saudi Arabia’s space agency development create specialized demand for space-qualified antennas. Terrestrial applications remain limited by infrastructure gaps, though undersea communication projects along Africa’s coasts present future opportunities. Market growth is tempered by reliance on imports and limited local technical expertise, driving partnerships between regional telecom operators and global antenna suppliers.

South America

South America’s market development remains uneven, with Brazil accounting for over 60% of regional demand through its aerospace and defense sectors. Argentina shows promise in satellite ground station applications. Economic instability and currency fluctuations discourage long-term investments in antenna manufacturing, leading to predominant reliance on imports. However, increasing rural connectivity initiatives and mining sector automation projects are creating niches for durable, weather-resistant waveguide solutions suitable for harsh environments.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Metallized Plastic Waveguide Antennas markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 2.1 million in 2024 and is projected to reach USD 3.1 million by 2032, growing at a CAGR of 5.2%.

- Segmentation Analysis: Detailed breakdown by type (Physical Vapor Deposition, Chemical Plating) and application (5G Communication, Satellite, Radar, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including Huber+Suhner and Boxun Tech, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging manufacturing processes and material advancements in waveguide antenna technology.

- Market Drivers & Restraints: Evaluation of factors driving adoption in 5G infrastructure and satellite communications, along with material cost challenges.

- Stakeholder Analysis: Strategic insights for antenna manufacturers, telecom equipment providers, and defense contractors regarding market opportunities.

The research employs both primary and secondary methodologies, including interviews with industry experts and analysis of verified market data to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Metallized Plastic Waveguide Antennas Market?

-> Metallized Plastic Waveguide Antennas Market was valued at 2.1 million in 2024 and is projected to reach US$ 3.1 million by 2032, at a CAGR of 5.2% during the forecast period.

Which key companies operate in this market?

-> Key players include Huber+Suhner and Boxun Tech, which collectively held a significant market share in 2024.

What are the key growth drivers?

-> Growth is driven by 5G network expansion, increasing satellite communications, and demand for lightweight antenna solutions in aerospace and defense applications.

Which region dominates the market?

-> Asia-Pacific is emerging as a high-growth region, while North America currently leads in technological adoption.

What are the emerging trends?

-> Emerging trends include advanced metallization techniques, integration with IoT devices, and development of cost-effective manufacturing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...