Low-Power Processor Market Insights

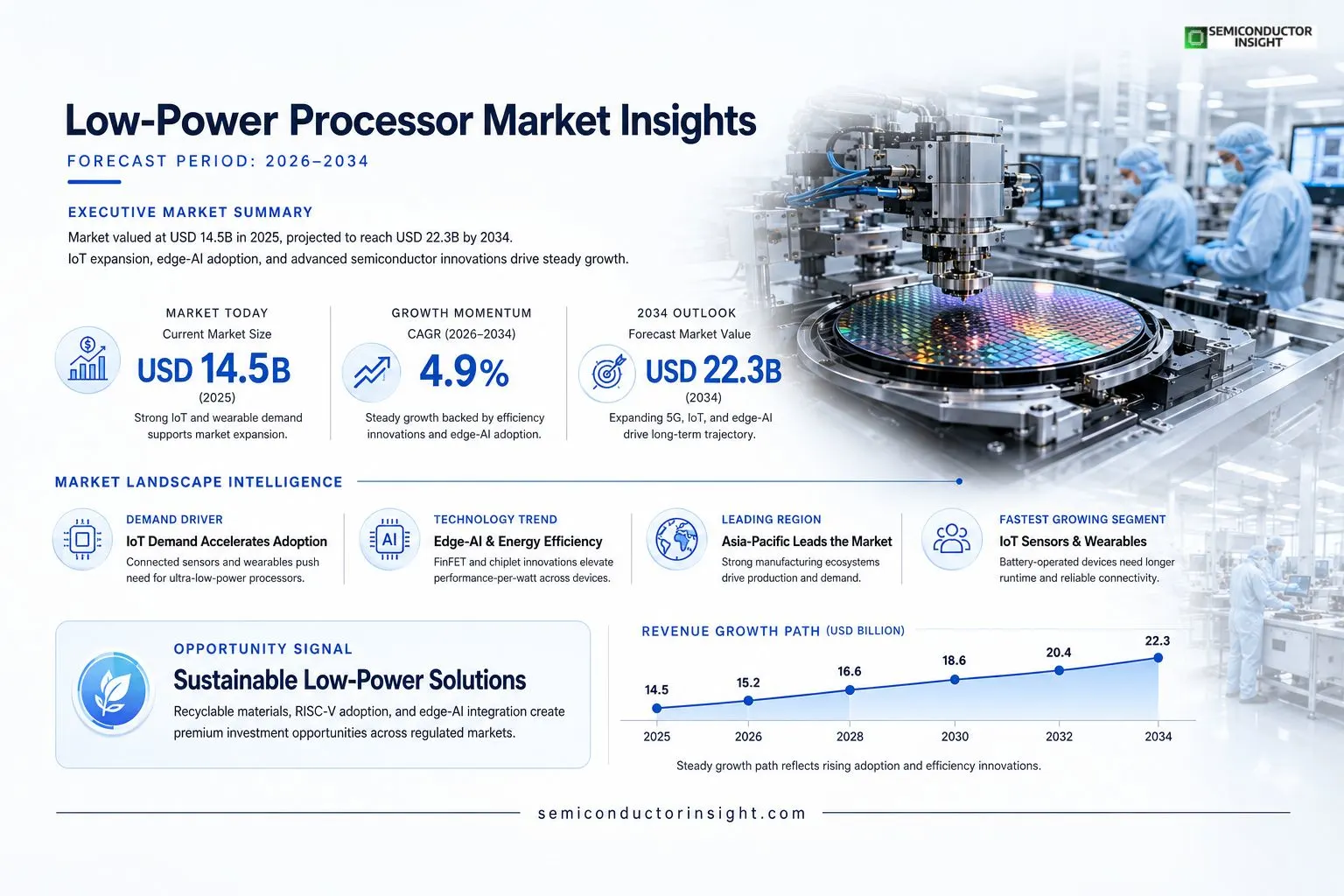

Low-Power Processor Market size was valued at USD 14.5 billion in 2025. The market is projected to grow from USD 15.2 billion in 2026 to USD 22.3 billion by 2034, exhibiting a CAGR of approximately 4.9% during the forecast period.

Low-Power Processors are energy‑efficient computing units designed for battery‑operated and embedded applications, enabling extended runtime while delivering adequate performance for tasks such as IoT connectivity, wearable devices, and edge‑AI inference. These processors typically incorporate architectures like ARM Cortex‑M series, RISC‑V cores optimized for minimal power draw, and specialized ASICs that balance computational capability with stringent power budgets.The market is experiencing rapid growth due to several factors, including rising adoption of Internet of Things (IoT) solutions, increasing demand for wearable technology, and heightened focus on sustainability which drives manufacturers toward energy‑efficient designs. Furthermore, advancements in semiconductor fabrication technologies such as FinFET and emerging chiplet integration are enhancing performance‑per‑watt ratios. Initiatives by key players,including Arm Ltd., Qualcomm Technologies Inc., NXP Semiconductors, Texas Instruments Inc., and MediaTek Inc.,are expected to further accelerate market expansion through new product launches and strategic partnerships.

MARKET DRIVERS

Rising Demand for Energy‑Efficient IoT Devices

The proliferation of connected sensors in smart homes, wearables, and industrial telemetry is pushing manufacturers to adopt ultra‑low‑power silicon. Design engineers prioritize processors that can operate for years on a single battery, which directly fuels growth in Low‑Power Processor Market.

Expansion of Edge Computing and AI Workloads

Edge servers and AI inference nodes require high‑performance cores that consume minimal energy to reduce cooling costs and extend deployment life. The convergence of AI acceleration and power‑saving architectures is a core catalyst for market expansion.

➤ “Power efficiency has become a decisive factor in processor selection, eclipsing raw clock speed for most emerging applications.”

Regulatory pressure for reduced carbon footprints in data centers further encourages adoption of low‑power designs, positioning Low‑Power Processor Market for sustained upward momentum.

MARKET CHALLENGES

Thermal Management and Performance Trade‑offs

Designers must balance heat dissipation with computational throughput. In constrained form factors, limited cooling solutions can restrict clock speeds, making it challenging to meet demanding AI or signal‑processing workloads without exceeding thermal budgets.

Other Challenges

Supply‑Chain Volatility

shortages of advanced semiconductor substrates and packaging materials increase lead times, potentially delaying product launches and inflating costs for low‑power solutions.

MARKET RESTRAINTS

High Development Costs for Custom ASICs

Creating application‑specific low‑power processors involves substantial R&D investment and mask set expenses. Smaller OEMs may lack the capital to pursue bespoke silicon, limiting market penetration to larger players with deep pockets.

MARKET OPPORTUNITIES

Emerging 5G Infrastructure and Edge AI

The rollout of 5G networks demands distributed processing at cell sites and edge nodes, where power availability is limited. This creates a significant growth avenue for low‑power processors optimized for real‑time analytics, positioning the market for a robust expansion over the next five years.

Low-Power Processor Market Trends

Energy‑Efficient Architectures Accelerate Adoption

Low-Power Processor Market is increasingly shaped by architectures that prioritize performance‑per‑watt. Designs such as the ARM Cortex‑M series and RISC‑V cores optimized for minimal voltage draw are becoming standard in battery‑operated devices. By integrating specialized ASIC blocks that handle sensor fusion, secure boot, or low‑latency edge‑AI inference, manufacturers achieve longer runtimes while maintaining sufficient compute capability for IoT connectivity, wearable health monitoring, and distributed analytics. Tight coupling of power‑gating techniques with dynamic frequency scaling further reduces idle power, enabling devices to stay active for months on a single charge. These technical advances also simplify thermal management, allowing compact form factors in wearables and industrial sensors.

Other Trends

Key Enablers

Low-Power Processor Market benefits from the continued expansion of Internet of Things deployments, where devices must operate unattended for years under strict power budgets. Wearable technology, especially health‑focused gadgets, demands ultra‑low consumption to meet consumer expectations for seamless daily wear. Sustainability programs in major OEMs prioritize components that lower overall energy use, directly influencing design choices. Advances in semiconductor processes, notably FinFET scaling and emerging chiplet integration, improve the power‑efficiency envelope, allowing higher functionality without proportional increases in draw. Chiplet‑based approaches also enable modular customization, letting designers combine a low‑power core with dedicated accelerators for machine‑learning inference. In parallel, industry standards for energy‑aware communication protocols, such as Bluetooth Low Energy 5.2, reinforce the need for processors that can quickly transition between sleep and active states.

Competitive Landscape and Innovation

Players in Low-Power Processor Market are aligning product roadmaps with ecosystem development to sustain growth. Arm Ltd., Qualcomm Technologies, NXP Semiconductors, Texas Instruments, and MediaTek are delivering expanded families that integrate built‑in voltage regulators, advanced wake‑up controllers, and machine‑learning micro‑kernels. Collaborative programs emphasize software‑defined power management, where runtime APIs allow applications to request precise performance levels, minimizing unnecessary energy expenditure. Strategic alliances with board‑level manufacturers produce reference design kits that accelerate OEM integration, reducing time‑to‑market for new smart sensors and edge‑AI nodes. In addition, joint ventures focused on open‑source development tools foster a broader developer base, ensuring that low‑power designs remain compatible with emerging AI frameworks. Regulatory trends toward lower carbon footprints are also prompting manufacturers to certify their low‑power silicon under emerging green‑chip programs, further reinforcing market adoption across multiple regions worldwide and driving.

COMPETITIVE LANDSCAPEKey Industry Players

Low-Power Processor Market – Competitive Overview

Low‑Power Processor Market is anchored by a handful of tier‑1 semiconductor firms that dominate design IP, fabrication partnerships, and ecosystem enablement. Arm Ltd. remains the de‑facto standard‑setter with its Cortex‑M and Cortex‑A families, which are licensed to virtually every major fab and OEM, giving it a market share advantage that shapes pricing and roadmap dynamics. Qualcomm Technologies leverages its Snapdragon series to blend connectivity and power efficiency for mobile and IoT devices, while Texas Instruments capitalizes on its analog‑centric portfolio to embed ultra‑low‑power cores in sensor‑rich edge nodes. MediaTek’s aggressive cost‑competitiveness and broad SoC integration further intensify competitive pressure, especially in emerging Asian markets. Collectively, these leaders drive the bulk of revenue growth, set performance‑per‑watt benchmarks, and dictate the direction of advanced process nodes such as 7 nm FinFET and upcoming chiplet architectures.Beyond the headline players, a diversified set of niche specialists fuels innovation in specific verticals. NXP Semiconductors and STMicroelectronics focus on automotive and industrial safety‑critical applications, delivering hardened low‑power cores that meet stringent functional‑safety standards. Renesas Electronics and Microchip Technology target the embedded control market with RISC‑V and proprietary architectures optimized for battery‑operated wearables. Smaller but strategically important firms such as Cypress Semiconductor (now part of Infineon) and Analog Devices provide mixed‑signal and sensor‑fusion capabilities that complement core processors. Samsung Electronics and Intel Corporation are expanding their integrated foundry services to capture design‑win opportunities, while Apple’s in‑house silicon demonstrates the premium segment’s appetite for ultra‑efficient custom CPUs. This layered ecosystem ensures robust competition across performance, power, and price dimensions.

List of Key Low-Power Processor Companies Profiled

- Arm Ltd.

- Qualcomm Technologies Inc.

- NXP Semiconductors

- Texas Instruments Inc.

- MediaTek Inc.

- Samsung Electronics

- Intel Corporation

- STMicroelectronics

- Renesas Electronics

- Microchip Technology

- Analog Devices Inc.

- Broadcom Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ARM Cortex‑M based processors

|

| By Application |

|

IoT sensors and gateways

|

| By End User |

|

Consumer electronics manufacturers

|

| By Architecture |

|

Harvard low‑power architecture

|

| By Target Device |

|

Battery‑powered wearables

|

Regional Analysis: North America

United States

The expansion of the Internet of Things is a primary driver for low-power processors in the US, with devices ranging from smart home appliances to industrial sensors demanding energy-efficient computing.

The burgeoning wearable technology market, encompassing smartwatches and fitness trackers, heavily relies on low-power processors to extend battery life and enhance user experience.

The increasing adoption of edge computing in various sectors, including manufacturing and healthcare, necessitates low-power processors capable of processing data closer to the source.

The automotive industry’s shift towards electric vehicles and advanced driver-assistance systems (ADAS) fuels the demand for specialized low-power processors for vehicle control and infotainment.

North America

North America is a key market for Low-Power Processor Market, with substantial investments in research and development driving innovation in this sector. The region’s strong technological infrastructure and high adoption rates of connected devices contribute to a consistent demand for energy-efficient computing solutions. Several factors are shaping the market dynamics, including the growing emphasis on sustainability, the expanding IoT ecosystem, and the increasing adoption of edge computing technologies. Business strategies in North America often involve collaborations between processor manufacturers and device makers, as well as strategic partnerships with software developers to optimize performance and power consumption. The competitive landscape is characterized by a mix of large multinational corporations and smaller, specialized players, each striving to deliver innovative low-power solutions. The market is expected to witness continued growth in the coming years, driven by the expansion of various end-use industries and the increasing demand for energy-efficient devices.

Europe

Europe represents a significant and mature market within Low-Power Processor Market. The region’s strong focus on energy efficiency and data privacy regulations influences the demand for low-power computing solutions across various sectors. Key trends in Europe include a growing adoption of IoT in industrial automation, the rise of wearable health devices, and increasing investments in AI and machine learning at the edge. Business strategies in Europe often emphasize compliance with stringent data protection laws, fostering collaborations within the European Union, and promoting sustainable manufacturing practices. The competitive landscape is shaped by a combination of established European semiconductor companies and players, all vying for market share with innovative low-power processor designs. The market is predicted to continue its growth trajectory, driven by the expansion of its industrial sector and increasing consumer demand for connected devices.

Asia-Pacific

Asia-Pacific is the fastest-growing region in Low-Power Processor Market, driven by rapid industrialization and a burgeoning consumer electronics sector. Countries like China, India, and Japan are experiencing exponential growth in demand for low-power processors across various applications, including smartphones, wearables, and IoT devices. Key trends in the region include the increasing adoption of 5G technology, the expansion of smart manufacturing initiatives, and the growing demand for AI-powered solutions. Business strategies in Asia-Pacific often involve local partnerships, cost-effective manufacturing, and a focus on catering to the specific needs of the regional market. The competitive landscape is characterized by a large number of domestic and international players, creating intense competition and driving innovation. The market is poised for continued strong growth, fueled by the region’s robust economic expansion and rising disposable incomes.

South America

South America presents a promising, albeit developing, market for Low-Power Processor Market. Growing urbanization, increasing smartphone penetration, and the expanding industrial sector are driving demand for energy-efficient computing solutions. Key trends include the growth of IoT in agriculture, the increasing adoption of wearables for health monitoring, and the development of smart city initiatives. Business strategies in South America often focus on offering cost-effective solutions and building strong relationships with local distributors and partners. The competitive landscape is relatively fragmented, with a mix of and regional players. While the market is still in its early stages of development, it is expected to witness significant growth in the coming years, driven by economic expansion and increasing digital adoption.

Middle East & Africa

The Middle East & Africa region is an emerging market for Low-Power Processor Market, with increasing investments in infrastructure development and technological advancements. The growing adoption of IoT in smart cities, the expansion of the industrial sector, and the rising demand for consumer electronics are driving demand for energy-efficient computing solutions. Key trends include the development of smart infrastructure projects, the growth of e-commerce, and the increasing adoption of AI-powered solutions. Business strategies in the region often involve strategic alliances with local partners, focus on offering tailored solutions, and addressing the specific needs of the regional market. The competitive landscape is relatively nascent but expected to intensify as the market matures. The region is projected to experience considerable growth in the future, driven by its ongoing economic diversification and technological advancements.

Report Scope

This market research report provides a comprehensive analysis of the Low-Power Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Low-Power Processor Market?

-> Low-Power Processor Market was valued at USD 14.5 billion in 2025 and is expected to reach USD 22.3 billion by 2034, exhibiting a CAGR of approximately 4.9%.

Which key companies operate in Low-Power Processor Market?

-> Key players include Arm Ltd., Qualcomm Technologies Inc., NXP Semiconductors, Texas Instruments Inc., and MediaTek Inc.

What are the key growth drivers?

-> Key growth drivers include rising adoption of IoT solutions, increasing demand for wearable devices, sustainability focus driving energy‑efficient designs, and advancements in FinFET and chiplet integration technologies.

Which region dominates the market?

-> Asia‑Pacific leads Low-Power Processor Market due to strong semiconductor manufacturing presence and robust demand from consumer electronics and automotive sectors, while North America remains a significant contributor.

What are the emerging trends?

-> Emerging trends include integration of edge‑AI capabilities, adoption of RISC‑V open‑source cores, development of ultra‑low‑power ASICs, and increased use of chiplet‑based architectures for modular power‑efficient designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...