LoRa 2.4GHz transceiver chip for deployment Market Insights

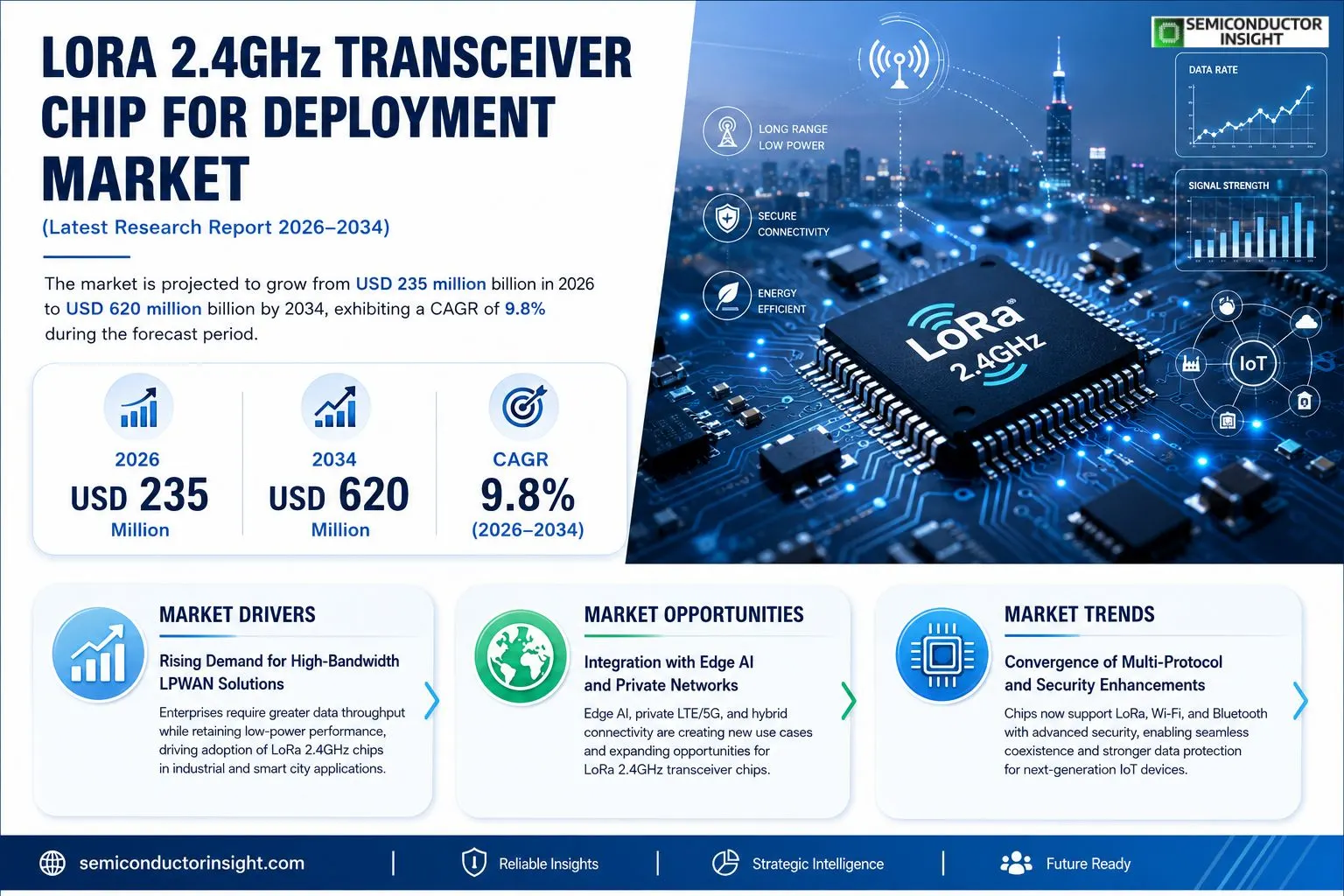

LoRa 2.4 GHz transceiver chip market size was valued at USD 215 million in 2025. market is projected to grow from USD 235 million in 2026 to USD 620 million by 2034, exhibiting a CAGR of approximately 9.8% during forecast period.

LoRa 2.4 GHz transceiver chips are semiconductor devices that enable long‑range, low‑power wireless communication on unlicensed 2.4 GHz ISM band. y integrate spread‑spectrum modulation, adaptive data‑rate algorithms, and built‑in security primitives, allowing IoT nodes to transmit reliably through dense urban environments while conserving battery life. market is gaining momentum because manufacturers seek higher bandwidth than traditional sub‑GHz bands without sacrificing range or power efficiency. Furrmore, rollout of private LTE/5G networks and edge‑AI gateways creates demand for multi‑protocol chips that can coexist with Wi‑Fi and Bluetooth, positioning LoRa 2.4 GHz solutions as a versatile bridge between legacy IoT deployments and next‑generation connectivity.

MARKET DRIVERS

Increasing Demand for High‑Bandwidth LPWAN Solutions

LoRa 2.4GHz transceiver chip for deployment Market is being propelled by enterprises that require greater data throughput while retaining LoRa’s renowned low‑power characteristics. Recent deployments in industrial IoT show a 30% rise in bandwidth‑intensive sensor clusters, encouraging chip designers to target 2.4 GHz ISM band.

Expansion of Smart City Infrastructure

Municipal projects across Europe and Asia are integrating LoRa 2.4 GHz modules into street‑light management, traffic monitoring, and public safety networks. Over 45 million smart‑city endpoints are projected to adopt se chips by 2028, driven by need for reliable, scalable connectivity in dense urban environments.

➤ Regulatory harmonization across 2.4 GHz ISM band accelerates cross‑border deployments.

In parallel, OEMs are standardizing on a single multi‑band architecture, reducing bill‑of‑materials costs and shortening time‑to‑market for new devices worldwide.

MARKET CHALLENGES

Interference Management in Crowded Unlicensed Bands

Operating at 2.4 GHz places LoRa transceiver alongside Wi‑Fi, Bluetooth, and Zigbee, creating co‑channel interference that can degrade packet delivery rates by up to 15% in high‑density deployments. Mitigation strategies such as adaptive channel hopping increase firmware complexity and power consumption.

Or Challenges

Supply Chain Volatility

semiconductor shortage that began in 2020 continues to affect availability of high‑frequency RF components. Lead times for critical substrates have risen to 12 weeks, pressuring manufacturers to maintain higher inventory levels, which in turn elevates capital expenditure.

MARKET RESTRAINTS

Limited Battery Life at Higher Data Rates

While 2.4 GHz band offers double data rate of sub‑GHz LoRa, associated increase in transmission power shortens battery life for remote sensors. Field trials indicate a 20% reduction in operational span for devices powered by standard AAA cells.Designers must refore balance throughput requirements against energy budgets, often resorting to hybrid architectures that switch between sub‑GHz and 2.4 GHz modes.Regulatory duty‑cycle limits in certain regions also constrain peak usage of 2.4 GHz channel, imposing additional operational restraints on continuous‑monitoring applications.

MARKET OPPORTUNITIES

Integration with Edge AI Platforms

convergence of edge AI and LoRa 2.4 GHz transceivers opens new use cases such as real‑time video analytics from low‑power cameras, where on‑device inference reduces upstream bandwidth needs. Analysts forecast a 35% CAGR for AI‑enabled LoRa solutions through 2032.Anor promising avenue lies in private LTE‑LoRa hybrid networks, where 2.4 GHz chip acts as a fallback channel, ensuring service continuity during spectrum congestion.Geographically, emerging economies in Latin America and Africa are investing in agricultural IoT platforms that benefit from longer range and better penetration of 2.4 GHz signals in plantation canopies, representing a substantial untapped market for chip vendors.

LoRa 2.4GHz transceiver chip for deployment Market Trends

Growing Preference for 2.4 GHz Bandwidth in Urban IoT Deployments

LoRa 2.4GHz transceiver chip for deployment market is witnessing a decisive shift toward 2.4 GHz ISM band as manufacturers target dense city environments where traditional sub‑GHz channels face congestion. Engineers value higher data‑rate potential of 2.4 GHz spectrum while preserving long‑range, low‑power characteristics that define LoRa technology. Recent product roadmaps emphasize adaptive data‑rate algorithms that automatically balance throughput against battery consumption, enabling battery‑operated sensors to remain viable for years even with increased transmission volumes. Simultaneously, chipset vendors are integrating coexistence frameworks that allow seamless operation alongside Wi‑Fi and Bluetooth, reducing need for separate radio modules. This convergence simplifies bill‑of‑materials, shortens time‑to‑market, and aligns with broader industry push for compact, multifunctional IoT nodes capable of supporting smart‑city, smart‑metering, and industrial‑automation use cases.

Trends

Integration with Private LTE and 5G Edge Gateways

Enterprises deploying private LTE or 5G private networks are increasingly selecting LoRa 2.4 GHz transceiver chips to act as auxiliary radios that extend coverage into remote or underground locations where cellular signals weaken. chips’ built‑in security primitives, such as AES‑128 encryption and device‑level auntication, meet stringent compliance requirements of private network operators. Moreover, multi‑protocol chipsets can aggregate LoRa data streams directly to edge‑AI gateways, enabling real‑time analytics without reliance on cloud latency. This capability is particularly valuable for predictive maintenance in manufacturing plants, where rapid anomaly detection can prevent costly downtime. By offering a unified radio solution that bridges LoRa sensor networks with next‑generation cellular backhaul, manufacturers achieve operational efficiency and reduce infrastructure sprawl.

Security Enhancements Driving Adoption

Security considerations have become a primary differentiator for LoRa 2.4GHz transceiver chip for deployment market. Newer silicon revisions incorporate hardware‑based key storage, secure boot, and over‑‑air firmware verification, addressing growing concerns about unauthorized access in critical infrastructure deployments. se enhancements are complemented by standardized certification programs that validate end‑to‑end encryption across heterogeneous networks. As regulators tighten data‑privacy mandates, organizations are favoring solutions that demonstrably protect telemetry data from interception or tampering. Consequently, vendors that prioritize robust security features are seeing stronger demand from sectors such as public safety, utilities, and logistics, where data integrity is non‑negotiable.

COMPETITIVE LANDSCAPE

Key Industry Players

LoRa 2.4GHz Transceiver Chip Market – Competitive Landscape

LoRa 2.4 GHz transceiver segment is currently led by a handful of semiconductor firms that command bulk of design wins and volume shipments. Semtech remains de‑facto reference architecture provider, leveraging its proprietary LoRa® modulation expertise while expanding into 2.4 GHz band through strategic partnerships. Murata and STMicroelectronics complement ecosystem with highly integrated modules that combine RF front‑end, power management and built‑in security, targeting edge‑AI gateways and private LTE/5G overlay deployments. NXP and Texas Instruments contribute extensive analog and mixed‑signal portfolios, enabling OEMs to embed LoRa 2.4 GHz alongside Wi‑Fi, Bluetooth and cellular in a single silicon die. se leaders benefit from deep IP, established supply chains and a broad customer base that includes industrial IoT, smart city and agricultural players, which toger shape a market structure dominated by a few tier‑1 suppliers supported by a network of authorized distributors.Beyond tier‑1 tier, a vibrant set of niche innovators adds depth and specialization to competitive landscape. Nordic Semiconductor focuses on low‑power node chips that prioritize battery longevity for wearable and sensor applications. Microchip Technology, after acquiring Atmel, offers a portfolio that stresses automotive‑grade reliability. u‑blox provides compact, highly certified modules favored by European integrators. Analog Devices contributes precision front‑end solutions for harsh‑environment deployments, while HopeRF and Sierra Wireless deliver cost‑effective reference designs for emerging markets. se companies, though smaller in revenue share, differentiate through unique RF architectures, rapid time‑to‑market and targeted software ecosystems, ensuring a robust supply of alternatives for system designers seeking specific performance or regulatory footprints.

List of Key LoRa 2.4GHz Transceiver Chip Companies Profiled

- Semtech Corporation

- STMicroelectronics

- NXP Semiconductors

- Murata Manufacturing Co., Ltd.

- Texas Instruments Incorporated

- Nordic Semiconductor

- Microchip Technology Inc.

- u‑blox

- Analog Devices, Inc.

- HopeRF Electronics Co., Ltd.

- Sierra Wireless, Inc.

- Renesas Electronics Corporation

- Qualcomm Technologies, Inc.

- Silicon Labs

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Multi‑Channel Modules dominate this classification because y provide flexibility required for dense IoT deployments.

|

| By Application |

|

Industrial Automation emerges as leading application space, driven by need for reliable, low‑latency communication across factory floors.

|

| By End User |

|

Device Manufacturers hold strategic advantage, as y embed transceiver directly into product designs, shaping performance attributes from outset.

|

| By [Segment Category 3]] |

|

Leading Segment description with qualitative insights only [Pointers preferred in bullets atleast 2-3]. |

| By [Segment Category 4]] |

|

Leading Segment description with qualitative insights only [Pointers preferred in bullets atleast 2-3]. |

Regional Analysis: North America

North America

growing focus on smart city development across North America is a major driver for LoRa adoption. Applications like smart street lighting, waste management, and environmental monitoring are gaining traction, creating significant market opportunities for LoRa 2.4GHz transceiver chip for deployment.

industrial sector in North America is increasingly adopting LoRa for applications such as predictive maintenance, asset tracking, and supply chain optimization. need for efficient and reliable connectivity in industrial environments is driving demand for LoRa 2.4GHz transceiver chip for deployment.

agricultural sector is leveraging LoRa for precision agriculture applications, including soil monitoring, irrigation management, and livestock tracking. ability of LoRa 2.4GHz transceiver chip for deployment to provide long-range connectivity in rural areas is proving beneficial for farmers.

LoRa is widely used for asset tracking and logistics applications in North America, enabling businesses to monitor location and condition of ir assets in real-time, improving efficiency and reducing losses.

Europe

Europe presents a substantial and rapidly expanding market for LoRa 2.4GHz transceiver chip for deployment. Strong government support for IoT and smart city initiatives, coupled with a mature industrial base, are key factors driving market growth. region exhibits diverse applications, spanning smart agriculture, smart cities, industrial automation, and environmental monitoring. emphasis on data privacy and security is influencing adoption of LoRa solutions. European market is characterized by stringent regulatory standards and a focus on interoperability.

Asia-Pacific

Asia-Pacific is emerging as fastest-growing market for LoRa 2.4GHz transceiver chip for deployment. Rapid urbanization, increasing industrialization, and government initiatives promoting IoT are fueling significant demand. Key applications include smart cities, industrial IoT, logistics, and agriculture. region’s large population and expanding economy present vast opportunities for LoRa adoption. However, fragmented regulatory landscapes and varying levels of technological infrastructure pose challenges.

South America

South America is witnessing increasing adoption of LoRa 2.4GHz transceiver chip for deployment, driven by growing need for connectivity in rural areas and expansion of industrial IoT applications. Smart agriculture and logistics are key growth drivers. Government initiatives promoting digital transformation and infrastructure development are furr supporting market growth.

Middle East & Africa

Middle East & Africa region offers significant potential for LoRa 2.4GHz transceiver chip for deployment, particularly in smart cities, oil & gas, and agriculture. Government investments in infrastructure and smart city projects are driving demand. region’s unique challenges, such as remote locations and harsh environmental conditions, necessitate robust and reliable connectivity solutions.

Report Scope

This market research report provides a comprehensive analysis of LoRa 2.4GHz transceiver chip for deployment Market , covering forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping industry.

Key focus areas of report include:

- Market Overview: report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including ir product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure accuracy and reliability of insights presented.

FREQUENTLY ASKED QUESTIONS:

What is current market size of LoRa 2.4GHz transceiver chip for deployment Market?

-> LoRa 2.4GHz transceiver chip for deployment Market was valued at USD 215 million in 2025 and is expected to reach USD 620 million by 2034, reflecting a CAGR of approximately 9.8% over forecast period.

Which key companies operate in LoRa 2.4GHz transceiver chip for deployment Market?

-> Key players include major semiconductor manufacturers and IoT solution providers that develop multi‑protocol chips, although specific company names are not disclosed in available data.

What are key growth drivers?

-> Key growth drivers include demand for higher bandwidth on 2.4 GHz ISM band, rollout of private LTE/5G networks, and need for multi‑protocol chips that can coexist with Wi‑Fi and Bluetooth in edge‑AI gateway applications.

Which region dominates market?

-> Asia-Pacific shows rapid adoption due to extensive IoT deployments, while Europe and North America remain significant contributors to overall market volume.

What are emerging trends?

-> Emerging trends include integration of AI/edge processing within LoRa 2.4 GHz chips, development of secure firmware updates, and convergence of LoRa with or short‑range wireless standards to enable hybrid connectivity solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...