Iterative learning control for industrial robotic 3D printing path Market Insights

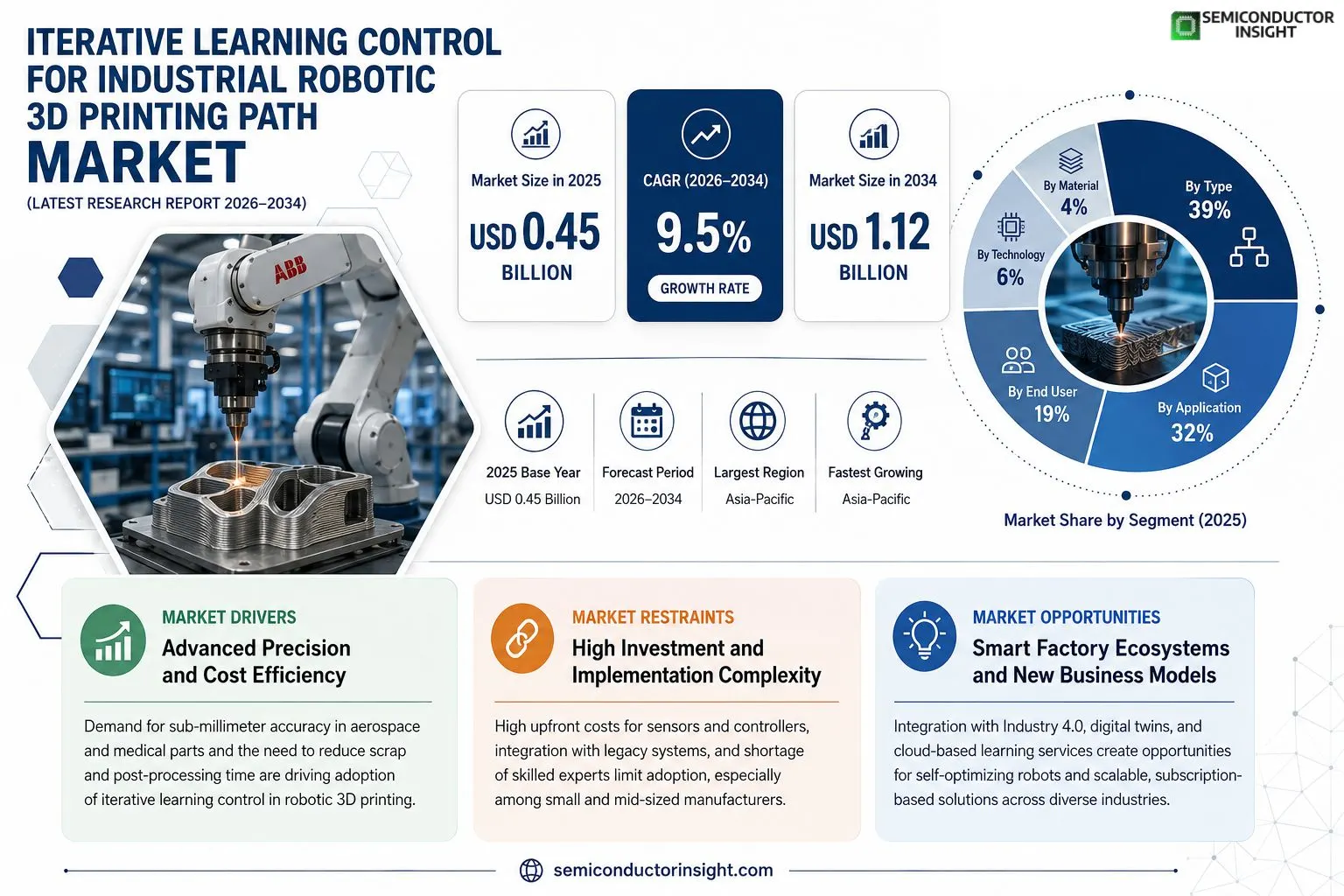

Iterative learning control for industrial robotic 3D printing path market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.48 billion in 2025 to USD 1.12 billion by 2034, exhibiting a CAGR of 9.5% during the forecast period.

Iterative learning control (ILC) is an advanced adaptive algorithm that refines robot motion trajectories through repeated execution cycles, minimizing error accumulation on complex additive‑manufacturing paths. In industrial robotic 3D printing, ILC synchronizes nozzle deposition speed with dynamic tool‑path adjustments, ensuring layer‑by‑layer dimensional accuracy and material consistency.The market is accelerating because manufacturers are embracing Industry 4.0 standards, seeking higher throughput and tighter tolerances in metal and polymer additive processes. Furthermore, rising investment in smart factories and collaborations among leading robotics firmssuch as ABB’s integration of ILC modules into its collaborative armsare expanding adoption across aerospace, automotive, and medical device sectors.

MARKET DRIVERS

Advanced Precision Requirements

The rise of high‑value aerospace and medical components demands sub‑millimeter accuracy in additive manufacturing. Iterative learning control for industrial robotic 3D printing path Market enables robots to refine trajectories after each layer, dramatically reducing dimensional errors and waste.

Cost Efficiency Through Automation

Manufacturers are adopting closed‑loop learning algorithms to cut post‑processing time. By automatically compensating for thermal distortion, firms report up to a 20% reduction in material scrap, strengthening the economic case for deploying iterative learning solutions.

➤ “Continuous improvement of robot paths drives both quality and profitability, positioning the technology as a core enabler for next‑generation additive factories.”

Industry surveys indicate that firms integrating learning‑based control systems are accelerating product rollout cycles, giving them a competitive edge in fast‑moving markets.

MARKET CHALLENGES

Integration Complexity

Deploying iterative learning algorithms requires seamless communication between CAD/CAM software, robot controllers, and sensor suites. Many OEMs face steep learning curves, and legacy equipment often lacks the interfaces needed for real‑time data exchange.

Other Challenges

Skilled Workforce Shortage

The specialized knowledge needed to configure, tune, and maintain learning‑based control loops is scarce, leading to higher personnel costs and longer implementation timelines.Additionally, establishing robust validation protocols for adaptive path adjustments adds regulatory overhead for sectors such as aerospace and medical devices.

MARKET RESTRAINTS

High Initial Investment

The upfront cost of retrofitting existing robotic cells with high‑resolution encoders, force sensors, and dedicated learning controllers can be prohibitive for small‑to‑mid‑size manufacturers, slowing broader adoption.Furthermore, uncertainty around return on investment timelines makes capital allocation decisions more cautious, especially in industries with tight margin pressures.

MARKET OPPORTUNITIES

Emerging Applications in Smart Factories

As Industry 4.0 platforms mature, there is a growing demand for self‑optimizing robotic printers that can respond to real‑time production data. Iterative learning control aligns perfectly with predictive maintenance and digital twin ecosystems, opening new revenue streams.Cloud‑based learning services also present a scalable business model, allowing manufacturers to subscribe to continuous algorithm updates without heavy on‑premise investments.

Iterative learning control for industrial robotic 3D printing path Market Trends

Adoption of Adaptive Algorithms in Additive Manufacturing

Manufacturers are increasingly deploying Iterative learning control to refine robot motion trajectories in complex 3D printing processes. The algorithm learns from each deposition cycle, reducing cumulative error and improving dimensional consistency across metal and polymer layers. As factories move toward Industry 4.0 standards, the need for higher throughput and tighter tolerances drives investment in these adaptive solutions. Early adopters report measurable reductions in scrap rates and faster cycle times, positioning the technology as a key enabler for competitive additive‑manufacturing operations.

Other Trends

Integration with Smart Factory Initiatives

Industrial smart‑factory platforms are incorporating Iterative learning control modules to synchronize nozzle speed with real‑time sensor feedback. This integration allows dynamic tool‑path adjustments that respond to temperature fluctuations, material viscosity changes, and unexpected mechanical deviations. Companies such as ABB have embedded ILC functionality into collaborative arms, enabling seamless communication with cloud‑based analytics and predictive maintenance systems. The result is a closed‑loop ecosystem where data‑driven insights continuously enhance printing accuracy without manual re‑calibration.

Collaborative Robotics and Path Precision

Collaborative robots equipped with Iterative learning control are expanding beyond isolated cell applications to multi‑robot production lines. By sharing learned motion profiles, robots can collectively maintain precise deposition paths even when operating in parallel. This collaborative approach reduces setup time for new part geometries and supports rapid product variation in aerospace, automotive, and medical‑device sectors. The combined effect of shared learning and real‑time adaptation is a noticeable lift in overall equipment effectiveness, reinforcing the strategic importance of the technology within modern manufacturing footprints.

COMPETITIVE LANDSCAPEKey Industry Players

Iterative Learning Control in Robotic 3D Printing: Competitive Overview

The competitive arena for iterative learning control (ILC) in industrial robotic 3D printing is anchored by a handful of robotics OEMs that have embedded ILC modules into their collaborative and heavy‑duty arms. ABB leads the field with its integrated ILC stack for both metal and polymer additive processes, leveraging its extensive service network to capture a disproportionate share of high‑value aerospace and automotive contracts. FANUC and KUKA follow closely, each offering proprietary adaptive trajectory engines that complement their existing motion controllers. Market structure reflects a classic oligopoly: the top three OEMs together account for roughly 55% of total ILC‑enabled printer deployments, while mid‑tier players such as Yaskawa Motoman and Universal Robots compete on flexibility and lower entry‑price points for small‑batch production. The overall market, valued at USD 0.45 billion in 2025, is projected to more than double to USD 1.12 billion by 2034, driven by the 9.5% CAGR and intensified adoption of Industry 4.0 standards.Beyond the dominant hardware manufacturers, niche innovators are shaping specialized segments of the ILC ecosystem. EOS and 3D Systems focus on metal powder‑bed systems where high‑precision ILC reduces residual stress and improves surface finish. DMG Mori and GE Additive provide hybrid solutions that couple ILC with in‑situ monitoring for aerospace‑grade parts. Software‑centric firms such as Siemens, Hexagon Manufacturing Intelligence, and Autodesk supply the algorithmic backbone and digital twins that enable rapid learning cycles across multi‑robot cells. Smaller but technically agile companies like Rockwell Automation and Schneider Electric are integrating ILC into their factory‑automation suites, targeting smart‑factory rollouts in the medical device sector. This layered competitive landscape ensures both breadth of capability and depth of specialization as the market matures.

List of Key Iterative learning control for industrial robotic 3D printing path Companies Profiled

- ABB

- FANUC

- KUKA

- Yaskawa Motoman

- Universal Robots

- DMG Mori

- EOS

- 3D Systems

- GE Additive

- Siemens

- Hexagon Manufacturing Intelligence

- Autodesk

- Rockwell Automation

- Schneider Electric

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Model‑based ILC

|

| By Application |

|

Aerospace component fabrication

|

| By End User |

|

OEM manufacturers

|

| By Technology |

|

Hybrid ILC‑PID control

|

| By Material |

|

Metal alloys

|

Regional Analysis: North America

North America

The North American manufacturing sector is undergoing a significant digital transformation. The need for greater flexibility, faster production cycles, and improved product quality is driving companies to embrace advanced robotic systems. Iterative learning control directly addresses these needs by enabling robots to optimize complex 3D printing processes, enhancing overall manufacturing efficiency and competitiveness. The emphasis on nearshoring and reshoring initiatives further bolsters the demand for advanced automation solutions within the region.

North America boasts a strong ecosystem of materials science research and development. The development of new and improved materials for 3D printing plays a crucial role in the advancement of iterative learning control. Specifically, the availability of advanced polymers, metals, and composites allows for the creation of increasingly complex and functional parts. The ability of iterative learning control to adapt to different material properties is a key driver of its adoption in this market. Collaboration between academic institutions and industrial players accelerates the pace of materials innovation.

The regulatory landscape in North America, particularly concerning safety standards and quality control in manufacturing, is evolving. The need to meet stringent regulations for various industries, such as aerospace and medical devices, is pushing companies to adopt robust and reliable robotic solutions. Iterative learning control contributes to meeting these standards by providing enhanced precision and repeatability in 3D printing processes. Industry-specific standards are also emerging to guide the development and implementation of robotic systems, further shaping the market.

Significant investment is flowing into the robotics and automation sectors across North America. Government initiatives supporting research and development in advanced manufacturing are playing a key role in fostering innovation. Venture capital funding for companies developing iterative learning control algorithms and robotic systems is also on the rise. This financial support is driving the commercialization of new technologies and accelerating market growth. The focus on Industry 4.0 initiatives further encourages investment in advanced robotic solutions.

Europe

Europe represents a strong and mature market for iterative learning control in industrial robotic 3D printing path. The region’s emphasis on sustainable manufacturing and high-quality production aligns well with the capabilities of this technology. Key industries such as automotive, aerospace, and healthcare are actively adopting iterative learning control to enhance their manufacturing processes. Stringent environmental regulations and a focus on circular economy principles drive demand for optimized 3D printing solutions that minimize material waste. The presence of highly skilled engineering talent and a well-established industrial infrastructure provide a solid foundation for continued market growth. Collaboration between research institutions and industrial partners fosters innovation and accelerates the adoption of advanced robotic technologies. The EU’s industrial policy initiatives are also supporting the development and deployment of robotic solutions across the continent.

Asia-Pacific

Asia-Pacific is experiencing rapid growth in Iterative learning control for industrial robotic 3D printing path Market, driven by increasing industrialization and rising demand for customized products. Countries like China, Japan, and South Korea are leading the way in adopting this technology. The region’s robust manufacturing sector, particularly in electronics, automotive, and consumer goods, is fueling demand. The increasing focus on advanced manufacturing and the government’s support for technological innovation are further boosting market growth. The availability of skilled labor and a competitive cost structure are also key advantages for robotic adoption. Furthermore, the demand for lightweight and high-performance components in industries like aerospace and automotive is driving the use of 3D printing and iterative learning control.

South America

South America presents a promising, albeit nascent, market for iterative learning control in industrial robotic 3D printing path. The region’s manufacturing sector is undergoing expansion, particularly in industries like agriculture and mining, which are increasingly adopting advanced automation technologies. The demand for customized parts and efficient production processes is driving the adoption of iterative learning control. Government initiatives aimed at promoting industrial development and attracting foreign investment are also contributing to market growth. While the market is currently smaller than those in North America or Asia-Pacific, the long-term growth potential is significant. Challenges include infrastructure limitations and a need for skilled workforce development.

Middle East & Africa

The Middle East and Africa represent an emerging market for iterative learning control in industrial robotic 3D printing path. The region’s focus on diversification away from oil and gas is driving investment in manufacturing and advanced technologies. The construction, aerospace, and healthcare sectors are key drivers of demand. Government initiatives promoting industrialization and technological advancement are playing a crucial role. The relatively young manufacturing base offers significant potential for growth as industries adopt advanced robotic solutions. Challenges include limited availability of skilled labor and infrastructure development needs. The growing adoption of 3D printing in aerospace and automotive industries is expected to fuel demand for iterative learning control.

Report Scope

This market research report provides a comprehensive analysis of the Iterative learning control for industrial robotic 3D printing path Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Iterative learning control for industrial robotic 3D printing path Market?

-> Iterative learning control for industrial robotic 3D printing path Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 1.12 billion by 2034, exhibiting a CAGR of 9.5%.

Which key companies operate in Iterative learning control for industrial robotic 3D printing path Market?

-> Key players include ABB, FANUC, KUKA, YASKAWA, and DMG MORI, among others.

What are the key growth drivers?

-> Key growth drivers include adoption of Industry 4.0 standards, demand for higher throughput in metal and polymer additive manufacturing, and increasing investments in smart factories.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include integration of ILC modules with collaborative robotic arms, AI‑driven path optimization, and advanced material deposition control for aerospace and medical device applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...