MARKET INSIGHTS

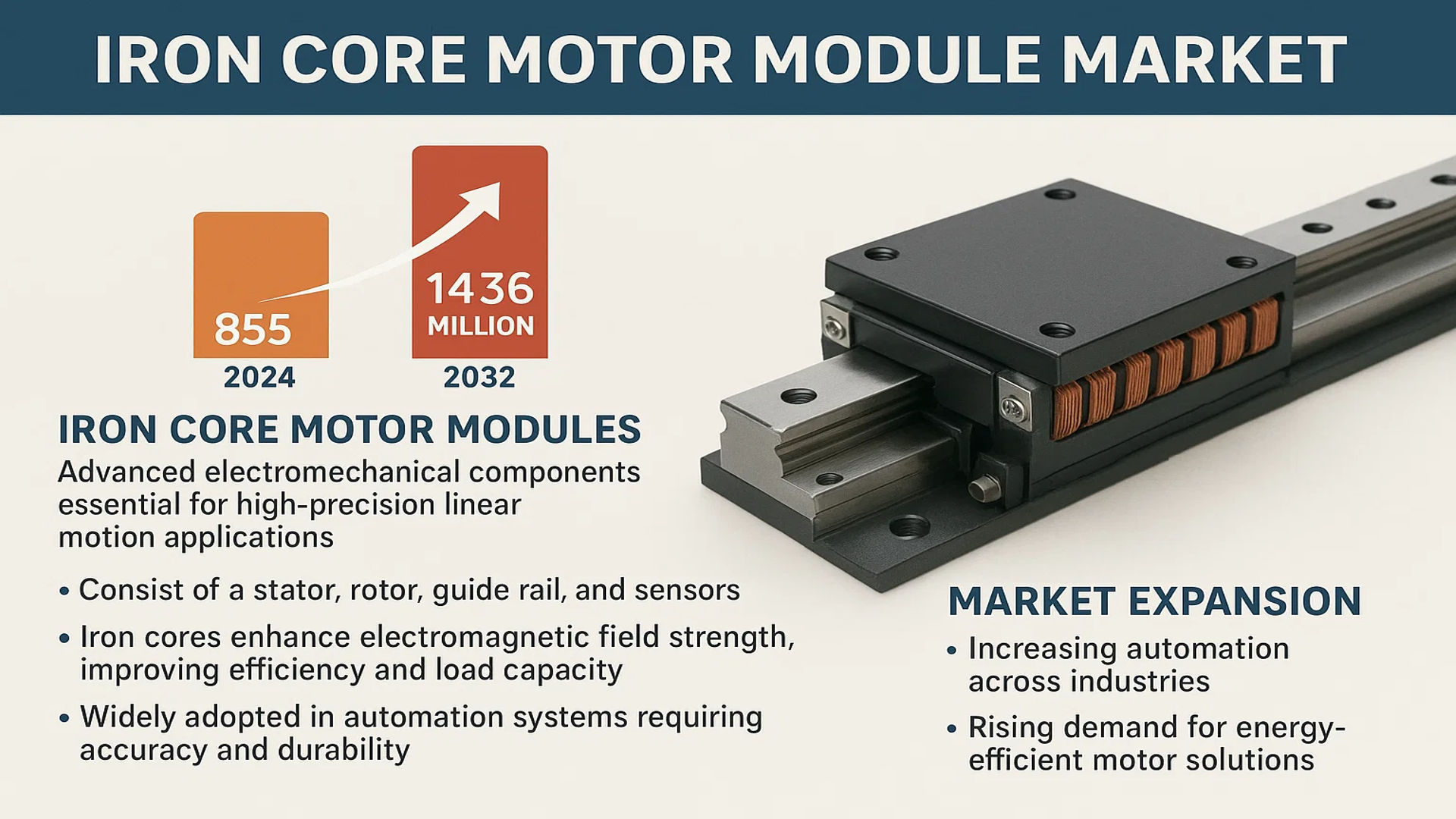

The global Iron Core Motor Module Market was valued at 855 million in 2024 and is projected to reach US$ 1436 million by 2032, at a CAGR of 7.7% during the forecast period.

Iron core motor modules are advanced electromechanical components essential for high-precision linear motion applications. These modules consist of a stator, rotor, guide rail, and sensors, utilizing electromagnetic induction to convert electrical energy into precise linear movement. The inclusion of iron cores significantly enhances electromagnetic field strength, improving motor efficiency and load capacity. They are widely adopted in automation systems requiring exceptional accuracy and durability.

Market expansion is driven by increasing automation across industries such as manufacturing, healthcare, and transportation, coupled with rising demand for energy-efficient motor solutions. The brushless motor segment is gaining traction due to its superior performance and longer lifespan. Key players like Siemens, ABB, and Yaskawa Electric are investing in R&D to enhance product capabilities, further propelling market growth. Additionally, rapid industrialization in emerging economies presents lucrative opportunities for market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Industrial Automation Boom to Accelerate Iron Core Motor Module Demand

The global surge in industrial automation adoption is significantly propelling the iron core motor module market forward. As manufacturing sectors worldwide embrace Industry 4.0 technologies, the requirement for precision motion control systems has intensified. Iron core motors offer superior performance in high-load applications compared to traditional motors, with torque outputs exceeding 30% higher in similar form factors. The robotics sector alone is expected to drive over 40% of global demand, particularly in material handling and assembly line applications where iron core motors’ high force density proves essential. Recent advances in direct drive linear motion systems have further enhanced efficiency, with leading manufacturers now achieving positional accuracy within ±5 microns.

Energy Efficiency Regulations to Stimulate Market Growth

Stringent global energy efficiency standards are compelling manufacturers to transition from conventional motors to advanced iron core brushless modules. These motors demonstrate 15-20% higher energy efficiency compared to traditional brushed alternatives, translating to substantial operational cost savings. The International Electrotechnical Commission’s latest IE4 efficiency classification has accelerated adoption, particularly in European and North American markets where regulatory pressures are strongest. Additionally, the reduced cogging torque characteristic of optimized iron core designs minimizes energy losses during partial load operation – a critical advantage in variable speed applications that constitute nearly 60% of industrial motor usage.

Medical Equipment Miniaturization to Create New Application Areas

The healthcare industry’s push towards compact, high-precision medical devices is opening new frontiers for iron core motor modules. These motors are proving indispensable in surgical robotics, imaging systems and laboratory automation where space constraints demand maximum power density. Recent innovations have yielded iron core modules with power-to-weight ratios exceeding 1kW/kg – a capability revolutionizing portable medical equipment design. The growing adoption of robotic-assisted surgery, projected to maintain 22% CAGR through 2030, particularly benefits from the rapid response times and precision positioning enabled by advanced iron core servo motors.

MARKET RESTRAINTS

Intense Price Competition from Alternative Technologies to Limit Market Expansion

The iron core motor module market faces formidable competition from emerging linear motor technologies, particularly in cost-sensitive applications. Coreless linear motors, while offering lower force density, provide superior acceleration characteristics and are gaining traction in high-speed automation. This competition exerts downward price pressure, with some sectors seeing 20-25% cost differentials between iron core and alternative solutions. The automotive industry’s shift toward integrated motor-drive units further compounds this challenge, as manufacturers increasingly favor compact, low-cost solutions over modular designs.

Thermal Management Challenges in High-Density Applications

Iron core motors’ superior power density comes with inherent thermal constraints that limit performance in continuous operation scenarios. The iron laminations, while enhancing magnetic flux, also create significant eddy current losses – particularly problematic in applications requiring sustained operation at over 70% rated load. Advanced cooling solutions can add 15-30% to system costs, reducing cost competitiveness in price-sensitive markets. This thermal limitation has prompted some industries to opt for alternative technologies despite iron core motors’ superior torque characteristics.

MARKET CHALLENGES

Supply Chain Vulnerabilities for Rare Earth Magnets Threaten Market Stability

The iron core motor industry faces significant material sourcing challenges, with over 80% of rare earth elements required for high-performance magnets originating from limited geographic regions. Recent geopolitical tensions have caused price volatility exceeding 300% for key materials like neodymium. This volatility dramatically impacts production costs and forces manufacturers to either absorb margins or implement frequent price adjustments – both scenarios creating friction in customer adoption cycles.

Integration Complexity in Legacy Systems

Retrofitting iron core motor modules into existing industrial equipment often requires substantial system redesign, creating adoption barriers. The comprehensive drive electronics and sophisticated control algorithms needed for optimal performance can increase total implementation costs by 40-60% compared to traditional motor solutions. This integration challenge is particularly acute in developing markets where modernization budgets remain constrained.

MARKET OPPORTUNITIES

Emerging Robotics Applications to Drive Next Growth Phase

The rapidly evolving field of collaborative robotics presents substantial opportunities for iron core motor advancement. The unique combination of compact size, high torque density and precise controllability makes these motors ideal for next-generation cobot joints and end-effectors. Market projections indicate the collaborative robotics sector will require over 1.2 million precision motor units annually by 2026 – representing a largely untapped market segment for iron core technology providers.

Smart Manufacturing Initiatives Creating Demand for Intelligent Motor Solutions

The integration of IoT capabilities into motion control systems is creating premium opportunities for intelligent iron core motor modules. Modern smart factories increasingly demand motors with integrated condition monitoring, predictive maintenance features and networked control – capabilities that align perfectly with iron core technology’s inherent precision. Early adopters implementing these smart motor solutions report 30-50% reductions in unplanned downtime, creating compelling value propositions for broader industrial adoption.

IRON CORE MOTOR MODULE MARKET TRENDS

Automation and Industry 4.0 Integration Driving Market Expansion

The rapid adoption of automation across manufacturing and industrial applications is fueling demand for high-performance iron core motor modules. With a projected CAGR of 7.7%, this market is being propelled by Industry 4.0 initiatives that require precise motion control in robotic assembly lines and smart factories. These modules offer superior torque density and thermal efficiency compared to coreless alternatives, making them ideal for heavy-duty CNC machines and automated material handling systems that dominate modern production facilities. The growing need for energy-efficient industrial automation is prompting manufacturers to develop iron core solutions with up to 95% operational efficiency.

Other Trends

Medical Robotics Revolution

Specialized iron core motor modules are becoming critical components in advanced medical equipment, particularly in surgical robotics and diagnostic imaging systems. The healthcare sector’s shift toward miniaturized, high-torque motion solutions has led to the development of ultra-compact iron core modules with position accuracy under 5 microns. As robotic-assisted surgeries increase by approximately 18% annually, motor suppliers are focusing on sterilization-compatible designs that meet stringent FDA and CE medical device requirements.

Transportation Electrification Creating New Demand

The global push toward electric mobility is generating innovative applications for iron core motor modules in electric vehicle drivetrains and charging systems. Automakers increasingly utilize these modules in battery cooling pumps and automated charging arms due to their high power density and vibration resistance. With EV production expected to grow at 25% CAGR through 2030, motor manufacturers are developing specialized modules capable of withstanding extreme temperature fluctuations between -40°C to 150°C while maintaining consistent torque output.

Emerging APAC Manufacturing Hubs

Asia-Pacific has emerged as the fastest-growing market, accounting for over 45% of global iron core motor module demand. China’s position as the world’s manufacturing center, combined with aggressive automation investments in South Korea and Japan’s robotics leadership, is driving localized production of motor modules. Regional players are gaining market share through innovative modular designs that reduce installation time by up to 30% compared to conventional solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Drive Innovation in High-Precision Automation Solutions

The global Iron Core Motor Module market is characterized by a mix of multinational conglomerates and specialized manufacturers competing through technological differentiation. As of 2024, Siemens and ABB collectively hold over 25% of the market share, primarily due to their comprehensive automation solutions portfolios and extensive service networks across industrial clusters worldwide. This dominance is further reinforced by their vertical integration capabilities, from motor design to complete motion control systems.

Meanwhile, Japanese powerhouse Yaskawa Electric has been gaining traction through its specialized offerings in robotics-integrated motor modules, particularly in high-speed packaging and semiconductor manufacturing applications. Their recent innovations in energy-efficient brushless motor modules have positioned them as a preferred supplier for eco-conscious manufacturers. Similarly, Bosch has strengthened its market position through strategic collaborations with automotive OEMs, where iron core modules are increasingly replacing traditional hydraulic systems.

The competitive intensity is further heightened by emerging Chinese players like Delta Electronics and Shenzhen Fgs Mechanical Electrical Equipment, which compete aggressively on price-performance ratios. These regional specialists have been capturing market share in cost-sensitive segments while gradually improving their technological capabilities through increased R&D investments – estimated to grow at 12-15% annually through 2032.

List of Key Iron Core Motor Module Manufacturers

- Siemens AG (Germany)

- ABB Ltd (Switzerland)

- Yaskawa Electric Corporation (Japan)

- Robert Bosch GmbH (Germany)

- Schneider Electric SE (France)

- Parker Hannifin Corporation (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Fanuc Corporation (Japan)

- Moog Inc. (U.S.)

- Delta Electronics (Taiwan)

- Omron Corporation (Japan)

- Aimega Motion Technology (China)

- Shenzhen Fgs Mechanical Electrical Equipment (China)

- CCTL Linear Motion Technology (China)

- MBYS Precision Machinery (China)

Segment Analysis:

By Type

Brushless Motor Module Segment Dominates Due to Energy Efficiency and Low Maintenance Needs

The market is segmented based on type into:

- Brushed Motor Module

- Subtypes: Single-phase, Three-phase, and others

- Brushless Motor Module

- Subtypes: PMSM, BLDC, and others

By Application

Industrial Production Leads the Market Due to High Adoption in Automation Systems

The market is segmented based on application into:

- Industrial Production

- Sub-categories: Robotics, CNC Machines, Conveyor Systems

- Medical Equipment

- Sub-categories: Surgical Robots, Diagnostic Machines

- Transportation

- Military Research

- Others

By End User

Manufacturing Sector Holds Major Share Due to Rising Automation Investments

The market is segmented based on end user into:

- Automotive Industry

- Electronics & Semiconductor

- Healthcare Sector

- Aerospace & Defense

- Others

By Power Rating

High Power Modules Drive Market Growth in Heavy Industrial Applications

The market is segmented based on power rating into:

- Low Power (<1 kW)

- Medium Power (1-10 kW)

- High Power (>10 kW)

Regional Analysis: Iron Core Motor Module Market

Asia-Pacific

The Asia-Pacific region dominates the global iron core motor module market, driven by rapid industrial automation and strong manufacturing expansion across China, Japan, and South Korea. China alone accounts for over 40% of the regional market share due to its vast electronics and automotive industries, where iron core motors are widely used in robotics and precision manufacturing equipment. Government initiatives like Made in China 2025 further accelerate adoption, prioritizing high-efficiency motor technologies. A robust semiconductor supply chain and cost-competitive production capabilities solidify the region’s leadership, though rising labor costs and trade tensions present long-term challenges.

North America

North America’s market thrives on technological innovation and high demand for automation in aerospace, defense, and medical sectors. The U.S. leads with significant R&D investments, particularly in brushless iron core motor modules for military and electric vehicle applications. Stricter energy-efficiency standards, such as DOE regulations, push manufacturers toward advanced designs. However, reliance on imports for raw materials like rare-earth magnets creates supply chain vulnerabilities. Collaborations between firms like Parker Hannifin and academic institutions aim to mitigate these risks through localized production and material recycling initiatives.

Europe

Europe’s focus on sustainability and Industry 4.0 adoption fuels demand for energy-efficient iron core motor modules, especially in Germany and Italy’s automotive sectors. EU directives on motor efficiency (e.g., IE4 standards) mandate the use of premium-class motors, driving retrofits in existing industrial systems. Siemens and ABB lead in developing modular solutions for smart factories, integrating IoT capabilities for predictive maintenance. Despite these advancements, market growth is tempered by high production costs and competition from Asian manufacturers offering lower-priced alternatives.

South America

The market in South America remains nascent but shows potential in Brazil’s agribusiness and mining sectors, where iron core motors enhance heavy machinery performance. Economic instability and underdeveloped infrastructure, however, limit large-scale deployments. Local manufacturers face challenges in scaling production due to limited access to advanced components, relying heavily on imports from Asia and North America. Strategic partnerships with global players could unlock growth, particularly in renewable energy projects requiring reliable motor systems.

Middle East & Africa

Growth in this region is uneven, with the UAE and Saudi Arabia spearheading adoption through industrial diversification programs like Vision 2030. Oil and gas applications dominate, utilizing rugged iron core modules for drilling and pipeline operations. While urbanization drives demand for automated solutions, geopolitical risks and underinvestment in R&D hinder technological uptake. Emerging opportunities lie in desalination plants and solar energy infrastructure, where motor efficiency is critical for operational cost reduction.

Report Scope

This market research report provides a comprehensive analysis of the Global Iron Core Motor Module Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Brushed Motor Module, Brushless Motor Module), application (Industrial Production, Medical Equipment, Transportation, Military Research, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, motor efficiency improvements, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Iron Core Motor Module Market?

-> Iron Core Motor Module Market was valued at 855 million in 2024 and is projected to reach US$ 1436 million by 2032, at a CAGR of 7.7% during the forecast period.

Which key companies operate in Global Iron Core Motor Module Market?

-> Key players include Siemens, ABB, Yaskawa Electric, Bosch, Schneider Electric, Parker Hannifin, Mitsubishi Electric Corporation, Fanuc Corporation, Moog, and Delta, among others.

What are the key growth drivers?

-> Key growth drivers include increasing automation in industrial applications, demand for high-precision motion control, and growth in medical equipment manufacturing.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by manufacturing expansion in China and Japan, while North America maintains significant market share.

What are the emerging trends?

-> Emerging trends include integration of smart sensors, development of energy-efficient motor modules, and adoption in robotics applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...