MARKET INSIGHTS

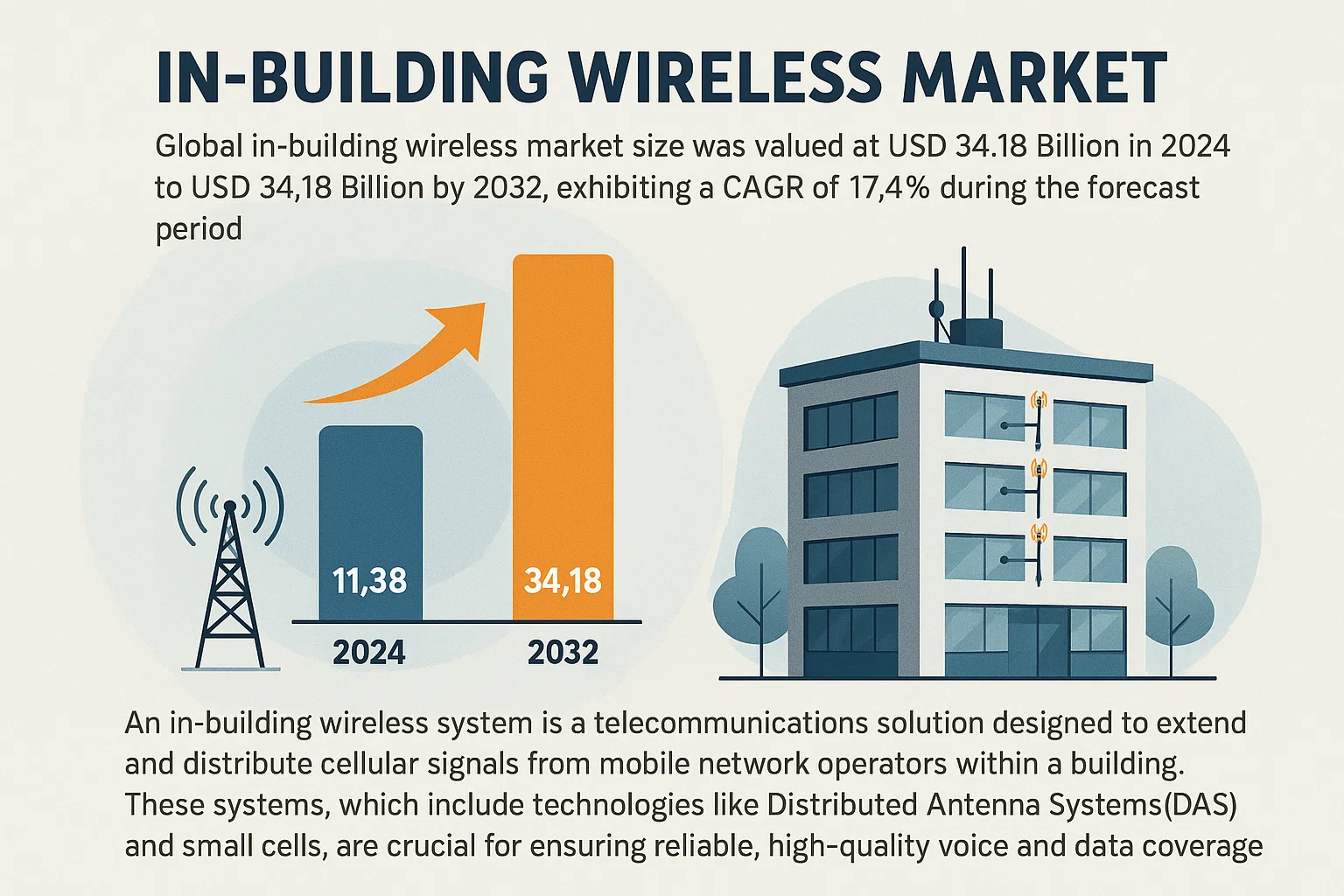

Global In-Building Wireless Market size was valued at USD 11.38 billion in 2024 to USD 34.18 billion by 2032, exhibiting a CAGR of 17.4% during the forecast period.

An in-building wireless system is a telecommunications solution designed to extend and distribute cellular signals from mobile network operators within a building. These systems, which include technologies like Distributed Antenna Systems (DAS) and small cells, are crucial for ensuring reliable, high-quality voice and data coverage in indoor environments where traditional macro network signals often fail to penetrate effectively.

The market is experiencing robust growth driven by the escalating demand for seamless mobile connectivity, the proliferation of smart devices, and the rapid adoption of 5G technology. Furthermore, the surge in construction of large commercial complexes, airports, and stadiums, which require robust indoor coverage, is significantly contributing to market expansion. The competitive landscape is concentrated, with the top five manufacturers—including CommScope, Corning Incorporated, and Ericsson—collectively holding nearly 70% of the global market share, underscoring the high level of industry consolidation.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of 5G Networks and IoT Devices to Accelerate Market Expansion

The global rollout of 5G technology represents a fundamental driver for the in-building wireless market. 5G networks, while offering significantly higher data speeds and lower latency, face challenges with signal penetration through building materials. This inherent characteristic necessitates robust in-building solutions to ensure seamless connectivity. The number of global 5G connections is projected to exceed 1.9 billion by the end of 2024, creating immense pressure on network operators and enterprises to enhance indoor coverage. Furthermore, the explosive growth of Internet of Things (IoT) devices, estimated to surpass 29 billion active endpoints globally, demands reliable and ubiquitous wireless connectivity within commercial, industrial, and residential buildings for applications ranging from smart building automation to asset tracking. This convergence of 5G deployment and IoT proliferation is a primary catalyst for market growth.

Rising Demand for Enhanced Mobile Experience in Commercial Real Estate

There is a growing, non-negotiable expectation for flawless cellular coverage within modern commercial buildings. Property owners and facility managers now view reliable in-building wireless systems as a critical utility, akin to electricity and water, essential for tenant satisfaction, retention, and property valuation. In sectors such as corporate offices, retail complexes, and healthcare facilities, poor cellular reception can directly impact productivity, customer experience, and even emergency communication capabilities. Consequently, investments in Distributed Antenna Systems (DAS) and small cells are increasingly becoming a standard part of building infrastructure planning and development, driven by the need to meet user expectations and maintain competitive advantage in the real estate market.

Increasing Public Safety Communication Mandates to Fuel Regulatory Adoption

Stringent government regulations and building codes mandating reliable public safety communication systems within large structures are significantly propelling the market. Many jurisdictions now require buildings over a certain size or with specific occupancy levels to install systems that ensure first responders have uninterrupted radio communication during emergencies. These regulations are a critical factor, particularly in North America and Europe, compelling building owners to deploy in-building wireless solutions that support emergency responder radio coverage. This regulatory push transforms the market from a luxury enhancement to a compliance necessity, ensuring a steady stream of demand from the government, transportation, and large commercial sectors.

MARKET RESTRAINTS

High Capital and Operational Expenditures to Hinder Widespread Deployment

The significant initial investment required for designing, installing, and commissioning in-building wireless systems, particularly active DAS, acts as a major restraint. These systems involve substantial costs for components, specialized engineering, and labor, which can be prohibitive for small and medium-sized enterprises or buildings with budget constraints. Furthermore, the ongoing operational expenses for power, maintenance, and potential upgrades add to the total cost of ownership. This financial barrier often leads to prolonged decision-making cycles and can deter investment, especially in price-sensitive markets and older buildings where retrofitting presents additional structural and logistical challenges.

Technical Complexities in System Design and Integration to Slow Market Penetration

Designing an effective in-building wireless network is a highly complex process that requires meticulous planning to account for a building’s unique architecture, construction materials, and existing infrastructure. The integration of these systems with multiple mobile network operators (MNOs) to ensure carrier neutrality often involves complex negotiations and technical coordination, creating delays. Moreover, the need to support a multitude of frequency bands for 4G, 5G, and public safety communications increases the system’s technical sophistication. This complexity necessitates highly skilled RF engineers and technicians, and any shortcomings in the design or installation phase can lead to suboptimal performance, creating reluctance among potential adopters.

Spectrum Allocation and Regulatory Hurdles to Create Implementation Challenges

The management and allocation of radio frequency spectrum present ongoing challenges for the deployment of in-building wireless solutions. Regulatory bodies govern the use of spectrum, and the process of obtaining necessary approvals can be time-consuming and vary significantly by region. The advent of 5G introduces new spectrum bands, such as C-band and mmWave, which behave differently indoors and require new approaches to system design. Navigating these regulatory frameworks and ensuring compliance with evolving spectrum policies adds a layer of uncertainty and potential delay for projects, acting as a restraint on faster market growth.

MARKET CHALLENGES

Ensuring Future-Proofing and Technology Scalability Poses a Significant Challenge

The rapid pace of technological evolution in wireless standards presents a formidable challenge for the in-building wireless market. A system deployed today must be scalable and adaptable to accommodate future technologies and increased network demands without requiring a complete and costly overhaul. The transition from 4G to 5G, and eventually to future generations, requires solutions that are inherently flexible. This challenge of future-proofing investments makes selecting the right technology and architecture critical, as building owners and operators seek to avoid obsolescence and protect their long-term capital investments in infrastructure.

Other Challenges

Multi-Operator Coordination

Achieving consensus and coordination among multiple, often competing, mobile network operators for the deployment of a neutral-host DAS is a persistent challenge. Aligning technical requirements, commercial agreements, and deployment schedules can be a protracted process, often slowing down project timelines and increasing complexity for the building owner or system integrator.

Powering and Backhaul Constraints

Providing adequate power and fiber backhaul to often remotely located equipment units within a building, especially for active DAS, can be logistically and financially challenging. Ensuring uninterrupted power supply and sufficient bandwidth capacity to handle growing data traffic is essential for system performance but can be difficult to achieve in certain building environments.

MARKET OPPORTUNITIES

Emergence of Private Cellular Networks and Industry 4.0 to Unlock New Verticals

The rise of private LTE and 5G networks for enterprises represents a substantial growth opportunity. Industries such as manufacturing, logistics, ports, and mining are increasingly deploying their own dedicated cellular networks to support mission-critical applications, industrial IoT, and automation. These private networks require tailored in-building and in-campus wireless solutions to ensure secure, reliable, and high-performance connectivity for robotics, automated guided vehicles, and real-time data analytics. This shift towards Industry 4.0 opens up entirely new vertical markets beyond traditional commercial real estate, driving demand for specialized industrial-grade in-building wireless systems.

Adoption of Open RAN and Neutral-Host Models to Democratize Market Access

The growing industry momentum behind Open Radio Access Network (Open RAN) architectures presents a significant opportunity to reduce costs and increase flexibility. Open RAN promotes interoperability between hardware and software from different vendors, which can lower barriers to entry and foster innovation. Coupled with the neutral-host business model, where a third party builds and operates the network for multiple MNOs, these trends can make in-building wireless solutions more affordable and accessible for a wider range of venues, including mid-sized buildings and public spaces that were previously underserved.

Integration with Smart Building Systems to Create Value-Added Services

The convergence of in-building wireless infrastructure with broader smart building management systems creates a compelling opportunity. The same DAS or small cell infrastructure can be leveraged to support a wide array of building IoT sensors for occupancy monitoring, environmental control, energy management, and security. This integration allows building operators to derive additional value from their wireless investment, transforming it from a cost center into a platform that enhances operational efficiency, sustainability, and occupant experience. This value-added proposition is becoming a key differentiator and driver for new installations.

IN-BUILDING WIRELESS MARKET TRENDS

5G Network Integration Emerges as a Primary Market Driver

The global rollout of 5G networks is fundamentally reshaping the in-building wireless landscape, creating unprecedented demand for robust indoor coverage solutions. While 5G offers significantly higher data speeds and lower latency, its higher frequency bands—particularly millimeter wave—face substantial penetration challenges through building materials. This physical limitation necessitates sophisticated in-building systems to ensure reliable connectivity. The market has responded with advanced Distributed Antenna Systems (DAS) and small cells specifically engineered for 5G frequencies. Commercial real estate developers now consider 5G readiness as a standard building requirement, with premium office spaces and retail complexes investing heavily in future-proof infrastructure. The transition to 5G is not merely about faster downloads; it enables transformative applications like augmented reality in retail, real-time IoT monitoring in manufacturing, and ultra-high-definition video conferencing in corporate environments, all of which depend on flawless indoor wireless performance.

Other Trends

Enterprise Digital Transformation Acceleration

The accelerated pace of enterprise digital transformation across all sectors continues to drive substantial investment in in-building wireless infrastructure. Organizations are deploying comprehensive wireless solutions to support cloud migration, IoT device proliferation, and mobile workforce requirements. The commercial segment, which holds over 65% market share, demonstrates particularly strong adoption as businesses recognize that reliable wireless connectivity directly impacts operational efficiency and customer experience. Modern office designs increasingly favor wireless connectivity over traditional wired infrastructure, reducing installation costs while increasing flexibility. Furthermore, the industrial sector’s adoption of Industry 4.0 principles has created demand for specialized wireless systems that can withstand harsh environments while supporting critical automation and monitoring applications. This trend reflects a broader shift toward wireless-first operational models across multiple industries.

Convergence of IT and Operational Technology Networks

A significant trend reshaping the market involves the convergence of traditionally separate IT and operational technology (OT) networks within enterprise environments. Organizations are implementing unified in-building wireless solutions that serve both employee connectivity needs and operational requirements such as building automation, security systems, and environmental monitoring. This convergence creates efficiency gains and cost reductions while enabling data sharing across previously siloed systems. The integration often requires specialized expertise in both telecommunications and building management systems, leading to increased collaboration between network providers and facility management companies. This trend is particularly evident in smart building projects where a single wireless infrastructure might support everything from HVAC control to security cameras and employee Wi-Fi, creating more responsive and efficient building environments while optimizing infrastructure investments.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus on Technological Innovation and Strategic Alliances to Maintain Market Position

The global In-Building Wireless market exhibits a semi-consolidated structure, characterized by the presence of both multinational corporations and specialized niche players. CommScope and Corning Incorporated collectively dominate a substantial portion of the market, leveraging their extensive product portfolios and established relationships with mobile network operators globally. Their leadership is reinforced by continuous investment in research and development, particularly in Distributed Antenna Systems (DAS) and small cell technologies, which remain critical to indoor coverage solutions.

Ericsson and Huawei also command significant market shares, driven by their end-to-end capabilities in network infrastructure and strong foothold across diverse geographic regions. Ericsson’s focus on 5G-ready solutions and Huawei’s expansive presence in the Asia-Pacific region contribute notably to their competitive standing. Furthermore, these companies actively engage in partnerships with commercial real estate developers and government entities to deploy scalable in-building wireless systems, addressing the growing demand for seamless connectivity.

Strategic initiatives such as mergers, acquisitions, and collaborations are increasingly common as companies aim to expand their technological expertise and geographic reach. For instance, several key players have recently acquired smaller firms specializing in IoT integration and neutral-host solutions, enabling them to offer more comprehensive services. Additionally, advancements in energy-efficient systems and support for multi-operator environments are becoming focal points, reflecting the industry’s shift towards sustainable and flexible infrastructure.

Meanwhile, emerging players like JMA Wireless and Dali Wireless are gaining traction through innovative, software-defined solutions that offer greater flexibility and cost-efficiency. Their growth is supported by targeted investments in R&D and strategic entry into high-growth markets, particularly in North America and Asia-Pacific. These dynamics indicate a competitive environment where agility and technological differentiation are crucial for long-term success.

List of Key In-Building Wireless Companies Profiled

- CommScope (U.S.)

- Corning Incorporated (U.S.)

- AT&T (U.S.)

- Ericsson (Sweden)

- Cobham (U.K.)

- TE Connectivity (Switzerland)

- Nokia (Alcatel-Lucent) (Finland)

- Huawei (China)

- Anixter (WESCO International, Inc.) (U.S.)

- Infinite Electronics Inc (U.S.)

- JMA Wireless (U.S.)

- Oberon Inc (U.S.)

- Dali Wireless (Canada)

- Betacom Incorporated (U.S.)

- Lord & Company Technologies (U.S.)

Segment Analysis:

By Type

DAS Segment Dominates the Market Due to Superior Coverage and Reliability in Large Facilities

The market is segmented based on type into:

- DAS (Distributed Antenna Systems)

- Small Cells

- Repeaters

- Other Enabling Technologies

By Application

Commercial Segment Leads Due to Growing Need for Seamless Connectivity in Business Environments

The market is segmented based on application into:

- Commercial

- Industrial

- Government

- Transportation

- Others

By End-User

Enterprise Facilities Account for Largest Adoption Due to Digital Transformation Initiatives

The market is segmented based on end-user into:

- Enterprise Facilities

- Hospitals and Healthcare

- Hospitality

- Education Institutions

- Others

By Service

Managed Services Gaining Traction as Organizations Outsource Network Management

The market is segmented based on service into:

- Managed Services

- Professional Services

- Installation and Integration

Global In-Building Wireless Market: Regional Analysis

North America

The North American market continues to lead globally with a market share exceeding 40%, driven by massive infrastructure investments and rapid 5G deployment. The United States alone has allocated over $42 billion through various federal programs specifically targeting network infrastructure modernization, creating immense demand for distributed antenna systems (DAS) and small cell solutions. Canada’s growing smart city initiatives and Mexico’s increasing urban development projects further contribute to regional dominance. The region benefits from strong regulatory frameworks ensuring public safety communication systems in all major commercial buildings.

Europe

European markets demonstrate robust growth with particular strength in Western Europe. Germany leads with its Industry 4.0 initiatives and extensive 5G rollout across manufacturing facilities, while the UK remains strong in healthcare and commercial infrastructure upgrades. The EU’s Digital Agenda and various national broadband initiatives drive demand for in-building wireless solutions, particularly in countries like France, Germany, and the Nordics. Eastern European markets show promising growth rates as they catch up with Western counterparts in digital infrastructure development.

Asia-Pacific

The Asia-Pacific region represents the fastest-growing market with China and India leading the expansion. China’s massive infrastructure development and digital transformation initiatives account for approximately 35% of regional market activity. India follows closely with its Digital India campaign and rapid urban development. Japan and South Korea continue to innovate with advanced manufacturing and smart city projects. Southeast Asian nations show accelerating adoption rates as they develop their digital infrastructure, with countries like Vietnam and Indonesia showing particularly strong growth in recent years.

Rest of World

Emerging markets across South America, Middle East, and Africa demonstrate varying growth patterns. Brazil leads South American markets with large-scale infrastructure projects in major cities. Middle Eastern countries, particularly UAE and Saudi Arabia, show significant investment in smart city technologies and commercial infrastructure. African markets present both challenges and opportunities, with South Africa and Nigeria showing the most consistent growth in urban centers, while infrastructure development across the continent remains uneven but steadily improving.

Report Scope

This market research report provides a comprehensive analysis of the global and regional in-building wireless markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global In-Building Wireless Market?

->In-Building Wireless Market size was valued at USD 11.38 billion in 2024 to USD 34.18 billion by 2032, exhibiting a CAGR of 17.4% during the forecast period.

Which key companies operate in Global In-Building Wireless Market?

-> Key players include CommScope, Corning Incorporated, AT&T, Ericsson, Cobham, TE Connectivity, Alcatel-Lucent, Huawei, and Anixter, among others.

What are the key growth drivers?

-> Key growth drivers include 5G network deployments, smart building infrastructure, IoT connectivity demands, and increasing mobile data consumption.

Which region dominates the market?

-> North America holds the largest market share at approximately 40%, while Asia-Pacific is the fastest-growing region with increasing investments in smart infrastructure.

What are the emerging trends?

-> Emerging trends include integrated DAS and small cell solutions, edge computing integration, AI-driven network optimization, and sustainable building connectivity solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...