HPC Processor Market Insights

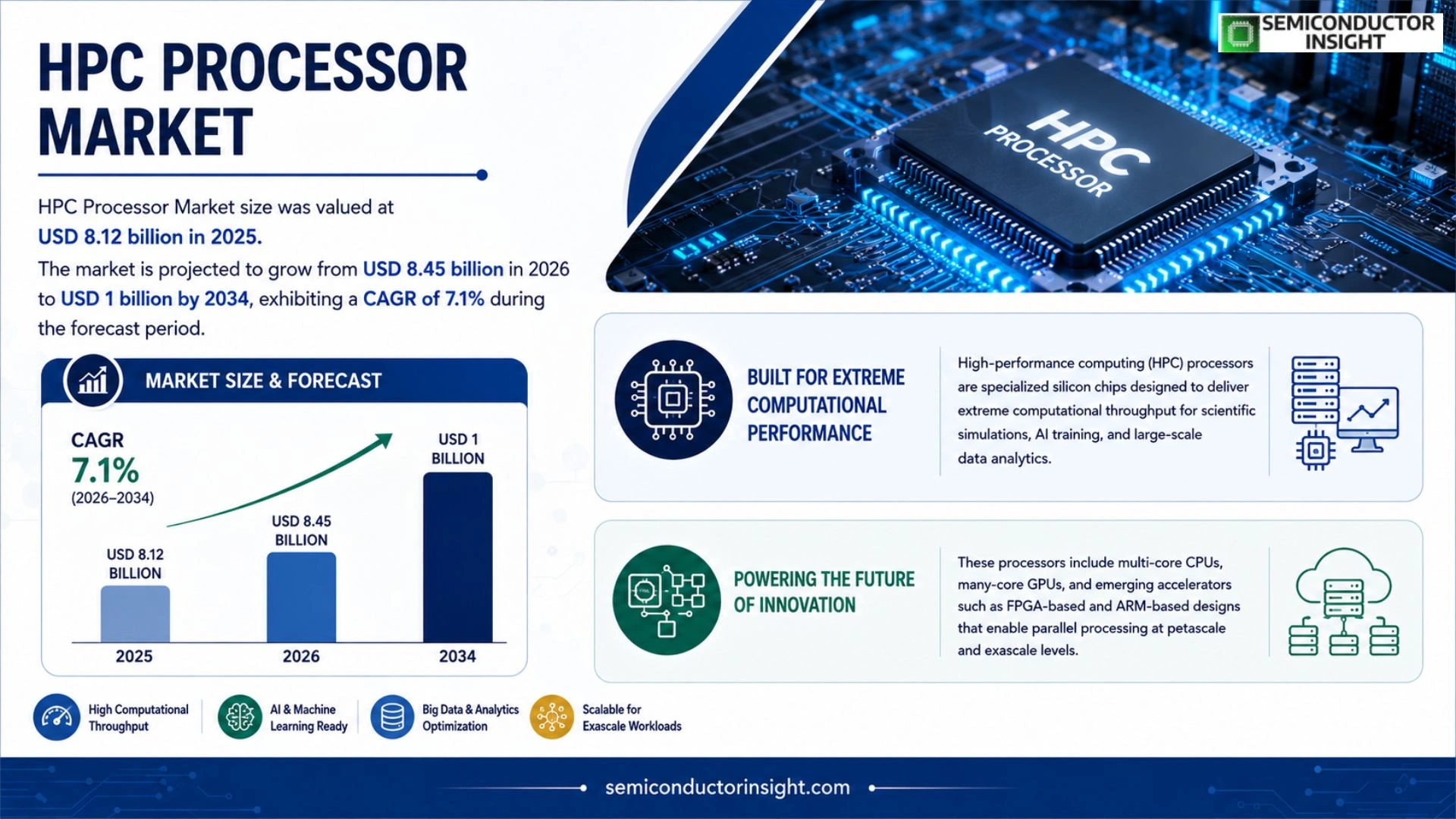

Global HPC Processor Market size was valued at USD 8.12 billion in 2025. The market is projected to grow from 5.73 USD 8.45 billion in 2026 to USD 1billion by 2034, exhibiting a CAGR of 7.1% during the forecast period.

High‑performance computing (HPC) processors are specialized silicon chips designed to deliver extreme computational throughput for scientific simulations, AI training, and large‑scale data analytics. These processors include multi‑core CPUs, many‑core GPUs, and emerging accelerators such as FPGA‑based and ARM‑based designs that enable parallel processing at petascale and exascale levels.

The market is experiencing rapid growth due to several factors, including rising investment in supercomputing infrastructure, increasing demand for AI‑driven workloads, and governmental initiatives toward exascale computing milestones. Furthermore, advancements in semiconductor manufacturing nodes and the shift toward heterogeneous architectures are driving adoption across research institutions and cloud providers. Key players such as Intel, AMD, NVIDIA, IBM, and ARM are actively expanding their portfolios through strategic partnerships and technology roadmaps.

MARKET DRIVERS

Rising Demand for AI‑Driven Workloads

HPC Processor Market is being propelled by an unprecedented surge in artificial‑intelligence and machine‑learning applications across scientific research, finance, and autonomous systems. Organizations are investing heavily in processors that can deliver petaflop‑scale performance while maintaining energy efficiency, leading to a compound annual growth rate projected above 12% through 2032.

Expansion of Cloud‑Based HPC Services

Leading cloud providers are expanding their high‑performance computing portfolios, offering on‑demand access to cutting‑edge processors. This shift lowers capital expenditure barriers for enterprises, driving broader adoption of HPC Processor Market and creating a virtuous cycle of demand for next‑generation silicon.

➤ According to industry surveys, 68% of firms plan to upgrade their HPC infrastructure within the next 18 months to support AI workloads.

In parallel, governmental initiatives targeting climate modeling, drug discovery, and national security are allocating substantial budgets to modernize supercomputing facilities, further amplifying the growth trajectory of HPC Processor Market.

MARKET CHALLENGES

Supply Chain Bottlenecks for Advanced Lithography

The transition to sub‑5 nm process nodes hinges on scarce lithography equipment, leading to production delays for cutting‑edge HPC processors. These constraints elevate component costs and compress profit margins for system integrators.

Other Challenges

Thermal Management Limits

High‑performance chips generate substantial heat, requiring sophisticated cooling solutions that increase total ownership cost and limit deployment in edge environments.

MARKET RESTRAINTS

Elevated Power Consumption

While performance gains are impressive, many new HPC processors draw upwards of 300 W per socket, constraining data‑center operators who must balance compute density with energy budgets. This power envelope acts as a restraint on wider market penetration.

MARKET OPPORTUNITIES

Emergence of ARM‑Based HPC Architectures

ARM’s low‑power, high‑core‑count designs are gaining traction as viable alternatives to traditional x86 solutions. Early adopters report up to 30% lower energy per operation, presenting a compelling value proposition that could reshape HPC Processor Market landscape over the next decade.

HPC Processor Market Trends

Rise of Heterogeneous Architectures

HPC Processor Market is increasingly defined by heterogeneous system designs that combine high‑core‑count CPUs with many‑core GPUs and specialized accelerators. This architectural shift enables parallel execution of diverse workloads, from scientific simulations to AI model training, while optimizing power and performance envelopes. Leading vendors are integrating ARM‑based designs and FPGA accelerators into single compute nodes, allowing researchers to target petascale performance without resorting to monolithic processor solutions. The trend is reinforced by advances in semiconductor nodes that deliver higher transistor density, making it feasible to embed multiple processor types on one package. As a result, system builders are adopting modular stacks that can be reconfigured for specific application profiles, accelerating time‑to‑insight across research institutions and cloud platforms.

Other Trends

AI‑Driven Workload Expansion

Artificial‑intelligence workloads are a primary catalyst for growth HPC Processor Market. Deep‑learning training cycles demand massive matrix operations, which are efficiently handled by many‑core GPUs and emerging AI‑optimized accelerators. Institutions are upgrading their supercomputing clusters to include dedicated AI inference engines, reducing latency for real‑time analytics. This demand also pushes software ecosystems toward unified programming models that abstract the underlying hardware diversity, enabling developers to leverage both CPUs and accelerators without extensive code rewrites. The convergence of AI and traditional HPC tasks is prompting vendors to deliver integrated solutions that balance double‑precision scientific computing with tensor‑focused AI performance, delivering greater utilization across mixed‑workload environments.

Edge and Cloud Integration

Another notable development is the migration of high‑performance compute capabilities to edge devices and public‑cloud offerings. Enterprises are deploying compact HPC nodes at the network edge to process data locally, minimizing bandwidth costs and meeting strict latency requirements for applications such as autonomous systems and real‑time analytics. Simultaneously, cloud providers are expanding their catalog of HPC‑optimized instances, offering on‑demand access to the latest processor architectures without capital expenditure. This dual‑path strategy broadens the reach of high‑performance solutions, allowing smaller organizations to benefit from cutting‑edge processor technology while large‑scale research facilities continue to scale out traditional data‑center deployments.

COMPETITIVE LANDSCAPE

Key Industry Players

HPC Processor Market Competitive Landscape Overview

HPC Processor Market is anchored by a few dominant vendors that shape the overall architecture roadmap. Intel remains the principal supplier of high‑core‑count CPUs, leveraging its Xeon Scalable family and the upcoming Sapphire Rapids generation to deliver memory‑centric performance for large‑scale simulations. AMD has captured significant share with its EPYC processors and the Instinct GPU line, offering competitive price‑performance and native support for heterogeneous computing. NVIDIA leads the accelerator segment through its CUDA‑enabled GPUs, such as the A100 and H100, which dominate AI‑driven HPC workloads and exascale initiatives. IBM contributes niche expertise with Power9 and Power10 CPUs tailored for enterprise‑grade supercomputers, while ARM provides energy‑efficient designs increasingly adopted in modular clusters. Collectively, these leaders drive a market size projected to reach $15.73 billion by 2034, propelled by investments in exascale projects, cloud‑based HPC services, and advances in semiconductor process nodes. The convergence toward heterogeneous compute stacks, combining CPUs, GPUs, and custom accelerators, intensifies cooperation and competition among these vendors.

Beyond the primary tier, a constellation of niche and emerging players enriches the competitive landscape with specialized IP and accelerator solutions. Xilinx (now part of AMD) supplies high‑performance FPGA fabrics that enable adaptive workloads and low‑latency interconnects for scientific instruments. Qualcomm’s Snapdragon HPC variants target edge‑centric AI training, while Marvell’s OCTEON and ThunderX platforms deliver ARM‑based servers for hyperscale data centers. Traditional system integrators such as Dell Technologies and Hewlett Packard Enterprise (HPE) bundle CPUs and GPUs into turnkey supercomputing solutions, often partnering with Cray, now a HPE business unit, to provide optimized interconnect fabrics. Japanese firm Fujitsu leverages its A64FX ARM‑based CPU to power the world‑leading Fugaku supercomputer. Chinese manufacturer Huawei continues to push its Kunpeng and Ascend lines despite geopolitical constraints. New‑wave startups,including Cerebras Systems, Graphcore, SambaNova Systems, and Tenstorrent,are introducing wafer‑scale and data‑flow architectures that challenge conventional GPU dominance and promise to reshape future HPC processor portfolios. These diverse offerings stimulate benchmark‑driven innovation, as organizations benchmark against the TOP500 list to validate performance gains.

List of Key HPC Processor Companies Profiled

- Intel Corporation

- Advanced Micro Devices (AMD)

- NVIDIA Corporation

- IBM

- ARM Ltd.

- Xilinx Inc.

- Qualcomm Technologies, Inc.

- Marvell Technology Group Ltd.

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Fujitsu Limited

- Huawei Technologies Co., Ltd.

- Cray Inc.

- Cerebras Systems

- Graphcore Ltd.

- SambaNova Systems

- Tenstorrent Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Many‑core GPUs

|

| By Application |

|

AI model training

|

| By End User |

|

Research institutions

|

| By Architecture |

|

Heterogeneous architectures

|

| By Deployment Mode |

|

Hybrid cloud HPC

|

Regional Analysis: North America

Government funding and strategic initiatives are key drivers for HPC processor adoption in the US, particularly in areas like national security, climate research, and healthcare. This support fuels innovation and creates a stable demand for high-performance computing resources.

The burgeoning AI and data analytics sectors are major catalysts for HPC processor demand, requiring substantial computational power for training complex models and processing massive datasets. This trend is expected to continue, driving further innovation in processor architectures.

The increasing integration of HPC with cloud computing platforms is transforming the market, offering scalability, flexibility, and cost-effectiveness to users. This trend is fostering the development of specialized processors optimized for cloud environments.

Growing concerns about energy consumption are driving a strong focus on energy-efficient processor designs. This trend is prompting manufacturers to develop processors with lower power requirements without compromising performance.

Europe

Europe represents a significant and evolving market for HPC processors. Driven by strong research and development activities across various scientific disciplines – including climate modeling, drug discovery, and materials science – the demand for high-performance computing is steadily increasing. The European Union’s initiatives, such as the EuroHPC Joint Undertaking, are playing a pivotal role in fostering collaboration and accelerating the adoption of HPC technologies. Emphasis is placed on energy efficiency and sustainability, with a growing interest in processors designed for low power consumption. The market is witnessing a shift towards heterogeneous computing architectures, combining CPUs, GPUs, and specialized accelerators to optimize performance for specific workloads. While the US remains a dominant force, European companies are actively innovating and striving to gain market share. Key areas of focus include advancements in exascale computing and the development of processors tailored for AI and machine learning applications. The interconnectedness of European research institutions and industrial partners facilitates knowledge sharing and technological progress, creating a dynamic ecosystem for HPC innovation. The continent’s commitment to data sovereignty and security also influences processor selection and deployment strategies.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing region HPC Processor Market, fueled by rapid industrialization, increasing investments in technology, and a burgeoning research sector. China, in particular, is making significant strides in HPC, with substantial investments in supercomputer infrastructure and AI development. The demand for HPC processors is driven by applications in areas such as manufacturing, finance, and artificial intelligence. The region is witnessing a shift towards localized processor development, with companies striving to reduce reliance on foreign suppliers. The increasing adoption of cloud computing and edge computing is also contributing to the growth of the HPC market. The Asia-Pacific region presents both opportunities and challenges for HPC processor manufacturers, with diverse market needs and varying levels of technological sophistication. The focus on data analytics and machine learning is driving demand for processors optimized for these workloads. Government support for technological advancements and a growing talent pool are key factors contributing to the region’s rapid growth. The competitive landscape is becoming increasingly intense, with both domestic and international players vying for market share.

South America

South America presents a relatively nascent but promising market for HPC processors. Driven primarily by government investments in scientific research and the expansion of data centers, the demand for high-performance computing is slowly growing. Brazil and Argentina are key markets in the region, with increasing adoption of HPC for applications in areas such as oil and gas exploration, agriculture, and weather forecasting. However, the market is still constrained by limited investment capital and a lack of skilled personnel. The increasing availability of cloud computing services is providing an alternative to on-premise HPC infrastructure, which may limit the growth of the processor market. The region faces challenges related to infrastructure development and regulatory uncertainty. Government initiatives to promote technological innovation and digital transformation are expected to boost the demand for HPC processors in the coming years. The focus is shifting towards applications that can leverage HPC for data analysis, modeling, and simulation.

Middle East & Africa

The Middle East and Africa represent a developing market for HPC processors, driven by investments in infrastructure development, government initiatives to promote technological advancement, and increasing demand for data analytics. Countries like Saudi Arabia, the UAE, and South Africa are witnessing growing adoption of HPC for applications in areas such as oil and gas, finance, and healthcare. The expansion of data centers and the increasing use of cloud computing are also contributing to the growth of the HPC market. However, the region faces challenges related to limited investment and a shortage of skilled workforce. Government initiatives to foster innovation and diversify economies are expected to spur demand for HPC processors in the long term. The focus is on leveraging HPC for applications that can improve efficiency, optimize resource utilization, and drive economic growth. The growing adoption of AI and machine learning is expected to further accelerate the demand for HPC in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the HPC Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of HPC Processor Market?

-> Global HPC Processor Market was valued at USD 8.12 billion in 2025 and is expected to reach USD 15.73 billion by 2034, reflecting a projected CAGR of 7.1% over the forecast period.

Which key companies operate HPC Processor Market?

-> Key players include Intel, AMD, NVIDIA, IBM, and ARM, among others.

What are the key growth drivers?

-> Key growth drivers include rising investment in supercomputing infrastructure, increasing demand for AI‑driven workloads, governmental initiatives toward exascale computing, advancements in semiconductor manufacturing nodes, and the shift toward heterogeneous architectures.

Which region dominates the market?

-> Adoption is strong across multiple regions, with especially robust activity in North America, Europe, and Asia‑Pacific, making the market truly global in scope.

What are the emerging trends?

-> Emerging trends include the integration of FPGA‑based and ARM‑based accelerators, development of heterogeneous computing platforms, and continued innovation in energy‑efficient processor designs for petascale and exascale workloads.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...