Silicon Carbide (SiC) Substrate Market Overview

Silicon Carbide (SiC) Substrates for RF Device are usually semi-insulating substrates

This report provides a deep insight into the global Silicon Carbide (SiC) Substrates for RF Device market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Silicon Carbide (SiC) Substrates for RF Device Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Silicon Carbide (SiC) Substrates for RF Device market in any manner.

Silicon Carbide (SiC) Substrate Market Analysis:

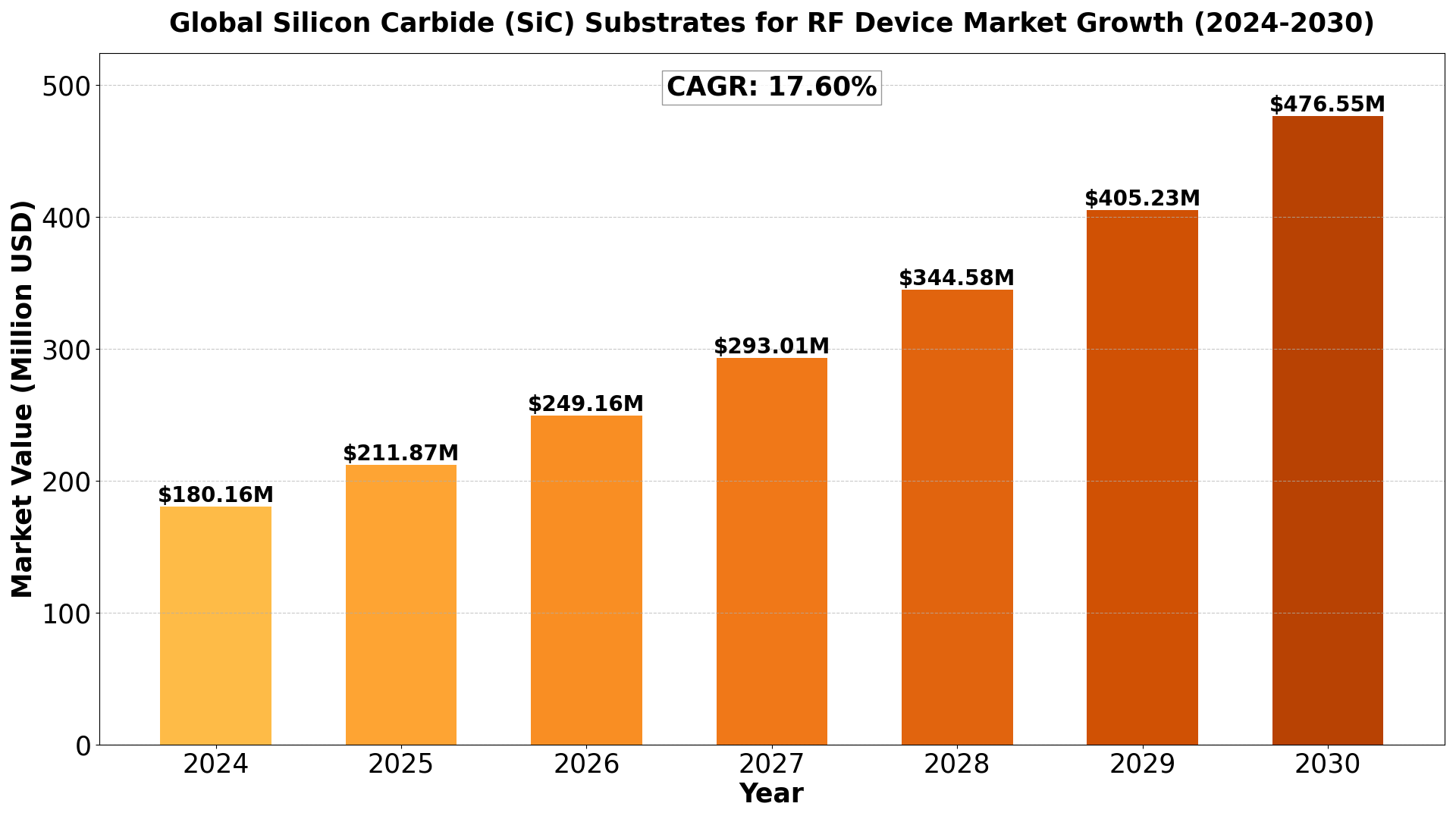

The Global Silicon Carbide (SiC) Substrates for RF Device Market size was estimated at USD 153.20 million in 2023 and is projected to reach USD 476.55 million by 2030, exhibiting a CAGR of 17.60% during the forecast period.

North America Silicon Carbide (SiC) Substrates for RF Device market size was USD 39.92 million in 2023, at a CAGR of 15.09% during the forecast period of 2024 through 2030.

Silicon Carbide (SiC) Substrate Key Market Trends :

- Expansion of 5G Networks: The rollout of 5G technology is one of the major drivers for the demand for SiC substrates in RF devices. SiC-based materials are essential for RF power amplifiers, which are crucial for high-frequency applications in 5G base stations and telecom infrastructure. SiC’s ability to handle high power and high frequency makes it ideal for meeting the performance requirements of 5G communications, driving market growth.

- Increase in Power-Efficient RF Devices: SiC substrates are favored for their high efficiency in power conversion and high thermal conductivity, which is essential for RF devices operating in high-power and high-temperature environments. This makes SiC substrates ideal for applications such as power amplifiers and radar systems, which require efficient energy handling and heat dissipation. As industries focus more on energy-efficient solutions, demand for SiC substrates will continue to rise.

- Demand for High-Power and High-Frequency Applications: SiC substrates are crucial in the development of high-power RF devices used in radar systems, satellite communication, and military applications. These industries require RF devices that can operate at high frequencies and power levels. As military and aerospace sectors continue to invest in advanced communication technologies, the demand for SiC substrates for RF devices is expected to grow.

- Advancements in SiC Manufacturing Technology: As SiC substrate manufacturing technologies improve, they are becoming more cost-effective and scalable. Innovations in crystal growth and wafer production processes are enhancing the quality of SiC substrates and making them more accessible for RF device applications. This trend is contributing to the growth of the market as SiC becomes more affordable and widespread in its adoption across various RF applications.

- Shift Toward Electrification and Renewable Energy Systems: SiC substrates are also used in power electronic systems for renewable energy and electric vehicle infrastructure, including RF devices for energy-efficient communication systems. As global efforts towards electrification and clean energy increase, the need for reliable and high-performance RF components also grows, further driving the demand for SiC-based solutions.

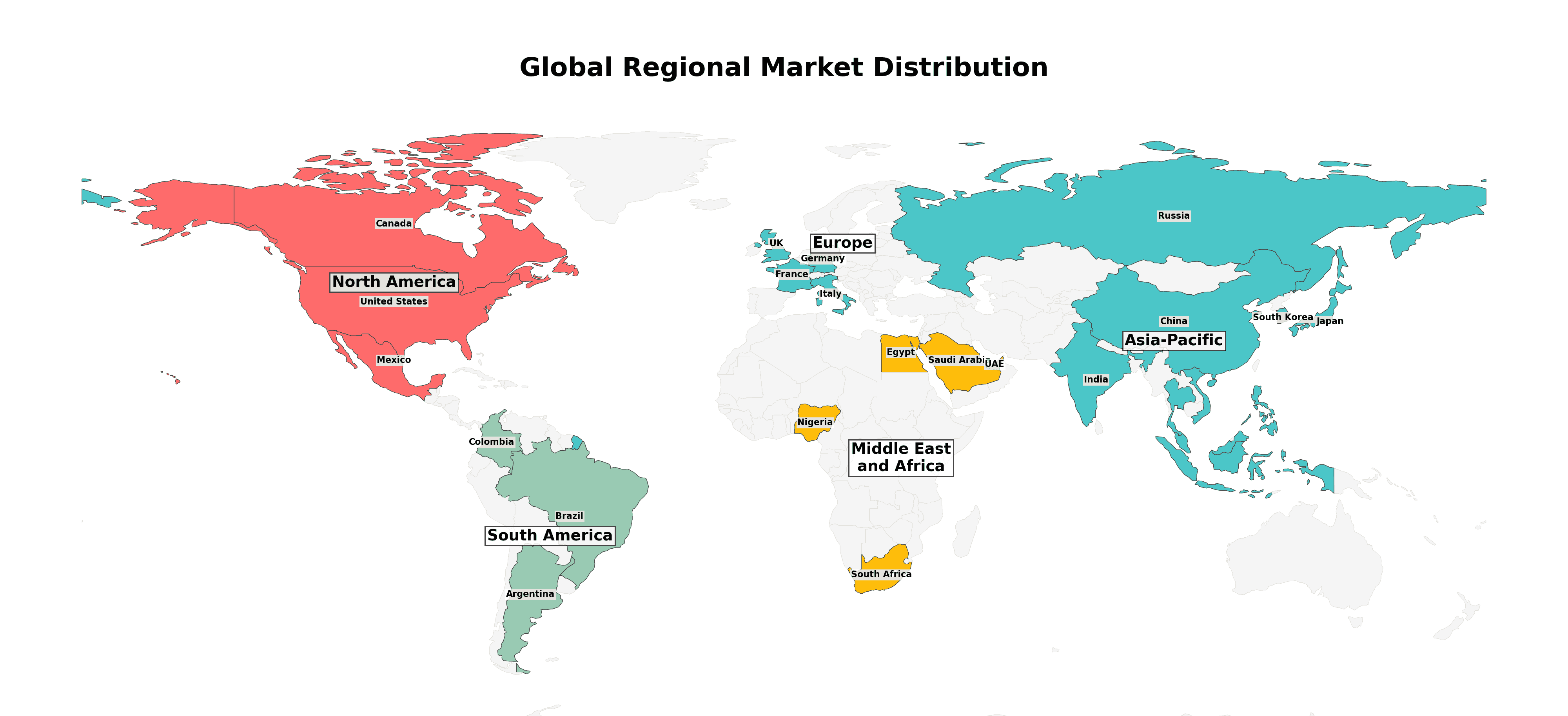

Silicon Carbide (SiC) Substrate Market Regional Analysis :

1. North America (USA, Canada, Mexico)

- USA: The largest market in the region due to advanced infrastructure, high disposable income, and technological advancements. Key industries include technology, healthcare, and manufacturing.

- Canada: Strong market potential driven by resource exports, a stable economy, and government initiatives supporting innovation.

- Mexico: A growing economy with strengths in automotive manufacturing, agriculture, and tourism, benefitting from trade agreements like the USMCA.

2. Europe (Germany, UK, France, Russia, Italy, Rest of Europe)

- Germany: The region’s industrial powerhouse with a focus on engineering, automotive, and machinery.

- UK: A hub for financial services, fintech, and pharmaceuticals, though Brexit has altered trade patterns.

- France: Strong in luxury goods, agriculture, and aerospace with significant innovation in renewable energy.

- Russia: Resource-driven economy with strengths in oil, gas, and minerals but geopolitical tensions affect growth.

- Italy: Known for fashion, design, and manufacturing, especially in luxury segments.

- Rest of Europe: Includes smaller yet significant economies like Spain, Netherlands, and Switzerland with strengths in finance, agriculture, and manufacturing.

3. Asia-Pacific (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific)

- China: The largest market in the region with a focus on technology, manufacturing, and e-commerce. Rapid urbanization and middle-class growth fuel consumption.

- Japan: Technological innovation, particularly in robotics and electronics, drives the economy.

- South Korea: Known for technology, especially in semiconductors and consumer electronics.

- India: Rapidly growing economy with strengths in IT services, agriculture, and pharmaceuticals.

- Southeast Asia: Key markets like Indonesia, Thailand, and Vietnam show growth in manufacturing and tourism.

- Rest of Asia-Pacific: Emerging markets with growing investment in infrastructure and services.

4. South America (Brazil, Argentina, Colombia, Rest of South America)

- Brazil: Largest economy in the region, driven by agriculture, mining, and energy.

- Argentina: Known for agriculture exports and natural resources but faces economic instability.

- Colombia: Growing economy with strengths in oil, coffee, and flowers.

- Rest of South America: Includes Chile and Peru, which have strong mining sectors.

5. The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA)

- Saudi Arabia: Oil-driven economy undergoing diversification with Vision 2030 initiatives.

- UAE: Financial hub with strengths in tourism, real estate, and trade.

- Egypt: Growing infrastructure development and tourism.

- Nigeria: Largest economy in Africa with strengths in oil and agriculture.

- South Africa: Industrialized economy with strengths in mining and finance.

- Rest of MEA: Includes smaller yet resource-rich markets like Qatar and Kenya with growing infrastructure investments.

Silicon Carbide (SiC) Substrate Market Segmentation :

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- Cree (Wolfspeed)

- II?VI Advanced Materials

- SICC Materials

- TankeBlue Semiconductor

- STMicroelectronics (Norstel)

- Hebei Synlight Crystal

- ROHM (sicrystal)

Market Segmentation (by Type)

- 4 Inch

- 6 Inch

- 8 Inch

Market Segmentation (by Application)

- 5G Base Station

- Lidar

- Others

Market Drivers

- Demand for High-Power and High-Frequency Devices SiC substrates are ideal for RF devices because of their high power-handling capabilities and performance at high frequencies. With the increasing demand for high-frequency communication, including 5G and beyond, SiC-based RF devices are becoming essential for base stations, power amplifiers, and RF front-end components. SiC substrates can handle high-power signals with minimal loss, making them highly valuable for modern telecommunications systems.

- Rise of 5G Networks The global rollout of 5G networks is a key driver for the SiC substrates market. 5G networks require RF devices that can operate efficiently at high frequencies (millimeter waves) and with greater power. SiC, with its wide bandgap, allows RF devices to perform well under these demanding conditions, facilitating the deployment of 5G infrastructure, including base stations and communication antennas. SiC’s capability to operate at higher frequencies also supports the development of next-generation RF amplifiers.

- Superior Thermal Management SiC substrates offer better thermal conductivity than traditional semiconductor materials like silicon. This ability to dissipate heat effectively is critical for RF devices that generate high amounts of heat, especially in high-power applications like radar and communications. As RF devices need to maintain stable performance over extended periods, the thermal properties of SiC help enhance the reliability and longevity of the devices.

- Shift to High-Power RF Devices RF power devices are increasingly used in industrial, military, and aerospace applications, where high-power capabilities are needed. SiC substrates enable the development of RF power amplifiers, transmitters, and other components that can handle high power levels while maintaining efficiency and stability. These capabilities make SiC substrates attractive for use in radar systems, satellite communication, and defense electronics.

- Miniaturization of RF Components As demand for smaller, more compact RF components grows, SiC substrates are becoming a viable option. Their high power handling and thermal management capabilities allow manufacturers to develop smaller, more integrated RF components without compromising performance. This trend is particularly relevant in the development of portable electronics, mobile communications, and IoT devices.

Market Restraints

- High Manufacturing Costs The production of SiC substrates is more expensive compared to traditional silicon-based materials. The high cost is primarily due to the complexity of growing SiC crystals and the specialized equipment required for wafer processing. The price of SiC substrates can be a limiting factor for widespread adoption, particularly in cost-sensitive applications.

- Challenges in Wafer Quality and Yield The production of high-quality SiC wafers for RF devices is a complex and delicate process. SiC crystals tend to have defects, such as dislocations or impurities, which can lead to lower yields in wafer production. These defects can impact the performance and reliability of RF devices. Improving the consistency and quality of SiC substrates remains a challenge for manufacturers.

- Limited Availability of Large-Diameter SiC Wafers SiC substrates, especially large-diameter wafers, are still not as widely available as silicon wafers, which limits scalability and mass production. As the demand for SiC-based RF devices grows, there is an ongoing need to increase the availability of large-diameter wafers to support larger-scale manufacturing.

- Competition from Other Materials While SiC is well-suited for high-power, high-frequency RF applications, other materials, such as gallium nitride (GaN) and gallium arsenide (GaAs), also offer similar benefits and are used in RF devices. GaN, in particular, is known for its ability to operate at high frequencies and power levels, and it is a significant competitor to SiC in certain RF applications.

Market Opportunities

- Growth of 5G and Next-Generation Communications The expansion of 5G networks worldwide presents a significant opportunity for SiC substrates in RF devices. As 5G relies on higher frequencies, higher power, and better thermal management, SiC’s properties make it an ideal material for base stations, antennas, and other RF components that support 5G infrastructure. As 5G deployment accelerates, the demand for SiC substrates will increase.

- Military and Aerospace Applications SiC substrates are increasingly used in military and aerospace applications, such as radar, communication systems, and electronic warfare devices. These sectors require RF devices capable of high power, frequency stability, and reliability in harsh environments. SiC’s ability to operate under extreme conditions gives it a competitive edge in these markets.

- Automotive Industry and Radar Systems The automotive sector, particularly for advanced driver-assistance systems (ADAS) and autonomous vehicles, relies heavily on radar systems. These systems require high-frequency, high-power RF devices, making SiC substrates a key material for the development of automotive radar sensors. The growing interest in autonomous vehicles and ADAS is expected to drive further adoption of SiC in automotive applications.

- Satellite Communications Satellite communication systems require highly efficient, high-power RF components, which are essential for transmitting and receiving signals over long distances. SiC substrates are well-suited for use in the development of RF amplifiers and other communication components for satellite systems. As satellite communication continues to grow, especially with the launch of new constellations like Starlink, the demand for SiC-based RF devices is expected to rise.

- Development of Compact, High-Efficiency RF Components As the demand for smaller, more efficient electronic devices grows, SiC substrates offer opportunities for the miniaturization of RF components without sacrificing performance. The ability to integrate SiC RF components into compact systems opens opportunities for new applications in consumer electronics, IoT devices, and wearables.

Market Challenges

- High Capital Investment for Manufacturing Facilities The capital investment required to build and operate facilities for the manufacturing of SiC substrates and RF devices is high. For companies to scale up production, they need to invest in specialized equipment, cleanroom facilities, and high-quality raw materials. These high upfront costs may deter smaller players from entering the market.

- Supply Chain Bottlenecks Due to the relatively niche nature of SiC wafer production, there can be supply chain disruptions, especially during periods of increased demand. Any disruption in the availability of SiC wafers could delay the production of RF devices, impacting overall market growth.

- Material Compatibility and Integration Integrating SiC substrates into existing RF systems requires overcoming material compatibility issues with other semiconductor materials used in device fabrication. The process of combining SiC with other materials, such as metals and dielectrics, can introduce additional technical challenges that need to be addressed during the design and manufacturing stages.

Key Benefits of This Market Research:

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Silicon Carbide (SiC) Substrates for RF Device Market

- Overview of the regional outlook of the Silicon Carbide (SiC) Substrates for RF Device Market:

Key Reasons to Buy this Report:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value (USD Billion) data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

- Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

- Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

- The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

- Includes in-depth analysis of the market from various perspectives through Porters five forces analysis

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

FAQs

Q1: What are Silicon Carbide (SiC) Substrates for RF Devices?

A1: Silicon Carbide (SiC) substrates for RF (Radio Frequency) devices are specialized wafers made from SiC material that are used in high-performance RF power devices. These substrates offer advantages like high thermal conductivity, high power handling, and the ability to operate at high frequencies, making them ideal for applications such as telecommunications and radar systems.

Q2: What is the current market size and forecast for the Silicon Carbide (SiC) Substrates for RF Device Market until 2030?

A2: The global SiC substrates for RF devices market size was USD 153.20 million in 2023 and is projected to reach USD 476.55 million by 2030, exhibiting a CAGR of 17.60% during the forecast period.

Q3: What are the key growth drivers in the Silicon Carbide (SiC) Substrates for RF Device Market?

A3: Key growth drivers include the growing demand for high-performance RF devices, the rise of 5G telecommunications, increased use in radar systems, and the need for high-frequency, high-power devices in applications like military communications, satellite systems, and industrial RF equipment.

Q4: Which regions dominate the Silicon Carbide (SiC) Substrates for RF Device Market?

A4: North America and Asia-Pacific dominate the market, with strong demand from the US, Japan, and China due to advancements in 5G infrastructure, military applications, and semiconductor manufacturing.

Q5: What are the emerging trends in the Silicon Carbide (SiC) Substrates for RF Device Market?

A5: Emerging trends include the growth of 5G networks, the development of next-generation radar and communication systems, and advancements in SiC substrate manufacturing techniques, leading to improved performance and lower costs for high-frequency RF devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...